Coffee Market Analysis Supply Tightness, Structural Shifts, and the Rise of Robusta (2026-2032)

Coffee Market size was valued at US$ 145.23 Bn. in 2025 with a CAGR of 6.6% reaching nearly 227.18 Bn. by 2032 while navigating a volatile supply environment shaped by climate disruption, inventory drawdowns, and shifting consumption patterns, with Robusta gaining share and Asia-Pacific emerging as the primary growth engine.

Coffee Market Overview:

The Global Coffee Market remains one of the most economically significant agricultural value chains, directly supporting over 25.7 million farmers worldwide. Coffee demand spans a wide spectrum of formats, from coffee beans, whole coffee beans, and ground coffee consumed at home to out-of-home beverages such as espresso and cold brew. In recent years, global coffee production reached approximately 175.5 million bags, marginally exceeding consumption of 174 million bags, marking the first surplus after three consecutive deficit years that had cumulatively drawn down nearly 17 million bags from global stocks.

Despite this return to surplus, market fundamentals remain structurally tight. Certified inventories in both New York and London declined sharply through 2024 and 2025, with Arabica stocks falling by nearly 50% year on year. As a result, coffee prices have become increasingly sensitive to weather disruptions, logistics constraints, and speculative activity. Global coffee prices increased by 37% during 2024, reaching a 13-year high in December, driven by supply disruptions across Brazil, Vietnam, and Indonesia. These price movements are directly influencing downstream categories such as instant coffee, coffee pods, and Nespresso pods, where formulation and sourcing flexibility are critical.

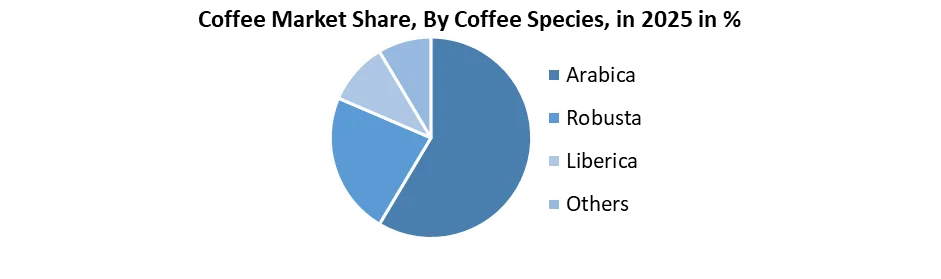

Structurally, the market is undergoing a gradual but meaningful shift in composition. Arabica coffee continues to dominate global consumption, accounting for around 60% of total production, supported by demand for premium and specialty coffee in developed markets. However, Robusta coffee has steadily gained share, rising to over 36% of global exports by late 2025, reflecting both supply-side constraints and changing consumer preferences in price-sensitive segments. This evolution is particularly evident in emerging markets, where affordability, convenience, and format diversity are reshaping how coffee is consumed across retail and foodservice channels.

To get more Insights: Request Free Sample Report

Coffee Market Key Highlights

• Demand Shift: Asia-Pacific recorded over 7% year-on-year consumption growth in 2025, while producing countries now account for more than one-third of global coffee consumption, structurally reducing export availability.

• Supply Concentration: Brazil and Vietnam together contribute nearly 50% of global coffee production, increasing systemic exposure to weather disruptions and policy changes in just two countries.

• Domestic Absorption: Brazil consumes over 40% of its own output, positioning it as the world’s second-largest consumer and limiting its ability to act as a swing exporter during supply shocks.

• Price Volatility: Coffee prices increased by 37% during 2024, reaching a 13-year high, driven by low inventories and weather-driven supply disruptions across Brazil, Vietnam, and Indonesia.

• Structural Price Pressure: Despite recent rallies, real coffee prices have declined long term, with Arabica prices falling 3% per year and Robusta 5% per year since 1970, reflecting chronic oversupply risk and buyer-side concentration.

