Orthopedic Trauma Fixation Devices Market Global Industry Analysis and Forecast (2026-2032)

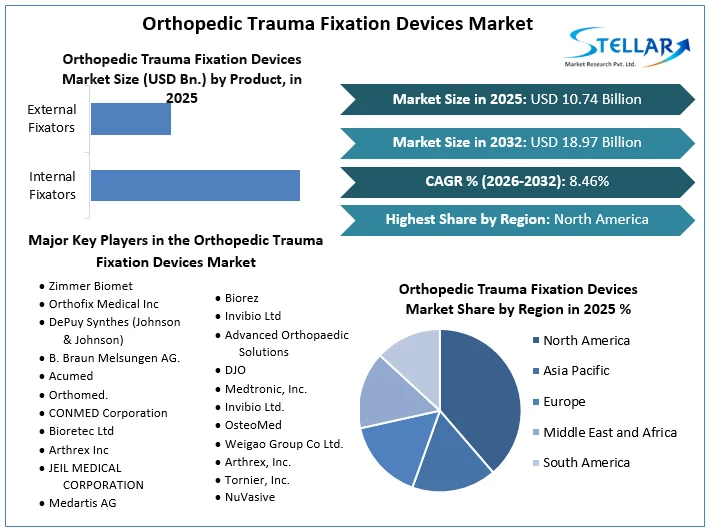

The Orthopedic Trauma Fixation Devices Market Size Was Valued at USD 10.74 Bn. in 2025 And the Total Global Orthopedic Trauma Fixation Devices Revenue is expected to grow at a CAGR of 8.46% from 2026 to 2032, Reaching Nearly USD 18.97 Bn. by 2032.

Orthopedic Trauma Fixation Devices Market Overview

Orthopedic trauma fixation devices are medical devices used to stabilize and support broken or injured bones and joints. The comprehensive SMR report provides a detailed analysis of market dynamics, trends, challenges, and opportunities shaping the industry landscape. The rise in traumatic injuries, attributed to road accidents, sports-related incidents, and falls among the elderly, is driving demand for orthopedic trauma fixation devices. At the same time, continuous advancements in materials, design, and surgical techniques are enhancing device efficacy and safety, driven by innovations like minimally invasive procedures and personalized implants. The increasing aging population, prone to osteoporosis and fractures, is further driving the market growth.

As this demographic continues to grow, the demand for orthopedic trauma fixation devices is expected to rise proportionately increasing market growth. Investing in research and development for advanced materials, technologies, and surgical techniques presents profitable opportunities for orthopedic trauma fixation device manufacturers. Emerging markets, with rapid urbanization and improving healthcare infrastructure, offer significant growth potential. Strategic partnerships with healthcare providers, research institutions, and technology companies are expected to facilitate innovation and market penetration. Diversifying product portfolios to address various fracture types and patient demographics enables companies to capitalize on evolving market trends and meet diverse customer needs, driving sustained growth.

To get more Insights: Request Free Sample Report

Orthopedic Trauma Fixation Devices Market Dynamics

Increasing Incidence of Traumatic Injuries

The orthopedic trauma fixation devices market is driven by a surge in traumatic injuries, attributed to various factors. Globally, road accidents claim 1.35 million lives annually, leading to musculoskeletal injuries that necessitate fixation devices. Increasing participation in sports results in more sports-related injuries, driving demand for advanced fixation devices. Additionally, the aging population faces a higher risk of falls, with one in four adults aged 65 and over experiencing falls each year in the US. These falls often result in hip fractures, spurring the need for implants such as hip screws and plates for repair.

Traumatic injuries pose a significant burden on healthcare systems worldwide. The impact is associated with the combined life years lost from cancer, cardiovascular disease (CVD), and HIV. Trauma stands as the third leading cause of death across all age groups, with particularly high mortality rates among young individuals. Additionally, burn-related mortalities exceed 300,000 annually worldwide. A report from SMR highlighted a threefold higher burden of diseases among men compared to women, with chronic diseases like CVD (15.7%) and motor vehicle crashes (MVCs) (13.7%) being significant contributors to lost years of healthy life. Despite women being underrepresented in various studies, including those concerning non-trauma medical disorders due to socio-cultural barriers, it's imperative to ensure accurate representation of females in trauma-related research and healthcare interventions.

