Endoscopy Equipment Market - Global Industry Analysis and Forecast 2026-2032 by Product, Application, Hygiene, End User and Region

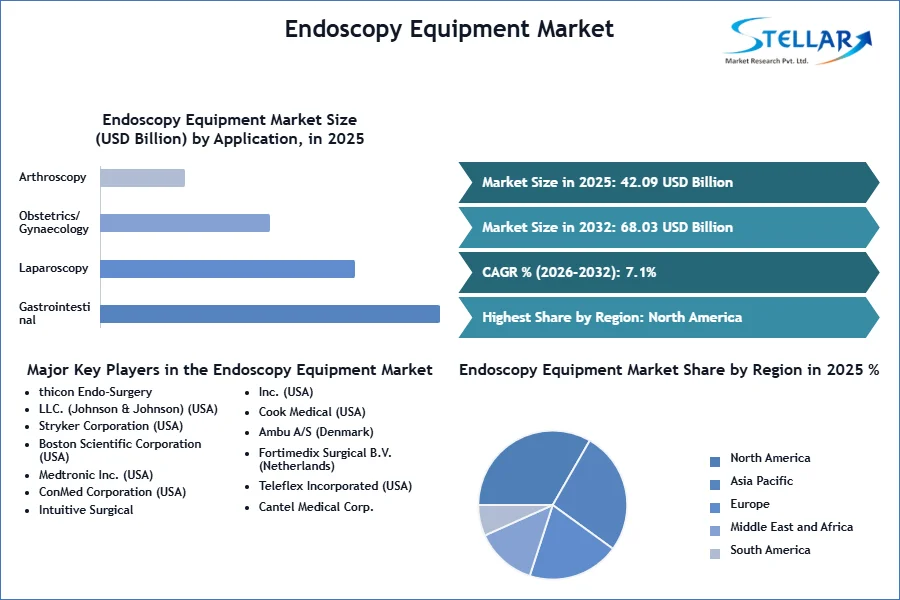

Global Endoscopy Equipment Market size was valued at USD 42.09 Bn. in 2025 and is expected to reach USD 68.03 Bn. by 2032, at a CAGR of 7.1%.

Endoscopy Equipment Market Overview

Endoscopy equipment is special equipment used to visually examine the internal organs and cavities of the body, usually using a flexible or rigid tube with a camera and light source.

The endoscopy equipment market refers to the global industry that produces and supplies equipment used for minimally invasive visual inspection and treatment of the body.

The growing need for less invasive procedures and breakthroughs in imaging technologies are leading to significant growth in the global endoscopy equipment market. Visualization systems are one of the main dominant areas as they play an important role in improving surgical precision and diagnostic accuracy. These systems combine artificial intelligence-based image processing with high-definition cameras to improve results.

Laparoscopy endoscopy is the fastest-growing subsegment that is preferred over open surgery due to its less invasive nature, faster recovery time, and lower risk of complications. The global endoscopy equipment market has benefited from continuous technological advances and the increasing inclination of patients to use less invasive procedures.

Regionally, North American Endoscopy Equipment Market held the largest market share of the Global Endoscopy Equipment Market in 2025 due to strong healthcare infrastructure, high healthcare costs, and continuous technological advancements from leading companies such as Boston Scientific and Medtronic. The Asia-Pacific region, is expected to grow at fastest rate due to the increase in chronic diseases, increasing health investment and government efforts to improve access to health care.

Manufacturers face challenges such as managing different regulatory environments in multiple regions, which affects their ability to develop new products and remain competitive in the market. However, despite these barriers, the market is vibrant, and companies are focusing on R&D to launch advanced technology and grow their global reach. Overall, the endoscopy equipment market is expected to evolve in the future with the world's changing healthcare needs and technological advancements.

To get more Insights: Request Free Sample Report

Endoscopy Equipment Market Trend

Advancements in Endoscopy Equipment: Integrating AI and Portable Technologies for Enhanced Patient Care

A major development in the endoscopy equipment market worldwide was the increasing use of advanced Visualization technologies. This development was motivated by the need for less invasive procedures and more accurate diagnostic tools. One notable example is the incorporation of machine learning algorithms and artificial intelligence (AI) into endoscopic systems. These innovations improve patient outcomes by increasing the accuracy of anomaly detection and diagnosis.