• Species Mix Shift: Robusta’s share of global exports rose to over 36% by late 2025, as the Arabica–Robusta price differential narrowed to multi-decade lows, accelerating blend reformulation in instant and RTD products.

• Sustainability Premium: Certified and specialty coffees represent only 9–12% of developed-market imports, yet capture a disproportionately higher value share, driven by price premiums, regulatory compliance, and traceability requirements.

Recent Trends Shaping the Coffee Industry

One of the most visible trends is the narrowing Arabica–Robusta price differential, which reached historical lows in late 2024. This has accelerated formulation changes among roasters, particularly in instant coffee and RTD beverages.

Convenience continues to shape consumption behavior among coffee enthusiasts. According to a consumer survey done across 13 countries shows rising at-home preparation, driven initially by inflation but sustained by habit formation. Instant coffee remains the preferred entry format in emerging markets, while RTD adoption remains selective and usage-based rather than habitual.

Sustainability has moved from marketing to compliance. Regulatory frameworks such as the EU Deforestation Regulation, despite timeline extensions, are reshaping sourcing strategies and increasing traceability investments across the value chain.

Coffee Market Segment Analysis:

By Coffee Species: Arabica vs Robusta

Arabica continues to dominate global consumption due to flavor profile and specialty positioning, accounting for roughly 60% of global production. South America controls the majority of Arabica exports, with Brazil and Colombia as anchor suppliers.

Robusta, however, is the fastest growing species segment. Its share of exports increased from below 30% historically to over 37.8% by late 2025. Vietnam alone contributes over half of global Robusta exports. Improved quality, better processing, and rising Arabica prices have repositioned Robusta from a cost alternative to a strategic blend component, particularly in instant and RTD formats.

By Distribution Channel: On-trade vs Off-trade

Off-trade dominated global coffee volumes, driven by supermarkets, grocery retail, and e-commerce. Home consumption surged during 2021–2023 and has remained structurally higher, with instant coffee benefiting the most in emerging markets.

On-trade channels, including cafes and restaurants, have recovered unevenly post-pandemic. While premium cafes are driving value growth through specialty offerings, volume recovery remains constrained by price sensitivity and shifting consumer routines, especially among younger demographics.

Coffee Market Regional Analysis:

South America remains the production anchor, accounting for nearly 50% of global output, with Brazil and Vietnam together supplying almost half of the world’s coffee. However, growth momentum has shifted decisively toward Asia and Africa.

Asia-Pacific recorded export growth of over 47% year on year in late 2025, driven by Vietnam’s recovery and Indonesia’s Robusta shipments. Africa, led by Uganda and Ethiopia, has emerged as the fastest growing supply region, with Uganda targeting 20 million bags by 2030 after record exports in 2024/25.

On the demand side, Europe remains the largest consuming region but is structurally stagnant, with declining consumption in several mature markets. Asia and producing countries now represent the primary volume growth engines.

Coffee Market Competitive Landscape

The global coffee market is highly consolidated, with the top five roasters accounting for an estimated 55–60% of global roasted and soluble coffee volumes. Nestlé S.A. is the market leader, holding more than 20% share of the global packaged coffee market, supported by Nescafé and Nespresso. Nestlé’s coffee business generates USD 25–27 billion annually, representing the largest single exposure in the sector.

JDE Peet’s and Keurig Dr Pepper form the second competitive tier, together controlling 19% of global packaged coffee sales. JDE Peet’s Europe division contributed over 55% of volumes, while Keurig’s single-serve platform accounts for 40% of at-home coffee consumption in the U.S.

In the premium segment, Lavazza, Illycaffè, and Massimo Zanetti Beverage Group collectively represent 9% of global value, with disproportionately higher margins driven by espresso and foodservice exposure. Starbucks Corporation, with USD 35 billion in FY2024 revenue, operates a structurally different model, capturing value through retail pricing rather than volume share.

Overall, competitive advantage is defined by scale, sourcing reach, and hedging capability, while specialty players remain <10% of global volume despite outsized influence on quality and sustainability standards.

Global Coffee Market Scope

|

Global Coffee Market Scope |

|

|

Market Size in 2025 |

USD 145.23 Bn. |

|

Market Size in 2032 |

USD 227.18 Bn. |

|

CAGR (2026-2032) |

6.6% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments Analysis |

By Product Type Whole-bean Ground Coffee Instant Coffee Ready-to-Drink (RTD) Coffee Pod and Capsules |

|

By Nature Conventional Organic |

|

|

By Origin Single Origin/Specialty Mixed |

|

|

By Roast Type Light Roast Medium Roast Dark Roast |

|

|

By Flavor French Vanilla Hazelnut Caramel Mocha Others |

|

|

By Price Range Mass / Economy Premium Super-Premium |

|

|

By Coffee Species Caffeinated Decaffeinated |

|

|

By Process Caffeinated Decaffeinated |

|

|

By Generation Gen Alpha (<=13) Gen Z (14-27) Millennials (28-43) Gen X (44-59) Others (Boomers 60+) |

|

|

By Packaging Bags Jars & Tins Sachets & Refill Packs Bottles / Cans Others |

|

|

By Distribution Channel On-trade Cafes Restaurants & Hotels Workplaces Others Off-trade Supermarkets/Hypermarkets Convenience Stores Grocery Stores Online/e-Commerce Others |

|

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Russia, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Thailand, Vietnam, Philippines, and Rest of APAC)

Middle East and Africa (South Africa, GCC, Nigeria, Egypt, Turkey, and Rest of ME&A)

South America (Brazil, Argentina, Colombia, Chile, Peru, and the Rest of South America)

Coffee Market Key Players

- Nestle S.A.

- Tchibo GmbH

- Strauss Group (Strauss Coffee)

- Lavazza

- Keurig Dr Pepper (Keurig division)

- Jacobs Douwe Egberts / JDE Peet’s

- Tata Consumer Products (Eight O’Clock Coffee)

- UCC Ueshima Coffee Co.

- Melitta Group

- Illy (Illycaffè)

- Massimo Zanetti Beverage Group

- Eight O’Clock Coffee Company

- Starbucks Corporation

- Peet’s Coffee

- Coffee Bean & Tea Leaf

- Segafredo Zanetti

- Farmer Bros. Co.

- Caribou Coffee Company

- Death Wish Coffee Company

- Hawaiian Isles Kona Coffee Company

- Gevalia

- Dallmayr

- Kicking Horse Coffee

- Stumptown Coffee Roasters

- Louis Dreyfus Co. Mexico

- Olam Agro Mexico

- Sabormex

- Café El Marino S.A. de C.V.

- Café Punta del Cielo

- Ruta Maya Coffee

- Cabo Coffee Company

Frequently Asked Questions

1. Global Coffee Market: Research Methodology

2. Global Coffee Market Introduction

2.1. Market Size (2025) & Forecast (2026-2032)

2.2. Market Size (USD) and Market Share (%) - By Segments, Regions and Country

2.3. Executive Summary

3. Global Coffee Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Headquarter

3.3.3. Product Portfolio

3.3.4. Production Capacity (Tons)

3.3.5. Marketing and Flavor Innovation

3.3.6. Sustainability & Certifications

3.3.7. Technology Adoption

3.3.8. Marketing & Promotional Activities

3.3.9. Distribution & Channel Strategy

3.3.10. Packaging & Innovation in Formats

3.3.11. Regulatory Compliance & Quality Standards

3.3.12. R&D Investment (%)

3.3.13. Pricing Strategy

3.3.14. Market Share (%)

3.3.15. Market Revenue (2025)

3.3.16. Global Presence

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

3.6. Recent Developments

3.7. Market Positioning & Share Analysis

3.7.1. Company Revenue, Coffee Revenue, and Market Share (%)

3.7.2. SMR Competitive Positioning

3.8. Strategic Developments & Partnerships

4. Coffee Market: Dynamics

4.1. Coffee Market Trends

4.2. Coffee Market Dynamics

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

5. Regulatory & Certification Landscape

5.1. Overview of Global and Regional Coffee Trade Regulations

5.2. Sustainability Certifications and Standards Impacting Sourcing

5.3. ESG, Traceability, and Ethical Sourcing Requirements

5.4. Packaging Sustainability Regulations and Compliance Trends

5.5. Impact of Regulatory Compliance on Production Costs

5.6. Future Regulatory Outlook and Policy Risks

6. Coffee Bean Production Analysis (2025)

6.1. Global Coffee Production Overview By Species (Arabica vs Robusta)

6.2. Major Coffee-Producing Regions and Country-Level Output Trends

6.3. Yield Variability, Farming Practices, and Productivity Benchmarks

6.4. Impact of Climate Change, Weather Events, and Crop Diseases on Production

6.5. Harvest Cycles, Seasonality, and Supply Availability Patterns

6.6. Medium- to Long-Term Production Outlook and Supply Risks

7. Coffee Pricing Analysis (2025)

7.1. Historical Coffee Price Trends By Product Type (2020–2025)

7.2. Key Price Volatility Drivers Including Supply Shocks and Speculation

7.3. Pricing Differences By Species, Origin, and Quality Grade

7.4. Price Transmission from Green Beans to Roasted and Retail Coffee

7.5. Impact of Input Costs, Logistics, and Currency Fluctuations on Pricing

7.6. Forward Pricing Outlook and Risk Mitigation Strategies

8. Private Label vs Branded Coffee Analysis

8.1. Market Share Comparison Between Private Label and Branded Coffee

8.2. Pricing Strategies and Margin Differentials Across Retail and Foodservice Channels

8.3. Product Positioning, Packaging, and Quality Perception Differences

8.4. Role of Retailers, Shelf-Space Control, and Private Label Expansion Strategies

8.5. Consumer Preference, Brand Loyalty, and Switching Behavior

8.6. Impact on Competitive Intensity and Long-Term Market Structure

9. Sustainability Economics & Carbon Footprint Analysis

9.1. Carbon Footprint Across the Coffee Supply and Value Chain

9.2. Cost Implications of Sustainability Certifications and Compliance

9.3. Economics of Sustainable Farming, Ethical Sourcing, and Traceability

9.4. Packaging Sustainability Costs and Circular Economy Impact

9.5. Carbon Pricing, Reporting Requirements, and Regulatory Cost Exposure

9.6. Return on Investment (ROI) of Sustainability Initiatives for Market Participants

10. Supply Chain Analysis

10.1. Coffee Cultivation and Harvesting Practices

10.2. Post-Harvest Handling, Processing, and Storage of Green Coffee

10.3. Role of Major Producing Countries and Export Supply Structure

10.4. Logistics, Transportation, and Supply Chain Infrastructure

