Global Intraosseous Infusion Devices Market Size, Revenue Analysis and Industry Outlook (2026-2032)

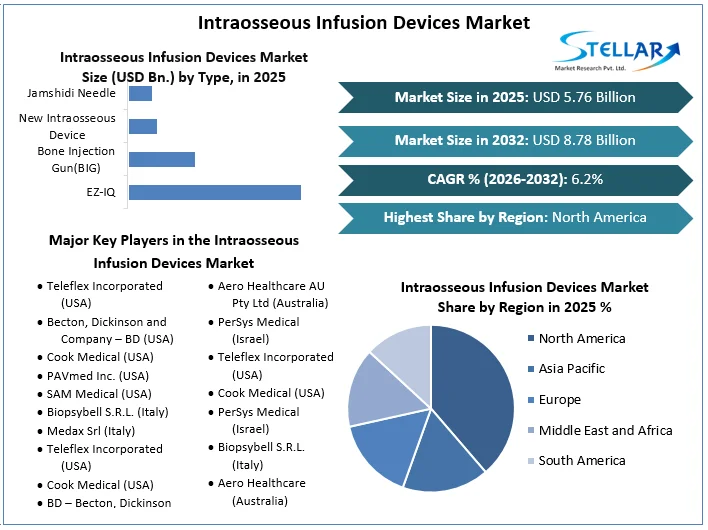

Intraosseous Infusion Devices Market Size was valued at USD 5.76 Bn. In 2025, the total Intraosseous Infusion Devices revenue is expected to grow by CAGR 6.2% from 2026 to 2032 and reach nearly USD 8.78 Bn. In 2032.

Intraosseous Infusion Devices Market Overview:

Intraosseous Infusion Devices (IO) are specialized tools used to establish vascular access through bone marrow, particularly in emergency situations when intravenous access (IV) is difficult or delayed. These devices allow rapid administration of fluids, blood products and medicines directly in the systemic circulation through the spinal cavity of a bone. Intraosseous Infusion Devices that fit the vascular access device are the devices used at the time of emergencies, where a rapid infusion of clinical treatment is performed. The growth of Intraosseous Infusion Devices (IO devices) is mainly attributed to their various benefits. IO devices are designed to maximise efficiency, safety eliminate unnecessary services and decrease treatment time. A sedentary lifestyle also determines Intraosseous Infusion Devices market growth as it causes various diseases, such as kidney disease in the final stage, COPD, urological diseases, cardiovascular disease, etc. Such chronic clinical conditions brought demand for vascular access devices during the forecast period.

According to American Heart Association report, with compiled data from the Centres for Disease Control and Prevention, the National Institutes of Health and other government sources, cardiovascular disease is a leading cause for death globally, associated with 17.3 Mn. deaths per year, which is further expected to increase to 23.6 Mn. by end of 2030.

As of April 2025, the United States implemented new import tariffs on medical devices, directly impacting intraosseous infusion devices. Previously subject to low or zero duties, these devices now face a universal 10% tariff on all imports. Moreover, imports from specific regions are subject to higher rates.

To get more Insights: Request Free Sample Report

Intraosseous Infusion Devices Market Dynamic:

Growing patient awareness about newly introduced treatment procedures to boost the Intraosseous Devices Market growth

The combination of growing patient awareness, government initiatives and technological advances is boosting the Intraosseous Infusion Devices market. As more health professionals become able to use these devices and, as patients become more informed about their benefits, the adoption of IO devices in emergency environments and intensive care continues its upward trajectory.

Government initiatives are also playing a crucial role in improving patient awareness and increasing the medical device policy of the Intraosseous Infusion Devices market in 2024, which aims to facilitate the orderly growth of the medical device sector to meet access objectives, accessibility, quality and innovation in public health. The Production Incentive Scheme (PLI) was introduced to promote domestic manufacturing of medical devices, including IO devices, providing financial incentives. A platform of medical devices established to reduce manufacturing costs and promote innovation in the medical device sector. These initiatives not only support the manufacturing sector but also indirectly contribute to increasing patient awareness, improving the availability and accessibility of advanced medical devices.

High cost associated with intraosseous infusion devices Impact limits Intraosseous Infusion Devices Market growth

The cost of Costs associated with the Intraosseous Infusion Devices (IO) significantly affect their adoption, especially in low-income and limited-resource settings. These devices are required, expensive for fast emergency vascular access cess, depending on the type and accessories of the device, prices ranging from USD 99 to USD 6,000 per unit. Such costs pose challenges for widespread implementation, especially in public health systems with restricted budgets. While the Global Intraosseous Infusion Device Market is expected to grow with highest CAGR, financial constraints are a significant barrier. Strategies such as collective purchases, development of economically reusable devices and local production are being searched to reduce costs and improve availability in the needy regions to increase accessibility.

Growth in the number of government and regulatory approvals to Boost in Intraosseous Infusion Devices Market

The global Intraosseous Infusion Devices (IO) market is experiencing significant growth, driven in part by an increase in government and regulatory approvals. These approvals are facilitating the introduction of advanced IO devices, improving emergency medical care worldwide. Regulatory agencies such as the US Food and Drug Administration (FDA) and the European Medicines Agency (EMA) were fundamental in approving new IO devices, ensuring that they meet strict safety and effectiveness standards.

For example, in June 2023, the incorporated Teleflex received FDA 510 (K) off for its EZ-IO arrow needle, a critical component of its intraosseous vascular access system. Such approvals not only validate the safety of these devices but also encourage their adoption in clinical environments.

Intraosseous Infusion Devices Market Segmentation:

Based on Type the Intraosseous Infusion Devices Market Segmented into EZ-IQ, Bone Injection Gun (BIG), New Intraosseous Device, Jamshidi Needle. EZ-IQ segment Dominated the market in 2025 and is expected to hold the largest share during the forecast period. The type of Intraosseous Infusion Device accounted for 21.5% in the Intraosseous Infusion Device Industry. The high growth of this product category is attributed to its rapid response and ensured intraosseous access in less than 30 seconds, thus favoured under critical and emergency medical conditions.

These devices are particularly valued due to their reliability to enable quick vascular access where conventional methods are unviable or take a long to achieve. The growing traction of EZ-IO devices by healthcare professionals shows their significance in improving patient outcomes and thereby securing their continued leadership in the market globally for intraosseous infusion solutions.

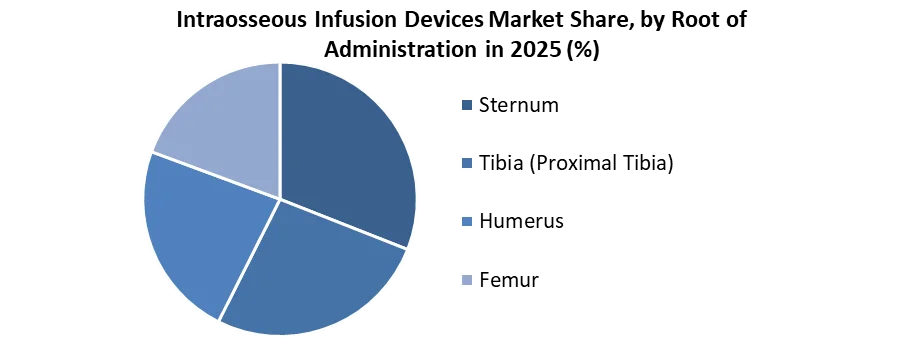

Based on Root of Administration the Intraosseous Infusion Devices Market is Segmented into Sternum, Tibia Proximal Tibia), Humerus and Femur. Sternum segment dominated the Intraosseous Infusion Device market in 2025 and is expected to hold largest share during the forecast period. Sternum segment is expected to be the most lucrative route of administration in the Intraosseous Infusion Devices market, with a huge market share of 30.9%. This enables the surge in growing preference for high-quality care and accuracy in determining the right interventions to be adopted, especially in critical and emergency situations.

The sternum offers advantages in access and efficiency over distal and proximal tibia routes and, therefore, is a preferred route for healthcare professionals. Such trends are likely to constitute the factors driving the growth of the Intraosseous Infusion Devices Market shortly due to the presence of this growing factor.

The expanding acceptance of technologically advanced music for intraosseous infusion practices to support better patient outcomes. The sternum's unique strategic anatomical position and rapid vascular access firmly make it a stronghold in the intraosseous infusion devices industry.