There has been a notable movement toward the creation of small portable endoscopy equipment. These improvements allow greater flexibility in providing care in a variety of clinical settings, such as ambulatory clinics and smaller health facilities.

To improve the vision of tissues and structures during treatment, Olympus and Pentax Medical have produced a new generation of endoscopes equipped with high-definition cameras and complex lenses.

- On 19 April 2023 - PENTAX Medical, a division of HOYA Group, has launched its two newest innovations: the PENTAX Medical INSPIRA™ premium video processor, and the i20c video endoscope series. The video processor acts as the bridge for legacy endoscopes1, bringing them to the next level image quality, whilst the i20c video endoscope series supports procedures with superior vision and ergonomics.

Endoscopy Equipment Market Dynamics

The Rising Prevalence of Chronic Diseases Fuels Demand for Advanced Endoscopy Equipment

The prevalence of chronic diseases across the globe increased the demand for advanced diagnostic and treatment options, which was a major factor influencing the global endoscopy equipment market. Chronic conditions like cancer, lung diseases, and gastrointestinal issues require regular monitoring and treatment, which is often accomplished through minimally invasive endoscopic procedures.

- In September 2023, according to WHO, Cardiovascular diseases account for most NCD deaths, or 17.9 million people annually, followed by cancers (9.3 million), chronic respiratory diseases (4.1 million), and diabetes (2.0 million including kidney disease deaths caused by diabetes).

The need for colonoscopy procedures essential for early detection and intervention has increased due to the increasing incidence of colon cancer worldwide. Using advanced endoscopy technologies such as robotic platforms, AI-assisted image processing and high-definition cameras, doctors can now more accurately identify problems and provide targeted treatment. This improves patient outcomes by enabling early diagnosis and reducing the need for more invasive surgical procedures within the global endoscopy equipment market.

The rising prevalence of chronic diseases, particularly cardiovascular diseases, cancers, chronic respiratory diseases, and diabetes, has significantly increased the demand for advanced endoscopic diagnostic and treatment options globally. This trend has fueled the growth of the endoscopy equipment market, as minimally invasive endoscopic procedures are commonly used to monitor and treat these conditions, enabling early detection and targeted interventions that improve patient outcomes.

Meeting Age-Related Healthcare Needs with Advanced Technologies

The aging population is a major factor driving the global endoscopy equipment market. As people grow older, they become more susceptible to various gastrointestinal conditions, such as bleeding, gallstones, and oesophageal disorders. These age-related health issues often necessitate diagnostic procedures like gastroscopy or endoscopic retrograde cholangiopancreatography (ERCP) to identify and manage the underlying problems.

This demographic trend creates a consistent demand for advanced endoscopic equipment that provide enhanced diagnostic precision, improved procedural efficiency, and minimized patient discomfort. In response, manufacturers are incentivized to invest in research and development to introduce new technologies in the endoscopy equipment market that address these evolving healthcare needs. The incorporation of innovative features like improved Visualization capabilities, robotic assistance, and AI-powered analysis can significantly enhance the effectiveness and convenience of endoscopic procedures, particularly for the growing elderly population.

As a result, the aging population serves as a significant driver for the global endoscopy equipment market, fueling the demand for innovative and user-friendly equipment that can effectively diagnose and manage age-related gastrointestinal disorders. This sustained demand encourages manufacturers to continuously improve their product offerings, driving market growth and expansion worldwide.

Navigating the Complex Regulatory Landscape: A Key Challenge for the Global Endoscopy Equipment Market

The global endoscopy equipment market faces a significant challenge in the form of the complex and diverse regulatory landscape across different regions. Obtaining regulatory approvals for new endoscopy technologies can be a lengthy and costly process, as manufacturers must navigate the distinct requirements and guidelines set by various authorities worldwide.

- In 2021, Olympus Corporation faced delays in launching its EVIS X1 advanced endoscopy system in certain markets due to the need to obtain regulatory approvals from multiple agencies. The company had to provide extensive documentation and conduct clinical trials to demonstrate the safety and efficacy of the new technology, in accordance with the specific regulations of each target market.

