Facility Management Market - Industry Analysis and Forecast (2026-2034) By Service Type, Technology, End-Use

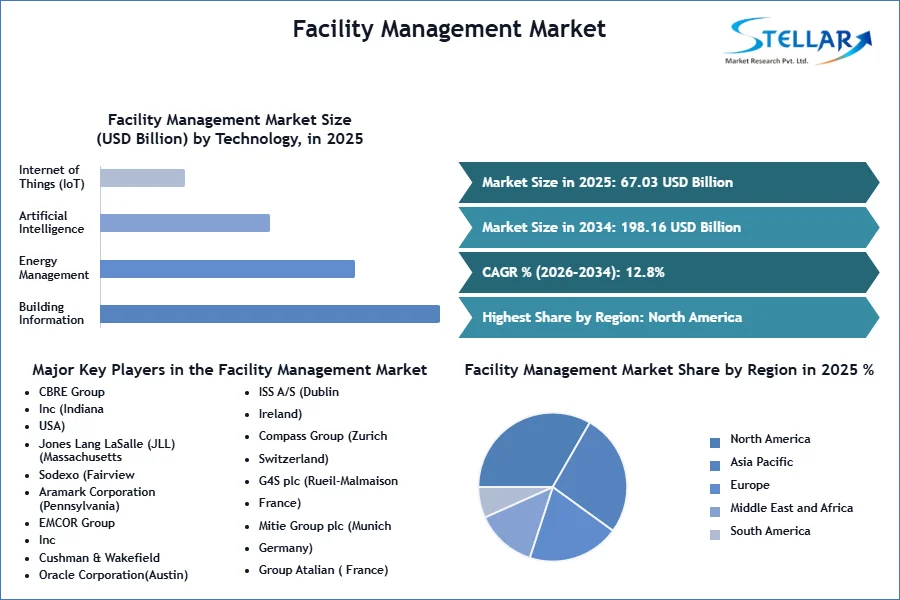

Global Facility Management Market size was valued at USD 67.03 Bn in 2025 and is expected to reach USD 198.16 Bn by 2034, at a CAGR of 12.8%.

Facility Management Market Overview

The global facility management market, essential for optimizing physical workplaces in alignment with organizational goals, encompasses a diverse range of competencies including emergency preparedness, sustainability practices, and efficient real estate management. Technology plays a pivotal role in enhancing facility management markets’ efficiency and effectiveness, with industry leaders such as IBM Corporation, Oracle Corporation, and SAP SE driving innovation through strategic mergers and partnerships. These collaborations strengthen capabilities, exemplified by Oracle's acquisition of Landmark Elevator and SAP SE's partnership with Honeywell to integrate cloud-based solutions for streamlined operational data management.

North America leads the facility management market adoption, spurred by market trends favoring adaptable workspaces and the rapid expansion of smart buildings. Leveraging advanced technologies like artificial intelligence (AI), Internet of Things (IoT), and automation, these smart buildings enhance energy efficiency, occupant comfort, and operational simplicity. Key companies in the facility management market like ABM Industries Inc. and Atlas Facilities Management Ltd. are prominent in offering comprehensive facility management services, including HVAC solutions and facility operation services, reflecting a growing preference for outsourcing to optimize costs and concentrate on core business activities.

In the Middle East and Africa, substantial growth opportunities arise from extensive infrastructure investments, particularly in Qatar and Saudi Arabia. These investments, driven by initiatives such as the Qatar 2022 FIFA World Cup and significant allocations to healthcare and education sectors, underscore a burgeoning demand for sustainable buildings and robust facility management services. South Africa, as a mature facility management market, emphasizes skill development and regulatory frameworks that promote service excellence and outsourcing efficiencies.

Despite technological advancements driving market growth, the facility management market faces challenges, notably a persistent shortage of skilled laborers. This shortage poses a significant hurdle amidst increasing demand for updated technological systems and sustainable practices. Looking ahead, the facility management market is poised for expansion globally, fueled by continued innovation in smart technologies and the rising imperative for sustainable infrastructure solutions worldwide.

To get more Insights: Request Free Sample Report

IoT and AI Integration: Major Trends Driving the Facility Management Market

The facility management industry is undergoing a significant transformation driven by rapid technological advancements and evolving client expectations. Key trends in the facility management market include the adoption of IoT and AI technologies by market leaders like CBRE Group and JLL, enhancing real-time monitoring and operational efficiency while reducing costs. Sustainability is increasingly pivotal, with companies such as ISS and Sodexo integrating green practices and renewable energy solutions to meet regulatory standards and appeal to environmentally conscious clients. This shift towards more integrated facility management solutions, exemplified by Farnek's HITEK and JLL's comprehensive approaches, streamlines services like maintenance and security, improving overall efficiency and client satisfaction. Smart buildings, supported by IoT sensors and digital twins, are also on the rise, optimizing space utilization and enhancing user experiences. Meanwhile, facility management providers are focusing on enhancing user comfort and wellness through ergonomic designs and personalized services, contributing to improved tenant retention and client attraction.

