China LiDAR for Mobile Robotics Market Size, Share, Growth Trends, Industry Analysis, Key Players, Investment Opportunities and Forecast 2026-2034

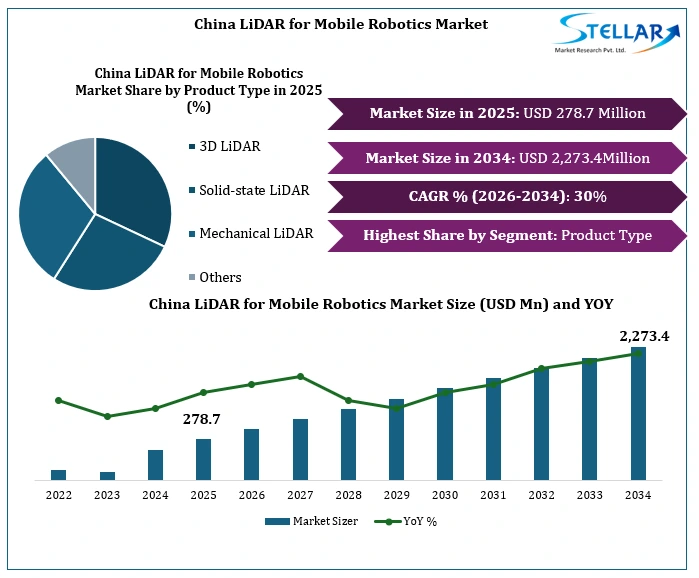

The China LiDAR for Mobile Robotics Market was valued at USD 278.7 Million in 2025 and is projected to reach USD 2,273.4 Million by 2034, reflecting a 30% CAGR.

Growth is driven by adoption of Autonomous Mobile Robot (AMR) and Automated Guided Vehicle (AGV) in manufacturing, warehousing, and logistics activities. The fast-paced evolution of smart factories and logistics infrastructure is raising the demand for LiDAR technology that provides navigation, mapping, localization, and obstacle detection capabilities. In addition, increasing investments in AI-based robotics and advanced automation are contributing to the adoption of LiDAR-equipped mobile robotics systems, thereby driving the market in China.

China LiDAR for Mobile Robotics Market Overview

The China LiDAR for Mobile Robotics Market is experiencing healthy growth due to the rising adoption of autonomous mobile robots across different sectors. LiDAR technology is essential for the navigation, mapping of the environment, localization, and obstacle detection of the robot in real-time. The increasing use of AMR and AGV in warehouses, logistics, and manufacturing is generating high demand for LiDAR. Rapid growth in the establishment of smart factories and automated warehouses in China is further fueling the growth of this market. Major LiDAR providers like Hesai and RoboSense are gradually diverting their attention from automotive sector towards mobile robotics.

Investments in AI-based robotics and industrial automation are also driving the growth of the LiDAR market in China. Increasing availability of small form factor and affordable solid-state LiDAR systems is making it easier to integrate LiDAR in different types of robotic systems. Mobile robots with LiDAR technology are being employed for tasks such as material handling, inspection, delivery, cleaning, and monitoring services. There is increasing demand for LiDAR from healthcare facilities, retail, and service robotics. Increasing adoption of humanoid robots and last mile delivery robots is further providing an opportunity for LiDAR providers in China.

To get more Insights: Request Free Sample Report

China LiDAR for Mobile Robotics Market Dynamics

China LiDAR for Mobile Robotics Market Drivers

Growing Pivot of LiDAR Manufacturers Toward Mobile Robotics Applications

Growing shift of leading Chinese LiDAR manufacturers such as Hesai and RoboSense from automotive ADAS toward mobile robotics applications is expected to accelerate demand for robotics-grade LiDAR systems, supported by large-scale deployment across logistics robots, delivery robots, lawnmowers, and industrial automation systems. RoboSense robotics LiDAR shipments are reported at 303,000 units in 2025, reflecting a 1,142% year-on-year increase, while robotics LiDAR volume reached 185,500 units in Q1 2026, surpassing ADAS for the first time, indicating a structural shift toward robotics applications.

Solid-State LiDAR Architectures Based on VCSEL and SPAD Technologies

Increasing integration of Vertical Cavity Surface Emitting Laser (VCSEL) emitters and Single Photon Avalanche Diode (SPAD) detectors is expected to enable compact, cost-efficient LiDAR systems suitable for mobile robotics applications, as semiconductor-based manufacturing supports scalable production and improved reliability in constrained environments. Solid-state LiDAR systems are designed for robotics use cases where low-cost sensing and stable performance in indoor environments remain essential, with companies such as Hesai developing SPAD-based architectures to support high-resolution perception and robotic navigation systems.

Increasing Scale and Cost Reduction Driving Commercial Deployment

Increasing production scaling and cost optimization across Chinese LiDAR manufacturers is expected to support broader adoption in mobile robotics, as economies of scale reduce unit costs and improve commercial viability for mass deployment. Hesai and RoboSense together delivered more than 2.5 million LiDAR units combined in 2025, reflecting strong manufacturing capacity expansion, while cost reductions driven by in-house chip development and automated production processes support wider robotics integration

China LiDAR for Mobile Robotics Market Opportunities

Elderly Care and Assisted Living Robots

The healthcare and elderly care sectors are becoming promising sectors for deployment of robots with LiDAR sensors. Such robots need to navigate safely, monitor continuously, and move reliably within human-centered environments like hospitals and nursing homes. Hence there will be a consistent demand for robots that aid in assisted living and perform service delivery operations.

Last Mile Delivery Robots Ecosystem

The urban and suburban environments are increasingly becoming testing grounds for last mile delivery robots. Such use cases involve detecting obstacles and planning a route adaptively due to the unpredictable nature of the environment. Thus the deployment of robots with LiDAR sensors becomes necessary for enabling navigation performance.

Indoor Mapping-as-a-Service Solutions

The demand for creating maps of indoor locations in real-time is rising within industrial warehouses, commercial buildings, and public infrastructure. Mobile robots with LiDAR is helping in mapping these locations in real-time without the need for scanning systems.

China LiDAR for Mobile Robotics Market Challenges

Site and Facility Challenges

There are many warehouses and manufacturing facilities that currently run on design and architecture based on traditional work processes involving humans. Thus, the layout becomes another limitation because it requires changes in navigation path, space and storage design, which makes the implementation time consuming process especially for middle-size companies because of high costs of changing facility infrastructure.

LiDAR Limitations in Relation to Environment Dynamics

The quality of LiDAR sensor performance in a highly dynamic and unstructured environment is low due to moving obstacles, reflection surfaces, and other interferences that affect signal stability. Thus, the problems with mapping and localization that is to be found in this case become another constraint related to the usage of LiDARs.

Workforce Constraint

Shortage of professionals in such spheres as robotics and LiDAR technologies makes it difficult for companies to use advanced mobile robotics solutions. This constraint is more visible for small businesses that have limited internal technical resources.

China LiDAR for Mobile Robotics Market Trends

Growing Demand for LiDAR for Humanoid Robots

The development of humanoid robots will create a gradually growing demand for LiDAR-based solutions due to the requirement of these robotic systems to perceive the space for environment mapping, navigation, and obstacle detection. From the market perspective, humanoid robotics is considered as a high-complexity application layer that is still in development and requires the application of LiDAR sensors to ensure safe interaction with people and objects in dynamically changing environments like healthcare institutions and service areas.

Growing Use Cases of LiDAR in Mobile Robotics

The number of LiDAR applications in mobile robotics is gradually growing in warehousing, logistics, manufacturing, healthcare, retail, and service robots, where navigation, localization, mapping, and obstacle detection are important for the efficient operation of the machines. It is a scale-related case study, where autonomous mobile robots and automated guided vehicles utilize LiDAR solutions for operation in structured and partially structured environments with little to no human interaction involved.

China LiDAR for Mobile Robotics Market Segmentation 2025

Product Type

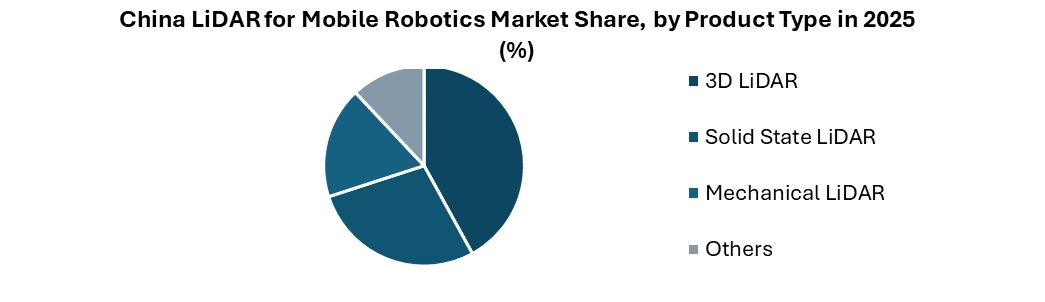

The 3D LiDAR is the largest with 42% market share owing to extensive application in AMRs, warehouse robots, and service robots where spatial mapping and obstacle detection are needed. Solid-State LiDAR makes up about 28% of the market share, experiencing fast growth because of smaller size, cheaper cost, and increased durability, making them ideal for logistics robots, delivery robots, and future humanoid robotics applications. The mechanical LiDAR has about 18% market share, which is mainly applied in cases that demand long-distance and high-resolution scanning, but gradually becomes less significant in the mobile robotics sector.

Component

Laser scanners hold around 26% share and act as the main sensing unit for distance measurement and mapping. Processors account for nearly 20% share due to rising need for real-time data processing and navigation support. Controllers contribute about 16% share, managing robot movement and system coordination. Cameras hold around 14% share, driven by increasing use of sensor fusion with LiDAR. IMUs account for about 10% share for motion tracking and stability, while GPS/GNSS receivers hold around 6% share mainly for outdoor positioning and navigation tasks. Other components include supporting modules used for system integration and connectivity.

Sensors

The 1D LiDAR sensor takes about 10% market share and is commonly used for simple distance sensing applications in automation processes in which full environmental mapping is not necessary. The 2D LiDAR sensors constitute 32% market share and are extensively employed in Automated Guided Vehicles (AGVs) and low-level Autonomous Mobile Robots (AMRs) in highly structured environments such as warehouses and manufacturing plants. The 3D LiDAR sensors make up about 58% market share since they offer full environmental recognition, real-time mapping, and effective obstacle avoidance functions.

Applications

warehousing and logistics owing to the adoption of AMR and AGV robots for material handling, sorting, and fulfilling purposes. In the industrial manufacturing sector, LiDAR technology is used by robots to automate manufacturing processes and inspecting processes. The healthcare and hospitals sector utilizes robots in their automation process for delivering, monitoring, and assistance purposes. Robots in the retail and commercial sectors are used in cleaning, managing inventory, and customer interaction services.

China LiDAR for Mobile Robotics Market Recent Market Developments:

On February 2025, RoboSense became the first LiDAR company to produce and deliver 1 million LiDAR units globally. The milestone unit, a fully solid-state E1R LiDAR, was delivered to Humanoid Robot (Shanghai) Co., Ltd. for integration into the Qinglong humanoid robot platform, highlighting the growing adoption of LiDAR in humanoid and mobile robotics applications.

On July 2025, At the 2025 World Artificial Intelligence Conference (WAIC), multiple Chinese robotics companies showcased humanoid and embodied AI robots equipped with RoboSense LiDAR solutions. The development reflects increasing integration of LiDAR sensors in next-generation mobile robots requiring autonomous navigation, perception, and obstacle avoidance capabilities

On January 2026, Hesai Technology announced plans to expand its annual LiDAR production capacity from 2 million units to more than 4 million units in 2026, reflecting growing adoption of LiDAR technology across autonomous mobile robots, logistics robots, service robots, and other intelligent robotic platforms. The capacity expansion is intended to address rising requirements for high-performance perception sensors used in navigation, localization, mapping, and obstacle detection applications within the robotics sector.

|

China LiDAR for Mobile Robotics Market |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2034 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 278.7 Mn. |

|

Forecast Period 2026 to 2034 CAGR: |

30% |

Market Size in 2034: |

USD 2,273.4 Mn. |

|

Segments

|

By Product Type |

|

|

|

By Sensors |

|

||

|

By Component |

|

||

|

|

By Application

|

|

|

China LiDAR for Mobile Robotics Market Key Players

- Hesai Technology

- RoboSense

- Livox

- SLAMTEC

- Seyond

- Leishen Intelligent

- Benewake

- SureStar

- Huawei

- Others

Frequently Asked Questions

Leading companies such as Hesai and RoboSense are expanding into mobile robotics because demand for robotics-grade LiDAR is rising rapidly across logistics robots, delivery robots, lawnmowers, industrial robots, and humanoid robots.

3D LiDAR holds the largest market share, accounting for about 42% of the market, due to its ability to provide accurate environmental mapping, real-time perception, and obstacle avoidance for mobile robots.

LiDAR is widely used in warehousing and logistics, industrial manufacturing, healthcare, retail, and service robotics for navigation, localization, mapping, material handling, inspection, and autonomous operation.

Major challenges include high facility modification costs, performance limitations in dynamic environments with moving obstacles and reflective surfaces, and a shortage of skilled professionals in robotics and LiDAR technologies.

1. China LiDAR for Mobile Robotics Market: Executive Summary

1.1. China LiDAR for Mobile Robotics Market Size and Forecast (USD Million)

1.2 Market Definition

1.3 Market Segmentation

1.4 Research Timelines

1.5 Assumptions

1.6 Limitation

2. China LiDAR for Mobile Robotics Market: Research Methodology

2.1 Data Mining

2.2 Secondary Research

2.3 Primary Research

2.4 Subject Matter Expert Advice

2.5 Quality Check

2.6 Final Review

2.7 Data Triangulation

2.8 Top-Down Approach

2.9 Bottom-Up Approach

2.10 Research Flow

2.11 Data Sources

3. China LiDAR for Mobile Robotics Market: Market Attractiveness Mapping

3. 1 China LiDAR for Mobile Robotics Market Overview

3.2 Competitive Analysis: Funnel Diagram (Tier 1, Tier 2, Tier 3)

3.3 China LiDAR for Mobile Robotics Market Absolute Market Opportunity

3.4 China LiDAR for Mobile Robotics Market Attractiveness Analysis, By Product Type

3.5 China LiDAR for Mobile Robotics Market Attractiveness Analysis, By Components

3.6 China LiDAR for Mobile Robotics Market Attractiveness Analysis, By Application

3.7 China LiDAR for Mobile Robotics Market Attractiveness Analysis, By Sensors

3.8 Future Market Opportunities

4. China LiDAR for Mobile Robotics Market: Market Outlook

4.1 China LiDAR for Mobile Robotics Market Evolution

4.2 China LiDAR for Mobile Robotics Market Outlook

4.3 Market Drivers

4.4 Market Restraints

4.5 Market Trends

4.6 Market Opportunity

4.7 Porter’s Five Forces Analysis

4.7.1 Threat of New Entrants

4.7.2 Bargaining Power of Suppliers

4.7.3 Bargaining Power of Buyers

4.7.4 Threat of Substitute Products

4.7.5 Competitive Rivalry of Existing Competitors

4.8 Value Chain Analysis

4.9 Pricing and Cost Structure

4.10 Port and Infrastructure Development

4.11 E-commerce USA Intelligent Transportation System

4.12 Geopolitical Impact Analysis on USA Intelligent Transportation System

4.13 Regulatory Standards & Policy Landscape

4.14 Intelligent Transportation System and Sustainability

4.15 Technology Analysis

5. China LiDAR for Mobile Robotics Market: By Product Type (2026-2034)

5.1 3D LiDAR

5.3 Solid State LiDAR

5.3 Mechanical LiDAR

5.3.1 Flash LiDAR

5.3.2MEMS LiDAR

5.3.3 OPA (Optical Phased Array)

6. China LiDAR for Mobile Robotics Market: By Component (2026-2034)

6.1 Laser Scanners

6.2 Inertial Measurement Units

6.3 GPS/GNSS Receivers

6.4 Cameras

6.5 Processors

6.6 Controllers

6.7 Others

7. China LiDAR for Mobile Robotics Market: By Application (2026-2034)

7.1 Warehousing and Logistics

7.2 Industrial Manufacturing

7.3 Healthcare & Hospital Automation

7.4 Retail & Commercial Space

7.5 Others

8. China LiDAR for Mobile Robotics Market: By Sensors (2026-2034)

8.1 1D LiDAR Sensors

8.2 2D LiDAR Sensors

8.3 3D LiDAR Sensors

9. SMR Competitive Matrix

10. China LiDAR for Mobile Robotics Market: Company Benchmarking

11. China LiDAR for Mobile Robotics Market: Company Profiles

11.1 Each Profile Covers:

11.2 Company Overview

11.3 Business Portfolio

11.4 Financial Overview

11.5 Industry Focus

11.6 Strategic Analysis

11.7 SWOT Analysis

11.8 Recent Developments

11.9 key players

1. Hesai Technology

2. RoboSense

3. Livox

4. SLAMTEC

5. Seyond

6. Leishen Intelligent

7. Benewake

8. SureStar

9. Huawei

10. Others

12. Risk Assessment and Scenario Analysis

13. Strategic Opportunity

14. Investments & Funding Analysis

15. Strategic Roadmap

15.1 Short-Term Roadmap 2026–2027

15.2 Mid-Term Roadmap 2028–2029

15.3 Long-Term Roadmap 2030–2032

16. Analyst Recommendations

16.1 Recommendations for ITS Companies

16.2 Recommendations for Investors

16.3 Recommendations for New Entrants

16.4 Recommendations for Maintenance Firms

16.5 Recommendations for Consulting and Strategy Teams