- In 2022, Stryker encountered challenges in the global rollout of its 1788 minimally invasive surgical camera, as the company had to ensure compliance with evolving regulatory standards across different regions. Maintaining continuous compliance with updated guidelines and requirements posed an ongoing hurdle, as regulatory bodies frequently revise their policies to address emerging safety concerns and technological advancements.

The lack of harmonization in regulatory approvals across regions adds to the complexity in the endoscopy equipment market globally. Several multinational endoscopy equipment manufacturers experienced staggered product launches and market access delays due to the differences in approval timelines and requirements in various countries. This has affected their competitiveness and market share, as they struggle to coordinate their global expansion strategies within the global endoscopy equipment market.

Endoscopy Equipment Market Segment Analysis

Based on Product, according to SMR analysis, Visualization Systems dominated the global endoscopy equipment market in 2024 owing to various key factors. Visualization systems, which include equipment such as high-definition cameras, video processors, and Visualization systems, are an integral part of endoscopic care. During procedures, these techniques are critical to obtaining accurate and comprehensive images that support accurate diagnosis and surgical procedures. The use of advanced Visualization systems has been further accelerated by the growing global demand for minimally invasive surgery, as these systems allow surgeons to perform complex procedures with greater safety and precision.

The continuous development of technology contributes to the dominance of the market of Visualization systems in the endoscopy equipment market. Manufacturers are innovating to introduce systems with advanced Visualization capabilities, ergonomic design and interoperability with other surgical equipment. These developments improve the efficiency of health delivery and meet the growing need for clinical outcomes.

- In April 2023, WiMi Hologram Cloud developed an innovative endoscopy system using holographic Visualization for complex programmable logic equipment (CPLD). This system aims to miniaturize medical equipment and develop medical optoelectronic microsensors.

- In September 2023, Stryker launched, 1788, a minimally invasive surgical camera, offering more vibrant image with balanced lighting.

- In November 2022, the acquisition of Apollo Endosurgery, Inc. by Boston Scientific Corporation for approximately USD 615 million in cash has significant implications for the global endoscopy equipment market, particularly in the "Visualization Systems Endoscope Equipment" category.

The need for Visualization systems within the endoscopy equipment market has increased due to the increase in chronic diseases requiring endoscopic procedures and the development of healthcare infrastructure in emerging economies. For example, rising healthcare costs and awareness of minimally invasive treatments have led to an increase in demand for these systems in regions such as Asia Pacific and South America.

Accessories endoscopic equipment product is expected to be the fastest growing sub-segment in the global endoscopy equipment market during the forecast period. These include essential components such as cables, light sources, and waste products that work with endoscopes and observation systems. This sub-segment is growing as more and more endoscopic procedures are performed worldwide, increasing the demand for appropriate accessories that ensure patient safety and operational efficiency. This model highlights the extensive expansion of the endoscopy equipment market, driven by both core components and add-on equipment that fulfill a wide range of global healthcare services.

Based on Application, according to SMR, Gastrointestinal Endoscopy dominated the global endoscopy equipment market in 2024. Its position in healthcare is due to several factors that emphasize its important role such as gastrointestinal endoscopy plays an essential role in the diagnosis and treatment of diseases related to the gastrointestinal tract, including cancer, polyps and gastrointestinal bleeding. The need for endoscopic surgeries has increased worldwide due to the increase in gastrointestinal diseases, where gastrointestinal endoscopy is necessary for both therapeutic and diagnostic procedures which fuels the endoscopy equipment market.

GI endoscopy has become more popular for several reasons. Advances in endoscopic technology, including high-definition imaging systems and therapeutic adjuvants, have improved the accuracy and efficiency of surgeries, making them less invasive and reliable. The increasing availability of endoscopic therapies increased the number of procedures performed as the global healthcare infrastructure evolves within the global endoscopy equipment market.

Examples of the dominance of GI endoscopy in global endoscopy equipment market in practice include the widespread use of tests such as colonoscopy in colorectal cancer screening. Largely because colonoscopy is widely recommended as a routine operation for the early diagnosis of colon cancer, many gastrointestinal endoscopic procedures are performed each year.