The insight is vital for the Orthopedic Trauma Fixation Devices Market as it underscores the need for gender-inclusive research and healthcare practices. By acknowledging and addressing the disparities in trauma care, orthopedic device manufacturers have been able to develop products and strategies that provide for the unique needs of female trauma patients. It involves designing fixation devices that accommodate anatomical differences and implementing trauma management protocols that consider gender-specific factors. Ultimately, prioritizing gender equity in trauma care leads to improved outcomes and better patient experiences, driving growth and innovation in the orthopedic trauma fixation market.

Top orthopedic implant companies are advancing orthopedic treatments with innovative concepts and technology.

|

COMPANY NAME |

PRODUCTS SUPPLY |

INNOVATIVE CONCEPT AND TECHNOLOGY |

|

Johnson & Johnson – |

|

Techniques

|

|

|

|

|

|

|

|

|

|

|

|

Patient Safety Concerns

Ensuring the safety and efficacy of orthopedic trauma fixation devices is paramount. Any issues related to device performance and safety undermine patient trust and trigger regulatory scrutiny, leading to potential market hold-ups. Patient trust is expected to diminish due to device failures and complications, resulting in injuries and prolonged recovery times, deterring patients from seeking essential treatment. Regulatory scrutiny intensifies, as bodies like the FDA closely monitor device safety, with incidents encouraging investigations and stricter regulations.

The scrutiny affects new device approvals and results in recalls, hindering market growth and innovation. Also, device failures are expected to lead to product liability lawsuits against manufacturers, causing significant financial losses and reputational harm. Ensuring device reliability, regulatory compliance, and swift resolution of issues are crucial for maintaining patient trust and market viability.

Orthopedic Trauma Fixation Devices Market Segment Analysis

By Product, Internal fixators such as comprising plates, screws, intramedullary nails, and bone cement, are surgically implanted within bones to achieve fracture stabilization. The Internal Fixators segment held the largest market share in the Global Orthopedic Trauma Fixation Devices Market in 2025. According to SMR analysis, the segment is further expected to grow at a CAGR of XX% during the forecast period. The dominance of internal fixation arises from its capacity to accelerate healing, optimize bone alignment, and enhance patient mobility in comparison to external fixators, rendering them suitable for diverse fracture scenarios.

Also, the SMR report covers the ongoing technological advancements that drive the adoption of minimally invasive surgical techniques, utilizing compact yet resilient internal fixation devices, thus encouraging the segment's growth trajectory. In the healthcare sector's transition towards value-based care, there is a significant focus on crafting economically viable internal fixation solutions that offer lasting advantages to patients. The prioritization of patient outcomes highlights the importance of internal fixators in enhancing treatment effectiveness and nurturing sustained well-being. As a result, their ongoing leadership in the orthopedic trauma devices market is positioned to persist, driven by advancements in surgical methodologies, technological innovations, and healthcare delivery strategies.

Orthopedic Trauma Fixation Devices Market Regional Analysis

North America leads the global Orthopedic Trauma Fixation Devices market, holding XX% of the market share in 2025. The region struggles with a notable burden of traumatic injuries, stemming from road accidents, sports-related incidents, and falls among the elderly driving demand for these devices. Additionally, North America increases the advanced healthcare infrastructure, facilitating access to innovative surgical techniques and technologies, thus encouraging the adoption of innovative fixation devices.

Also, strong reimbursement policies in the US and Canada ensure broader patient access to these devices, as a result strengthening the Orthopedic Trauma Fixation Devices market growth. The medical field has been witnessing a rise in minimally invasive surgery, employing smaller, specialized fixation devices. The trend encourages swifter patient recovery and shorter hospital stays. North American manufacturers lead in advancing fixation devices, integrating features such as biocompatibility, enhanced stability, and personalized patient solutions.

In North America, there's a rising focus on value-based care, stimulated by government initiatives. The approach prioritizes cost-effective medical devices that yield enhanced patient outcomes, potentially shaping the trajectory of trauma fixation device development and adoption. Regulatory oversight, led by bodies such as the FDA, stands pivotal in upholding the safety and efficiency standards of orthopedic trauma fixation devices. While stringent regulations are expected to influence the market, their primary goal is to safeguard patient well-being, underscoring the importance of compliance with rigorous standards.

Orthopedic Trauma Fixation Devices Market Competitive Landscape

Advancements in minimally invasive devices, such as smaller, specialized fixation tools, are revolutionizing recovery times in surgical procedures. Bioresorbable implants, designed to naturally degrade within the body, deny the necessity for subsequent removal surgeries, garnering increasing interest with ongoing research. The advent of patient-specific implants, made possible through 3D printing, holds promise for enhanced treatment outcomes and accelerated healing periods. These new product launches not only broaden treatment options but also enhance market competition.

- In June 2023, Acuitive Technologies Inc. announced the inaugural surgical use of its Citrelock ACL Tendon Fixation Device. Named Citregen, the novel product boasts a distinctive design, incorporating a tendon-friendly spiral thread and innovative resorbable technology, providing surgeons with an advanced solution for tendon fixation procedures.

- Orthofix Medical Inc. revealed the full commercial launch of the Galaxy Fixation Gemini system in the United States in September 2023. The stable external fixation system offers a rapid, readily available solution for both lower and upper limb fractures.

- In October 2021, CurvaFix Inc. debuted the CurvaFix implant in the United States, offering a solution for pelvic and acetabular fractures.

- In June 2021, Zimmer Biomet launched Bactiguard-coated orthopedic trauma implants in select areas across Europe, the Middle East, and Africa, aiming to reduce infection risks. These implants received the CE mark in January 2021.

|

Orthopedic Trauma Fixation Devices Market Scope |

|

|

Market Size in 2025 |

USD 10.74 Bn. |

|

Market Size in 2032 |

USD 18.97 Bn. |

|

CAGR (2026-2032) |

8.46% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

|

By Product Internal Fixators External Fixators |

|

By End User Hospital Orthopedic and Trauma Centres Ambulatory surgery centers |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Orthopedic Trauma Fixation Devices Market

- Zimmer Biomet

- Orthofix Medical Inc

- DePuy Synthes (Johnson & Johnson)

- B. Braun Melsungen AG.

- Acumed

- Orthomed.

- CONMED Corporation

- Bioretec Ltd

- Arthrex Inc

- JEIL MEDICAL CORPORATION

- Medartis AG

- Biorez

- Invibio Ltd

- Advanced Orthopaedic Solutions

- DJO

- Medtronic, Inc.

- Invibio Ltd.

- OsteoMed

- Weigao Group Co Ltd.

- Arthrex, Inc.

- Tornier, Inc.

- NuVasive

Frequently Asked Questions

Orthopedic trauma fixation devices can be costly, particularly for patients without adequate insurance coverage, limiting access to care in some regions. Obtaining regulatory approval for new orthopedic devices can be a lengthy and expensive process, which is expected to hinder innovation and market growth. Like any medical device, orthopedic trauma fixation devices are subject to safety and quality concerns and recalls can hurt market confidence and growth.

These are commonly used to stabilize fractured bones by affixing metal plates to the bone with screws, providing stability during the healing process. These devices are inserted into the medullary canal of long bones, such as the femur or tibia, to provide internal stabilization and support.

The Market size was valued at USD 10.74 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 8.46% from 2026 to 2032, reaching nearly USD 18.97 Billion.