Based on End User the Intraosseous Infusion Device Market Is segmented into Hospitals, Emergency Medical Services (EMS), Military and Defense, Ambulatory surgical Centers and Training and Education Centers. The Hospital segment dominated the market in 2025 and is expected to hold the largest share during the forecast period. The increased sophistication in demand for IO devices in emergency and critical care scenarios is the underpinnings of that leading market segment. Continual advances in technology, alongside the adoption of new scientific innovations, have enhanced the efficacy and dependability of these devices, thereby ensuring providers that the devices are indispensable. Growth continues to be propelled by an increased focus among health providers on bettering patient outcomes, assuring the market continued expansion.

Based on regional North America dominated the Intraosseous Infusion Devices Market in 2025 with the revenue share of 41.33% and is expected to hold the largest industry share during the forecast period. The factors such as well-established reimbursement policies, strong medical infrastructure, the existence of key players such as Teleflex Incorporated, Becton Dickinson Company, Cardinal Health, Inc. and Cook Group, and technological advancement in Intraosseous Infusion Devices Boost market growth. The combination of all these significant factors will make North America the most promising regional market over the forecast period.

Intraosseous Infusion Devices Competitive Landscape:

The Intraosseous Infusion Device Industry is highly competitive, dominated by key emerging Players in industry, such as Teleflex Incorporated (EZ-CIO System manufacturer), Becon, Dickinson and Company (BD), Cook Medical and Pavmed Inc., which developed the Portio system. Companies like Pyng Medical (Fast1), Persys Medical, Aero Healthcare and Biopsybell also play crucial roles. These companies are focused on technological advances, product innovation and strategic acquisitions to strengthen their global presence. For example, the acquisition of Teleflex da Vida Care and the acquisition of Straub Medical BD expanded its vascular access portfolios. The market is driven by increased demand for rapid vascular access to emergency care and trauma, FDA approvals for expanded use and growing adoption in military and pre-hospital environments. Emerging markets in Asia-Pacific and Latin America are offering new growth opportunities, making the competitive landscape dynamic and innovative innovation oriented guided by innovation.

|

Global Intraosseous Infusion Devices Market |

|

|

Market Size in 2025 |

USD 5.76 Bn. |

|

Market Size in 2032 |

USD 8.78 Bn. |

|

CAGR (2026-2032) |

6.2% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Type EZ-IQ Bone Injection Gun(BIG) New Intraosseous Device Jamshidi Needle |

|

By Root of Administration Sternum Tibia (Proximal Tibia) Humerus Femur |

|

|

By End Use Hospitals Emergency Medical services Military and Defence Ambulatory Surgical Centres |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, South Korea, Japan, India, Australia, Indonesia, Philippines, Malaysia, Vietnam, Thailand Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in Global Intraosseous Infusion Devices Industry

North America

- Teleflex Incorporated (USA)

- Becton, Dickinson and Company – BD (USA)

- Cook Medical (USA)

- PAVmed Inc. (USA)

- SAM Medical (USA)

Europe

- Biopsybell S.R.L. (Italy)

- Medax Srl (Italy)

- Teleflex Incorporated (USA)

- Cook Medical (USA)

- BD – Becton, Dickinson and Company (USA)

Asia Pacific

- Teleflex Incorporated (USA)

- Cook Medical (USA)

- BD – Becton, Dickinson and Company (USA)

- Aero Healthcare AU Pty Ltd (Australia)

- PerSys Medical (Israel)

Middle East & Africa

- Teleflex Incorporated (USA)

- Cook Medical (USA)

- PerSys Medical (Israel)

- Biopsybell S.R.L. (Italy)

- Aero Healthcare (Australia)

South America

- Teleflex Incorporated (USA)

- Cook Medical (USA)

- PerSys Medical (Israel)

- Aero Healthcare (Australia)

- Biopsybell S.R.L. (Italy)

Frequently Asked Questions

The EZ-IO segment dominated the market in 2025, accounting for 21.5% of the market share. Its popularity is due to its rapid response time, enabling vascular access in under 30 seconds, making it highly preferred in critical and emergency medical conditions.

The sternum route dominated in 2025 with a 30.9% market share. It is preferred due to its strategic anatomical location, offering rapid vascular access and greater efficiency compared to tibia and humerus routes, especially in emergencies.

Growth drivers include increased patient awareness, government initiatives, technological advancements, rising chronic disease prevalence, and the need for rapid vascular access in emergency care. Regulatory approvals and programs like PLI (Production Linked Incentive) further support market expansion.

Key companies include Teleflex Incorporated, Becton, Dickinson and Company (BD), Cook Medical, Pavmed Inc., Pyng Medical, PerSys Medical, Aero Healthcare, and Biopsybell. These firms are focused on innovation, acquisitions, and expanding their global presence through advanced device offerings and regulatory approvals.

1. Intraosseous Infusion Devices Market Introduction

1.1. Study Assumption and Market Definition

1.2. Scope of the Study

1.3. Executive Summary

2. Intraosseous Infusion Devices Market: Competitive Landscape

2.1. Ecosystem Analysis

2.2. SMR Competition Matrix

2.3. Competitive Landscape

2.4. Key Players Benchmarking

2.4.1. Company Name

2.4.2. Business Segment

2.4.3. End-user Segment

2.4.4. Revenue (2025)

2.4.5. Company Locations

2.5. Market Structure

2.5.1. Market Leaders

2.5.2. Market Followers

2.5.3. Emerging Players

2.6. Mergers and Acquisitions Details

3. Intraosseous Infusion Devices Market: Dynamics

3.1. Intraosseous Infusion Devices Market Trends by Region

3.1.1. North America Intraosseous Infusion Devices Market Trends

3.1.2. Europe Intraosseous Infusion Devices Market Trends

3.1.3. Asia Pacific Intraosseous Infusion Devices Market Trends

3.1.4. Middle East and Africa Intraosseous Infusion Devices Market Trends

3.1.5. South America Intraosseous Infusion Devices Market Trends

3.2. Intraosseous Infusion Devices Market Dynamics

3.2.1. Global Intraosseous Infusion Devices Market Drivers

3.2.2. Global Intraosseous Infusion Devices Market Restraints

3.2.3. Global Intraosseous Infusion Devices Market Opportunities

3.2.4. Global Intraosseous Infusion Devices Market Challenges

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

3.5. Regulatory Landscape by Region

3.5.1. North America

3.5.2. Europe

3.5.3. Asia Pacific

3.5.4. Middle East and Africa

3.5.5. South America

3.6. Key Opinion Leader Analysis for Intraosseous Infusion Devices Industry

4. Intraosseous Infusion Devices Market: Global Market Size and Forecast by Segmentation (by Value in USD Bn) (2025-2032)

4.1. Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

4.1.1. Self-service

4.1.2. EZ-IQ

4.1.3. Bone Injection Gun(BIG)

4.1.4. New Intraosseous Device

4.1.5. Jamshidi Needle

4.2. Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

4.2.1. Sternum

4.2.2. Tibia (Proximal Tibia)

4.2.3. Humerus

4.2.4. Femur

4.3. Intraosseous Infusion Devices Market Size and Forecast, By End Use (2025-2032)

4.3.1. Hospitals

4.3.2. Emergency Medical services

4.3.3. Military and Defence

4.3.4. Ambulatory Surgical Centres

4.4. Intraosseous Infusion Devices Market Size and Forecast, by Region (2025-2032)

4.4.1. North America

4.4.2. Europe

4.4.3. Asia Pacific

4.4.4. Middle East and Africa

4.4.5. South America

5. North America Intraosseous Infusion Devices Market Size and Forecast by Segmentation (by Value in USD Bn) (2025-2032)

5.1. North America Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

5.1.1. Self-service

5.1.2. EZ-IQ

5.1.3. Bone Injection Gun(BIG)

5.1.4. New Intraosseous Device

5.1.5. Jamshidi Needle

5.2. North America Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

5.2.1. Sternum

5.2.2. Tibia (Proximal Tibia)

5.2.3. Humerus

5.2.4. Femur

5.3. North America Intraosseous Infusion Devices Market Size and Forecast, By End Use (2025-2032)

5.3.1. Hospitals

5.3.2. Emergency Medical services

5.3.3. Military and Defence

5.3.4. Ambulatory Surgical Centres

5.4. North America Intraosseous Infusion Devices Market Size and Forecast, by Country (2025-2032)

5.4.1. United States

5.4.1.1. United States Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

5.4.1.1.1. Self-service

5.4.1.1.2. EZ-IQ

5.4.1.1.3. Bone Injection Gun(BIG)

5.4.1.1.4. New Intraosseous Device

5.4.1.1.5. Jamshidi Needle

5.4.1.2. United States Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

5.4.1.2.1. Sternum

5.4.1.2.2. Tibia (Proximal Tibia)

5.4.1.2.3. Humerus

5.4.1.2.4. Femur

5.4.1.3. United States Intraosseous Infusion Devices Market Size and Forecast, By End Use (2025-2032)

5.4.1.3.1. Healthcare

5.4.1.3.2. Hospitals

5.4.1.3.3. Emergency Medical services

5.4.1.3.4. Military and Defence

5.4.1.3.5. Ambulatory Surgical Centres

5.4.2. Canada

5.4.2.1. Canada Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

5.4.2.1.1. Self-service

5.4.2.1.2. EZ-IQ

5.4.2.1.3. Bone Injection Gun(BIG)

5.4.2.1.4. New Intraosseous Device

5.4.2.1.5. Jamshidi Needle

5.4.2.2. Canada Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

5.4.2.2.1. Sternum

5.4.2.2.2. Tibia (Proximal Tibia)

5.4.2.2.3. Humerus

5.4.2.2.4. Femur

5.4.2.3. Canada Intraosseous Infusion Devices Market Size and Forecast, By End Use (2025-2032)

5.4.2.3.1. Hospitals

5.4.2.3.2. Emergency Medical services

5.4.2.3.3. Military and Defence

5.4.2.3.4. Ambulatory Surgical Centres

5.4.2.4. Mexico Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

5.4.2.4.1. Self-service

5.4.2.4.2. EZ-IQ

5.4.2.4.3. Bone Injection Gun(BIG)

5.4.2.4.4. New Intraosseous Device

5.4.2.4.5. Jamshidi Needle

5.4.2.5. Mexico Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

5.4.2.5.1. Sternum

5.4.2.5.2. Tibia (Proximal Tibia)

5.4.2.5.3. Humerus

5.4.2.5.4. Femur

5.4.2.6. Mexico Intraosseous Infusion Devices Market Size and Forecast, By End Use (2025-2032)

5.4.2.6.1. Healthcare

5.4.2.6.2. Hospitals

5.4.2.6.3. Emergency Medical services

5.4.2.6.4. Military and Defence

5.4.2.6.5. Ambulatory Surgical Centres

6. Europe Intraosseous Infusion Devices Market Size and Forecast by Segmentation (by Value in USD Bn) (2025-2032)

6.1. Europe Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

6.2. Europe Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

6.3. Europe Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

6.4. Europe Intraosseous Infusion Devices Market Size and Forecast, by Country (2025-2032)

6.4.1. United Kingdom

6.4.1.1. United Kingdom Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

6.4.1.2. United Kingdom Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

6.4.1.3. United Kingdom Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

6.4.2. France

6.4.2.1. France Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

6.4.2.2. France Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

6.4.2.3. France Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

6.4.3. Germany

6.4.3.1. Germany Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

6.4.3.2. Germany Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

6.4.3.3. Germany Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

6.4.4. Italy

6.4.4.1. Italy Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

6.4.4.2. Italy Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

6.4.4.3. Italy Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

6.4.5. Spain

6.4.5.1. Spain Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

6.4.5.2. Spain Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

6.4.5.3. Spain Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

6.4.6. Sweden

6.4.6.1. Sweden Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

6.4.6.2. Sweden Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

6.4.6.3. Sweden Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

6.4.7. Austria

6.4.7.1. Austria Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

6.4.7.2. Austria Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

6.4.7.3. Austria Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

6.4.8. Rest of Europe

6.4.8.1. Rest of Europe Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

6.4.8.2. Rest of Europe Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

6.4.8.3. Rest of Europe Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

7. Asia Pacific Intraosseous Infusion Devices Market Size and Forecast by Segmentation (by Value in USD Bn) (2025-2032)

7.1. Asia Pacific Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

7.2. Asia Pacific Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

7.3. Asia Pacific Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

7.4. Asia Pacific Intraosseous Infusion Devices Market Size and Forecast, by Country (2025-2032)

7.4.1. China

7.4.1.1. China Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

7.4.1.2. China Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

7.4.1.3. China Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

7.4.2. S Korea

7.4.2.1. S Korea Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

7.4.2.2. S Korea Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

7.4.2.3. S Korea Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

7.4.3. Japan

7.4.3.1. Japan Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

7.4.3.2. Japan Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

7.4.3.3. Japan Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

7.4.4. India

7.4.4.1. India Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

7.4.4.2. India Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

7.4.4.3. India Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

7.4.5. Australia

7.4.5.1. Australia Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

7.4.5.2. Australia Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

7.4.5.3. Australia Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

7.4.6. Indonesia

7.4.6.1. Indonesia Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

7.4.6.2. Indonesia Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

7.4.6.3. Indonesia Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

7.4.7. Philippines

7.4.7.1. Phillippines Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

7.4.7.2. Malaysia Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

7.4.7.3. Malaysia Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

7.4.8. Malaysia

7.4.8.1. Malaysia Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

7.4.8.2. Malaysia Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

7.4.8.3. Malaysia Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

7.4.9. Vietnam

7.4.9.1. Vietnam Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

7.4.9.2. Vietnam Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

7.4.9.3. Vietnam Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

7.4.10. Thailand

7.4.10.1. Thailand Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

7.4.10.2. Thailand Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

7.4.10.3. Thailand Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

7.4.11. Rest of Asia Pacific

7.4.11.1. Rest of Asia Pacific Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

7.4.11.2. Rest of Asia Pacific Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

7.4.11.3. Rest of Asia Pacific Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

8. Middle East and Africa Intraosseous Infusion Devices Market Size and Forecast by Segmentation (by Value in USD Bn) (2025-2032)

8.1. Middle East and Africa Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

8.2. Middle East and Africa Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

8.3. Middle East and Africa Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

8.4. Middle East and Africa Intraosseous Infusion Devices Market Size and Forecast, by Country (2025-2032)

8.4.1. South Africa

8.4.1.1. South Africa Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

8.4.1.2. South Africa Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

8.4.1.3. South Africa Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

8.4.2. GCC

8.4.2.1. GCC Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

8.4.2.2. GCC Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

8.4.2.3. GCC Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

8.4.3. Nigeria

8.4.3.1. Nigeria Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

8.4.3.2. Nigeria Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

8.4.3.3. Nigeria Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

8.4.4. Rest of ME&A

8.4.4.1. Rest of ME&A Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

8.4.4.2. Rest of ME&A Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

8.4.4.3. Rest of ME&A Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

9. South America Intraosseous Infusion Devices Market Size and Forecast by Segmentation (by Value in USD Bn) (2025-2032)

9.1. South America Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

9.2. South America Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

9.3. South America Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

9.4. South America Intraosseous Infusion Devices Market Size and Forecast, by Country (2025-2032)

9.4.1. Brazil

9.4.1.1. Brazil Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

9.4.1.2. Brazil Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

9.4.1.3. Brazil Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

9.4.2. Argentina

9.4.2.1. Argentina Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

9.4.2.2. Argentina Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

9.4.2.3. Argentina Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

9.4.3. Rest of South America

9.4.3.1. Rest of South America Intraosseous Infusion Devices Market Size and Forecast, By Type (2025-2032)

9.4.3.2. Rest of South America Intraosseous Infusion Devices Market Size and Forecast, By Root of Administration (2025-2032)

9.4.3.3. Rest of South America Intraosseous Infusion Devices Market Size and Forecast, End Use (2025-2032)

10. Company Profile: Key Players

10.1. Teleflex Incorporated (USA)

10.1.1. Company Overview

10.1.2. Business Portfolio

10.1.3. Financial Overview

10.1.4. SWOT Analysis

10.1.5. Strategic Analysis

10.1.6. Recent Developments

10.2. Becton, Dickinson and Company – BD (USA)

10.3. Cook Medical (USA)

10.4. PAVmed Inc. (USA)

10.5. SAM Medical (USA)

10.6. Biopsybell S.R.L. (Italy)

10.7. Medax Srl (Italy)

10.8. Teleflex Incorporated (USA)

10.9. Cook Medical (USA)

10.10. BD – Becton, Dickinson and Company (USA)

10.11. Teleflex Incorporated (USA)

10.12. Cook Medical (USA)

10.13. BD – Becton, Dickinson and Company (USA)

10.14. Aero Healthcare AU Pty Ltd (Australia)

10.15. PerSys Medical (Israel)

10.16. Teleflex Incorporated (USA)

10.17. Cook Medical (USA)

10.18. PerSys Medical (Israel)

10.19. Biopsybell S.R.L. (Italy)

10.20. Aero Healthcare (Australia)

10.21. Teleflex Incorporated (USA)

10.22. Cook Medical (USA)

10.23. PerSys Medical (Israel)

10.24. Aero Healthcare (Australia)

10.25. Biopsybell S.R.L. (Italy)

11. Key Findings

12. Analyst Recommendations

13. Intraosseous Infusion Devices Market: Research Methodology