- In January 2023, FUJIFILM India launched FushKnife, a diathermic slitter and ClutchCutter, a rotatable forceps and this was introduced at the 63rd Annual Conference of Indian Society of Gastroenterology-ISGCON held in Jaipur.

- In November 2023, the American College of Gastroenterology (ACG) updated its 2021 guidelines to recommend colorectal cancer screening in average-risk individuals between age 45 and 75 years. This has contributed to the growing demand for colonoscopies, with the procedure being the most commonly performed gastrointestinal procedure in the United States.

Laparoscopy endoscopy is expected to be the fastest-growing segment of the global endoscopy equipment market during the forecast period. Laparoscopic treatment involves minimally invasive surgery through small incisions made possible by inserting special tools and a camera into the abdominal cavity. Laparoscopy is becoming increasingly popular due to its advantages over open surgery, including faster recovery, fewer complications after surgery and shorter hospital stays. Growing experience in surgery, patient demand for less invasive procedures and continuous technological advances that improve laparoscopic tools and techniques are contributing to the growth of this sub-segment in the global endoscopy equipment market.

For instances,

- A 2021 study found that patients undergoing laparoscopic appendectomy had a 1.2-day shorter hospital stay on average compared to open surgery.

- A study in 2022 showed that laparoscopic cholecystectomy resulted in smaller incisions and faster recovery times, with 92% of patients returning to normal activities within 2 weeks.

- According to SMR analysis, in 2023, a major hospital network invested USD 5 million to expand its laparoscopic surgery program, citing improved patient outcomes and cost-effectiveness.

These findings, along with reduced postoperative pain and lower complication rates, have led healthcare providers to increasingly adopt laparoscopic techniques, which made the laparoscopy endoscopy a fastest growing subsegment within the endoscopy equipment market.

Endoscopy Equipment Market Regional Insights

North American Endoscopy Equipment Market dominated the Global Endoscopy Equipment Market in 2024 due to advanced healthcare system, high healthcare expenditure, and presence of major market players. The region's strong investment in technological development of medical equipment such as endoscopy equipment has strengthened the position.

For instances, companies such as Medtronic and Boston Scientific continued to add products to their endoscopy product portfolios, thus helping to grow the market.

- In 2022, Medtronic, a leading global medical equipment company headquartered in the United States, has continued to expand its endoscopy product portfolio. Medtronic launched its GI Genius AI platform to enhance the accuracy of colonoscopy procedures.

- Boston Scientific, another major player in the endoscopy equipment market, is also based in the United States. The company has been actively investing in the development of innovative endoscopic technologies, such as its single-use colonoscopes and gastroscopes, which were introduced in 2023.

- In March 2022, Johns Hopkins Hospital unveiled its newly expanded endoscopy unit featuring the latest advancements in endoscopic technology. The investment reflects the hospital's commitment to providing high-quality care and staying at the forefront of medical innovation.

- In 2021, Canada also has a well-developed universal healthcare system, with total health expenditure reaching USD 265 billion, further driving the demand for endoscopic procedures and equipment.

- In 2020, the United States healthcare spending reached USD 4.1 trillion, accounting for 19.7% of the country's GDP. This high level of healthcare investment has enabled the adoption of advanced medical technologies, including endoscopy equipment.

The North American endoscopy equipment market has maintained its leading position in the global endoscopy equipment market due to the region's advanced healthcare infrastructure, high healthcare spending, presence of major industry players, and continuous technological advancements in endoscopic equipment and procedures.

The Asia-Pacific Endoscopy Equipment Market is expected to be the fastest growing regional market of Global Endoscopy Equipment Market. Rising healthcare costs, rising rates of chronic disease and the development of healthcare infrastructure in countries such as China and India have all contributed to the region's rapid growth. In the Asia-Pacific region, the use of minimally invasive procedures such as endoscopy has increased significantly due to corporate sector funding and government initiatives. Current cases include major expenditures by giant manufacturers such as Johnson and Johnson and Olympus Corporation to expand their market share in the region.

For Instances,

- China's Healthy China 2030 initiative aims to double the size of its health service industry to USD 2.4 trillion by 2030. India's healthcare market has grown by over 20% in the past five years.

Endoscopy Equipment Market Competitive Landscape

Major competitors such as Olympus Corporation, Karl Storz GmbH and Co. KG and Fujifilm Holdings Corporation have maintained their leading position in the fierce competition in the endoscopy equipment market. To meet changing healthcare needs, these industry leaders have focused on strengthening their product offerings by introducing advanced endoscopy systems and accessories within the endoscopy equipment market. They have invested heavily in improving imaging capabilities and ergonomic design.

Due to technological advances and tactical partnerships, startups like Pentax Medical and Boston Scientific Corporation have gained a competitive advantage within the endoscopy equipment market. These efforts were aimed at expanding product offerings and gaining global market share. Increasing R&D spending to bring next-generation endoscopy products to improve diagnostic accuracy and patient outcomes has further changed the competitive landscape of the market.

- In January 2023, AA Medical, a manufacturer of sustainable medical device solutions, successfully partnered with Certified Endoscopy Products, a prestigious Chicago-based medical device recycling company specializing in endoscopy devices.

- In February 2023, FUJIFILM Holdings Corporation announced the expansion of its endoscopy solutions portfolio with the new compact ultrasonic probe system PB2020-M2 at the 3rd Annual Conference on Interventional Pulmonology, “BRONCHUS 2023”.

- In March 2023, NVIDIA and Medtronic formed a strategic partnership to expedite the advancement of artificial intelligence (AI) in the healthcare sector. This collaboration involves the integration of NVIDIA's healthcare and edge AI technologies into Medtronic's GI Genius intelligent endoscopy module.

- In April 2023, Cook Medical secured a contract with healthcare performance improvement company Vizient to deliver endoscopy equipment to its member healthcare facilities.

- In October 2023, Mayo Clinic announced a significant investment in advanced endoscopy equipment, aiming to enhance their diagnostic capabilities and expand their endoscopy units to meet growing patient demand for minimally invasive procedures.

- In November 2023, Olympus Corporation, launched EVIS X1, a next-generation endoscopy system for the Chinese market and demonstrated this endoscopy system at the 6th annual China International Import Expo that was held in Shanghai from November 5th -10th.

- In January 2022, The Johnson & Johnson Medical Equipment Companies (JJMDC) collaborated with Microsoft Corporation Inc, (US) to enable and expand JJMDC’s secure and compliant digital surgery ecosystem.

- In June 2021, Cleveland Clinic upgraded its endoscopy facilities, investing in advanced instruments and expanding its unit to accommodate a higher volume of procedures. The move underscores the hospital's dedication to offering cutting-edge endoscopic services to patients

Endoscopy Equipment Market Scope

|

Endoscopy Equipment Market |

|

|

Market Size in 2025 |

USD 42.09 Bn. |

|

Market Size in 2032 |

USD 68.03 Bn. |

|

CAGR (2026–2032) |

7.1% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Endoscopy Equipment Market Segments |

By Product Endoscope Visualization System Other Endoscope Equipment Accessories |

|

By Application Gastrointestinal Endoscopy Laparoscopy Obstetrics/ Gynaecology Endoscopy Arthroscopy Urology Endoscopy (Cystoscopy) Bronchoscopy Ent Endoscopy Mediastinoscopy Other Applications |

|

|

By Hygiene Single-use Reprocessing Sterilization |

|

|

By End User Hospitals Ambulatory Surgery Centers/Clinics Other End Users |

|

|

Regional Scope |

North America – United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa – South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Endoscopy Equipment Market Key players

North America

- Ethicon Endo-Surgery, LLC. (Johnson & Johnson) (USA)

- Stryker Corporation (USA)

- Boston Scientific Corporation (USA)

- Medtronic Inc. (USA)

- ConMed Corporation (USA)

- Intuitive Surgical, Inc. (USA)

- Cook Medical (USA)

- Ambu A/S (Denmark)

- Fortimedix Surgical B.V. (Netherlands)

- Teleflex Incorporated (USA)

- Cantel Medical Corp.

Europe

- Olympus Corporation (Germany)

- Karl Storz SE & Co. KG (Germany)

- Richard Wolf GmbH (Germany)

- B. Braun Melsungen AG (Germany)

- Medi-Globe (Germany)

- Carl Zeiss AG (Germany)

- Arthrex, Inc.

- Laborie Medical Technologies Inc.

- Teleflex Incorporated (also operates in North America)

- Dantschke Medizintechnik (Germany)

Asia Pacific

- FUJIFILM Holdings Corporation (Japan)

- PENTAX Medical (a division of HOYA Corporation) (Japan)

- Nipro Corporation (Japan)

Frequently Asked Questions

North America is expected to dominate the Endoscopy Equipment Market during the forecast period.

The Endoscopy Equipment Market size is expected to reach USD 68.03 Billion by 2032.

The major top players in the Global Endoscopy Equipment Market are Ethicon Endo-Surgery, LLC. (Johnson & Johnson), Stryker Corporation, Boston Scientific Corporation, Medtronic Inc., Olympus Corporation, Karl Storz SE & Co. KG) and others.

The global endoscopy equipment market is driven by increasing prevalence of chronic diseases, technological advancements in endoscopic procedures, and rising demand for minimally invasive surgeries. during the forecast period.

1. Endoscopy Equipment Market: Research Methodology

2. Endoscopy Equipment Market Introduction

2.1. Study Assumption and Market Definition

2.2. Scope of the Study

2.3. Executive Summary

3. Global Endoscopy Equipment Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Product Segment

3.3.3. End-user Segment

3.3.4. Revenue (2025)

3.3.5. Company Headquarter

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

4. Endoscopy Equipment Market: Dynamics

4.1. Endoscopy Equipment Market Trends

4.2. Endoscopy Equipment Market Dynamics

4.2.1.1. Drivers

4.2.1.2. Restraints

4.2.1.3. Opportunities

4.2.1.4. Challenges

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

4.5. Technological Roadmap

4.6. Regulatory Landscape by Region

4.6.1. North America

4.6.2. Europe

4.6.3. Asia Pacific

4.6.4. Middle East and Africa

4.6.5. South America

5. Endoscopy Equipment Market: Global Market Size and Forecast (Value in USD Billion) (2026-2032)

5.1. Endoscopy Equipment Market Size and Forecast, By Product (2026-2032)

5.1.1. Endoscope

5.1.2. Visualization System

5.1.3. Other Endoscope Equipment

5.1.4. Accessories

5.2. Endoscopy Equipment Market Size and Forecast, By Application (2026-2032)

5.2.1. Gastrointestinal Endoscopy

5.2.2. Laparoscopy

5.2.3. Obstetrics/ Gynecology Endoscopy

5.2.4. Arthroscopy

5.2.5. Urology Endoscopy (Cystoscopy)

5.2.6. Bronchoscopy

5.2.7. Ent Endoscopy

5.2.8. Mediastinoscopy

5.2.9. Other Applications

5.3. Endoscopy Equipment Market Size and Forecast, By Hygiene (2026-2032)

5.3.1. Single-use

5.3.2. Reprocessing

5.3.3. Sterilization

5.4. Endoscopy Equipment Market Size and Forecast, By End User (2026-2032)

5.4.1. Hospitals

5.4.2. Ambulatory Surgery Centers/Clinics

5.4.3. Other End Users

5.5. Endoscopy Equipment Market Size and Forecast, by Region (2026-2032)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Endoscopy Equipment Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

6.1. North America Endoscopy Equipment Market Size and Forecast, By Product (2026-2032)

6.1.1. Endoscope

6.1.2. Visualization System

6.1.3. Other Endoscope Equipment

6.1.4. Accessories

6.2. North America Endoscopy Equipment Market Size and Forecast, By Application (2026-2032)

6.2.1. Gastrointestinal Endoscopy

6.2.2. Laparoscopy

6.2.3. Obstetrics/ Gynaecology Endoscopy

6.2.4. Arthroscopy

6.2.5. Urology Endoscopy (Cystoscopy)

6.2.6. Bronchoscopy

6.2.7. Ent Endoscopy

6.2.8. Mediastinoscopy

6.2.9. Other Applications

6.3. North America Endoscopy Equipment Market Size and Forecast, By Hygiene (2026-2032)

6.3.1. Single-use

6.3.2. Reprocessing

6.3.3. Sterilization

6.4. North America Endoscopy Equipment Market Size and Forecast, By End User (2026-2032)

6.4.1. Hospitals

6.4.2. Ambulatory Surgery Centers/Clinics

6.4.3. Other End Users

6.5. North America Endoscopy Equipment Market Size and Forecast, by Country (2026-2032)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Endoscopy Equipment Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

7.1. Europe Endoscopy Equipment Market Size and Forecast, By Product (2026-2032)

7.2. Europe Endoscopy Equipment Market Size and Forecast, By Application (2026-2032)

7.3. Europe Endoscopy Equipment Market Size and Forecast, By Hygiene (2026-2032)

7.4. Europe Endoscopy Equipment Market Size and Forecast, By End User (2026-2032)

7.5. Europe Endoscopy Equipment Market Size and Forecast, by Country (2026-2032)

7.5.1. United Kingdom

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Russia

7.5.8. Rest of Europe

8. Asia Pacific Endoscopy Equipment Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

8.1. Asia Pacific Endoscopy Equipment Market Size and Forecast, By Product (2026-2032)

8.2. Asia Pacific Endoscopy Equipment Market Size and Forecast, By Application (2026-2032)

8.3. Asia Pacific Endoscopy Equipment Market Size and Forecast, By Hygiene (2026-2032)

8.4. Asia Pacific Endoscopy Equipment Market Size and Forecast, By End User (2026-2032)

8.5. Asia Pacific Endoscopy Equipment Market Size and Forecast, by Country (2026-2032)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. ASEAN

8.5.7. Rest of Asia Pacific

9. Middle East and Africa Endoscopy Equipment Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

9.1. Middle East and Africa Endoscopy Equipment Market Size and Forecast, By Product (2026-2032)

9.2. Middle East and Africa Endoscopy Equipment Market Size and Forecast, By Application (2026-2032)

9.3. Middle East and Africa Endoscopy Equipment Market Size and Forecast, By Hygiene (2026-2032)

9.4. Middle East and Africa Endoscopy Equipment Market Size and Forecast, By End User (2026-2032)

9.5. Middle East and Africa Endoscopy Equipment Market Size and Forecast, by Country (2026-2032)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Nigeria

9.5.4. Rest of ME&A

10. South America Endoscopy Equipment Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

10.1. South America Endoscopy Equipment Market Size and Forecast, By Product (2026-2032)

10.2. South America Endoscopy Equipment Market Size and Forecast, By Application (2026-2032)

10.3. South America Endoscopy Equipment Market Size and Forecast, By Hygiene (2026-2032)

10.4. South America Endoscopy Equipment Market Size and Forecast, By End User (2026-2032)

10.5. South America Endoscopy Equipment Market Size and Forecast, by Country (2026-2032)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest Of South America

11. Company Profile: Key Players

11.1. Ethicon Endo-Surgery, LLC. (Johnson & Johnson)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Stryker Corporation

11.3. Boston Scientific Corporation

11.4. Medtronic Inc.

11.5. ConMed Corporation

11.6. Intuitive Surgical, Inc.

11.7. Cook Medical

11.8. Ambu A/S

11.9. Fortimedix Surgical B.V.

11.10. Teleflex Incorporated

11.11. Cantel Medical Corp.

11.12. Olympus Corporation

11.13. Karl Storz SE & Co. KG

11.14. Richard Wolf GmbH

11.15. B. Braun Melsungen AG

11.16. Medi-Globe

11.17. Carl Zeiss AG

11.18. Arthrex, Inc.

11.19. Laborie Medical Technologies Inc.

11.20. Teleflex Incorporated

11.21. Dantschke Medizintechnik

11.22. FUJIFILM Holdings Corporation

11.23. PENTAX Medical (a division of HOYA Corporation)

11.24. Nipro Corporation

12. Key Findings

13. Industry Recommendations