Industrial Sensors Market - Global Industry Analysis by Market Share, Trend, Size, Competitive Landscape, Regional Outlook and Forecast 2026-2034

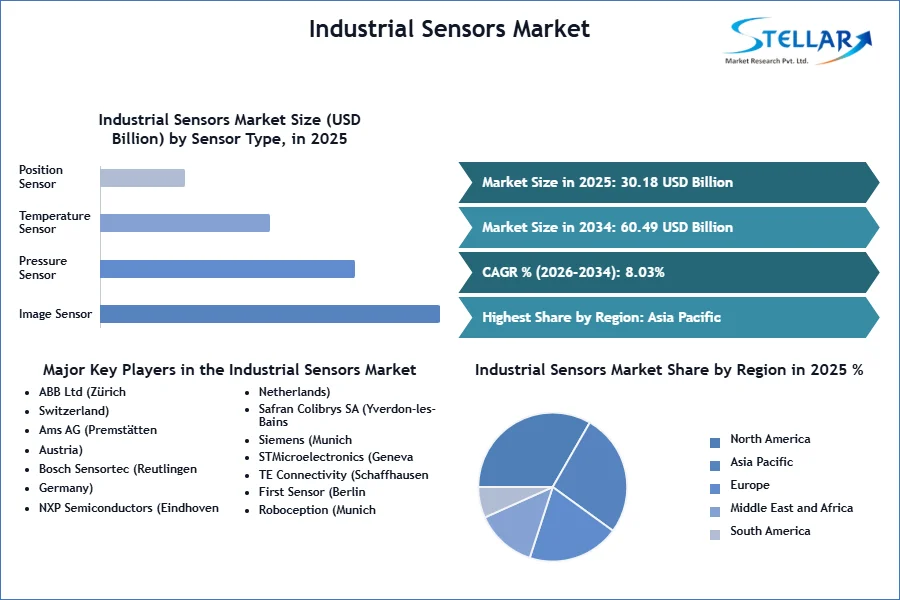

Global Industrial Sensors Market size was valued at USD 30.18 Bn. in 2025 and is expected to reach USD 60.49 Bn. by 2034, at a CAGR of 8.03 %.

Industrial Sensors Market Overview

Industrial sensors are specialized devices designed to detect, monitor, and provide data on various physical parameters in industrial processes. These parameters include factors like temperature, pressure, level, flow, and more. They play a pivotal role in ensuring the smooth and efficient operation of industrial machinery and processes by offering real-time information for decision-making and process control. Industrial sensors are used across a wide range of industries, including manufacturing, automotive, oil and gas, chemical, and pharmaceutical, to name a few. The Industrial Sensors Market, valued at USD 30.18 billion in 2025, is projected to grow at a CAGR of 8.03%, reaching USD 60.49 billion by 2034.

Sensors detect environmental changes and relay this information to electronic systems. The market benefits from increased remote sensing, IoT adoption, and predictive maintenance needs in industries like oil and gas. India is the largest importer of industrial sensors, primarily from China, Japan, and Germany. The report covers market trends, dynamics, competitive landscape, and analyses like PESTLE, Industry Value Chain, and Porter’s Five Forces, providing insights on sales, revenue, and growth opportunities.

Key players in the Industrial Sensors Market include companies such as Siemens, Honeywell International Inc., ABB Ltd, and Schneider Electric. Siemens, for instance, offers a diverse range of industrial sensors that cater to different applications, from temperature and pressure sensors to proximity and motion sensors. These sensors help businesses optimize their operations, enhance safety, and reduce downtime through the acquisition of critical data. The integration of IIoT and Industry 4.0 allows industries to create smart and connected manufacturing environments where data from industrial sensors is used to monitor equipment health, improve operational efficiency, and enhance overall productivity. This results in reduced downtime, cost savings, and improved quality control, making it a compelling incentive for businesses to invest in industrial sensors.

To get more Insights: Request Free Sample Report

Industrial Sensors Market Dynamics

Increasing Demand for Automation and Industry 4.0 Driving the Market

The shift towards automation and the adoption of Industry 4.0 principles are major driver for the industrial sensors market. Companies are investing heavily in automation technologies to streamline operations, reduce human error, and enhance productivity. Industrial sensors play a crucial role in this transformation by providing critical data for monitoring and controlling automated processes. For instance, 67% of financial services companies are currently adopting automation to some degree, with 21% planning to automate a quarter of banking roles by 2025. With such tremendous growth and potential, intelligent automation is undoubtedly reshaping the future of investment operations. The integration of sensors with industrial IoT platforms facilitates predictive maintenance, energy management, and process optimization, further propelling Industrial Sensors Industry growth.

Businesses are in a new industrial era that’s transforming traditional values in sensor manufacturing. Industry 4.0 provides the opportunity for industrial sensor companies to be responsive to customers in ways of traditional manufacturers. Through big data, augmented reality (AR), and cloud computing they respond immediately to customer demands in a short lead time. The industrial sensors market is driven by technological advancements, rising demand for automation, and increased IoT adoption. Innovations in sensor technology, such as miniaturization and AI integration, enhance performance and expand applications across various industries.

The push towards automation and Industry 4.0 principles is accelerating the use of sensors in automated systems, improving productivity and efficiency. The IoT connectivity enables real-time monitoring and data exchange, optimizing operations and reducing costs. Emerging markets and the growing demand for energy-efficient solutions present significant opportunities. Rapid industrialization in regions including Asia-Pacific and South America drives industrial sensor demand, while the global focus on sustainability boosts the need for advanced energy-monitoring sensors.

Evolution of Sensor Technologies to Boost the Market Growth

The rapid evolution of sensor technologies, such as IoT, AI, and machine learning, has significantly bolstered the industrial sensors market. Advanced sensors now offer higher accuracy, better reliability, and enhanced connectivity, making them indispensable in various industrial applications. These technological strides enable real-time data collection and analysis, optimizing industrial processes and improving operational efficiency. As industries increasingly adopt smart manufacturing and automation solutions, the demand for sophisticated sensors continues to surge, driving market growth.

Many industrial sensors are custom-made for manufacturers or system providers. It is not yet a marketable item. Sensor specifications vary depending on the application, raising sensor costs, and sensor manufacturers are unable to reduce costs due to a lack of mass production. CMOS image sensor market and image sensor market technologies are being explored to address these challenges. OEMs, on the other hand, demand sensor manufacturers to provide the most advanced technology at the lowest possible price, driving the need for innovations like Wireless Sensor Networks. As a result, Industrial Sensors manufacturers are under more price pressure, causing them to cut profits.

For instance, Panasonic Develops Organic Photoconductive Film (OPF) CMOS Image Sensor Technology that Achieves Excellent Color Reproducibility under Any Light Source Irradiation. The company has developed advanced technologies to detect, predict, and control drowsiness, enhancing safety and productivity in driving, working, and studying environments. Utilizing cameras and sensors, these technologies analyze 1,800 parameters such as blinking and facial expressions to detect even subtle levels of drowsiness.

By predicting changes in drowsiness, the system adjusts environmental factors like air conditioning, brightness, and audio to keep individuals alert. This non-contact approach leverages AI and infrared sensors, providing a comfortable and effective solution. The technology's potential applications extend beyond vehicles to offices and classrooms, promising to maintain alertness and enhance overall performance. Panasonic is set to support customers exploring these innovative sensing technologies from October 2017.

Smart sensors have the potential to be used in a variety of manufacturing industries, including petrochemical, semiconductor, food processing, and transportation, and are key in the Industrial Sensors Market. ABB launched a smart sensor solution, which connects low-voltage electric motors to the Industrial Internet, allowing them to be monitored continuously via a smartphone or web app. Easily affixed to almost any motor, the ABB AbilityTM Smart Sensor transmits data on, for example, vibration, temperature, loads and power consumption to the cloud, to be analyzed.

Alerts are generated as soon as any of the parameters deviates from the norm, allowing the operator to take preventive action before the motor malfunctions. They monitor and process vibration and noise signals, enabling machine health assessment and predictive maintenance, supporting the industrial industry in lowering maintenance costs and increasing cost savings by reducing downtime. The use of automotive oxygen sensors is a great example of this trend.