Emerging market trends such as AI-IoT convergence, the proliferation of smart building technologies, and the integration of sustainability practices are poised to drive significant growth in the facility management market. These advancements enable more efficient, environmentally friendly, and user-centered solutions, necessitating investments in technology infrastructure, workforce skills, and strategic partnerships to capitalize effectively on these market trends.

Facility Management Market Dynamics:

Technological Advancements and Sustainability Practices: Key Drivers of Facility Management Market Growth

In the facility management market, there has been dynamic change through the evolutionary steps of technological advancement in domains like IoT, AI, and cloud computing. For example, some of the technologies CBRE Group and ISS A/S are implementing to bring about operational efficiency, predictive maintenance, and energy optimization include IoT sensors and AI analytics. This innovation offers real-time monitoring, data-driven decision-making, and automation, driving cost savings and service excellence.

The same period has seen an increased demand for integrated facility management solutions, typified by JLL and Sodexo, able to revel in the smoothing of operations from hard to soft services, reducing administrative burdens, and improving cost efficiencies. Other than this, the providers from the facility management market such as Farnek and Mitie Group, consider the challenge to maintain sustainable practices, answer regulatory demands, and have the appeal of being greasy to clients. Outsourcing of non-core functions, led by Compass Group and EMCOR Group, further rationalizes operations, while smart building technologies championed by Jones Lang LaSalle promote efficiency, comfort, and sustainability. These market trends underline the dynamic growth opportunities driven by urbanization, infrastructure development, and evolving client needs around the world.

High Initial Investments and Regulatory Complexity: Significant Challenges Facing the Facility Management Market

The facility management market faces challenges such as high initial investments in advanced technologies like AI, IoT, and smart building solutions, particularly burdensome for smaller enterprises and developing companies in the facility management market. Strategies to mitigate these challenges include phased technology adoption focusing on high ROI areas like predictive maintenance, alongside exploring financing options, partnerships, and government incentives. Regulatory compliance complexities require robust frameworks integrating real-time monitoring and automated reporting, complemented by staff training and digital tools for streamlined documentation and audit preparedness. Collaboration with regulatory bodies ensures ongoing adherence to evolving standards in the facility management market and minimizes compliance risks effectively.

AI, IoT Integration, and Sustainability Initiatives: Key Opportunities Driving the Facility Management Market

The facility management market is poised for growth through innovations like AI and predictive analytics, enhancing operational efficiency and cost savings. IoT applications are expanding in energy management and smart buildings, driving revenue in Asia Pacific and Latin America. Healthcare facilities offer specialized opportunities, emphasizing patient-centric care and regulatory compliance. Sustainability initiatives, including green certifications, are pivotal, supporting eco-friendly practices and client preferences. Corporate real estate outsourcing trends and smart city integration further propel market expansion, while focusing on enhancing employee experience through workplace wellness and digital solutions underscores service differentiation and growth opportunities. These market trends enable facility management market players to meet diverse sector demands with innovative solutions and sustainable practices, enhancing operational excellence and client satisfaction globally.

Facility Management Market Segment Analysis:

By Service Type

The facility management market offers a diverse range of service types crucial for maintaining and optimizing physical assets efficiently. It is segmented into Hard Services, encompassing technical aspects like mechanical maintenance and HVAC systems managed by companies such as CBRE Group Inc. and JLL; Soft Services, focusing on user comfort and safety through services like cleaning and security provided by Sodexo and Compass Group; and Integrated Facility Management (IFM), combining both hard and soft services for streamlined operations and cost efficiency offered by Mitie Group plc and ISS A/S. Additionally, specialized services including sustainability consulting and smart building technologies deployment cater to evolving demands, highlighting the facility management market's commitment to enhancing operational environments and client satisfaction.

By Technology

In the facility management market, the Technology Subsegment analysis highlights transformative technologies that enhance operational efficiency, sustainability, and user experience across industries. AI technologies from IBM Watson IoT, Schneider Electric, and Siemens AG enable predictive analytics and automation, optimizing energy usage and maintenance. IoT solutions by Johnson Controls, Honeywell Building Technologies, and Bosch Building Technologies offer real-time data insights for smart building management, improving energy efficiency and space utilization. BIM technologies from Autodesk and Nemetschek Group facilitate digital building management, enhancing collaboration and lifecycle asset management. EMS platforms by Schneider Electric, Siemens AG, and ABB monitor and optimize energy consumption, supporting regulatory compliance and cost savings. These technologies, along with advanced analytics, cloud computing, robotics, and AR, drive efficiency and sustainability in facility management, shaping market growth and competitive advantage globally.

