Drive-by-Wire Market Global Industry Analysis and Forecast (2026-2032)

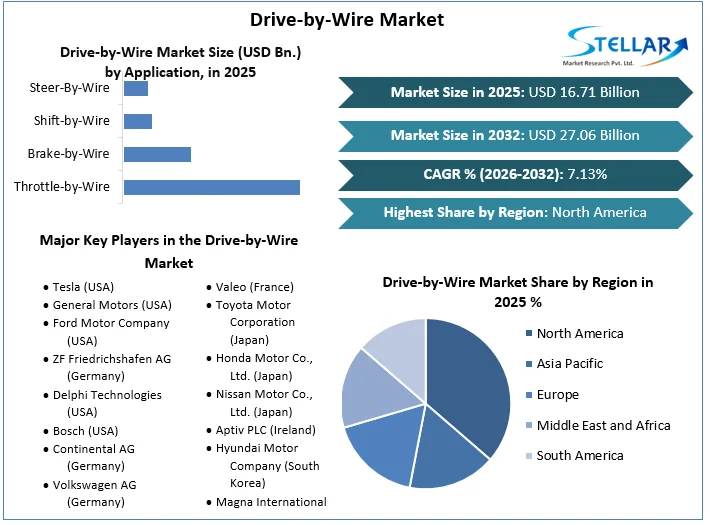

The Drive-by-Wire Market size was valued at USD 16.71 Billion in 2025 and the total Drive-by-Wire Market size is expected to grow at a CAGR of 7.13% from 2026 to 2032, reaching nearly USD 27.06 Billion by 2032.

Drive-by-Wire Market Overview

Drive-by-Wire is an advanced automotive technology that replaces traditional mechanical and hydraulic relationships with electronic controls for operating critical vehicle functions such as steering, braking, and acceleration. As the automotive industry increasingly shifts towards electric and self-driving vehicles drive-by-wire technology is becoming vital for achieving improved performance and safety standards. The global Drive-by-Wire market is driven by several factors, including the increasing demand for electric vehicles (EVs) and autonomous vehicles. The drive-by-wire market has several opportunities including advanced driver assistance systems (ADAS), the evolution towards fully autonomous vehicles, and the advancement in technology. Application, components, end-user, and geographic factors are used to segment the market.

Drive-by-Wire research report provides insights on market overview, market segmentation, current and future pricing, growth analysis, competitive landscape, and other such premium insights within the forecast period. The global Drive-by-Wire market is dynamic and rapidly evolving, creating opportunities for the vehicle industry. The relevant example is the partnership between automakers and battery suppliers like Tesla and Panasonic. This collaboration focuses on developing advanced batteries and improving battery management systems in vehicles. Gigafactory Nevada is a joint project by Tesla and Panasonic’s partnership, it is the world’s largest battery factory with a projected annual production capacity of over 100GWH. Thus, Companies involved in electric vehicle development, including drive-by-wire systems, are collaborating with battery manufacturers to improve battery technology for enhanced vehicle performance and range. Tesla, General Motors, Ford Motor Company, ZF Friedrichshafen AG, Delphi Technologies, Bosch, Continental AG, and Volkswagen AG are among the major leading players spending widely on Drive-by-Wire Product R&D.

To get more Insights: Request Free Sample Report

Drive-by-Wire Market Dynamics:

Increasing Demand for EVs and Autonomous Vehicles Driving the Growth of the Drive-by-Wire Market

The global drive-by-wire market is driven by the increasing demand for electric vehicles(EVs) and autonomous vehicles. Electric vehicle catalyst for boosting the growth of the drive-by-wire market. Unlike, traditional internal combustion engines, electric vehicles rely heavily on electronic systems for their operation. The architecture of EVs consists more advanced electronic control system. Electric vehicles do not contain mechanical connections in their internal combustion engines of vehicles. This feature of EVs enables the integration of drive-by-wire systems. It uses electronic signals to control vehicle functions like braking and steering. Drive-by-wire technology enhances the performance and responsiveness of EVs. It enables smooth acceleration and precise handling. As the market shifts towards the more cultured and high-performance electric models that help to boost the growth of the Drive-by-Wire market.