Growing Emphasis on Safety and Regulatory Compliance to Drive Market Growth

Stringent safety regulations and the need for regulatory compliance are driving the adoption of industrial sensors across various sectors. Industries such as manufacturing, oil and gas, and healthcare are increasingly implementing sensors to monitor hazardous environments, ensure worker safety, and comply with regulatory standards. These sensors help detect potential risks, prevent accidents, and maintain operational safety. The growing awareness of workplace safety and the rising number of government regulations are expected to fuel the demand for industrial sensors, supporting Industrial Sensors Market growth.

Environmental sensors is used in a variety of settings and applications, including homes, offices, factories, and other commercial buildings. Some common uses of environmental sensors include monitoring indoor air quality, detecting leaks and moisture, regulating temperature and humidity, and providing security and safety alerts. Also, it is used to gather data and insights for research, analysis, and decision-making. As global environmental awareness grows, the demand for accurate monitoring of air, water, and soil quality is intensifying. Regulatory bodies worldwide are implementing stringent environmental standards, compelling industries and municipalities to adopt advanced sensor technologies to comply with these regulations.

For instance, the European Union’s Green Deal and the Clean Air Act in the United States push for extensive environmental monitoring and control. These regulations necessitate the deployment of sophisticated sensors capable of real-time data collection and analysis, thereby driving Environmental Sensor demand and increasing the Industrial Sensors Market size growth. The increased public awareness and advocacy for sustainable practices fuel the adoption of environmental sensors in residential, commercial, and industrial applications. This confluence of regulatory pressure and societal demand significantly propels the market forward, encouraging continuous innovation and widespread implementation of environmental sensor technologies.

By integrating environmental sensors into the infrastructure of smart cities, municipalities gain real-time insights and make data-driven decisions to enhance urban living conditions. The collaboration between technology providers, city planners, and policymakers lead to innovative solutions tailored to specific urban challenges. This integration helps achieve sustainability goals and opens up new markets and growth avenues for Industrial Sensors manufacturers and related technology companies, positioning environmental sensors as pivotal components in the smart city ecosystem.

For instance, the Smart cities in Japan, driven by companies like Panasonic, Accenture, Toyota, Plug and Play, and LINE, are advancing economic, ecological, and social sustainability. Key projects include Panasonic's Fujisawa City, Accenture's Aizuwakamatsu initiatives, Toyota's Woven City, Plug and Play's Osaka accelerator, and LINE's smart services in Fukuoka. These cities focus on using ICT, AI, and IoT to address urban challenges, improve quality of life, and support sustainable development. Japan's smart cities emphasize social cohesion and technological innovation, targeting energy efficiency, data management, and community welfare.

The Industrial Sensors Market is projected to grow significantly, highlighting Japan's leadership in smart city development. Such development of smart cities in Japan drives the environmental sensor market growth by incorporating ICT, AI, and IoT to manage urban challenges. Projects by Panasonic, Accenture, Toyota, Plug and Play, and LINE emphasize energy efficiency, data management, and sustainable development. These smart cities require advanced environmental sensors to monitor air quality, energy usage, and ecological conditions, thereby boosting demand for such industrial sensors in the market.

However, the Industrial Sensors Market has issues of data security and privacy. As industrial sensors increasingly become connected to the Internet of Things (IoT) and integrated into more extensive networked systems, they generate vast amounts of data. This data, if not properly secured, can be vulnerable to cyber-attacks and breaches. Ensuring robust cybersecurity measures, such as encryption, secure communication protocols, and regular security updates, is crucial to protecting sensitive industrial information and maintaining trust in sensor technologies. The challenge lies in balancing the need for advanced data analytics and connectivity with the imperative to safeguard against potential security threats.

Expansion of Renewable Energy Sector and Growing Demand for Energy-Efficient Solutions

The global shift towards renewable energy sources offers a promising avenue for the industrial sensors market. Europe is a pioneer in the deployment of modern renewable energy technologies. The region can boast of being the home of the first offshore wind park and the first continent to have seen renewable policy schemes introduced. With the European Union striving to become carbon neutral by 2050, renewable energy investments will continue to be paramount in the future. However, as renewables account for roughly 22 percent of gross energy consumption as of 2022, the EU is still some way off from achieving its target.

As countries strive to reduce their carbon footprint and adopt sustainable energy solutions, the deployment of sensors in renewable energy applications is on the rise. Industrial sensors are essential for monitoring and optimizing the performance of solar panels, wind turbines, and other renewable energy systems. They help in ensuring efficient energy production, detecting faults, and enabling predictive maintenance. The expansion of the renewable energy sector is likely to drive the demand for advanced sensors, creating new growth opportunities for the market.

In 2023, China, the U.S., and Brazil led the world in renewable energy installations, with China boasting a capacity of around 1,453 gigawatts and the U.S. at 388 gigawatts. heavily investing in renewable energy installations, with China at the forefront with approximately 1,453 gigawatts of capacity in 2023. The U.S. follows with around 388 gigawatts. This growth in renewable energy is crucial for addressing climate change and mitigating its effects. As renewable energy becomes crucial for addressing climate change, the industrial sensors market is also growing rapidly. These sensors are vital in optimizing energy efficiency and monitoring environmental impacts in renewable energy systems, highlighting their importance in the global shift towards sustainable energy solutions.

Industrial Sensors Market Segment Analysis

Based on Sensor Type, the pressure sensor held the largest Industrial Sensors Market share in 2025, and it will continue to have the largest share for during the forecast period. Pressure sensors are used for many automotive, medical, industrial, consumer and building devices, which depend on accurate and stable pressure measurements to operate reliably. As more industries rely on pressure sensors to monitor and control their applications, demand for these technologies has greatly increased. With the development of modern technology, flexible human-machine interaction, artificial intelligence, portable detection, and other emerging fields have been built up.

The demand for high flexibility in these fields leads to flexible pressure sensors getting more and more attention and drive this segment's growth. The rising demand from sectors like consumer electronics, healthcare, automotive, improvements in sensor technology, expanding use of automation, IoT applications, and growing demand for pressure sensors in domestic appliances like refrigerators and washing machines. Use of pressure sensors in smartphones, increase in remote connectivity, and advancements in nanoelectromechanical system (NEMS) technology.

Also, in the field of robotics, the type of pressure sensor plays a vital role in work efficiency and performance. Especially, the lack of high performance in a pressure or force sensor is a major obstacle. Commercial pressure sensors like Flexiforce are becoming popular and are predominately used in robotics because of their low cost and simple operating principle. Asia's digital revolution is driving rapid growth in the Industrial Sensors Industry through pressure sensors demand.

The surge in IoT applications, smart manufacturing, and automotive advancements is boosting demand for precise pressure monitoring. Countries such as China, Japan, and South Korea are leading with robust technological ecosystems, fostering innovation and large-scale production. Additionally, government initiatives supporting digital transformation and industrial automation are propelling market growth, making Asia a significant hub for pressure sensor development and deployment.

Asian players are in the lead in nearly every aspect of digitalization, but some economies lag significantly behind. Asian economies lie all along the income spectrum, and correspondingly, the region has the highest dispersion in terms of the adoption of digital technologies, with Japan, Korea, Hong Kong SAR, and Singapore being global trendsetters. But at any given income level, Asian economies are at the frontier relative to their global peers. Moreover, even for relatively poor Asian economies, such as Cambodia and Nepal, digitalization is accelerating.

E-commerce and fintech are other areas in which Asia leads. For instance, China accounted for less than 1 percent of global e-commerce retail transaction value about a decade ago, but today, that share has grown to more than 40 percent. The penetration of e-commerce, as a percentage of total retail sales, now stands at 15 percent in China, compared with 10 percent in the United States. E-commerce penetration is lower in the rest of Asia but is growing fast, particularly in India, Indonesia and Vietnam.

Based on the use of Industry, the manufacturing segment dominated the largest Industrial Sensors Market share in 2025 and is expected to continue to do so throughout the forecast period. The rising acceptance of IoT sensors in processing plants and manufacturing is credited with the segment's rise. Also, IoT-based industrial sensors let producers achieve remote plant monitoring, increase the safety of industrial assets and personnel, and maximize operational efficiency. By achieving early failure detection, the integration of these industrial sensors in manufacturing services helps to reduce maintenance costs.

Industrial Sensors Market Regional Insight

Asia Pacific held the largest market share in 2025. The quick expansion is linked to substantial income prospects in the rapidly expanding industrial sector. Also, China is one of the region's important industrial locations, which will drive market growth through the forecast period. Asia-Pacific economies such as China, India, Indonesia, and Australia. Regional governments are heavily investing in approving new mining projects, creating new market opportunities. Industrial sensor imports shipments in India stood at 29.4K, imported by 1,318 India Importers from 1,994 Suppliers. India imports most of its Industrial sensor from China, Germany and Japan and is the 2nd largest importer of Industrial sensor in the World. The top 3 importers of Industrial sensor are Russia with 29,504 shipments followed by India with 29,365 and Vietnam at the 3rd spot with 23,682 shipments.

North America is expected to witness significant growth at a CAGR of xx% through the forecast period. The growth is attributed to rising industrialization in the region. The region's developing electronics sector, quick technical breakthroughs, growing population, and expanding vehicle industry may all be contributing to the growth of the worldwide industrial sensors market.

The report provides a comprehensive analysis of the global Industrial Sensors market, detailing past and current industry status along with forecasted trends and market size. It simplifies complex data for stakeholders and covers all industry aspects, focusing on key players, including market leaders, followers, and new entrants. The report includes PORTER and PESTEL analyses, examining both external and internal factors impacting the market. It aids in understanding market dynamics and structure by segmenting and projecting the global Industrial Sensors market size. The competitive analysis of key players by product, price, financial position, growth strategies, and regional presence offers valuable insights for investors.

Competitive Landscape

Key players in the Industrial Sensors Market are heavily investing in R&D to expand their product lines, driving further market growth. Strategic initiatives such as new product launches, contractual agreements, mergers and acquisitions, increased investments, and collaborations are also being employed to enhance their global presence. In this competitive and growing market, offering cost-effective solutions is crucial for survival and expansion. Amphenol Corporation aims to be a leading supplier of sensor products, recently launching the Telaire T3022 series of low-cost CO2 sensors.

Bosch Sensortech GmbH partnered with Edge Impulse in July 2022 to integrate machine learning with Bosch's sensors, enhancing industrial monitoring and sensing solutions. In April 2022, ABB Group invested USD 1.1 million in its Brno factory in the Czech Republic to boost advanced sensor production, aiming to reach 100,000 units annually by 2026. These developments highlight the dynamic nature of the Industrial Sensor Market, driven by innovation and strategic growth initiatives.

Conclusion: The Industrial Sensors Market is poised for significant growth, driven by increased automation, Industry 4.0 adoption, and the expansion of renewable energy. Key players like Siemens and Honeywell are leveraging technological advancements in IoT, AI, and machine learning to enhance sensor performance and connectivity. Pressure sensors segment lead the market due to their diverse applications and demand in sectors like manufacturing, automotive, and healthcare. The Asia-Pacific region, particularly China, is a major growth driver, supported by rapid industrialization and substantial investments. North America also shows promising growth potential. Stringent safety regulations and the need for real-time data are further propelling the market. However, challenges like data security and privacy remain. The market is expected to witness robust growth, with continuous innovations and expanding applications across various industries.

Industry Recommendation: The industrial sensors market is poised for significant growth driven by automation, IoT adoption, and Industry 4.0 advancements. To capitalize on this potential, companies should invest in innovative sensor technologies such as AI integration and wireless sensor networks. Prioritizing cybersecurity measures is essential to protect data integrity in increasingly connected environments. Exploring opportunities in renewable energy applications and smart city projects can also boost market presence. Manufacturers must balance high-tech capabilities with cost-efficiency to meet OEM demands. Strategic investments in emerging markets, particularly in Asia-Pacific, can unlock new revenue streams. Additionally, complying with stringent regulatory standards and enhancing product customization for diverse industrial applications will be critical for sustained growth and competitive advantage.

Industrial Sensors Market Scope

|

Industrial Sensors Market |

|

|

Market Size in 2025 |

USD 30.18 Bn. |

|

Market Size in 2034 |

USD 60.49 Bn. |

|

CAGR (2026-2034) |

8.03 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Industrial Sensors Market Segments |

By Sensor Type

|

|

By End Use Industry

|

|

|

Regional Scope |

North America (United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa (South Africa, GCC, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Industrial Sensors Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN and Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, and Rest of ME&A)

Industrial Sensors Market Key Players

Europe Industrial Sensors Manufacturers

- ABB Ltd (Zürich, Switzerland)

- Ams AG (Premstätten, Austria)

- Bosch Sensortec (Reutlingen, Germany)

- NXP Semiconductors (Eindhoven, Netherlands)

- Safran Colibrys SA (Yverdon-les-Bains, Switzerland)

- Siemens (Munich, Germany)

- STMicroelectronics (Geneva, Switzerland)

- TE Connectivity (Schaffhausen, Switzerland)

- First Sensor (Berlin, Germany)

- Siemens (Munich, Germany)

- Roboception (Munich, Germany)

North America Industrial Sensors Leading Players

- Analog Devices, Inc. (Massachusetts, United States)

- Amphenol Corporation (Connecticut, United States)

- Honeywell International (North Carolina, United States)

- Microchip (Arizona, United States)

- PCB Piezotronics, Inc. (United States)

- Rockwell Automation (Wisconsin, United States)

- Teledyne Technologies Incorporated (California, United States)

- MaxBotix (Minnesota, USA)

- Tekscan (Boston, USA)

- Cognex (Natick, USA)

- Texas Instruments (Dallas, USA)

- ATI Industrial Automation (Apex, USA)

Asia Pacific Industrial Sensors Companies

- Panasonic (Osaka, Japan)

- EPSON (Suwa, Nagano, Japan)

- Omron (Kyoto, Japan)

- OTC Daihen (Osaka, Japan)

- FANUC (Yamanashi, Japan)

Frequently Asked Questions

APAC is expected to dominate the Industrial Sensors Market during the forecast period.

The Industrial Sensors Market size is expected to reach USD 60.49 Bn by 2034.

The major top players in the Global Industrial Sensors Market are ABB Ltd, Panasonic and others.

Expansion of the renewable energy sector and growing demand for energy-efficient solutions is expected to create lucrative opportunity for market growth.

China held the largest Industrial Sensors Market share in 2025.

1. Industrial Sensors Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Assumptions

2. Industrial Sensors Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2034) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Industrial Sensors Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2023)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

3.5. Industrial Sensors Industry Ecosystem

3.5.1. Ecosystem Analysis

3.5.2. Role of the Companies in the Ecosystem

4. Industrial Sensors Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape

4.10.1. Market Regulation by Region

4.10.1.1. North America

4.10.1.2. Europe

4.10.1.3. Asia Pacific

4.10.1.4. Middle East and Africa

4.10.1.5. South America

4.10.2. Impact of Regulations on Market Dynamics

4.10.3. Government Schemes and Initiatives

5. Industrial Sensors Market Size and Forecast by Segments (by Value USD Billion)

5.1. Industrial Sensors Market Size and Forecast, By Sensor Type (2026-2034)

5.1.1. Image Sensor

5.1.2. Pressure Sensor

5.1.3. Temperature Sensor

5.1.4. Position Sensor

5.1.5. Force Sensor

5.1.6. Gas Sensor

5.1.7. Others

5.2. Industrial Sensors Market Size and Forecast, By End Use Industry (2026-2034)

5.2.1. Manufacturing

5.2.2. Automotive

5.2.3. Oil & Gas

5.2.4. Chemical

5.2.5. Pharmaceutical

5.2.6. Energy & Power

5.2.7. Mining

5.2.8. Others

5.3. Industrial Sensors Market Size and Forecast, by Region (2026-2034)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Industrial Sensors Market Size and Forecast (by Value USD Billion)

6.1. North America Industrial Sensors Market Size and Forecast, By Sensor Type (2026-2034)

6.1.1. Image Sensor

6.1.2. Pressure Sensor

6.1.3. Temperature Sensor

6.1.4. Position Sensor

6.1.5. Force Sensor

6.1.6. Gas Sensor

6.1.7. Others

6.2. North America Industrial Sensors Market Size and Forecast, By End Use Industry (2026-2034)

6.2.1. Manufacturing

6.2.2. Automotive

6.2.3. Oil & Gas

6.2.4. Chemical

6.2.5. Pharmaceutical

6.2.6. Energy & Power

6.2.7. Mining

6.2.8. Others

6.3. North America Industrial Sensors Market Size and Forecast, by Country (2026-2034)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Industrial Sensors Market Size and Forecast (by Value USD Billion)

7.1. Europe Industrial Sensors Market Size and Forecast, By Sensor Type (2026-2034)

7.2. Europe Industrial Sensors Market Size and Forecast, By End Use Industry (2026-2034)

7.3. Europe Industrial Sensors Market Size and Forecast, by Country (2026-2034)

7.3.1. UK

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Industrial Sensors Market Size and Forecast (by Value USD Billion)

8.1. Asia Pacific Industrial Sensors Market Size and Forecast, By Sensor Type (2026-2034)

8.2. Asia Pacific Industrial Sensors Market Size and Forecast, By End Use Industry (2026-2034)

8.3. Asia Pacific Industrial Sensors Market Size and Forecast, by Country (2026-2034)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Bangladesh

8.3.11. Pakistan

8.3.12. Rest of Asia Pacific

9. Middle East and Africa Industrial Sensors Market Size and Forecast (by Value USD Billion)

9.1. Middle East and Africa Industrial Sensors Market Size and Forecast, By Sensor Type (2026-2034)

9.2. Middle East and Africa Industrial Sensors Market Size and Forecast, By End Use Industry (2026-2034)

9.3. Middle East and Africa Industrial Sensors Market Size and Forecast, by Country (2026-2034)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Egypt

9.3.4. Nigeria

9.3.5. Rest of ME&A

10. South America Industrial Sensors Market Size and Forecast (by Value USD Billion)

10.1. South America Industrial Sensors Market Size and Forecast, By Sensor Type (2026-2034)

10.2. South America Industrial Sensors Market Size and Forecast, By End Use Industry (2026-2034)

10.3. South America Industrial Sensors Market Size and Forecast, by Country (2026-2034)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest of South America

11. Company Profile: Key players

11.1. ABB Ltd (Zürich, Switzerland)

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc.)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Ams AG (Premstätten, Austria)

11.3. Bosch Sensortec (Reutlingen, Germany)

11.4. NXP Semiconductors (Eindhoven, Netherlands)

11.5. Safran Colibrys SA (Yverdon-les-Bains, Switzerland)

11.6. Siemens (Munich, Germany)

11.7. STMicroelectronics (Geneva, Switzerland)

11.8. TE Connectivity (Schaffhausen, Switzerland)

11.9. First Sensor (Berlin, Germany)

11.10. Siemens (Munich, Germany)

11.11. Roboception (Munich, Germany)

11.12. Analog Devices, Inc. (Massachusetts, United States)

11.13. Amphenol Corporation (Connecticut, United States)

11.14. Honeywell International (North Carolina, United States)

11.15. Microchip (Arizona, United States)

11.16. PCB Piezotronics, Inc. (United States)

11.17. Rockwell Automation (Wisconsin, United States)

11.18. Teledyne Technologies Incorporated (California, United States)

11.19. MaxBotix (Minnesota, USA)

11.20. Tekscan (Boston, USA)

11.21. Cognex (Natick, USA)

11.22. Texas Instruments (Dallas, USA)

11.23. ATI Industrial Automation (Apex, USA)

11.24. Panasonic (Osaka, Japan)

11.25. EPSON (Suwa, Nagano, Japan)

11.26. Omron (Kyoto, Japan)

11.27. OTC Daihen (Osaka, Japan)

11.28. FANUC (Yamanashi, Japan)

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook