Dermal Fillers Market - Global Industry Analysis and Forecast 2026-2034 By Material, Product Type, Application, End User, and Region

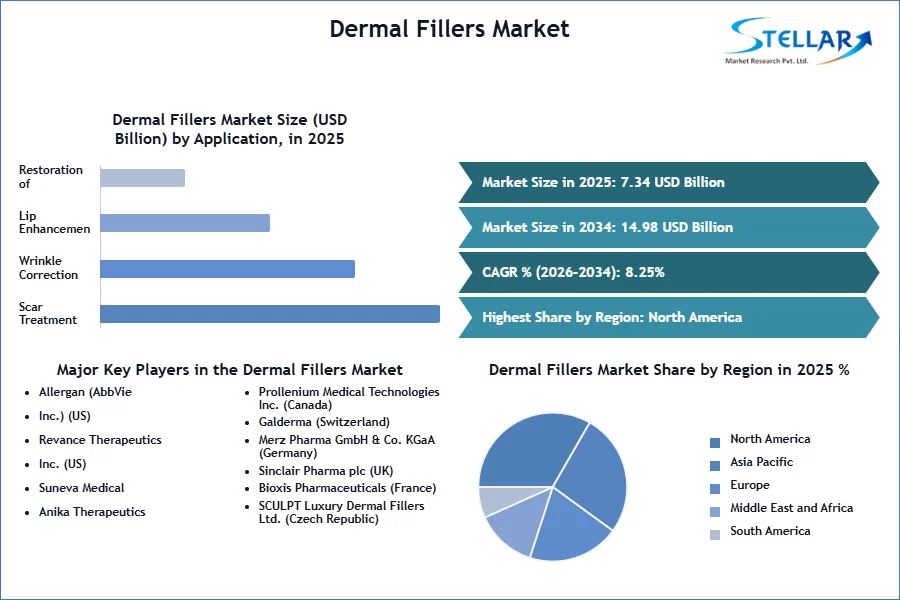

Global Dermal Fillers Market size was valued at USD 7.34 Bn in 2025 and is expected to reach USD 14.98 Bn by 2034, at a CAGR of 8.25%.

Dermal Fillers Market Overview

The dermal fillers market encompasses products used to restore volume, smooth wrinkles, and enhance facial contours. These fillers, which include biodegradable substances like hyaluronic acid and non-biodegradable materials such as silicone, are utilized primarily in cosmetic and reconstructive procedures.

The dermal fillers market is expanding rapidly, owing to a growing demand for minimally invasive cosmetic operations as patients seek non-surgical alternatives for facial rejuvenation and augmentation. Advances in filler technology, such as the development of novel materials and formulas, are also helping to drive market growth by providing more effective and long-lasting effects. Furthermore, rising awareness and acceptance of aesthetic operations among various demographics are driving dermal filler sales. The development of social media and beauty gurus has increased consumer interest and demand for the dermal fillers market.

In 2025, the dermal fillers market was primarily driven by two segments, hyaluronic acid (HA) and calcium hydroxylapatite (CaHA). Hyaluronic acid led the market due to its biocompatibility, effectiveness in moisturizing and plumping skin, and versatility in treating various skin issues. The specialty and dermatology clinics segment dominated as well, thanks to their specialized expertise and ability to offer customized, advanced aesthetic treatments. These clinics are pivotal in adopting innovations and technologies in the dermal fillers market, meeting the growing demand for personalized and minimally invasive cosmetic procedures.

To get more Insights: Request Free Sample Report

Dermal Fillers Market Trend

Rising Demand for Minimally Invasive Treatments Fuels Dermal Filler Market Growth

The shift towards minimally invasive procedures is significantly enhancing the dermal fillers market as patients increasingly prefer non-surgical options that require less recovery time. These treatments provide the advantage of improved aesthetics without the necessity for extensive downtime or major surgical interventions. Technological advancements in the dermal fillers market have further boosted the safety and efficacy of dermal fillers, aligning perfectly with the growing demand for immediate and visible enhancements. As societal acceptance of cosmetic procedures rises, more individuals are opting for dermal fillers as a convenient and efficient aesthetic solution. This trend reflects a broader preference for non-invasive treatments, driving growth in the dermal fillers market as an increasing number of people seek these accessible options for aesthetic improvement. The combined influence of societal developments, technical breakthroughs, and consumer demands in the dermal fillers market results in future growth that caters to those seeking minor changes without the commitment of invasive surgery.

For instance,

- In 2024, the trend towards quick and less invasive treatments in the in the dermal fillers market is evident, with Gen X at the forefront, accounting for 44% of all such procedures. Baby Boomers are not far behind, representing 29%. These two age groups collectively make up 73% of the total minimally invasive procedure market. Gen X leads, particularly in procedures such as neuromodulator injections (57%), hyaluronic acid fillers (50%), non-hyaluronic acid fillers (47%), and sclerotherapy (spider vein removal) (45%).

- According to the American Society of Plastic Surgeons 2024 report, approximately 23,672,269 minimally invasive cosmetic procedures occurred in 2024. These robust statistics further illustrate the significant surge in the popularity of minimally invasive cosmetic procedures.

Dermal Fillers Market Dynamics

Aging Population Fuels Dermal Fillers Market Demand

The aging population is a significant driver of growth in the dermal fillers market. As people age, they experience a natural loss of collagen and elastin, leading to wrinkles, sagging skin, and volume loss. Dermal fillers address these concerns by restoring lost volume, smoothing wrinkles, and enhancing facial contours, making them an attractive option for older adults seeking non-surgical solutions to maintain a youthful appearance. With a growing number of individuals in their 50s and beyond looking for aesthetic enhancements, the demand for dermal fillers is increasing. As the population ages, the need for effective and convenient cosmetic solutions like dermal fillers is expected to rise, driving dermal fillers market expansion.

For instance,

- The demand for dermal fillers among the aging population has seen a notable increase. It is estimated that over 50% - 65% of patients receiving dermal fillers in the U.S. are aged 40 and above, reflecting a growing trend among older adults seeking non-invasive solutions to combat signs of aging, such as wrinkles and volume loss.

High Costs and Potential Risks Pose Challenges for Dermal Fillers Market Growth.

While the dermal fillers market offers numerous aesthetic applications, several constraining factors are anticipated to hamper its growth throughout the forecast period. The exorbitant costs associated with these products are one factor that inhibits the development of the global derma fillers market. The price varies depending on the practitioner's expertise and qualifications, the time required for the procedure, and the efforts involved in the treatment. Moreover, the temporary effects of the products might necessitate individuals to undergo repeated aesthetic filler treatments, imposing a financial strain on them and potentially discouraging them from choosing elective procedures. In addition, the adverse effects after the administration of filler injections significantly contribute toward reducing the growth of the derma fillers market. These factors pose a significant challenge to the expansion of the dermal fillers market.

Dermal Fillers Market Segment Analysis

Based on Material, in 2025, the dermal fillers market was predominantly driven by two key segments, Hyaluronic acid (HA) and calcium Hydroxylapatite (CaHA).

In the dermal fillers market, the hyaluronic acid segment emerged as the leader, accounting for the largest market share in 2025. This dominance is due to HA's inherent presence in the body, which improves biocompatibility and lowers the chance of adverse reactions. Hyaluronic acid fillers are popular because of their ability to moisturize and plump the skin, making them effective for addressing fine lines, wrinkles, and volume loss. The segment is expected to expand further because of continued product advancements and rising customer demand for safe, effective, and minimally invasive aesthetic solutions. They can also be used to enhance the lips and cheeks and to improve the appearance of scars and other skin imperfections. They are available in different formulations, allowing practitioners to customize treatments to each patient’s individual needs. They can vary in thickness, consistency, and longevity, and can be injected at different depths in the skin to achieve specific effects.

Following closely, the calcium hydroxylapatite segment maintained the second largest market share in the dermal fillers market in 2024, owing to its safety profile and effectiveness in boosting collagen formation. Both segments are projected to maintain their growth rates in the dermal fillers market over the forecast period due to technological developments and consumer preferences.

For Instance,

- In August 2024, May pharm launched a hyaluronic acid dermal filler called SEDY FILL, which is used for non-surgical b006Fdy shape correction.

- In 2025, the FDA approved Restylane Contour, a new hyaluronic acid filler that aims to offer natural-looking volume and contouring for the cheeks and mid-face.

- In February 2021, Merz Aesthetics introduced an injectable hyaluronic acid filler with Lidocaine called BELOTERO BALANCE (+) in the U.S. market.

- In April 2024, Allergan Aesthetics launched HArmonyCa, an injectable dermal filler with Lidocaine that utilizes calcium hydroxylapatite (CaHA) for sustained collagen stimulation and hyaluronic acid for immediate lift.

Based on End-User, The dermal fillers market was predominantly driven by the specialty and dermatology clinics segment, which held the largest market share in 2025. Specialty and dermatology clinics are specifically equipped to offer a wide range of aesthetic treatments, including dermal fillers, with specialized expertise. These clinics provide personalized consultations and customized treatment plans that cater to individual patient needs, enhancing the efficacy and safety of the procedures. Patients increasingly seek expert care in settings that offer advanced, tailored treatments for facial rejuvenation and volumization. Specialty clinics are also well-positioned to leverage new product innovations in the dermal fillers market and technologies, such as advanced formulations and techniques, keeping them at the forefront of aesthetic trends in the dermal filler market.

The segment’s growth is expected to continue due to ongoing advancements in dermal filler technologies and increasing consumer awareness of aesthetic treatments. Specialty clinics’ ability to offer comprehensive, expert care and their alignment with the latest industry developments will likely sustain their leading position in the dermal fillers market throughout the forecast period.

Dermal Fillers Market Regional Insights

In 2025, the dermal fillers market was primarily led by North America and Europe, both exhibiting strong growth and significant market shares. The North American dermal fillers market accounted for the largest market share, largely due to a high volume of cosmetic procedures and a robust healthcare infrastructure. The region benefits from a well-educated and financially stable population, which drives demand for various cosmetic treatments, including dermal fillers. The U.S. dermal fillers market dominates the North American market due to its high rate of cosmetic procedures and well-developed healthcare infrastructure. Companies like Allergan (AbbVie) and Galderma lead the market with their advanced HA-based products, such as Juvederm and Restylane, which are widely used in the U.S. Growing acceptance of cosmetic treatments and increasing disposable income contribute to the expansion of the Canada dermal fillers market.

The European dermal fillers market held a significant market share in 2025. The region's strong R&D activities and increasing consumer interest in aesthetic treatments drive market growth. The German dermal fillers market is a major player in the European market, known for its high number of cosmetic procedures involving hyaluronic acid. Companies such as Revance Aesthetics and Medytox are prominent in the German market, offering new product lines and technologies. The European market is anticipated to expand, driven by increasing rates of cosmetic procedures and a significant geriatric population. The ISAPS survey indicated Germany's substantial contribution to the market, with a high volume of hyaluronic acid procedures, underscoring Europe's strong standing in the global dermal fillers market.

For instance,

- According to the American Society of Plastic Surgeons, there were 26.2 million surgical and minimally invasive cosmetic and reconstructive procedures performed in the U.S. in 2024.

- According to the Aesthetic Society, Americans spent over USD 14.6 billion on aesthetic procedures in 2021, with surgical revenues increasing by 63%.

- Data published by the International Society of Plastic Surgery (ISAPS) stated that a total of 77,924 non-surgical procedures were performed in the UK dermal fillers market in 2024.

- In December 2024, SYMATESE enters into an exclusive licensing agreement with EVOLUS. SYMATESE broadens its commercial territories in Europe and the UK for ESTYME FILLERS. Based on its Next-Generation HA technology, EVOLUS neurotoxin, NUCEIVA will be marketed in France by SYMATESE subsidiary.

- According to a report by the American Society of Plastic Surgeons, around 4.8 million cosmetic minimally invasive procedures were performed in the U.S. in 2024.

Dermal Fillers Market Competitive Landscape

In the competitive landscape of the dermal fillers market, AbbVie (Allergan) and Galderma emerge as prominent key players in the dermal fillers market, driving innovation and growth.

AbbVie, through its Allergan division, maintains a strong lead with its popular Juvederm line of hyaluronic acid fillers. Recent advancements include the introduction of Juvederm Volbella XC for lip enhancement and HarmonyCa, a unique combination of hyaluronic acid and calcium hydroxylapatite designed to stimulate collagen production. AbbVie's extensive product portfolio and regulatory approvals further solidify its dominance in the dermal filler market.

Galderma, with its Restylane collection, closely follows suit. The launch of Restylane Kysse, specifically formulated for lip augmentation, showcases the company's commitment to innovation in hyaluronic acid-based fillers. Galderma focus on integrating cutting-edge technologies and expanding its product range enables it to maintain a strong competitive position in the dermal fillers market.

Several companies drive the growth of the dermal filler market through strategic product launches and a dedication to innovation.

Dermal Fillers Market Scope

|

Dermal Fillers Market Scope |

|

|

Market Size in 2025 |

USD 7.34 Bn. |

|

Market Size in 2034 |

USD 14.98 Bn. |

|

CAGR (2026-2034) |

8.25% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segment Analysis |

By Material

|

|

By Product Type

|

|

|

By Application

|

|

|

By End-User

|

|

|

Regional Scope |

North America – United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa – South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Dermal Fillers Key players

North America

- Allergan (AbbVie, Inc.) (US)

- Revance Therapeutics, Inc. (US)

- Suneva Medical, Inc. (US)

- Anika Therapeutics, Inc. (US)

- Prollenium Medical Technologies Inc. (Canada)

Europe

- Galderma (Switzerland)

- Merz Pharma GmbH & Co. KGaA (Germany)

- Sinclair Pharma plc (UK)

- Bioxis Pharmaceuticals (France)

- SCULPT Luxury Dermal Fillers Ltd. (Czech Republic)

Asia Pacific

- BIOPLUS CO., LTD. (South Korea)

- Huadong Medicine Co., Ltd. (China)

- Medytox Inc. (South Korea)

Middle East and Africa (MEA)

- DR. Korman (Israel)

South America

- Marllor Biomedical SRL (Argentina)

- Laboratórios Lupera (Brazil)

- Dermal Aesthetics (Brazil)

- LipoAesthetic (Colombia)

- Esthetique (Chile)

Frequently Asked Questions

Ans. North America is expected to dominate the Dermal Fillers Market during the forecast period.

Ans. The Dermal Fillers Market size is expected to reach USD 14.98 Billion by 2034

Ans. The major top players in the Global Dermal Fillers Market are Allergan (AbbVie, Inc.) (US), Revance Therapeutics, Inc. (US), Galderma (Switzerland), Suneva Medical, Inc. (US), Huadong Medicine Co., Ltd. (China), and others.

Ans. The Global Dermal Fillers Market is driven by increasing demand for non-invasive cosmetic procedures, advancements in filler technology, rising aging populations, and growing awareness of aesthetic treatments.

1. Dermal Fillers Market: Research Methodology

2. Dermal Fillers Market Introduction

2.1. Study Assumption and Market Definition

2.2. Scope of the Study

2.3. Executive Summary

3. Global Dermal Fillers Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Product Segment

3.3.3. End-user Segment

3.3.4. Revenue (2025)

3.3.5. Company Headquarter

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

4. Dermal Fillers Market: Dynamics

4.1. Dermal Fillers Market Trends

4.2. Dermal Fillers Market Dynamics

4.2.1.1. Drivers

4.2.1.2. Restraints

4.2.1.3. Opportunities

4.2.1.4. Challenges

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

4.5. Regulatory Landscape by Region

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Middle East and Africa

4.5.5. South America

5. Dermal Fillers Market: Global Market Size and Forecast (Value in USD Billion) (2026-2034)

5.1. Dermal Fillers Market Size and Forecast, By Material (2026-2034)

5.1.1. Hyaluronic Acid

5.1.2. Calcium Hydroxylapatite

5.1.3. Poly-L-lactic Acid

5.1.4. PMMA (Poly (Methyl Methacrylate))

5.1.5. Fat Fillers

5.1.6. Others

5.2. Dermal Fillers Market Size and Forecast, By Product Type (2026-2034)

5.2.1. Biodegradable

5.2.2. Non-Biodegradable

5.3. Dermal Fillers Market Size and Forecast, By Application (2026-2034)

5.3.1. Scar Treatment

5.3.2. Wrinkle Correction Treatment

5.3.3. Lip Enhancement

5.3.4. Restoration of Volume/Fullness

5.3.5. Others

5.4. Dermal Fillers Market Size and Forecast, By End-User (2026-2034)

5.4.1. Specialty & Dermatology Clinics

5.4.2. Hospitals & Clinics

5.4.3. Others

5.5. Dermal Fillers Market Size and Forecast, by Region (2026-2034)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Dermal Fillers Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2034)

6.1. North America Dermal Fillers Market Size and Forecast, By Material (2026-2034)

6.1.1. Hyaluronic Acid

6.1.2. Calcium Hydroxylapatite

6.1.3. Poly-L-lactic Acid

6.1.4. PMMA (Poly (Methyl Methacrylate))

6.1.5. Fat Fillers

6.1.6. Others

6.2. North America Dermal Fillers Market Size and Forecast, By Product Type (2026-2034)

6.2.1. Biodegradable

6.2.2. Non-Biodegradable

6.3. North America Dermal Fillers Market Size and Forecast, By Application (2026-2034)

6.3.1. Scar Treatment

6.3.2. Wrinkle Correction Treatment

6.3.3. Lip Enhancement

6.3.4. Restoration of Volume/Fullness

6.3.5. Others

6.4. North America Dermal Fillers Market Size and Forecast, By End-User (2026-2034)

6.4.1. Specialty & Dermatology Clinics

6.4.2. Hospitals & Clinics

6.4.3. Others

6.5. North America Dermal Fillers Market Size and Forecast, by Country (2026-2034)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Dermal Fillers Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2034)

7.1. Europe Dermal Fillers Market Size and Forecast, By Material (2026-2034)

7.2. Europe Dermal Fillers Market Size and Forecast, By Product Type (2026-2034)

7.3. Europe Dermal Fillers Market Size and Forecast, By Application (2026-2034)

7.4. Europe Dermal Fillers Market Size and Forecast, By End-User (2026-2034)

7.5. Europe Dermal Fillers Market Size and Forecast, by Country (2026-2034)

7.5.1. United Kingdom

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Russia

7.5.8. Rest of Europe

8. Asia Pacific Dermal Fillers Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2034)

8.1. Asia Pacific Dermal Fillers Market Size and Forecast, By Material (2026-2034)

8.2. Asia Pacific Dermal Fillers Market Size and Forecast, By Product Type (2026-2034)

8.3. Asia Pacific Dermal Fillers Market Size and Forecast, By Application (2026-2034)

8.4. Asia Pacific Dermal Fillers Market Size and Forecast, By End-User (2026-2034)

8.5. Asia Pacific Dermal Fillers Market Size and Forecast, by Country (2026-2034)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. ASEAN

8.5.7. Rest of Asia Pacific

9. Middle East and Africa Dermal Fillers Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2034)

9.1. Middle East and Africa Dermal Fillers Market Size and Forecast, By Material (2026-2034)

9.2. Middle East and Africa Dermal Fillers Market Size and Forecast, By Product Type (2026-2034)

9.3. Middle East and Africa Dermal Fillers Market Size and Forecast, By Application (2026-2034)

9.4. Middle East and Africa Dermal Fillers Market Size and Forecast, By End-User (2026-2034)

9.5. Middle East and Africa Dermal Fillers Market Size and Forecast, by Country (2026-2034)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Nigeria

9.5.4. Rest of ME&A

10. South America Dermal Fillers Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2034)

10.1. South America Dermal Fillers Market Size and Forecast, By Material (2026-2034)

10.2. South America Dermal Fillers Market Size and Forecast, By Product Type (2026-2034)

10.3. South America Dermal Fillers Market Size and Forecast, By Application (2026-2034)

10.4. South America Dermal Fillers Market Size and Forecast, By End-User (2026-2034)

10.5. South America Dermal Fillers Market Size and Forecast, by Country (2026-2034)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest Of South America

11. Company Profile: Key Players

11.1. Allergan (AbbVie, Inc.) (US)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Revance Therapeutics, Inc. (US)

11.3. Suneva Medical, Inc. (US)

11.4. Anika Therapeutics, Inc. (US)

11.5. Prollenium Medical Technologies Inc. (Canada)

11.6. Galderma (Switzerland)

11.7. Merz Pharma GmbH & Co. KGaA (Germany)

11.8. Sinclair Pharma plc (UK)

11.9. Bioxis Pharmaceuticals (France)

11.10. SCULPT Luxury Dermal Fillers Ltd. (Czech Republic)

11.11. BIOPLUS CO., LTD. (South Korea)

11.12. Huadong Medicine Co., Ltd. (China)

11.13. Medytox Inc. (South Korea)

11.14. DR. Korman (Israel)

11.15. Marllor Biomedical SRL (Argentina)

11.16. Laboratórios Lupera (Brazil)

11.17. Dermal Aesthetics (Brazil)

11.18. LipoAesthetic (Colombia)

11.19. Esthetique (Chile)

12. Key Findings

13. Industry Recommendations