The demand for autonomous driving abilities is pushing the adoption of drive-by-wire systems. Autonomous vehicles are essential for implementing advanced driver-assistance systems(ADAS) and fully autonomous features within them. The interaction between electric vehicle (EV) technology and drive-by-wire systems leads to advanced innovations in this sector. Both Electric and autonomous vehicles are safe and more efficient to use. These features of EVs and autonomous vehicles drive market growth and encourage the manufacturers to innovate new features in this sector. Technological advancements in battery such as increased range and faster charging times enhance the application of EVs.Innovations in electronic control systems and sensors also enhance the vehicle performance and safety. The United States dominates the market because of major Leading Players and well-established infrastructure

Rise in Demand for Advanced Driver Assistance Systems (ADAS) and the Evolution Towards Fully Autonomous Vehicles Are Major Opportunities of Drive-by-Wire Market

The Drive-by-Wire Market is witnessing promising opportunities driven by advanced driver assistance systems (ADAS) and the evolution toward fully autonomous vehicles. The demand for precise and reliable control systems is overriding by the consumers which leads manufacturers to increasingly invest in autonomous driving technologies. Drive-by-wire technology is essential for enabling the modified vehicle responses required for safe and effective automated driving. This arrangement positions drive-by-wire systems at the forefront of innovation by allowing manufacturers to differentiate their contributions in a highly competitive market. Early and significant investment in drive-by-wire systems can provide a competitive advantage for companies as the automotive industry transitions towards autonomous vehicles and advanced monitoring frameworks. Manufacturers that embrace drive-by-wire technology within the context of smart city initiatives can position themselves as leaders in the next generation of urban flexibility solutions.

The Drive-by-Wire Market Faces Challenges and Risks Associated with Electronic Failure and Data Hacking.

The drive-by-wire market faces significant challenges associated with electronic failure and data hacking. These challenges are essential in determining the adoption and public awareness of drive-by-wire systems in modern vehicles. Electronic failure indicates a significant concern in drive-by-wire systems. It heavily relies on complex electronic components and software to perform critical vehicle functions such as steering and braking. Traditional mechanical systems can often function with redundancy. The drive-by-wire systems have been exposed to single points of failure. There is a failure in the communication network between the components of vehicles it can lead to terrible outcomes. The capacity for digital failure increases big safety issues amongst manufacturers and clients. It requires difficult checking out and validation protocols. Manufacturers must implement fail-safe mechanisms such as redundant systems and robust diagnostics to ensure that any electronic issues do not compromise vehicle safety. This requires not only the development cost but also ongoing maintenance and updates.

Data security is also the biggest challenge in the drive-by-wire market. As vehicles are most connected through the combination of advanced technologies and communication systems. They become more vulnerable to cyber threats. Hackers may try to exploit weaknesses in electronic control units(ECUs) or the communication network and gain illegal access to critical systems. This could lead to dangerous situations. It includes manipulation of vehicle control, unauthorized tracking, or compromise of personal data stored in the vehicle system. This will not only create risks to passenger safety but also discourage consumer confidence in the technology. These are several challenges faced by the drive-by-wire market.

Drive-by-Wire Market Segment Analysis:

Based on Application the market is classified as throttle-by-wire, brake-by-wire, shift-by-wire, and steer-by-wire. The shift-by-wire segment dominated the global market in 2025. The shift-by-wire utilizes an electronic device to change the gearbox mode in vehicles. This system helps to eliminate the mechanical linkage between the gearbox and the lever. Shift-by-wire offers an effortless shifting of gears through a push button. These are the key factors of shift-by-wire that boost the growth of the drive-by-wire market.

Throttle-by-wire, steer-by-wire, and brake-by-wire segments are expected to hold the largest share in the forecast year. Throttle-by-wire is the most common form of drive-by-wire used in the automotive industry. It uses a sequence of electronic sensors and actuators instead of mechanical cables. Throttle sensors are used in vehicles. In this system, the gas device transmits a signal that prompts the electromechanical actuator to open the throttle. Brake-by-wire systems use electronic sensors, actuators, and control algorithms to operate the braking function. When the driver applies the brakes the system sends signals to the brake actuators. In which it applies the brakes accordingly. This is the most important key feature of brake-by-wire. Steer-by-wire systems use electronic sensors, motors, and control units to manage steering inputs by allowing for exact and responsive control without the direct mechanical connections between the steering wheel and the wheels.

