Video Surveillance Market: Global Size, Share, Growth, Trends, and Forecast Analysis Report (2026-2032)

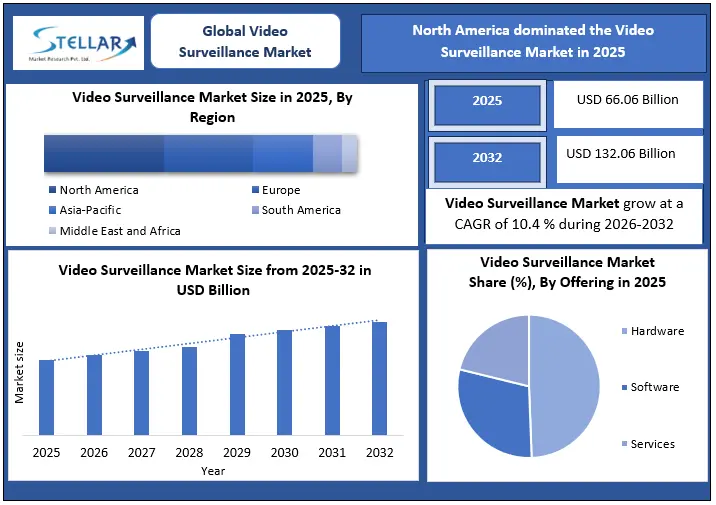

The Global Video Surveillance Market was valued at USD 66.06 billion in 2025, projected to reach USD 132.06 billion by 2032, growing at a CAGR of 10.4% during the forecast period.

Global Video Surveillance Market Overview:

Video surveillance market encompasses IP cameras, analog cameras, video management systems, and cloud-based monitoring solutions deployed across diverse industries. The market demonstrates robust expansion driven by rising security threats, smart city initiatives, and artificial intelligence integration. The global video surveillance market was valued at USD 66.06 billion in 2025, projected to reach USD 132.06 billion by 2032, growing at a CAGR of 10.4% during the forecast period. Over 1 billion surveillance cameras operate worldwide as of 2025, with installations growing at an unprecedented rate.

This comprehensive report provides actionable insights into market size, revenue forecasts, and growth opportunities across 45+ countries. Business leaders, investors, and security professionals gain access to detailed competitive analysis covering 30+ leading manufacturers. The report examines technology adoption rates, pricing trends, and regulatory impacts shaping investment decisions through 2032.

IP-based surveillance systems captured over 67% market share in 2025, replacing traditional analog infrastructure. Cloud video surveillance subscriptions reached 15 million users globally. Artificial intelligence-enabled cameras now represent a USD XX billion segment with 36% annual growth projections.

To get more Insights: Request Free Sample Report

Video Surveillance Market Drivers: Global crime rates averaging 45 incidents per 1,000 residents drive surveillance adoption across urban centers. Government spending on public safety infrastructure exceeded USD XX billion in 2025, with 27% allocated to video monitoring systems. Smart city projects in 600+ cities worldwide mandate integrated surveillance networks for traffic management and emergency response.

Retail theft costs businesses USD 100 billion annually, pushing 78% of retailers to upgrade surveillance capabilities. Banking institutions deploy an average of 42 cameras per branch to meet regulatory compliance requirements. Insurance premium reductions of 10-20% incentivize commercial property surveillance installations.

4K resolution cameras priced below USD 150 make professional-grade surveillance accessible to small businesses. Thermal imaging technology adoption increased 40% during 2020-2025 for health screening and perimeter security applications.

Resolutions of Common Analog Video Cameras

|

Analog Video Format |

Resolution |

|

1080p Resolution |

1920 × 1080 |

|

720p Resolution |

1280 × 720 |

|

D1 Resolution |

704 × 480 (NTSC for the United States) |

|

720 × 576 (PAL for Europe) |

|

|

CIF Resolution |

352 × 240 |

|

QCIF Resolution |

176 × 120 |

Video Surveillance Market Restraints: GDPR and similar privacy regulations in 120+ countries restrict facial recognition deployment and data retention practices. Initial system costs ranging from USD 5,000 to USD 500,000 depending on scale create budget barriers. Cybersecurity incidents affecting 30% of networked cameras expose vulnerability concerns among enterprise customers.

Video Surveillance Market Trends: AI-powered video analytics achieved 96% accuracy in facial recognition and 88% in behavior detection. Thermal cameras sales surged 180% during 2020-2023, establishing permanent presence in access control systems. Wireless 5G-enabled cameras eliminate installation costs averaging USD 150 per camera for wired infrastructure.

Body-worn cameras market for law enforcement reached USD XX million with 45% adoption across police departments. Multi-sensor 360-degree cameras reduce equipment needs by 75% in large venues. Cybersecurity-certified cameras command 15-20% price premiums in enterprise segments.

Video Surveillance Market Regional Insights

In 2025, North America held the largest market share, accounting for 32% of the global surveillance market revenue, valued at $XX billion. United States operates 70 million surveillance cameras with $15 billion annual spending on upgrades and new installations. The report details state-level adoption rates, vendor market shares, and procurement trends across federal, state, and municipal levels.

Asia Pacific leads growth with 42% CAGR in smart surveillance deployments. China's 700 million installed cameras represent 54% of global camera population. India's smart city mission across 100 cities creates $8 billion infrastructure opportunity through 2027. This analysis provides city-wise investment data, technology preferences, and competitive landscape across 10+ Asia Pacific markets.

Europe maintains 95 cameras per 1,000 residents, highest globally. UK surveillance spending reached $1.2 billion annually with 6 million cameras deployed nationwide. The report examines GDPR compliance impacts, technology migration patterns, and market consolidation trends across European countries.

Middle East surveillance market grows 18% annually driven by mega-events, tourism infrastructure, and oil facility security. Saudi Arabia and UAE combined investments exceed $3 billion for smart city surveillance deployments.

Video Surveillance Market Segment Analysis

Video Surveillance Market Size by Component (2025)

Hardware segment valued at $XX billion holds 58% market share in 2025. IP cameras dominate with 68% adoption, priced between $80-$1,500 based on specifications. PTZ cameras grow at 15% CAGR serving applications requiring flexible monitoring across 300-degree coverage areas in 2025.

This report analyzes pricing trends across 12 camera categories, examining 200+ SKUs from leading manufacturers. Storage segment forecasts through 2032 cover NVR, hybrid DVR, and cloud storage adoption curves with cost-per-terabyte projections.

Video Surveillance Market Size by Application

Commercial sector represents 45% of deployments averaging 28 cameras per installation. Retail surveillance spending reached $12 billion globally with loss prevention ROI averaging 300%. Banking institutions mandate surveillance meeting ISO 27001 standards with 90-day video retention requirements.

Critical infrastructure protection accounts for $18 billion surveillance spending across energy, water, and transportation facilities. The report examines application-specific requirements, compliance mandates, and technology adoption rates across vertical markets.

Video Surveillance Market Competitive Landscape

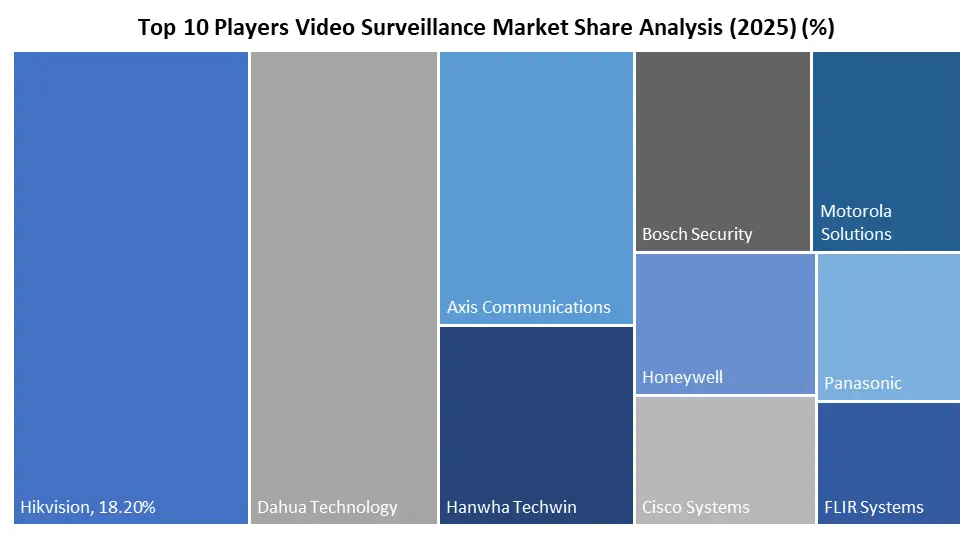

Top 10 manufacturers control 62% market share with Hikvision and Dahua leading at 18% and 14% respectively. The report profiles 30+ key players with financial performance, product portfolios, and strategic initiatives. Analysis includes merger and acquisition trends totaling $8.5 billion in 2022-2025, pricing strategies, and distribution channel dynamics.

Companies investing $500 million+ annually in AI research gain competitive advantages in analytics capabilities. This report provides SWOT analysis, market positioning matrices, and growth strategies for emerging players and established leaders.

Global Video Surveillance Market Scope

|

Global Video Surveillance Market |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2032 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 66.06 Billion |

|

Forecast Period 2026 to 2032 CAGR: |

10.4 % |

Market Size in 2032: |

USD 132.06 Billion |

|

Video Surveillance Market Segment Analysis |

By Offering |

Hardware Cameras Monitors Storage Devices Accessories Software Video Management Software Video Analytics Software Service Video Surveillance-as-a-Service installation & Maintenance |

|

|

By System |

Analog IP Hybrid |

||

|

By Deployment |

Cloud On-Premises |

||

|

By Enterprise Size |

Large Enterprise SMEs |

||

|

By Pricing Model |

Per Camera Per System Subscription-Based Pay-Per-Use |

||

|

By Connectivity |

Wired Systems Wireless Systems Cellular/Remote Surveillance Systems |

||

|

By Vertical |

City Surveillance and Safe-City Commercial Retail and Malls BFSI and Fin-Tech Critical Infrastructure Energy and Utilities Transportation (Airports, Rail, Ports) Industrial Manufacturing Residential and Smart-Home Defense and Homeland Security |

||

Video Surveillance Market Key Players Analysis

Hardware Providers

- Hikvision Digital Technology Co., Ltd.

- Zhejiang Dahua Technology Co., Ltd.

- Axis Communications AB

- Bosch Security Systems

- Hanwha Vision Co., Ltd.

- Panasonic Corporation

- Sony Corporation

- FLIR Systems

- Pelco (Schneider Electric)

- VIVOTEK Inc.

- Mobotix AG

- IDIS Co., Ltd.

- CP Plus International

- Infinova Corporation

- Others

Solution Providers

- Genetec Inc.

- Milestone Systems A/S

- Qognify Inc. (Hexagon)

- Verint Systems Inc.

- Salient Systems Inc.

- AxxonSoft

- MIRASYS Inc.

- OpenEye

- Costar Technologies

- Eagle Eye Networks

- Videoloft (Manything)

- Cisco Systems, Inc.

- ADT Security Services Inc.

- Brivo Systems Inc.

- Others

Frequently Asked Questions

The privacy concerns surrounding video surveillance are a major restraint in the video surveillance market

The key players are Pelco, Uniview, etc.

the commercial segment is expected to witness a CAGR of 11.3% in the aforementioned forecast period.