10.5. Key Supply Chain Risks, Bottlenecks, and Optimization Opportunities

11. Consumer Behavior & Coffee Consumption Trends

11.1. Global Coffee Consumption Patterns and Per-Capita Trends By country

11.2. At-Home Versus Out-of-Home Consumption Dynamics

11.3. Shift Toward Premium, Specialty, and Single-Origin Coffees

11.4. Demand for Flavored, Functional, and Low-Sugar Coffee Variants

11.5. Consumer Willingness to Pay and Price Sensitivity Analysis

11.6. Regional Differences in Taste, Format, and Consumption Habits

12. Ready-to-Drink (RTD) Coffee Market Deep Dive

12.1. RTD Coffee Market Size and Growth Outlook

12.2. Key Drivers Including Convenience, On-the-Go Consumption, and Youth Demand

12.3. Product Innovation in Flavors, Functionality, and Formulations

12.4. Packaging Trends and Shelf-Life Considerations

12.5. Competitive Landscape and Brand Strategies

12.6. Regional Hotspots and Future Growth Potential

13. Technology & Innovation Trends

13.1. Innovations in Coffee Roasting, Brewing, and Extraction Technologies

13.2. Advances in Processing Efficiency, Automation, and Quality Control

13.3. Smart Packaging, Shelf-Life Extension, and Freshness-Preservation Solutions

13.4. Digital Traceability, Blockchain, and Supply Chain Transparency Tools

13.5. Product Innovation in RTD, Functional, and Specialty Coffee

13.6. Impact of Technology Adoption on Cost Efficiency and Product Differentiation

14. Investment Landscape & Strategic Activity

14.1. Investment Trends Across Coffee Farming, Processing, and Branding

14.2. Venture Capital and Private Equity Activity in the Coffee Sector

14.3. Startup Ecosystem, Innovation Hubs, and Emerging Business Models

14.4. Mergers, Acquisitions, and Strategic Partnerships

14.5. Capital Allocation Toward Sustainability and ESG Initiatives

14.6. Investment Outlook and Strategic Implications for Market Participants

15. Substitute Products & Competitive Beverage Analysis

15.1. Competitive Landscape of Alternative Beverages

15.2. Impact of Substitutes on Coffee Demand

15.3. Price and Value Comparison Across Beverages

15.4. Flavor, Formulation, and Convenience Differentiation

15.5. Consumer Switching Behavior and Insights

15.6. Strategic Implications for Coffee Industry Players

16. Coffee Trade & Import-Export Analysis (2025)

16.1. Overview of Global Coffee Trade Flows and Major Exporting Countries

16.2. Key Importing Markets and Consumption Trends

16.3. Trade Volumes, Values, and Growth Rates By Country/Region

16.4. Tariffs, Non-Tariff Barriers, and Trade Policy Implications

16.5. Impact of Supply-Demand Gaps and Logistics on International Trade

16.6. Future Outlook and Strategic Implications for Producers, Roasters, and Traders

17. Global Coffee Market: Size and Forecast by Segmentation (By Value USD Million and Volume Tons) (2025-2032)

17.1. Global Coffee Market Size and Forecast, By Product Type

17.1.1. Whole-bean

17.1.2. Ground Coffee

17.1.3. Instant Coffee

17.1.4. Ready-to-Drink (RTD)

17.1.5. Coffee Pod and Capsules

17.2. Global Coffee Market Size and Forecast, By Nature

17.2.1. Conventional

17.2.2. Organic

17.3. Global Coffee Market Size and Forecast, By Origin

17.3.1. Single Origin/Specialty

17.3.2. Mixed

17.4. Global Coffee Market Size and Forecast, By Roast Type

17.4.1. Light Roast

17.4.2. Medium Roast

17.4.3. Dark Roast

17.5. Global Coffee Market Size and Forecast, By Flavor

17.5.1. French Vanilla

17.5.2. Hazelnut

17.5.3. Caramel

17.5.4. Mocha

17.5.5. Others

17.6. Global Coffee Market Size and Forecast, By Price Range

17.6.1. Mass / Economy

17.6.2. Premium

17.6.3. Super-Premium

17.7. Global Coffee Market Size and Forecast, By Coffee Species

17.7.1. Arabica

17.7.2. Robusta

17.7.3. Liberica

17.7.4. Others

17.8. Global Coffee Market Size and Forecast, By Process

17.8.1. Caffeinated