Based on Components the market is classified as an actuator, electronic control unit(ECU), engine control module (ECM), electronic throttle control module(ETCM), electronic transmission control unit(ETCU), feedback motor, parking pawl, sensors, others. The actuator segment dominated the global market in 2025. It is an electromechanical device that converts electrical signals into mechanical movement. It plays a crucial role in controlling vehicle functions such as steering, braking, and acceleration without the need for traditional mechanical linkages.

Based on End-User type market is divided into passenger cars, commercial vehicles, electric vehicles, Off-highway vehicles, and others. The passenger cars segment held the largest market share. The rising sales of passenger cars are expected to dominate the market in this segment. Government tax benefits offered on the purchases of hybrid and electric vehicles are the demands for passenger cars over the forecast period. Commercial vehicles are used mainly for transporting goods or passengers for business purposes. These vehicles are designed to operate in various commercial sectors such as logistics, public transport, construction, and services industries. Electric vehicles are automobiles that are powered by electricity. They use electric motors and batteries instead of conventional internal combustion engines. Off-highway vehicles are designed for use on rough surfaces rather than the standard roads. They are used for applications such as construction, agriculture, mining, etc.

Drive-by-Wire Market Regional Insight:

North America was the dominant region in the global Drive-by-wire market in 2025 and is expected to continue its dominance during the forecast period. North America, led by the U.S. has major vehicle manufacturing companies that drive the market in that region. Canada was also the fastest-growing market in the North American region. The region is home to major automotive manufacturers and tech companies such as General Motors, Ford, and Tesla, which are at the forefront of incorporating advanced electronic control systems into electric and autonomous that invest expressively in the research and development of these technologies. Also, stringent safety and production protocols encourage the adoption of drive-by-wire systems to meet compliance standards. A well-established automotive supply chain combined with increasing consumer demand for enhanced driving experiences and safety features led to a boost in the growth of the drive-by-wire market. These are the key factors that support North America's leadership in this market. The dominance of North America in the Drive-by-Wire market is further strengthened by its capacity to develop and innovate new applications thud driving sustained growth in the market globally.

Drive-by-Wire Market Competitive Landscape:

The competitive landscape of the market is determined by intense competition among global and regional players such as Tesla, General Motors, Ford Motor Company, ZF Friedrichshafen AG, and Delphi Technologies these companies influence their extensive R&D experiences for development.

In the global Drive-by-Wire market, Tesla and General Motors are the two major key players. Tesla is the pioneer of electric and autonomous driving. Tesla has a global presence, its primary focus and development are centered in the United States along with growing influence in China and Europe. Tesla has innovated autopilot with advanced driver assistance systems (ADAS). It includes features like automatic lane keeping, adaptive cruise control, and traffic-aware cruise control is at the forefront of the industry. Tesla is the largest Drive-by-Wire company globally. The company has united advanced drive-by-wire systems into electric vehicles (EVs) by utilizing electronic control mechanisms for steering and braking. This system improves vehicle performance, responsiveness, and safety by providing precise control without the traditional mechanical linkages. These features of the company boost them to stand out as the leading players in the Drive-by-Wire market.

General Motors is another major key player in the Drive-by-Wire market. The company has invested heavily in electric and autonomous vehicle development through its Cruise Automation subsidiary, focusing on creating scalable autonomous vehicle platforms. This includes integrating drive-by-wire systems that enhance vehicle flexibility, safety, and efficiency. Both Tesla and General Motors show strong contenders in the competitive landscape of the drive-by-wire market, with each manipulating innovations and adapting to market demands as well as regulatory changes.