1. Global Video Surveillance Market: Research Methodology

2. Global Video Surveillance Market Introduction

2.1. Market Size (2025) & Forecast (2026-2032)

2.2. Market Size (Value USD Bn.) and Market Share (%) - By Segments, Regions and Country

2.3. Executive Summary

3. Global Video Surveillance Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Headquarter

3.3.3. Product Portfolio

3.3.4. Technology Adoption

3.3.5. Marketing & Promotional Activities

3.3.6. Regulatory Compliance

3.3.7. R&D Investment (%)

3.3.8. Pricing Strategy

3.3.9. Market Share (%)

3.3.10. Market Revenue (2025)

3.3.11. Global Presence

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

3.6. Recent Developments

3.7. Market Positioning & Share Analysis

3.7.1. Company Revenue, Video Surveillance Revenue, and Market Share (%)

3.7.2. SMR Competitive Positioning

3.8. Strategic Developments & Partnerships

4. Video Surveillance Market: Dynamics

4.1. Video Surveillance Market Trends

4.2. Video Surveillance Market Dynamics

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.2.4. Threats

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

5. Video Surveillance Market Hardware Layer Analysis

5.1. Camera Market by Type (Fixed, PTZ, Thermal, Specialty Cameras)

5.2. Storage Infrastructure (On-site NVR/DVR vs Cloud Storage)

5.3. Edge Devices and AI-enabled Cameras Adoption

5.4. Hardware ASP Trends and Regional Price Compression

5.5. Replacement Cycles and Installed Base Dynamics

6. Video Surveillance Market Software and Intelligence Stack

6.1. Video Management Software (VMS) Market Structure

6.2. Video Analytics Penetration and Attach Rates

6.3. AI Use Cases: Facial Recognition, Object Detection, Behavior Analysis

6.4. Open Platform vs Proprietary Ecosystems

6.5. Cybersecurity and Data Governance in Surveillance Networks

7. Video Surveillance Market Service and Business Model Transformation

7.1. Video Surveillance-as-a-Service (VSaaS) Market Size and Growth

7.2. Managed Monitoring and Remote Operations

7.3. Installation, Integration, and Lifecycle Maintenance Economics

7.4. Shift from CapEx to OpEx Buying Models

7.5. Recurring Revenue Contribution by Region and Vertical

8. Video Surveillance Market Connectivity and Infrastructure Landscape

8.1. Wired vs Wireless Surveillance Architectures

8.2. Cellular and Remote Surveillance in Infrastructure and Mobility Use Cases

8.3. Edge vs Centralized Processing Models

8.4. Network Bandwidth Requirements and Cost Implications

9. Video Surveillance Market Vertical-Specific Adoption and Spend Patterns

9.1. Smart City and Safe City Programs (Project Pipeline and Funding Models)

9.2. Commercial Sector

9.2.1. Retail and Mall Surveillance (Loss Prevention and Customer Analytics)

9.2.2. BFSI and FinTech (Compliance-driven Deployments)

9.3. Critical Infrastructure

9.3.1. Energy and Utilities

9.3.2. Transportation (Airports, Rail, Ports)

9.4. Industrial Manufacturing (Process Monitoring and Safety Analytics)

9.5. Residential and Smart Home Surveillance

9.6. Defense and Homeland Security (Border, Perimeter, Tactical Systems)

10. Video Surveillance Market Installed Base and Replacement Cycle Analysis

10.1. Global Installed Camera Base by Region and Vertical

10.2. Analog to IP Migration Rate

10.3. Average Replacement Cycles (Camera, Storage, VMS)

10.4. Brownfield vs Greenfield Deployment Share

10.5. Upgrade Triggers (AI Enablement, Compliance, Security Breaches)

