Electronics Ceramics and Electrical Ceramics Market Global Industry Analysis and Forecast (2026-2032) by Material Type, Product Type and End-Use Industry

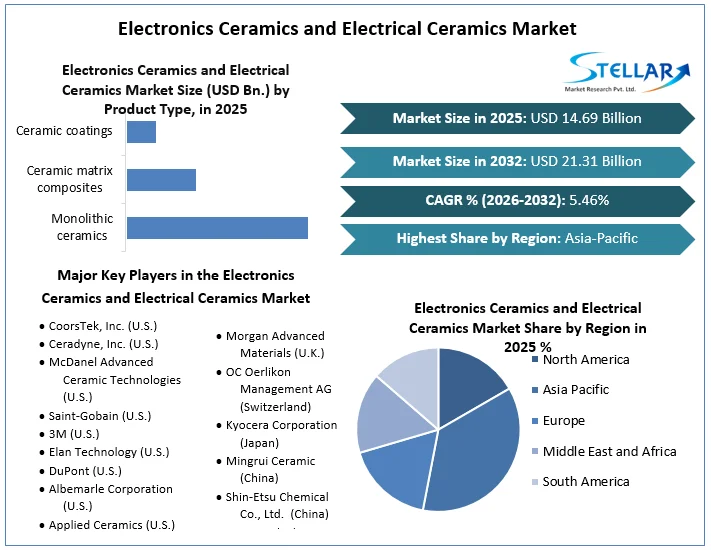

Global Electronics Ceramics and Electrical Ceramics Market size was valued at USD 14.69 Bn. in 2025 and is expected to reach USD 21.31 Bn. by 2032, at a CAGR of 5.46%.

Electronics Ceramics and Electrical Ceramics Market Overview

Electrical and electronic ceramics represent a specialized category of engineered materials known for their exceptional electrical properties. These ceramics play a vital role in improved uses such as in display technology, quantum technology, memory devices, and sensors; and they possess high electrical resistance, dielectric strength, piezoelectricity, ferroelectricity, and semi-conductivity depending on the formula of the compound or the status of the material.

The Electronics Ceramics and Electrical Ceramics Market is on the rise, which is mainly due to increasing consumer electronics demand and scientific and technical solutions constant developments. Gross materials in this market consist of alumina, zirconia, and titanate ceramics required to make different parts such as capacitors, insulators, and substrates. That form of ceramics is purposely made to provide particular electrical functions and is employed in substrates, integrated circuits and packages, multi-chip modules, capacitors, ferrites, insulators, piezoelectric devices, and superconductors.

The nearly $4. Bearing in mind that electronics is a 5 trillion-dollar industry worldwide, it relies on ceramic parts utilized in smartphones, computers, TVs, automobiles, and medical equipment. Modern state developments have made it possible to produce ceramics with semiconducting, superconducting, piezoelectric, and magnetic characteristics.

The demand for passive components, which store or transform energy without controlling electron flow, is high. Ceramic capacitors, especially miniaturized multilayer ceramic capacitors (MLCCs), are experiencing rapid growth driven by the mobile device and communications sector. MLCCs are now commercially available in sizes as small as 0.25mm by 0.125mm by 0.125mm. Piezoelectric ceramics, which generate electrical charges under pressure or change size under an electric field, are used in filters, resonators, transducers, acoustic elements, actuators, and pressure sensors. These ceramics facilitate the miniaturization of electromechanical features and are gaining popularity in consumer electronics, robotics, automotive, sensors and instrumentation, and energy harvesting in the Electronics Ceramics and Electrical Ceramics Market.

The Electronics Ceramics and Electrical Ceramics Market also includes ferrite-based permanent magnets and high-reliability circuit devices like low- and high-temperature co-fired ceramics and ceramic electronic substrates. Innovation in this market is driven by advancements in high-performance insulating materials and miniaturized components, supporting growth in power distribution, telecommunications, and other sectors. Market reports by Stellar Market Research provide comprehensive insights into market value, growth rate, segmentation, geographical coverage, major players, and expert analysis, covering production capacities, distributor and partner networks, price trends, and supply chain and demand deficits.

To get more Insights: Request Free Sample Report

Electronics Ceramics and Electrical Ceramics Market Dynamics

Drivers

Advanced Technologies and Rising Demand for Electronic Goods

The Electronics Ceramics and Electrical Ceramics Market is expected to expand as a result of the progress in technologies and the necessity of using electronic devices. The requirement that these devices should be compact also means that ceramics that are specialisms in the miniaturization of antennae for GPS and Bluetooth in cell phones are crucial. There is an increasing demand due to increased incomes and enhancement in living standards of populations, hence the increased demand for expanded market growth.

Dominance of Consumer Appliances

Electronics and electrical ceramics are also expected to grow at an exponential rate, especially the ones related to consumer appliances. These ceramics are widely applied to electronic substrates and spark plug insulators because of their outstanding electric and mechanical performances as well as stable chemical stabilities against corrosion and wear. Zirconate titanate takes preference among all the piezoelectric ceramics in terms of costs, chemical stability, and mechanical properties in the Electronics Ceramics and Electrical Ceramics Market. The perks for the consumer end are that it makes devices that respond to charges more sensitive, those that work in high temp, and those with constant dielectric influence for the diminutive sensors, antennas, capacitors, and resistors.

Adoption of IoT and Smart Devices

Wider adoption of connected devices in health care, manufacturing, & transport services is protruding forecast sales of Superior electrical ceramics. These ceramics are very important in sensors and actuators that are the ingredients of IoT technology. For instance, ceramic sensors in healthcare enable precise monitoring in wearable health devices, driving the Electronics Ceramics and Electrical Ceramics Market growth as industries seek reliable solutions for smart technology implementations.

Stringent Government Regulations

Stringent government regulations are a significant driver for the Electronics Ceramics and Electrical Ceramics Market. International standards related to energy conversation, environmental protection, and safety also favor the usage of electronics ceramics and electrical ceramics in energy-saving gadgets, electric cars, solar panels, and the like. These regulations include the utilization and promotion of environmentally friendly materials and technologies thus urging the adoption of these ceramics to conform to the standards and performance.

Opportunities

Expansion of the Renewable Energy Sector

The expanding renewable energy sector mainly in photovoltaic and wind energy conversion systems is given as the major driver for the advanced Electronics Ceramics and Electrical Ceramics Market. In insulators, sensors, and distribution of power in renewable energy systems, these materials are of great importance. For example, electrical ceramics play a critical role in solar photovoltaic systems where they are used to insulate high-voltage devices for efficient electricity distribution. This has been highly favored due to the ever-increasing awareness concerning the use of environmentally friendly energy.

Advancements in Semiconductor Manufacturing

Innovations in high-frequency and high-power electronics due to the fast growth of semiconductor industries are putting pressure on ceramics for special electrical needs. For instance, the advance in using GaN semiconductors for high-frequency applications such as in wireless communication needs ceramics with desirable properties of high thermal conductivity complemented by electrical insulation. This has become the trend that is a great force in the expansion of the Electronics Ceramics and Electrical Ceramics Market.

Market Insights

Recent developments, trade regulations, import-export analysis, and production analysis are key aspects influencing the market. The optimization of value chains, the impact of domestic and localized players, and the identification of emerging revenue pockets provide substantial growth opportunities. Changes in Electronics Ceramics and Electrical Ceramics Market regulations, strategic market growth analysis, market size, category growths, application niches, product approvals, launches, geographic expansions, and technological innovations are also critical factors.

For more detailed market insights and strategic decisions to drive market growth, contact Stellar Market Research for an analyst brief.

Challenges

High Cost and Technical Complexity

The manufacturing processes for high-quality electroceramic components are intricate and costly, limiting their widespread adoption. This challenge is particularly pronounced for smaller enterprises that may struggle with the technical complexity of designing and implementing Electronics Ceramics and Electrical Ceramics in various applications. The high production costs and the need for specialized knowledge impede market growth. Efforts in research and development are essential to enhance manufacturing efficiency and reduce costs. Collaborative initiatives among industry stakeholders are needed to streamline production processes, invest in skill development, and explore cost-effective alternatives. These measures will help make the Electronics Ceramics and Electrical Ceramics Market more accessible and economically viable.

Raw Material Shortages and Shipping Delays: Market Impact and Current Scenario

Stellar Market Research provides a comprehensive analysis of the Electronics Ceramics and Electrical Ceramics Market, focusing on the impact of raw material shortages and shipping delays. This involves evaluating strategic possibilities, formulating effective action plans, and aiding businesses in crucial decision-making. Beyond standard reporting, Stellar Market Research offers detailed insights into procurement levels, forecasted shipping delays, regional distributor mapping, commodity and production analysis, price trends, sourcing strategies, category performance, supply chain risk management solutions, advanced benchmarking, and other procurement and strategic support services.

Electronics Ceramics and Electrical Ceramics Market Segment Analysis

Based on the Material Type: Forecasting says that alumina ceramics to have a strong growth rate of XX% CAGR; the Electronics Ceramics and Electrical Ceramics Market value reach USD XX billion in 2025. This growth is a result of properties such as high mechanical strength, wear and thermal resistance, and strong corrosion tolerance. Because of these features, alumina ceramics are commonly used in developing medical equipment and home utensils. Alumina is stated to be hard and resistant to wear in a study that appeared in Ceramics International 2025.

The present review published in the Journal of Materials Science (2022) has pointed out that one of the most beneficial qualities of alumina is that it does not degrade in environments it is applied to, whether they are industrial or consumer. This property is noted in a 2025 article by Advanced Ceramics to improve the performance and durability of electronics by maintaining the component when exposed to heat.

Based on the End-Use Industry: Thus, the end-user segment of the Electronics Ceramics and Electrical Ceramics Market for surgical instruments & other medical devices will have the highest growth rate of XX% during the given period of 2032. It is notably noted that this rise is more or less associated with the increasing demand for sophisticated medical instruments like pacemakers, defibrillators, and endoscope forceps that incorporate electronics and electrical ceramics in their working chamber for their attributes of better performance and endurance.

In the Medical Device Technology report for 2025, there is a gradual increase in the usage of pacemakers, defibrillators, and endoscope forceps that use advanced ceramics to improve the device’s performance and durability. Research published in Biomedical Engineering Trends (2023) focuses on a modern development that shows how ceramics technology is improving medical devices.

Electronics Ceramics and Electrical Ceramics Market Regional Insights

Asia-Pacific is expected to dominate the Electronics Ceramics and Electrical Ceramics Market, driven by its well-established electrical and electronics industries. Key markets in this region include China, Japan, India, South Korea, and Vietnam. China, with its world-leading electronics manufacturing base, particularly in smartphones and OLED TVs, holds a 40% global market share in technical ceramics. India, emerging as a significant player due to government initiatives like Digital India, has seen its consumer electronics market reach $11 billion in 2019. Japan, home to major electronics giants such as Sony and Toshiba, continues to be a strong competitor in semiconductor manufacturing.

The rising digital literacy and the demand for advanced electronic devices further fuel the use of high-quality ceramics in these technologies. Additionally, China's substantial investment in 5G infrastructure, with companies like Huawei leading in 5G patent applications, exemplifies the region’s push towards high-speed internet adoption, increasing the demand for electronic ceramic components.

North America is also a major market, with the United States holding a significant share of $3 billion in 2025. The presence of leading manufacturers and a thriving medical devices sector, projected to reach $208 billion by 2025, drive the demand for high-quality ceramics. The growth is supported by increasing hospitalization rates and investments in advanced medical equipment. The United States remains the largest medical device market, contributing significantly to the demand for electronics and electrical ceramics.

The Electronics Ceramics and Electrical Ceramics Market analysis includes factors such as domestic regulations, value chain dynamics, and competitive landscape. Key considerations include technical trends, Porter’s Five Forces analysis, and case studies to forecast market scenarios. The impact of global brands, domestic competition, tariffs, and trade routes also play a crucial role in shaping market trends and forecasts.

Electronics Ceramics and Electrical Ceramics Market Scope

|

Electronics Ceramics and Electrical Ceramics Market |

|

|

Market Size in 2025 |

USD 14.69 Bn. |

|

Market Size in 2032 |

USD 21.31 Bn. |

|

CAGR (2026-2032) |

5.46 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Electronics Ceramics and Electrical Ceramics Market Segments |

By Material Type Alumina ceramics Titanate ceramics Zirconia ceramics Silica ceramics Others |

|

By Product Type Monolithic ceramics Ceramic matrix composites Ceramic coatings Others |

|

|

|

By End-Use Industry Home appliances Power grids Medical devices Mobile phones Others |

|

Regional Scope |

North America (United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa ( South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Electronics Ceramics and Electrical Ceramics Market Key players

North America

- CoorsTek, Inc. (U.S.)

- Ceradyne, Inc. (U.S.)

- McDanel Advanced Ceramic Technologies (U.S.)

- Saint-Gobain (U.S.)

- 3M (U.S.)

- Elan Technology (U.S.)

- DuPont (U.S.)

- Albemarle Corporation (U.S.)

- Applied Ceramics (U.S.)

Europe

- CeramTec GmbH (Germany)

- Morgan Advanced Materials (U.K.)

- OC Oerlikon Management AG (Switzerland)

Asia Pacific

- Kyocera Corporation (Japan)

- Mingrui Ceramic (China)

- Shin-Etsu Chemical Co., Ltd. (China)

- NGK Spark Plug Co., Ltd. (Japan)

- Murata Manufacturing Co., Ltd. (Japan)

- TDK Corporation (Tokyo, Japan)

- Samsung Electro-Mechanics Co., Ltd. (Suwon, South Korea)

- Mitsubishi Materials Corporation (Tokyo, Japan)

- Yageo Corporation (Taipei, Taiwan)

- Nitto Denko Corporation (Osaka, Japan)

- Sumitomo Chemical Co., Ltd. (Osaka, Japan)

Frequently Asked Questions

Asia-Pacific is expected to dominate the Electronics Ceramics and Electrical Ceramics Market during the forecast period.

The Electronics Ceramics and Electrical Ceramics Market size is expected to reach USD 21.31 Billion by 2032.

The major top players in the Global Electronics Ceramics and Electrical Ceramics Market are Kyocera Corporation (Japan), Mingrui Ceramic (China), Shin-Etsu Chemical Co., Ltd. (China), NGK Spark Plug Co., Ltd. (Japan), Murata Manufacturing Co., Ltd. (Japan) CoorsTek, Inc. (U.S.), Ceradyne, Inc. (U.S.), McDanel Advanced Ceramic Technologies (U.S.), Saint-Gobain (U.S.) and others.

Advanced Packaging Technologies, Technological Advancements, Renewable Energy Integration, and Rising Demand in the Automotive Industry are expected to drive market growth during the forecast period.

1. Electronics Ceramics and Electrical Ceramics Market: Research Methodology

2. Electronics Ceramics and Electrical Ceramics Market Introduction

2.1. Study Assumption and Market Definition

2.2. Scope of the Study

2.3. Executive Summary

3. Global Electronics Ceramics and Electrical Ceramics Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Product Segment

3.3.3. End-user Segment

3.3.4. Revenue (2025)

3.3.5. Company Headquarter

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

4. Electronics Ceramics and Electrical Ceramics Market: Dynamics

4.1. Electronics Ceramics and Electrical Ceramics Market Trends

4.2. Electronics Ceramics and Electrical Ceramics Market Dynamics

4.2.1.1. Drivers

4.2.1.2. Restraints

4.2.1.3. Opportunities

4.2.1.4. Challenges

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

4.5. Water Depth Roadmap

4.6. Regulatory Landscape by Region

4.6.1. North America

4.6.2. Europe

4.6.3. Asia Pacific

4.6.4. Middle East and Africa

4.6.5. South America

5. Electronics Ceramics and Electrical Ceramics Market: Global Market Size and Forecast (Value in USD Billion) (2025-2032)

5.1. Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By Material Type (2025-2032)

5.1.1. Alumina ceramics

5.1.2. Titanate ceramics

5.1.3. Zirconia ceramics

5.1.4. Silica ceramics

5.1.5. Others

5.2. Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By Product Type (2025-2032)

5.2.1. Monolithic ceramics

5.2.2. Ceramic matrix composites

5.2.3. Ceramic coatings

5.2.4. Others

5.3. Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By End-Use Industry (2025-2032)

5.3.1. Home appliances

5.3.2. Power grids

5.3.3. Medical devices

5.3.4. Mobile phones

5.3.5. Others

5.4. Electronics Ceramics and Electrical Ceramics Market Size and Forecast, by Region (2025-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Electronics Ceramics and Electrical Ceramics Market Size and Forecast by Segmentation (Value in USD Billion) (2025-2032)

6.1. North America Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By Material Type (2025-2032)

6.1.1. Alumina ceramics

6.1.2. Titanate ceramics

6.1.3. Zirconia ceramics

6.1.4. Silica ceramics

6.1.5. Others

6.2. North America Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By Product Type (2025-2032)

6.2.1. Monolithic ceramics

6.2.2. Ceramic matrix composites

6.2.3. Ceramic coatings

6.2.4. Others

6.3. North America Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By End-Use Industry (2025-2032)

6.3.1. Home appliances

6.3.2. Power grids

6.3.3. Medical devices

6.3.4. Mobile phones

6.3.5. Others

6.4. North America Electronics Ceramics and Electrical Ceramics Market Size and Forecast, by Country (2025-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Electronics Ceramics and Electrical Ceramics Market Size and Forecast by Segmentation (Value in USD Billion) (2025-2032)

7.1. Europe Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By Material Type (2025-2032)

7.2. Europe Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By Product Type (2025-2032)

7.3. Europe Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By End-Use Industry (2025-2032)

7.4. Europe Electronics Ceramics and Electrical Ceramics Market Size and Forecast, by Country (2025-2032)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Russia

7.4.8. Rest of Europe

8. Asia Pacific Electronics Ceramics and Electrical Ceramics Market Size and Forecast by Segmentation (Value in USD Billion) (2025-2032)

8.1. Asia Pacific Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By Material Type (2025-2032)

8.2. Asia Pacific Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By Product Type (2025-2032)

8.3. Asia Pacific Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By End-Use Industry (2025-2032)

8.4. Asia Pacific Electronics Ceramics and Electrical Ceramics Market Size and Forecast, by Country (2025-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. ASEAN

8.4.7. Rest of Asia Pacific

9. Middle East and Africa Electronics Ceramics and Electrical Ceramics Market Size and Forecast by Segmentation (Value in USD Billion) (2025-2032)

9.1. Middle East and Africa Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By Material Type (2025-2032)

9.2. Middle East and Africa Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By Product Type (2025-2032)

9.3. Middle East and Africa Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By End-Use Industry (2025-2032)

9.4. Middle East and Africa Electronics Ceramics and Electrical Ceramics Market Size and Forecast, by Country (2025-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Nigeria

9.4.4. Rest of ME&A

10. South America Electronics Ceramics and Electrical Ceramics Market Size and Forecast by Segmentation (Value in USD Billion) (2025-2032)

10.1. South America Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By Material Type (2025-2032)

10.2. South America Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By Product Type (2025-2032)

10.3. South America Electronics Ceramics and Electrical Ceramics Market Size and Forecast, By End-Use Industry (2025-2032)

10.4. South America Electronics Ceramics and Electrical Ceramics Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. CoorsTek, Inc. (U.S.)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Ceradyne, Inc. (U.S.)

11.3. McDanel Advanced Ceramic Technologies (U.S.)

11.4. Saint-Gobain (U.S.)

11.5. 3M (U.S.)

11.6. Elan Technology (U.S.)

11.7. DuPont (U.S.)

11.8. Albemarle Corporation (U.S.)

11.9. Applied Ceramics (U.S.)

11.10. CeramTec GmbH (Germany)

11.11. Morgan Advanced Materials (U.K.)

11.12. OC Oerlikon Management AG (Switzerland)

11.13. Kyocera Corporation (Japan)

11.14. Mingrui Ceramic (China)

11.15. Shin-Etsu Chemical Co., Ltd. (China)

11.16. NGK Spark Plug Co., Ltd. (Japan)

11.17. Murata Manufacturing Co., Ltd. (Japan)

11.18. TDK Corporation (Tokyo, Japan)

11.19. Samsung Electro-Mechanics Co., Ltd. (Suwon, South Korea)

11.20. Mitsubishi Materials Corporation (Tokyo, Japan)

11.21. Yageo Corporation (Taipei, Taiwan)

11.22. .Nitto Denko Corporation (Osaka, Japan)

11.23. .Sumitomo Chemical Co., Ltd. (Osaka, Japan)

12. Key Findings

13. Industry Recommendations