The segments covered in the market report are by Product and End User.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Orthopedic Trauma Fixation Devices Market Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Orthopedic Trauma Fixation Devices Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovations

4. Orthopedic Trauma Fixation Devices Market: Dynamics

4.1. Orthopedic Trauma Fixation Devices Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Orthopedic Trauma Fixation Devices Market Drivers

4.3. Orthopedic Trauma Fixation Devices Market Restraints

4.4. Orthopedic Trauma Fixation Devices Market Opportunities

4.5. Orthopedic Trauma Fixation Devices Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape by Region

4.10.1. North America

4.10.2. Europe

4.10.3. Asia Pacific

4.10.4. Middle East and Africa

4.10.5. South America

5. Orthopedic Trauma Fixation Devices Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

5.1. Orthopedic Trauma Fixation Devices Market Size and Forecast, by Product (2025-2032)

5.1.1. Internal Fixators

5.1.2. External Fixators

5.2. Orthopedic Trauma Fixation Devices Market Size and Forecast, by End User (2025-2032)

5.2.1. Hospital

5.2.2. Orthopedic and Trauma Centres

5.2.3. Ambulatory surgery centers

5.3. Orthopedic Trauma Fixation Devices Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Orthopedic Trauma Fixation Devices Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

6.1. North America Orthopedic Trauma Fixation Devices Market Size and Forecast, by Product (2025-2032)

6.1.1. Internal Fixators

6.1.2. External Fixators

6.2. North America Orthopedic Trauma Fixation Devices Market Size and Forecast, by End User (2025-2032)

6.2.1. Hospital

6.2.2. Orthopedic and Trauma Centres

6.2.3. Ambulatory surgery centers

6.3. North America Orthopedic Trauma Fixation Devices Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Orthopedic Trauma Fixation Devices Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

7.1. Europe Orthopedic Trauma Fixation Devices Market Size and Forecast, by Product (2025-2032)

7.2. Europe Orthopedic Trauma Fixation Devices Market Size and Forecast, by End User (2025-2032)

7.3. Europe Orthopedic Trauma Fixation Devices Market Size and Forecast, by Country (2025-2032)

7.3.1. United Kingdom

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Orthopedic Trauma Fixation Devices Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

8.1. Asia Pacific Orthopedic Trauma Fixation Devices Market Size and Forecast, by Product (2025-2032)

8.2. Asia Pacific Orthopedic Trauma Fixation Devices Market Size and Forecast, by End User (2025-2032)

8.3. Asia Pacific Orthopedic Trauma Fixation Devices Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Rest of Asia Pacific

9. Middle East and Africa Orthopedic Trauma Fixation Devices Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

9.1. Middle East and Africa Orthopedic Trauma Fixation Devices Market Size and Forecast, by Product (2025-2032)

9.2. Middle East and Africa Orthopedic Trauma Fixation Devices Market Size and Forecast, by End User (2025-2032)

9.3. Middle East and Africa Orthopedic Trauma Fixation Devices Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Nigeria

9.3.4. Rest of ME&A

10. South America Orthopedic Trauma Fixation Devices Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

10.1. South America Orthopedic Trauma Fixation Devices Market Size and Forecast, by Product (2025-2032)

10.2. South America Orthopedic Trauma Fixation Devices Market Size and Forecast, by End User (2025-2032)

10.3. South America Orthopedic Trauma Fixation Devices Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest Of South America

11. Company Profile: Key Players

11.1. Zimmer Biomet

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc.)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Orthofix Medical Inc

11.3. DePuy Synthes (Johnson & Johnson)

11.4. B. Braun Melsungen AG.

11.5. Acumed

11.6. Orthomed.

11.7. CONMED Corporation

11.8. Bioretec Ltd

11.9. Arthrex Inc

11.10. JEIL MEDICAL CORPORATION

11.11. Medartis AG

11.12. Biorez

11.13. Invibio Ltd

11.14. Advanced Orthopaedic Solutions

11.15. DJO

11.16. Medtronic, Inc.

11.17. Invibio Ltd.

11.18. OsteoMed

11.19. Weigao Group Co Ltd.

11.20. Arthrex, Inc.

11.21. Tornier, Inc.

11.22. NuVasive

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook