Gantry Robots Market Size, Share, Growth Trends, Industry Analysis, Key Players, Investment Opportunities and Forecast 2026-2034

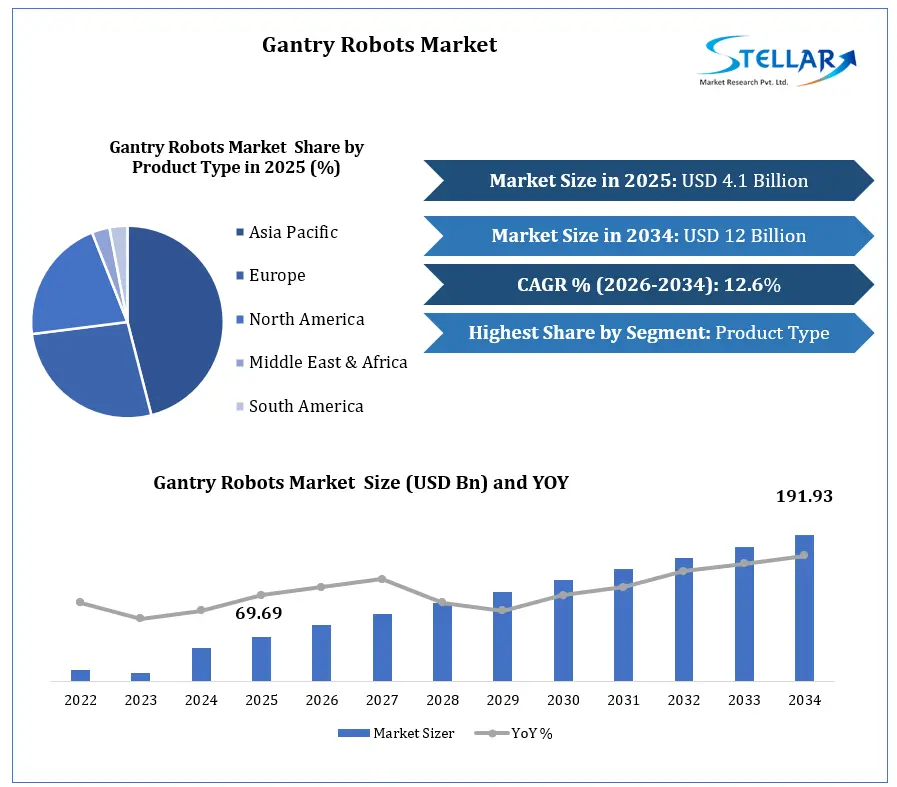

The global gantry robots’ market was valued at USD 4.1 billion in 2025 and is forecast to reach USD 12.0 billion by 2034, at a CAGR of 12.6%.

Industrial automation is no longer optional automotive plants, electronics manufacturers, and logistics operators are all scaling robotic systems to stay competitive. Gantry robots are at the center of that investment, handling material transport, palletizing, machine tending, and high-precision assembly across high-volume production environments. Superior payload capacity, repeatable accuracy, and the ability to integrate with AI-powered control systems and machine vision technology make them a practical, long-term infrastructure choice not just a productivity upgrade.

Gantry Robots Market Overview

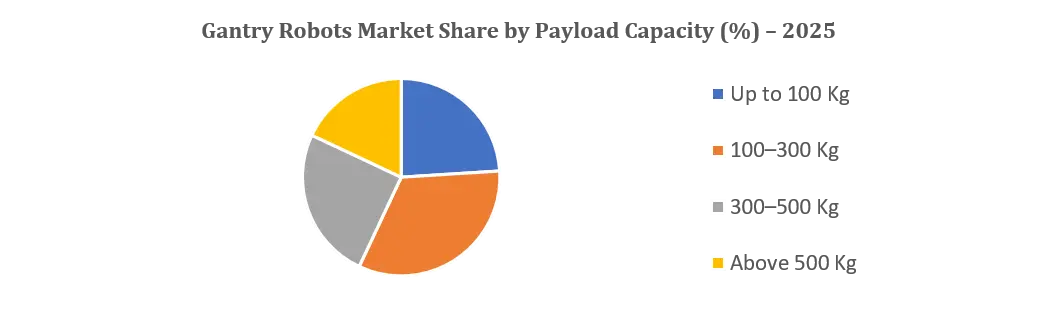

The global gantry robots market was valued at USD 4.1 billion in 2025 and is projected to reach USD 12.0 billion by 2034, growing at a CAGR of 12.6% a trajectory backed by real, compounding demand across industrial automation, warehouse automation, smart manufacturing, and Industry 4.0 adoption. Material handling leads application demand at 34%, followed by palletizing and packaging at 25%, with machine tending, assembly, and welding making up the balance across manufacturing plants and distribution centers. The 100–300 kg payload segment dominates at 33%, covering the widest range of industrial jobs from automotive lines to packaging systems, while the 300–500 kg and above-500 kg brackets serve heavy industry and aerospace where unit value and precision requirements are exceptionally high this is too much ai

To get more Insights: Request Free Sample Report

Gantry Robots Market Dynamics

Gantry Robots Market Drivers

Gantry Robots Expand With Automated Warehousing and Enhanced Manufacturing

The rapid growth of warehouse automation, manufacturing smart factories, and e-commerce fulfillment centers has fueled the demand for gantry robots. Greater investment in robotic material handling, automated sortation and palletizing, and AI-enabled warehouse technologies has further spurred the demand for gantry robots designed for high-speed and high-precision logistics.

NEOintralogistics highlighted the need for automation solutions that can decrease operating costs by 65% and the need for warehouse labor personnel by 70% when they received €3 million in funding to develop their automation solutions in January 2026.

J-Elephant received strategic investment from Geek+ in June 2026. This grants J-Elephant the ability to deploy pallet warehouse automation across more than 40 countries and a high-density pallet storage system using VPR technology. All of these advancements directly correlate with a greater need to innovate warehouse and manufacturing facility automation, which, in turn, increases the demand for gantry robots.

Increasing Investment for Semiconductor and Electronics Manufacturing

Economic activities to build semiconductor fabrication and electronics assembly infrastructure along with sophisticated chip manufacturing and quantum computing infrastructure are fueling the demand for high-precision gantry robots. These robots are essential for cleanrooms and are critical for wafer handling, automated transportation of materials, and PCB fabrication, assembly, and inspection tasks, among others. The demand for assembly gantry robots is also growing due to the capability of the systems to minimize the risks of contamination within the manufacturing environment, increase productivity, and especially, optimize the manufacturing process.

In October 2025, the Indian government allocated ?55 billion (USD 626 million) to seven electronics manufacturing projects to build facilities to make PCBs, camera modules, and other electronic components.

On May 2026, U.S. Department of Commerce announced USD 2.013 billion under the CHIPS Act to advance quantum and semiconductor manufacturing, which included USD 1 billion to IBM and USD 375 million to GlobalFoundries. More advanced manufacturing systems under these contracts lead to greater demand for gantry robots to carry wafers and perform precision assembly and material handling for high throughput manufacturing.

Rise of Industry 4.0 and Smart Factory Automation

The combination of Industry 4.0, smart factories, and digital manufacturing is adding momentum to the deployment of gantry robots. To improve manufacturing efficiency, lower labor costs, and gain greater flexibility in production, manufacturers are incorporating AI-based robotics along with machine vision and automated workflows.

High Demand for Gantry Robots with Greater Payload Capacity

The increased level of automation in the automotive and heavy machinery and metal fabrication sectors is driving the need for high-payload gantry robots. Precision and reliability in handling large and heavy components are critical to most modern industrial operations.

Growth of Automotive Manufacturing Automation

The increased investment in building automotive manufacturing plants, particularly to support the production of electric vehicles (EVs), as well as advances in the automation of automotive assembly, is driving the need for gantry robots. Gantry robots are commonplace for handling, assembly automation, welding, and the transportation of manufacturing materials and tools.

Gantry Robots Market Opportunities

Growth in E-Commerce Logistics Infrastructure

The e-commerce and omnichannel retail sectors are growing rapidly, and companies invest in automated warehouses, distribution centers and fulfillment hubs. Gantry robots are being used more frequently for palletizing, transporting, packaging and high-speed sorting of goods, offering opportunities for manufacturers in the logistics automation market sector.

Semiconductor Manufacturing Market Drives Increased Use

The expansion of semiconductor manufacturing plants and electronic manufacturing centers demands greater use of highly precise gantry robot systems. Wafer handling, component handling and automation of cleanrooms all lead to gains in production efficiency, uptime, precision and reliability which in turn helps manufacturers to improve production efficiency and reduce operational costs.

AI-Enabled Gantry Robots Open New Opportunities for Growth

With the advancement of artificial intelligence (AI), machine vision and analytics, gantry robots are becoming more autonomous and intelligent. AI-enabled gantry robots can leverage real-time data to optimize the work flow, enhance object detection accuracy and predictive maintenance, and help operators in making better decisions, ultimately opening new opportunities for manufacturers in advanced manufacturing and industrial automation.Gantry Robots

Gantry Robots Market Restraints

High initial capital investment

Getting a gantry robot system up and running costs more than just the hardware. You're looking at automation software, sensors, machine vision systems, control units, facility modifications, installation, and staff training all before the first production cycle runs. For large manufacturers, that's a manageable investment with a clear ROI path. For small and mid-sized businesses, it's a real barrier. Budget constraints and longer payback periods mean many SMEs are still on the sidelines, particularly in cost-sensitive industries and developing markets where automation adoption is still building momentum.

Shortage of skilled workforce and technical expertise

The robots are getting smarter but finding people who can deploy, program, and maintain them is getting harder. Demand for qualified robotics engineers, automation specialists, and maintenance technicians is outpacing supply across most industrial markets. When the right expertise isn't available, implementation timelines stretch, operational costs climb, and systems run below their actual capability. This gap hits hardest in emerging economies, where industrial automation is expanding quickly but workforce development hasn't kept pace creating a real bottleneck for full-scale gantry robot deployment.

Gantry Robots Market Trends

AI-powered robotics and machine vision integration

AI and machine vision are no longer add-ons they're becoming standard in how gantry robots are built and sold. The ability to detect objects, catch defects mid-line, and adjust movement without stopping production is something manufacturers across automotive and electronics simply can't ignore anymore. It saves time, cuts waste, and removes a lot of the guesswork that used to require human oversight.

Growth of robotic palletizing solutions

More warehouses and factories are turning to gantry robots for palletizing because the business case is hard to argue with. You get faster throughput, fewer errors, and you're not dependent on shift schedules or labor availability. In food & beverage and logistics especially, where margins are tight and volumes are high, this kind of consistency has real dollar value.

Digital twin and predictive maintenance adoption

Nobody wants a robot going down mid-shift with no warning. That's why more manufacturers are pairing their gantry systems with digital twin software and predictive maintenance tools so they can spot a problem before it becomes a stoppage. It extends equipment life, keeps utilization high, and gives operations teams actual visibility instead of just reacting when something breaks.

Gantry Robots Market Segmentation 2025

By Payload Capacity

The 100–300 kg segment ran the show in 2025, pulling in 33% of the market. Why? Because that payload range fits the widest range of real industrial jobs automotive lines, warehouse floors, packaging systems. It's not too heavy, not too light, and it handles volume without breaking a sweat. At 25%, the 300–500 kg bracket is where heavy industry lives. Big facilities running steel, bulk components, or large assemblies aren't experimenting with automation anymore they're scaling it. The up-to-100 kg segment at 24% is quietly closing the gap. Electronics and precision assembly don't need muscle they need accuracy and speed, and lighter gantry systems are delivering exactly that as those industries keep growing.

Above 500 kg sits at 18% the smallest slice, but don't mistake that for low value. Aerospace, shipbuilding, and heavy fabrication operate at a scale where one robot replaces significant manual risk and labor cost. Fewer buyers, bigger contracts, long-term commitments. The overall picture is clear: payload demand is spread across the board, but the mid-range is where the volume is and that's where competition is heating up fastest.

By Application

Material handling took the top spot at 34%, and it makes complete sense. Moving things loading, unloading, shifting materials across a plant or warehouse floor is where the volume is. Gantry robots do it faster, safer, and without shift changes. Palletizing and packaging came in at 25%. E-commerce and high-speed fulfillment have put serious pressure on output speed, and businesses that automated this early are already seeing the payoff in throughput and consistency. Machine tending at 16% reflects a quieter but steady trend factories don't want skilled workers babysitting CNC machines. Gantry robots take over that job reliably, freeing people for work that actually needs human judgment. Assembly operations held 13%. Automotive and electronics are the main drivers here, and as product complexity grows, so does the case for robotic precision over manual assembly. Welding and inspection round it out at 12% smaller share, but high-stakes work. Accuracy here directly affects product quality and safety, which is exactly why automation is gaining ground fast.

By End-Use Industry

Automotive leads at 29%, and it's been the backbone of industrial robotics for decades. Assembly lines, welding bays, body component handling gantry robots are woven into every stage of modern vehicle production. Electronics and semiconductors follow at 23%. This is precision-critical, cleanroom-compatible automation. As chip demand climbs and tolerances tighten, there's no room for human error and the investment reflects that. Logistics and warehousing at 18% is the fastest-moving story in the group. Fulfillment centers are scaling at a pace that manual labor simply can't match. Automated distribution hubs are no longer a competitive advantage they're becoming the baseline. Food and beverage at 12% is driven by hygiene standards, packaging speed, and the push to reduce contamination risk. Robots don't get tired, don't call in sick, and don't touch what they're not supposed to. Aerospace and heavy machinery hold 10% low volume, high precision, massive unit value. One deployment here can justify the ROI many times over. The remaining 8% across other industries signals that adoption is spreading well beyond the traditional strongholds. The market is broadening, not just deepening.

Gantry Robots Market Reginal Analysis:

Asia-Pacific 42% Regional market leader

The gantry robot industry has a clear leader in the Asia-Pacific region, which has a market share of 42%. This is by far the largest market share of any region in the world. Major drivers of industrial automation in the Asia-Pacific are China's large-scale expansion of smart factory infrastructure and automated production lines in sectors like automotive, electronics and heavy manufacturing; Japan and South Korea's world-class robotics ecosystems developed through decades of precise manufacturing; and India's rapid development through government-led initiatives to support Industry 4.0 and advanced manufacturing processes that are promoting faster adoption of gantry robots into previously manual industries. The Asia-Pacific region has an unbeatable combination of high-volume production, governmental support in the form of favourable policies and the growing capacity for semiconductor/electronics manufacturing that will continue making it the primary regional growth area for gantry robots.

Europe 27% Mature market, sustained investment

With 27% market share of the world's gantry robots, Europe has one of the strongest industrial robotics ecosystems in place. Germany, Italy and France are still the principal markets driving demand through ongoing investments in automation solutions across automotive manufacturing, aerospace engineering and precision industrial production. The emphasis on flexible manufacturing methods, efficient operations and delivering high-value output has driven consistent and purposeful investments into robotics throughout Europe. Europe is not a region of volume production but rather is focused on producing quality output; thus, gantry robots play an integral role in their efforts to achieve this goal.

North America's Share = 23% The rise of smart manufacturing continues

North America represents 23% of the global gantry robot market; the United States is leading adoption of gantry robots within warehouse automation, robotic material handling, semiconductor manufacturing and e-commerce fulfilment infrastructure. As a result of labour shortages, increased operational costs and increasing logistics requirements, the rate at which companies are automating has increased significantly since the onset of the pandemic. Investment in smart manufacturing technology and automated distribution centres is on the rise across the continent and there is no indication of this trend slowing. That said, the growth of the gantry robot market in North America is not just about expansion; it is also about a fundamental shift in the structure of how companies rely on automation over the long term.

Latin America 5% Emerging automation market

Latin America holds approximately 5% of the global gantry robots market, with Brazil and Mexico leading regional industrial modernization efforts. Automotive assembly operations and expanding manufacturing automation investments are gradually building the foundation for broader gantry robot adoption. Infrastructure gaps and slower industrial digitization have kept adoption below developed market levels, but improving industrial infrastructure and rising demand for operational efficiency are creating real commercial opportunity. For companies with a long-term regional strategy, Latin America represents an early-mover advantage worth acting on now.

Middle East & Africa 3% High-potential frontier market

The Middle East and Africa account for 3% of the global market the smallest share, but one with meaningful upside. Gulf Cooperation Council (GCC) countries are actively investing in logistics infrastructure, automated warehousing, and smart manufacturing projects as part of broader economic diversification agendas. High dependence on manual labor, combined with rising demand for industrial efficiency and operational consistency, makes the business case for gantry robot deployment increasingly compelling. Early-stage adoption is underway, and as industrial diversification accelerates across the region, the market is positioned for steady, long-term expansion.

Gantry Robots Market Recent Market Developments

On June 2025, ABB Ltd. launched the Flexley Mover P603, an AI-powered autonomous mobile robot (AMR) capable of handling payloads up to 1,500 kg. The platform integrates AI-driven Visual SLAM navigation and advanced robotics software to enhance intralogistics, warehouse automation, and material handling operations, reflecting the growing demand for intelligent robotic systems in industrial environments.

On March 2025, FANUC Corporation showcased its latest automated warehouse and logistics solutions at ProMat 2025, featuring advanced robotic palletizing, depalletizing, AI-powered vision systems, and warehouse automation technologies designed to improve throughput and operational efficiency in distribution centers.

On May 2025, FANUC Corporation introduced the new M-710iD Series industrial robots, designed for material handling, assembly, palletizing, machine tending, and welding applications. The next-generation platform offers enhanced performance, improved payload capabilities, and greater flexibility for automated manufacturing operations.

On June 2025, FANUC Corporation released ROBOGUIDE Version 10, its next-generation robot simulation and offline programming software featuring virtual reality capabilities, enhanced CAD integration, and improved digital twin functionality. The software helps manufacturers optimize robotic workcells and accelerate automation deployment.

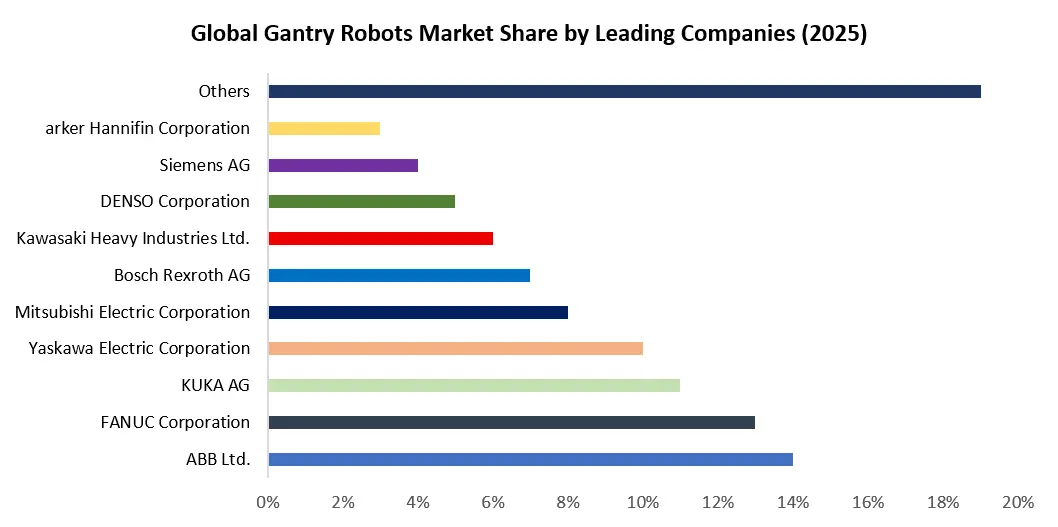

Key Players Analysis of the Gantry Robots Market

Competition levels in the Gantry Robots Market are fierce, with the dominant international industrial automation companies being ABB Ltd., FANUC Corporation, KUKA AG, Yaskawa Electric Corporation, Mitsubishi Electric, and Bosch Rexroth. Each company has built itself a strong foothold within the market through their extensive range of products and global distribution channels and are continually investing in developing new technologies related to industrial automation. Companies are also focusing on using Artificial Intelligence to assist with powering robots, integrating machine vision with their robotics systems, utilizing digital twin technologies to create accurate models of the manufacturing process, providing smart factory solutions, and creating advanced material handling systems. Companies see a direct correlation between the increasing demand for warehouse automation, automotive manufacturing robots, semiconductor manufacturing, and applications requiring high payloads using robotic systems and therefore have expanded their offerings of gantry-style robots in order to strengthen their market presence in key verticals. In addition, these companies utilize technological innovations, form strategic alliances and partnerships, and invest resources into developing next-generation robotic systems to continue to grow and evolve the global market for gantry-style robots.

|

Gantry Robots Market |

||||

|

Report Coverage |

Details |

|

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2034 |

|

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 4.1 Bn. |

|

|

Forecast Period 2026 to 2034 CAGR: |

12.6% |

Market Size in 2034: |

USD 12 Bn. |

|

|

Segments

|

By Collaborative Type |

|

|

|

|

By Collaborative Tools |

|

|

||

|

By Payload Capacity |

|

|

||

|

|

By Application

|

|

|

|

|

|

By End User |

|

|

|

Gantry Robots Market Recent Market Key Players

- ABB Ltd.

- FANUC Corporation

- KUKA AG

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Bosch Rexroth AG

- Kawasaki Heavy Industries Ltd.

- DENSO Corporation

- Siemens AG

- Parker Hannifin Corporation

- OMRON Corporation

- Stäubli International AG

- Epson Robots

- Universal Robots A/S

- Festo SE & Co. KG

- Schneider Electric SE

- IAI Corporation

- Güdel Group AG

- Aerotech Inc.

- HIWIN Technologies Corp.

- Sintelon Intelligent Equipment Co., Ltd.

- Yamaha Motor Co., Ltd.

- NACHI-FUJIKOSHI Corp.

- Beckhoff Automation GmbH & Co. KG

- Rockwell Automation, Inc.

Frequently Asked Questions

The market is projected to reach approximately USD 12.00 Billion by 2034, growing at a CAGR of 12.6% during the forecast period from 2026 to 2034.

The 100–300 Kg payload capacity segment holds the largest market share, accounting for approximately 33% of the market in 2025, owing to its extensive use in automotive manufacturing, packaging, and material handling applications.

Material Handling is the leading application segment, representing approximately 34% of the market in 2025 due to growing automation across manufacturing facilities, warehouses, and distribution centers.

Key growth drivers include the expansion of warehouse automation, increasing adoption of Industry 4.0 and smart factory technologies, rising demand for high-payload material handling systems, growth in e-commerce fulfillment centers, and advancements in AI-powered robotics and machine vision technologies.

- Gantry Robots Market Introduction

1.1. Study Assumption and Market Definition

1.2. Scope of the Study

1.3. Executive Summary - Gantry Robots Market: Competitive Landscape

2.1. SMR Competition Matrix

2.2. Key Players Benchmarking

2.2.1. Company Name

2.2.2. Headquarter

2.2.3. Product Segment

2.2.4. End-User Segment

2.2.5. Revenue Details in 2025

2.2.6. Market Share (%)

2.2.7. Growth Rate (%)

2.2.8. Distribution Channel

2.2.9. Return on Investment (%)

2.2.10. Technological Capabilities

2.2.11. Geographical Presence

2.3. Market Structure

2.3.1. Market Leaders

2.3.2. Market Followers

2.3.3. Emerging Players

2.4. Mergers and Acquisitions Details - Gantry Robots Market: Dynamics

3.1. Gantry Robots Market Trends

3.2. Gantry Robots Market Dynamics

3.2.1. Drivers

3.2.2. Opportunities

3.2.3. Trends

3.2.4. Challenges

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

3.5. Regulatory Landscape by Region

3.6. Key Opinion Leader Analysis for the Global Industry

3.7. Analysis of Government Schemes and Initiatives for Industry - Gantry Robots Market: Global Market Size and Forecast by Segmentation (by Value in USD Billion and Volume) (2026-2034)

4.1. Gantry Robots Market Size and Forecast, by Payload Capacity (2026-2034)

4.1.1. Up to 100 Kg

4.1.2. 100–300 Kg

4.1.3. 300–500 Kg

4.1.4. Above 500 Kg

4.2. Gantry Robots Market Size and Forecast, by Application (2026-2034)

4.2.1. Material Handling

4.2.2. Palletizing & Packaging

4.2.3. Machine Tending

4.2.4. Assembly Operations

4.2.5. Welding

4.2.6. Inspection & Quality Control

4.3. Gantry Robots Market Size and Forecast, by Axis Configuration (2026-2034)

4.3.1. 1-Axis Gantry Robots

4.3.2. 2-Axis Gantry Robots

4.3.3. 3-Axis Gantry Robots

4.3.4. Multi-Axis Gantry Robots

4.4. Gantry Robots Market Size and Forecast, by End-Use Industry (2026-2034)

4.4.1. Automotive

4.4.2. Electronics & Semiconductor

4.4.3. Logistics & Warehousing

4.4.4. Food & Beverage

4.4.5. Aerospace & Defense

4.4.6. Heavy Machinery & Metal Fabrication

4.4.7. Pharmaceuticals

4.4.8. Others

4.5. Gantry Robots Market Size and Forecast, by Region (2026-2034)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Middle East and Africa

4.5.5. South America

- 5. North America Gantry Robots Market Size and Forecast by Segmentation (by Value in USD Billion and Volume) (2026-2034)

1. North America Gantry Robots Market Size and Forecast, by Payload Capacity (2026-2034)

5.2. North America Gantry Robots Market Size and Forecast, by Application (2026-2034)

5.3. North America Gantry Robots Market Size and Forecast, by Axis Configuration (2026-2034)

5.4. North America Gantry Robots Market Size and Forecast, by End-Use Industry (2026-2034)

5.5. North America Gantry Robots Market Size and Forecast, by Country (2026-2034)

5.5.1. United States

5.5.2. Canada

5.5.3. Mexico - Europe Gantry Robots Market Size and Forecast by Segmentation (by Value in USD Billion and Volume) (2026-2034)

6.1. Europe Gantry Robots Market Size and Forecast, by Payload Capacity (2026-2034)

6.2. Europe Gantry Robots Market Size and Forecast, by Application (2026-2034)

6.3. Europe Gantry Robots Market Size and Forecast, by Axis Configuration (2026-2034)

6.4. Europe Gantry Robots Market Size and Forecast, by End-Use Industry (2026-2034)

6.5. Europe Gantry Robots Market Size and Forecast, by Country (2026-2034)

6.5.1. United Kingdom

6.5.2. France

6.5.3. Germany

6.5.4. Italy

6.5.5. Spain

6.5.6. Russia

6.5.7. Rest of Europe - Asia Pacific Gantry Robots Market Size and Forecast by Segmentation (by Value in USD Billion and Volume) (2026-2034)

7.1. Asia Pacific Gantry Robots Market Size and Forecast, by Payload Capacity (2026-2034)

7.2. Asia Pacific Gantry Robots Market Size and Forecast, by Application (2026-2034)

7.3. Asia Pacific Gantry Robots Market Size and Forecast, by Axis Configuration (2026-2034)

7.4. Asia Pacific Gantry Robots Market Size and Forecast, by End-Use Industry (2026-2034)

7.5. Asia Pacific Gantry Robots Market Size and Forecast, by Country (2026-2034)

7.5.1. China

7.5.2. Japan

7.5.3. South Korea

7.5.4. India

7.5.5. Australia

7.5.6. Southeast Asia

7.5.7. Rest of Asia Pacific - Middle East and Africa Gantry Robots Market Size and Forecast by Segmentation (by Value in USD Billion and Volume) (2026-2034)

8.1. Middle East and Africa Gantry Robots Market Size and Forecast, by Payload Capacity (2026-2034)

8.2. Middle East and Africa Gantry Robots Market Size and Forecast, by Application (2026-2034)

8.3. Middle East and Africa Gantry Robots Market Size and Forecast, by Axis Configuration (2026-2034)

8.4. Middle East and Africa Gantry Robots Market Size and Forecast, by End-Use Industry (2026-2034)

8.5. Middle East and Africa Gantry Robots Market Size and Forecast, by Country (2026-2034)

8.5.1. GCC

8.5.2. South Africa

8.5.3. Egypt

8.5.4. Nigeria

8.5.5. Rest of MEA - South America Gantry Robots Market Size and Forecast by Segmentation (by Value in USD Billion and Volume) (2026-2034)

9.1. South America Gantry Robots Market Size and Forecast, by Payload Capacity (2026-2034)

9.2. South America Gantry Robots Market Size and Forecast, by Application (2026-2034)

9.3. South America Gantry Robots Market Size and Forecast, by Axis Configuration (2026-2034)

9.4. South America Gantry Robots Market Size and Forecast, by End-Use Industry (2026-2034)

9.5. South America Gantry Robots Market Size and Forecast, by Country (2026-2034)

9.5.1. Brazil

9.5.2. Argentina

9.5.3. Colombia

9.5.4. Chile

9.5.5. Rest of South America - Company Profile: Key Players

10.1 ABB Ltd.

10.2 FANUC Corporation

10.3 KUKA AG

10.4 Yaskawa Electric Corporation

10.5 Mitsubishi Electric Corporation

10.6 Bosch Rexroth AG

10.7 Kawasaki Heavy Industries Ltd.

10.8 DENSO Corporation

10.9 Siemens AG

10.10 OMRON Corporation

10.11 Others - Gantry Robots Market Key Findings

- Gantry Robots Market Analyst Recommendations

- Gantry Robots Market: Research Methodology