11. Video Surveillance Market Data Monetization and Operational Intelligence Use Cases

11.1. Transition from Security to Business Intelligence

11.2. Retail Footfall and Heat Mapping Economics

11.3. Manufacturing Process Optimization via Video

11.4. City Analytics (Traffic Flow, Crowd Management)

11.5. Revenue Uplift Potential from Analytics Layers

12. Global Video Surveillance Market: Size and Forecast by Segmentation (By Value USD Million) (2025-2032)

12.1. Global Video Surveillance Market Size and Forecast, By Offering

12.2. Hardware

12.2.1. Cameras

12.2.2. Monitors

12.2.3. Storage Devices

12.2.4. Accessories

12.3. Software

12.3.1. Video Management Software

12.3.2. Video Analytics Software

12.4. Service

12.4.1. Video Surveillance-as-a-Service

12.4.2. installation & Maintenance

12.5. Global Video Surveillance Market Size and Forecast, By System

12.5.1. Analog

12.5.2. IP

12.5.3. Hybrid

12.6. Global Video Surveillance Market Size and Forecast, By Deployment

12.6.1. Cloud

12.6.2. On-Premises

12.7. Global Video Surveillance Market Size and Forecast, By Enterprise Size

12.7.1. Large Enterprise

12.7.2. SMEs

12.8. Global Video Surveillance Market Size and Forecast, By Pricing Model

12.8.1. Per Camera

12.8.2. Per System

12.8.3. Subscription-Based

12.8.4. Pay-Per-Use

12.9. Global Video Surveillance Market Size and Forecast, By Connectivity

12.9.1. Wired Systems

12.9.2. Wireless Systems

12.9.3. Cellular/Remote Surveillance Systems

12.10. Global Video Surveillance Market Size and Forecast, By Vertical

12.10.1. City Surveillance and Safe-City

12.10.2. Commercial

12.10.2.1. Retail and Malls

12.10.2.2. BFSI and Fin-Tech

12.10.3. Critical Infrastructure

12.10.3.1. Energy and Utilities

12.10.3.2. Transportation (Airports, Rail, Ports)

12.10.4. Industrial Manufacturing

12.10.5. Residential and Smart-Home

12.10.6. Defense and Homeland Security

12.11. Global Video Surveillance Market Size and Forecast, By Region

12.11.1. North America

12.11.2. Europe

12.11.3. Asia Pacific

12.11.4. Middle East and Africa

12.11.5. South America

13. North America Video Surveillance Market Size and Forecast By Segmentation (By Value USD Million) (2025-2032)

13.1. North America Market Size and Forecast, By Offering

13.2. North America Market Size and Forecast, By System

13.3. North America Market Size and Forecast, By Deployment

13.4. North America Market Size and Forecast, By Enterprise Size

13.5. North America Video Surveillance Market Size and Forecast, By Pricing Model

13.6. North America Video Surveillance Market Size and Forecast, By Connectivity

13.7. North America Video Surveillance Market Size and Forecast, By Vertical

13.8. North America Market Size and Forecast, By Country

13.8.1. United States

13.8.2. Canada

13.8.3. Mexico

14. Europe Video Surveillance Market Size and Forecast By Segmentation (By Value USD Million) (2025-2032)

14.1. Europe Market Size and Forecast, By Offering

14.2. Europe Market Size and Forecast, By System

14.3. Europe Market Size and Forecast, By Deployment

14.4. Europe Market Size and Forecast, By Enterprise Size

14.5. Europe Video Surveillance Market Size and Forecast, By Pricing Model

14.6. Europe Video Surveillance Market Size and Forecast, By Connectivity

14.7. Europe Video Surveillance Market Size and Forecast, By Vertical

14.8. Europe Market Size and Forecast, By Country

14.8.1. United Kingdom

14.8.2. France

14.8.3. Germany

14.8.4. Italy

14.8.5. Spain

14.8.6. Sweden

14.8.7. Russia

14.8.8. Rest of Europe

15. Asia Pacific Video Surveillance Market Size and Forecast By Segmentation (By Value USD Million) (2025-2032)

15.1. Asia Pacific Market Size and Forecast, By Offering

15.2. Asia Pacific Market Size and Forecast, By System

15.3. Asia Pacific Market Size and Forecast, By Deployment

15.4. Asia Pacific Market Size and Forecast, By Enterprise Size

15.5. Asia Pacific Video Surveillance Market Size and Forecast, By Pricing Model

15.6. Asia Pacific Video Surveillance Market Size and Forecast, By Connectivity

15.7. Asia Pacific Video Surveillance Market Size and Forecast, By Vertical

15.8. Asia Pacific Market Size and Forecast, By Country

15.8.1. China

15.8.2. Japan

15.8.3. South Korea

15.8.4. India

15.8.5. Australia

15.8.6. Malaysia

15.8.7. Thailand

15.8.8. Vietnam

15.8.9. Indonesia

15.8.10. Philippines

15.8.11. Rest of Asia Pacific

16. Middle East and Africa Video Surveillance Market Size and Forecast By Segmentation (By Value USD Million) (2025-2032)

16.1. Middle East and Africa Market Size and Forecast, By Offering

16.2. Middle East and Africa Market Size and Forecast, By System

16.3. Middle East and Africa Market Size and Forecast, By Deployment

16.4. Middle East and Africa Market Size and Forecast, By Enterprise Size

16.5. Middle East and Africa Video Surveillance Market Size and Forecast, By Pricing Model

16.6. Middle East and Africa Video Surveillance Market Size and Forecast, By Connectivity

16.7. Middle East and Africa Video Surveillance Market Size and Forecast, By Vertical

16.8. Middle East and Africa Market Size and Forecast, By Country

16.8.1. South Africa

16.8.2. GCC

16.8.3. Nigeria

16.8.4. Egypt

16.8.5. Turkey

16.8.6. Rest of ME&A

17. South America Video Surveillance Market Size and Forecast By Segmentation (By Value USD Million) (2025-2032)

17.1. South America Market Size and Forecast, By Offering

17.2. South America Market Size and Forecast, By System

17.3. South America Market Size and Forecast, By Finish

17.4. South America Market Size and Forecast, By Enterprise Size

17.5. South America Video Surveillance Market Size and Forecast, By Pricing Model

17.6. South America Video Surveillance Market Size and Forecast, By Connectivity

17.7. South America Video Surveillance Market Size and Forecast, By Vertical

17.8. South America America Market Size and Forecast, By Country

17.8.1. Brazil

17.8.2. Argentina

17.8.3. Colombia

17.8.4. Chile

17.8.5. Rest Of South America

18. Company Profile: Key Players

18.1. Hikvision Digital Technology Co., Ltd.

18.1.1. Company Overview

18.1.2. Business Portfolio

18.1.3. Financial Overview

18.1.4. SWOT Analysis

18.1.5. Strategic Analysis

18.1.6. Recent Developments

18.2. Zhejiang Dahua Technology Co., Ltd.

18.3. Axis Communications AB

18.4. Bosch Security Systems

18.5. Hanwha Vision Co., Ltd.

18.6. Panasonic Corporation

18.7. Sony Corporation

18.8. FLIR Systems

18.9. Pelco (Schneider Electric)

18.10. VIVOTEK Inc.

18.11. Mobotix AG

18.12. IDIS Co., Ltd.

18.13. CP Plus International

18.14. Infinova Corporation

18.15. Genetec Inc.

18.16. Milestone Systems A/S

18.17. Qognify Inc. (Hexagon)

18.18. Verint Systems Inc.

18.19. Salient Systems Inc.

18.20. AxxonSoft

18.21. MIRASYS Inc.

18.22. OpenEye

18.23. Costar Technologies

18.24. Eagle Eye Networks

18.25. Videoloft (Manything)

18.26. Cisco Systems, Inc.

18.27. ADT Security Services Inc.

18.28. Brivo Systems Inc.

19. Key Findings

20. Industry Recommendations