17.8.2. Decaffeinated

17.9. Global Coffee Market Size and Forecast, By Generation

17.9.1. Gen Alpha

17.9.2. Gen Z

17.9.3. Millennial

17.9.4. Gen X

17.9.5. Others

17.10. Global Coffee Market Size and Forecast, By Packaging

17.10.1. Bags

17.10.2. Jars & Tins

17.10.3. Sachets & Refill Packs

17.10.4. Bottles / Cans

17.10.5. Others

17.11. Global Coffee Market Size and Forecast, By Distribution Channel

17.11.1. On-trade

17.11.1.1. Cafes

17.11.1.2. Restaurants & Hotels

17.11.1.3. Workplaces

17.11.1.4. Others

17.11.2. Off-trade

17.11.2.1. Supermarkets/Hypermarkets

17.11.2.2. Convenience Stores

17.11.2.3. Grocery Stores

17.11.2.4. Online/e-Commerce

17.11.2.5. Others

17.12. Global Coffee Market Size and Forecast, By Region

17.12.1. North America

17.12.2. Europe

17.12.3. Asia Pacific

17.12.4. Middle East and Africa

17.12.5. South America

18. North America Coffee Market Size and Forecast By Segmentation (By Value USD Million and Volume Tons) (2025-2032)

18.1. North America Market Size and Forecast, By Product Type

18.2. North America Market Size and Forecast, By Nature

18.3. North America Market Size and Forecast, By Origin

18.4. North America Market Size and Forecast, By Roast Type

18.5. North America Market Size and Forecast, By Flavor

18.6. North America Market Size and Forecast, By Price Range

18.7. North America Market Size and Forecast, By Coffee Species

18.8. North America Market Size and Forecast, By Process

18.9. North America Market Size and Forecast, By Generation

18.10. North America Market Size and Forecast, By Packaging

18.11. North America Market Size and Forecast, By Distribution Channel

18.12. North America Market Size and Forecast, By Country

18.12.1. United States

18.12.2. Canada

18.12.3. Mexico

19. Europe Coffee Market Size and Forecast By Segmentation (By Value USD Million and Volume Tons) (2025-2032)

19.1. Europe Market Size and Forecast, By Product Type

19.2. Europe Market Size and Forecast, By Nature

19.3. Europe Market Size and Forecast, By Origin

19.4. Europe Market Size and Forecast, By Roast Type

19.5. Europe Market Size and Forecast, By Flavor

19.6. Europe Market Size and Forecast, By Price Range

19.7. Europe Market Size and Forecast, By Coffee Species

19.8. Europe Market Size and Forecast, By Process

19.9. Europe Market Size and Forecast, By Generation

19.10. Europe Market Size and Forecast, By Packaging

19.11. Europe Market Size and Forecast, By Distribution Channel

19.12. Europe Market Size and Forecast, By Country

19.12.1. United Kingdom

19.12.2. France

19.12.3. Germany

19.12.4. Italy

19.12.5. Spain

19.12.6. Sweden

19.12.7. Russia

19.12.8. Rest of Europe

20. Asia Pacific Coffee Market Size and Forecast By Segmentation (By Value USD Million and Volume Tons) (2025-2032)

20.1. Asia Pacific Market Size and Forecast, By Product Type

20.2. Asia Pacific Market Size and Forecast, By Nature

20.3. Asia Pacific Market Size and Forecast, By Origin

20.4. Asia Pacific Market Size and Forecast, By Roast Type

20.5. Asia Pacific Market Size and Forecast, By Flavor

20.6. Asia Pacific Market Size and Forecast, By Price Range

20.7. Asia Pacific Market Size and Forecast, By Coffee Species

20.8. Asia Pacific Market Size and Forecast, By Process

20.9. Asia Pacific Market Size and Forecast, By Generation

20.10. Asia Pacific Market Size and Forecast, By Packaging

20.11. Asia Pacific Market Size and Forecast, By Distribution Channel

20.12. Asia Pacific Market Size and Forecast, By Country

20.12.1. China

20.12.2. Japan

20.12.3. South Korea

20.12.4. India

20.12.5. Australia

20.12.6. Malaysia

20.12.7. Thailand

20.12.8. Vietnam

20.12.9. Indonesia

20.12.10. Philippines

20.12.11. Rest of Asia Pacific

21. Middle East and Africa Coffee Market Size and Forecast By Segmentation (By Value USD Million and Volume Tons) (2025-2032)

21.1. Middle East and Africa Market Size and Forecast, By Product Type

21.2. Middle East and Africa Market Size and Forecast, By Nature

21.3. Middle East and Africa Market Size and Forecast, By Origin

21.4. Middle East and Africa Market Size and Forecast, By Roast Type

21.5. Middle East and Africa Market Size and Forecast, By Flavor

21.6. Middle East and Africa Market Size and Forecast, By Price Range

21.7. Middle East and Africa Market Size and Forecast, By Coffee Species

21.8. Middle East and Africa Market Size and Forecast, By Process

21.9. Middle East and Africa Market Size and Forecast, By Generation

21.10. Middle East and Africa Market Size and Forecast, By Packaging

21.11. Middle East and Africa Market Size and Forecast, By Distribution Channel

21.12. Middle East and Africa Market Size and Forecast, By Country

21.12.1. South Africa

21.12.2. GCC

21.12.3. Nigeria

21.12.4. Egypt

21.12.5. Turkey

21.12.6. Rest of ME&A

22. South America Coffee Market Size and Forecast By Segmentation (By Value USD Million and Volume Tons) (2025-2032)

22.1. South America Market Size and Forecast, By Product Type

22.2. South America Market Size and Forecast, By Nature

22.3. South America Market Size and Forecast, By Finish

22.4. South America Market Size and Forecast, By Roast Type

22.5. South America Market Size and Forecast, By Flavor

22.6. South America Market Size and Forecast, By Price Range

22.7. South America Market Size and Forecast, By Coffee Species

22.8. South America Market Size and Forecast, By Process

22.9. South America Market Size and Forecast, By Generation

22.10. South America Market Size and Forecast, By Packaging

22.11. South America Market Size and Forecast, By Distribution Channel

22.12. South America Market Size and Forecast, By Country

22.12.1. Brazil

22.12.2. Argentina

22.12.3. Colombia

22.12.4. Chile

22.12.5. Rest Of South America

23. Company Profile: Key Players

23.1. Nestle SA

23.1.1. Company Overview

23.1.2. Business Portfolio

23.1.3. Financial Overview

23.1.4. SWOT Analysis

23.1.5. Strategic Analysis

23.1.6. Recent Developments

23.2. Tchibo GmbH

23.3. Strauss Group (Strauss Coffee)

23.4. Lavazza

23.5. Keurig Dr Pepper (Keurig division)

23.6. Jacobs Douwe Egberts / JDE Peet’s

23.7. Tata Consumer Products (Eight O’Clock Coffee)

23.8. UCC Ueshima Coffee Co.

23.9. Melitta Group

23.10. Illy (Illycaffè)

23.11. Massimo Zanetti Beverage Group

23.12. Eight O’Clock Coffee Company

23.13. Starbucks Corporation

23.14. Peet’s Coffee

23.15. Coffee Bean & Tea Leaf

23.16. Segafredo Zanetti

23.17. Farmer Bros. Co.

23.18. Caribou Coffee Company

23.19. Death Wish Coffee Company

23.20. Hawaiian Isles Kona Coffee Company

23.21. Gevalia

23.22. Dallmayr

23.23. Kicking Horse Coffee

23.24. Stumptown Coffee Roasters

23.25. Louis Dreyfus Co. Mexico

23.26. Olam Agro Mexico

23.27. Sabormex

23.28. Café El Marino S.A. de C.V.

23.29. Café Punta del Cielo

23.30. Ruta Maya Coffee

23.31. Cabo Coffee Company

24. Key Findings

25. Industry Recommendations