|

Drive-by-Wire Market Scope |

|

|

Market Size in 2025 |

USD 16.71 Bn. |

|

Market Size in 2032 |

USD 27.06 Bn. |

|

CAGR (2026-2032) |

7.13 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Component Actuator Electronic Control Unit(ECU) Engine Control Module (ECM) Electronic Throttle Control Module(ETCM), Electronic Transmission Control Unit(ETCU) Feedback Motor Parking Pawl Sensors Others |

|

By Application Throttle-by-Wire Brake-by-Wire Shift-by-Wire Steer-By-Wire Others |

|

|

By End User Passenger Car Commercial Vehicle, Electric Vehicle Off-highway Vehicles Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Switzerland,Netherland and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Rest of APAC South America-Brazil, Argentina, Chile, Colombia Middle East and Africa - South Africa, Nigeria, Israel, Egypt, UAE, Rest of the Middle East and Africa |

Key Player in the Drive-By-Wire Market

- Tesla (USA)

- General Motors (USA)

- Ford Motor Company (USA)

- ZF Friedrichshafen AG (Germany)

- Delphi Technologies (USA)

- Bosch (USA)

- Continental AG (Germany)

- Volkswagen AG (Germany)

- Daimler AG (Germany)

- Valeo (France)

- Toyota Motor Corporation (Japan)

- Honda Motor Co., Ltd. (Japan)

- Nissan Motor Co., Ltd. (Japan)

- Aptiv PLC (Ireland)

- Hyundai Motor Company (South Korea)

- Magna International (Canada)

- LG Electronics (South Korea)

- Infineon Technologies AG (Germany)

- Hitachi Automotive Systems (Japan)

- Nexteer Automotive (USA)

- Wabco Holdings (Belgium)

- BorgWarner Inc. (USA)

- Kistler Group (Switzerland)

- Thyssenkrupp AG (Germany)

- Ficosa International (Spain)

Frequently Asked Questions

Ans. North America is expected to lead the Drive-By-Wire Market during the forecast period.

Ans. An analysis of profit trends and projections for companies in the Drive-By-Wire Market is included, offering insights into factors driving profitability, cost management strategies, and financial performance metrics.

Ans. The Drive-by-Wire Market size was valued at USD 16.71 Billion in 2025 and the total Drive-by-Wire Market size is expected to grow at a CAGR of 7.13% from 2026 to 2032, reaching nearly USD 27.08 Billion by 2032.

Ans. The segments covered in the market report are by Component, by Application and by End User.

1. Drive-by-Wire Market: Research Methodology

2. Drive-by-Wire Market: Executive Summary

3. Drive-by-Wire Market: Competitive Landscape

4. Potential Areas for Investment

4.1. Stellar Competition Matrix

4.2. Competitive Landscape

4.3. Key Players Benchmarking

4.4. Market Structure

4.4.1. Market Leaders

4.4.2. Market Followers

4.4.3. Emerging Players

4.5. Consolidation of the Market

5. Drive-by-Wire Market: Dynamics

5.1. Market Driver

5.1.1. Increasing Consumer Awareness

5.1.2. Innovation in Product Offerings

5.2. Market Trends by Region

5.2.1. North America

5.2.2. Europe

5.2.3. Asia Pacific

5.2.4. South America

5.2.5. Middle East and Africa

5.3. Market Drivers by Region

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. South America

5.3.5. Middle East and Africa

5.4. Market Restraints

5.5. Market Opportunities

5.6. Market Challenges

5.7. PORTER’s Five Forces Analysis

5.8. PESTLE Analysis

5.9. Strategies for New Entrants to Penetrate the Market

5.10. Regulatory Landscape by Region

5.10.1. North America

5.10.2. Europe

5.10.3. Asia Pacific

5.10.4. South America

5.10.5. Middle East and Africa

6. Drive-by-Wire Market Size and Forecast by Segments (by Value Units)

6.1. Drive-by-Wire Market Size and Forecast, by Application (2025-2032)

6.1.1. Throttle-by-wire

6.1.2. Brake-by-wire

6.1.3. Shift-by-wire

6.1.4. Steer-by-wire

6.1.5. Others

6.2. Drive-by-Wire Market Size and Forecast, by Component (2025-2032)

6.2.1. Actuator

6.2.2. Electronic Control Unit(ECU)

6.2.3. Engine Control Module (ECM)

6.2.4. Electronic Throttle Control Module(ETCM)

6.2.5. Electronic transmission control unit(ETCU)

6.2.6. Feedback motor

6.2.7. Parking pawl

6.2.8. Sensors

6.2.9. Others

6.3. Drive-by-Wire Market Size and Forecast, by End-Use (2025-2032)

6.3.1. Passenger Car

6.3.2. Commercial Vehicle

6.3.3. Electric Vehicle

6.3.4. Off-highway vehicles

6.3.5. Others

6.4. Drive-by-Wire Market Size and Forecast, by Region (2025-2032)

6.4.1. North America

6.4.2. Europe

6.4.3. Asia Pacific

6.4.4. South America

6.4.5. Middle East and Africa

7. North America Drive-by-Wire Market Size and Forecast (by Value Units)

7.1. North America Drive-by-Wire Market Size and Forecast, by Application (2025-2032)

7.1.1. Throttle-by-wire

7.1.2. Brake-by-wire

7.1.3. Shift-by-wire

7.1.4. Steer-by-wire

7.1.5. Others

7.2. North America Drive-by-Wire Market Size and Forecast, by Component (2025-2032)

7.2.1. Actuator

7.2.2. Electronic Control Unit(ECU)

7.2.3. Engine Control Module (ECM)

7.2.4. Electronic Throttle Control Module(ETCM)

7.2.5. Electronic transmission control unit(ETCU)

7.2.6. Feedback motor

7.2.7. Parking pawl

7.2.8. Sensors

7.2.9. Others

7.3. North America Drive-by-Wire Market Size and Forecast, by End-Use (2025-2032)

7.3.1. Passenger Car

7.3.2. Commercial Vehicle

7.3.3. Electric Vehicle

7.3.4. Off-highway vehicles

7.3.5. Others

7.4. North America Drive-by-Wire Market Size and Forecast, by Country (2025-2032)

7.4.1. United States

7.4.2. Canada

7.4.3. Mexico

8. Europe Drive-by-Wire Market Size and Forecast (by Value Units)

8.1. Europe Drive-by-Wire Market Size and Forecast, by Application (2025-2032)

8.1.1. Throttle-by-wire

8.1.2. Brake-by-wire

8.1.3. Shift-by-wire

8.1.4. Steer-by-wire

8.1.5. Others

8.2. Europe Drive-by-Wire Market Size and Forecast, by Component (2025-2032)

8.2.1. Actuator

8.2.2. Electronic Control Unit(ECU)

8.2.3. Engine Control Module (ECM)

8.2.4. Electronic Throttle Control Module(ETCM)

8.2.5. Electronic transmission control unit(ETCU)

8.2.6. Feedback motor

8.2.7. Parking pawl

8.2.8. Sensors

8.2.9. Others

8.3. Europe Drive-by-Wire Market Size and Forecast, by End-Use (2025-2032)

8.3.1. Passenger Car

8.3.2. Commercial Vehicle

8.3.3. Electric Vehicle

8.3.4. Off-highway vehicles

8.3.5. Others

8.4. Europe Drive-by-Wire Market Size and Forecast, by Country (2025-2032)

8.4.1. UK

8.4.2. France

8.4.3. Germany

8.4.4. Italy

8.4.5. Spain

8.4.6. Switzerland

8.4.7. Netherland

8.4.8. Rest of Europe

9. Asia Pacific Drive-by-Wire Market Size and Forecast (by Value Units)

9.1. Asia Pacific Drive-by-Wire Market Size and Forecast, by Application (2025-2032)

9.1.1. Throttle-by-wire

9.1.2. Brake-by-wire

9.1.3. Shift-by-wire

9.1.4. Steer-by-wire

9.1.5. Others

9.2. Asia Pacific Drive-by-Wire Market Size and Forecast, by Component (2025-2032)

9.2.1. Actuator

9.2.2. Electronic Control Unit(ECU)

9.2.3. Engine Control Module (ECM)

9.2.4. Electronic Throttle Control Module(ETCM)

9.2.5. Electronic transmission control unit(ETCU)

9.2.6. Feedback motor

9.2.7. Parking pawl

9.2.8. Sensors

9.2.9. Others

9.3. Asia Pacific Drive-by-Wire Market Size and Forecast, by End-Use (2025-2032)

9.3.1. Passenger Car

9.3.2. Commercial Vehicle

9.3.3. Electric Vehicle

9.3.4. Off-highway vehicles

9.3.5. Others

9.4. Asia Pacific Drive-by-Wire Market Size and Forecast, by Country (2025-2032)

9.4.1. China

9.4.2. South Korea

9.4.3. Japan

9.4.4. India

9.4.5. Australia

9.4.6. Indonesia

9.4.7. Malaysia

9.4.8. Vietnam

9.4.9. Taiwan

9.4.10. Rest of Asia Pacific

10. South America Drive-by-Wire Market Size and Forecast (by Value USD Billion)

10.1. South America Drive-by-Wire Market Size and Forecast, by Application (2025-2032)

10.1.1. Throttle-by-wire

10.1.2. Brake-by-wire

10.1.3. Shift-by-wire

10.1.4. Steer-by-wire

10.1.5. Others

10.2. South America Drive-by-Wire Market Size and Forecast, by Component (2025-2032)

10.2.1. Actuator

10.2.2. Electronic Control Unit(ECU)

10.2.3. Engine Control Module (ECM)

10.2.4. Electronic Throttle Control Module(ETCM)

10.2.5. Electronic transmission control unit(ETCU)

10.2.6. Feedback motor

10.2.7. Parking pawl

10.2.8. Sensors

10.2.9. Others

10.3. South America Drive-by-Wire Market Size and Forecast, by End-Use (2025-2032)

10.3.1. Passenger Car

10.3.2. Commercial Vehicle

10.3.3. Electric Vehicle

10.3.4. Off-highway vehicles

10.3.5. Others

10.4. South America Drive-by-Wire Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Argentia

10.4.3. Chile

10.4.4. colombia

11. Middle East and Africa Drive-by-Wire Market Size and Forecast (by Value USD Billion)

11.1. Middle East and Africa Drive-by-Wire Market Size and Forecast, by Application (2025-2032)

11.1.1. Throttle-by-wire

11.1.2. Brake-by-wire

11.1.3. Shift-by-wire

11.1.4. Steer-by-wire

11.1.5. Others

11.2. Middle East and Africa Drive-by-Wire Market Size and Forecast, by Component (2025-2032)

11.2.1. Actuator

11.2.2. Electronic Control Unit(ECU)

11.2.3. Engine Control Module (ECM)

11.2.4. Electronic Throttle Control Module(ETCM)

11.2.5. Electronic transmission control unit(ETCU)

11.2.6. Feedback motor

11.2.7. Parking pawl

11.2.8. Sensors

11.2.9. Others

11.3. Middle East and Africa Drive-by-Wire Market Size and Forecast, by End-Use (2025-2032)

11.3.1. Passenger Car

11.3.2. Commercial Vehicle

11.3.3. Electric Vehicle

11.3.4. Off-highway vehicles

11.3.5. Others

11.4. Middle East and Africa Drive-by-Wire Market Size and Forecast, by Country (2025-2032)

11.4.1. South Africa

11.4.2. SaudibArebia

11.4.3. Egypt

11.4.4. UAE

11.4.5. Rest of ME&A

12. Company Profile: Key players

12.1. Tesla

12.1.1. Company Overview

12.1.2. Financial Overview

12.1.3. Business Portfolio

12.1.4. SWOT Analysis

12.1.5. Business Strategy

12.1.6. Recent Development

12.2. General Motors

12.3. Ford Motor Company

12.4. ZF Friedrichshafen AG

12.5. Delphi Technologies

12.6. Bosch

12.7. Continental AG

12.8. Volkswagen AG

12.9. Daimler AG

12.10. Valeo

12.11. Toyota Motor Corporation

12.12. Honda Motor Co., Ltd.

12.13. Nissan Motor Co., Ltd.

12.14. Aptiv PLC

12.15. Hyundai Motor Company

12.16. Magna International

12.17. LG Electronics

12.18. Infineon Technologies AG

12.19. Hitachi Automotive Systems

12.20. Nexteer Automotive

12.21. Wabco Holdings

12.22. BorgWarner Inc.

12.23. Kistler Group

12.24. Thyssenkrupp AG

12.25. Ficosa International

13. Key Findings

14. Industry Recommendations