By End-Use

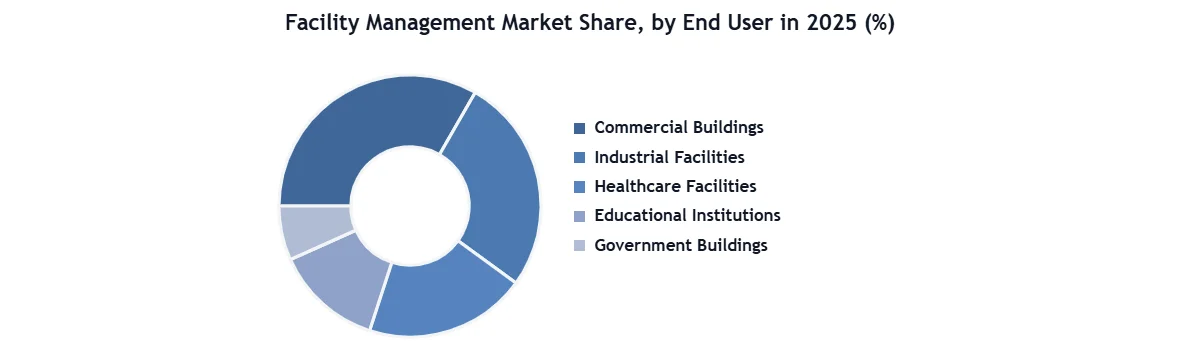

In the facility management market, the End-user Segment analysis highlights sectors such as Commercial Buildings, where CBRE Group Inc., Cushman & Wakefield, and Jones Lang LaSalle (JLL) offer integrated services for office spaces and retail centers, enhancing operational efficiency and tenant satisfaction. Industrial Facilities, served by EMCOR Group, Inc. and G4S plc, focus on specialized maintenance and safety to optimize productivity and compliance. Healthcare Facilities, managed by Sodexo and Aramark Corporation, prioritize patient care through biomedical equipment maintenance and sterile environment management.

Educational Institutions, supported by Compass Group and Mitie Group plc, emphasize safety and sustainability to foster conducive learning environments. Government Buildings, managed by ISS A/S and Cushman & Wakefield, ensure regulatory compliance and public infrastructure maintenance. Residential Buildings benefit from Mitie Group plc and Compass Group's services, enhancing tenant satisfaction and property management efficiency. Other segments like cultural institutions, sports venues, transportation hubs, and data centers have unique facility management needs addressed by specialized providers, facilitating operational excellence and industry-specific compliance. Understanding these diverse needs enables service providers to deliver tailored solutions that optimize efficiency, sustainability, and client strategic objectives across varied sectors and industries.

Facility Management Market Regional Insights

North America dominates the global facility management market, driven by the wide-ranging implementation of cutting-edge technologies and a strong regulatory framework. The United States forms a significant portion of the facility management market due to its heavy investment in smart building technologies, sustainability initiatives, and sophisticated facility management solutions. Firms like CBRE Group, Inc. and Jones Lang LaSalle (JLL) lead the facility management market through integrated services that achieve enhanced building performance, reduced operational costs, and better tenant satisfaction. Such companies are able to extract value from data analytics, IoT, AI, and BIM to deliver facility management solutions that are customized for commercial, industrial, and healthcare sectors to improve operational efficiency and create better workplace experiences.

The facility management market dynamics in North America are majorly driven by the need to attain sustainability and energy efficiency through government regulations and corporate mandates that address reducing carbon emissions. Notably, features of this region include the development of IoT applications in real-time monitoring and predictive maintenance aimed at optimizing building operations for occupant comfort. These would include client-managed service models and strategic joint ventures to deliver integrated facility management solutions with an assurance of innovation and service excellence within North America's dynamic market.

Europe is a leading region in the global facility management market, driven by stringent environmental regulations and widespread adoption of smart building technologies. Key countries such as Germany and the United Kingdom lead in facility management market share due to their proactive sustainability efforts and innovative facility management practices. ISS A/S from Denmark and Sodexo from France are prominent players, offering integrated services and leveraging AI and digitalization to optimize operations in commercial and public sectors. Europe's market dynamics include a focus on energy efficiency through technologies like BIM and EMS, alongside initiatives promoting green certifications and circular economy practices.

Competitive Landscape of the Facility Management Market

The global facility management market is fiercely competitive, with companies competing to offer comprehensive solutions ranging from hard and soft services to integrated facility management (IFM) and advanced technologies. Key players in the facility management market like CBRE Group, Inc. and Jones Lang LaSalle (JLL) lead the facility management market with distinct strategic approaches. CBRE integrates IoT and AI technologies to optimize operational efficiency and attract multinational corporations and institutional investors seeking comprehensive real estate solutions. In contrast, JLL focuses on sustainable and technology-driven solutions, investing in AI-powered analytics and smart building technologies to enhance user experience and operational effectiveness. Both companies leverage their global presence, diverse service offerings, and technological innovations to maintain leadership in the competitive facility management landscape.

Facility Management Market Scope

|

Facility Management Market Scope |

|

|

Market Size in 2025 |

USD 67.03 Bn. |

|

Market Size in 2034 |

USD 198.16 Bn. |

|

CAGR (2026-2034) |

12.8% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Facility Management Market Segments |

By Service Type Hard Services Soft Services Integrated Facility Management other services |

|

By Technology Building Information Modeling (BIM) Energy Management Systems (EMS) Artificial Intelligence (AI) Internet of Things (IoT) Other Technology |

|

|

|

By End-Use Commercial Buildings Industrial Facilities Healthcare Facilities Educational Institutions Government Buildings Residential Buildings Other |

|

Regional Scope |

North America - (United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - ( South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Facility Management Market Key players

North America

- CBRE Group, Inc (Indiana, USA)

- Jones Lang LaSalle (JLL) (Massachusetts, USA)

- Sodexo (Fairview, USA)

- Aramark Corporation (Pennsylvania)

- EMCOR Group, Inc

- Cushman & Wakefield

- Oracle Corporation(Austin)

Europe

- ISS A/S (Dublin, Ireland)

- Compass Group (Zurich, Switzerland)

- G4S plc (Rueil-Malmaison, France)

- Mitie Group plc (Munich, Germany)

- Group Atalian ( France)

Asia Pacific

- Aden group (Singapore)

- Aeon Delight Co., Ltd (Tokyo, Japan)

- Broadspectrum (Ventia) (Australia)

- EXZY COMPANY LIMITED (Thailand)

Middle East and Africa (MEA)

- EFS Facilities Services Group (Dubai, UAE)

- Oman International Services Holding Company ( Oman)

- Imdaad LLC (Dubai, UAE)

- Khidmah LLC (Abu Dhabi, UAE)

South America

- Grupo Brasanitas ( Brazil)

- GRSA (Grupo de Soluções em Alimentação) ( Brazil)

- Temon Service (Buenos Aires, Argentina)

Frequently Asked Questions

Ans. Smart building technologies, sustainability initiatives, data analytics, and integrated service solutions.

Ans. It promotes energy efficiency, waste reduction, and compliance with green building standards.

Ans. By automating operations, optimizing space usage, enhancing security, and providing real-time insights.

Ans. Aging infrastructure, cost management, technology adoption, skilled labor shortage, and regulatory compliance.

Ans. Expansion in emerging markets, specialized service offerings, innovation with IoT and AI, and sustainable solutions.

Ans. Integrated Facility Management (IFM) due to comprehensive service offerings across sectors.

Ans. Towards integrated, sustainable solutions with a focus on efficiency, technology integration, and personalized service delivery.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Facility Management Market Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2034) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Facility Management Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Service Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Service Launches and Innovations

3.5. Facility Management Industry Ecosystem

3.5.1. Ecosystem Analysis

3.5.2. Role of the Companies in the Ecosystem

4. Facility Management Market: Dynamics

4.1. Facility Management Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Facility Management Market Drivers

4.3. Facility Management Market Restraints

4.4. Facility Management Market Opportunities

4.5. Facility Management Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape

4.9.1. Market Regulation by Region

4.9.1.1. North America

4.9.1.2. Europe

4.9.1.3. Asia Pacific

4.9.1.4. Middle East and Africa

4.9.1.5. South America

4.9.2. Impact of Regulations on Market Dynamics

4.9.3. Government Schemes and Initiatives

5. Facility Management Market: Global Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

5.1. Facility Management Market Size and Forecast, by Service Type (2026-2034)

5.1.1. Hard Services

5.1.2. Soft Services

5.1.3. Integrated Facility Management

5.1.4. Other Services

5.2. Facility Management Market Size and Forecast, by Technology (2026-2034)

5.2.1. Building Information Modeling (BIM)

5.2.2. Energy Management Systems (EMS)

5.2.3. Artificial Intelligence (AI)

5.2.4. Internet of Things (IoT)

5.2.5. Other Technology

5.3. Facility Management Market Size and Forecast, by End-Use (2026-2034)

5.3.1. Commercial Buildings

5.3.2. Industrial Facilities

5.3.3. Healthcare Facilities

5.3.4. Educational Institutions

5.3.5. Government Buildings

5.3.6. Residential Buildings

5.3.7. Other

5.4. Facility Management Market Size and Forecast, by Region (2026-2034)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Facility Management Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

6.1. North America Facility Management Market Size and Forecast, by Service Type (2026-2034)

6.1.1. Hard Services

6.1.2. Soft Services

6.1.3. Integrated Facility Management

6.1.4. Other Services

6.2. North America Facility Management Market Size and Forecast, by Technology (2026-2034)

6.2.1. Building Information Modeling (BIM)

6.2.2. Energy Management Systems (EMS)

6.2.3. Artificial Intelligence (AI)

6.2.4. Internet of Things (IoT)

6.2.5. Other Technology

6.3. North America Facility Management Market Size and Forecast, by End-Use (2026-2034)

6.3.1. Commercial Buildings

6.3.2. Industrial Facilities

6.3.3. Healthcare Facilities

6.3.4. Educational Institutions

6.3.5. Government Buildings

6.3.6. Residential Buildings

6.3.7. Other

6.4. North America Facility Management Market Size and Forecast, by Country (2026-2034)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Facility Management Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

7.1. Europe Facility Management Market Size and Forecast, by Service Type (2026-2034)

7.2. Europe Facility Management Market Size and Forecast, by Technology (2026-2034)

7.3. Europe Facility Management Market Size and Forecast, by End-Use (2026-2034)

7.4. Europe Facility Management Market Size and Forecast, by Country (2026-2034)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Russia

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Facility Management Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

8.1. Asia Pacific Facility Management Market Size and Forecast, by Service Type (2026-2034)

8.2. Asia Pacific Facility Management Market Size and Forecast, by Technology (2026-2034)

8.3. Asia Pacific Facility Management Market Size and Forecast, by End-Use (2026-2034)

8.4. Asia Pacific Facility Management Market Size and Forecast, by Country (2026-2034)

8.4.1. China

8.4.2. India

8.4.3. Japan

8.4.4. South Korea

8.4.5. Australia

8.4.6. ASEAN

8.4.7. Rest of Asia Pacific

9. Middle East and Africa Facility Management Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

9.1. Middle East and Africa Facility Management Market Size and Forecast, by Service Type (2026-2034)

9.2. Middle East and Africa Facility Management Market Size and Forecast, by Technology (2026-2034)

9.3. Middle East and Africa Facility Management Market Size and Forecast, by End-Use (2026-2034)

9.4. Middle East and Africa Facility Management Market Size and Forecast, by Country (2026-2034)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Egypt

9.4.4. Nigeria

9.4.5. Rest of ME&A

10. South America Facility Management Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

10.1. South America Facility Management Market Size and Forecast, by Service Type (2026-2034)

10.2. South America Facility Management Market Size and Forecast, by Technology (2026-2034)

10.3. South America Facility Management Market Size and Forecast, by End-Use (2026-2034)

10.4. South America Facility Management Market Size and Forecast, by Country (2026-2034)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. CBRE Group, Inc (Indiana, USA)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Jones Lang LaSalle (JLL) (Massachusetts, USA)

11.3. Sodexo (Fairview, USA)

11.4. Aramark Corporation (Pennsylvania)

11.5. EMCOR Group, Inc

11.6. Cushman & Wakefield

11.7. Oracle Corporation(Austin)

11.8. ISS A/S (Dublin, Ireland)

11.9. Compass Group (Zurich, Switzerland)

11.10. G4S plc (Rueil-Malmaison, France)

11.11. Mitie Group plc (Munich, Germany)

11.12. Group Atalian ( France)

11.13. Aden group (Singapore)

11.14. Aeon Delight Co., Ltd (Tokyo, Japan)

11.15. Broadspectrum (Ventia) (Australia)

11.16. EXZY COMPANY LIMITED (Thailand)

11.17. EFS Facilities Services Group (Dubai, UAE)

11.18. Oman International Services Holding Company ( Oman)

11.19. Imdaad LLC (Dubai, UAE)

11.20. Khidmah LLC (Abu Dhabi, UAE)

11.21. Grupo Brasanitas ( Brazil)

11.22. GRSA (Grupo de Soluções em Alimentação) ( Brazil)

11.23. Temon Service (Buenos Aires, Argentina)

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook