Orthopedic Extremity Market Global Industry Analysis and Forecast (2026-2032)

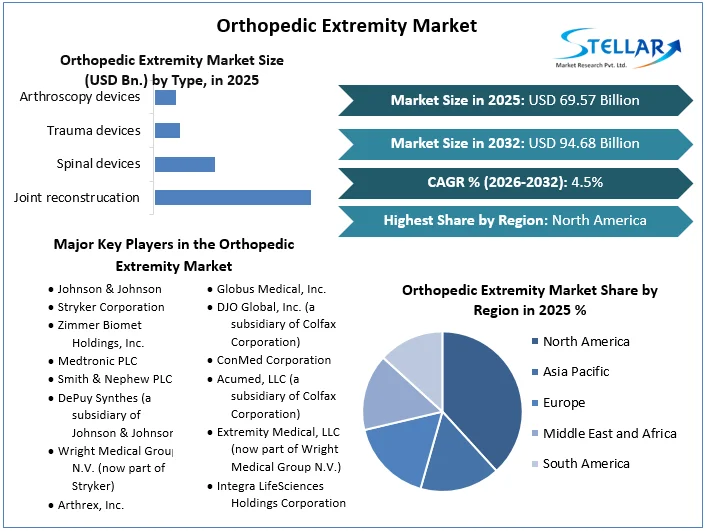

The Orthopedic Extremity Market is expected to grow at 4.5% CAGR from 2025 to 2032, from USD 69.57 billion to USD 94.68 billion.

Orthopedic Extremity Market Overview:

Within the larger healthcare sector, the orthopedic extremities market is a dynamic and quickly developing subsegment. Its primary focus is on the identification, management, and rehabilitation of musculoskeletal disorders and injuries that affect the extremities, which include the limbs, joints, and related tissues. This market includes a wide range of goods and services, including as orthopedic implants, fracture fixation tools, soft tissue repair techniques, and joint replacements. The demand for orthopedic extremities treatments is still being driven by the aging population, rising sports-related injuries, and occurrence of diseases like osteoarthritis. Orthopedic extremities operations have become more widespread thanks to technological developments and minimally invasive surgical methods, which also provide patients with better results and faster recovery times.

To get more Insights: Request Free Sample Report

Orthopedic Extremity Market Dynamics:

Globally, the aging population is one of the main factors driving the orthopedic extremity market. Musculoskeletal diseases including osteoarthritis and joint degeneration become more common as populations age. A significant demand for orthopedic extremities treatments, such as joint replacements and related surgeries, has been generated by this demographic transition. Orthopedic extremity products and services have a steady and expanding market because older people frequently seek therapies to maintain or improve their mobility and quality of life. In order to fulfill the demands of this aging population, manufacturers and healthcare providers are therefore driven to innovate and broaden their product offerings, fueling market expansion.

Orthopedic Extremity Market Opportunities:

A considerable opportunity for product growth and improvement is provided by technology breakthroughs. Emerging technologies like 3D printing, artificial intelligence, and robots have the potential to completely change how orthopedic implants and devices are designed and made. These developments may result in more specialized and accurate treatments, enhancing patient outcomes and speeding up rehabilitation. the growing popularity of outpatient and minimally invasive procedures opens up new business potential. Orthopedic operations for the extremities that can be carried out in ambulatory settings are becoming more popular as healthcare organizations strive to cut costs and improve patient comfort. Manufacturers and healthcare professionals can profit from this trend by creating minimally invasive procedures and equipment and by streamlining the patient flow for faster healing and shorter hospital stays.

Another significant chance is the expansion of the market globally. Spending on orthopedic treatment has increased in emerging economies with expanding middle-class populations. Companies can extend their consumer base by tapping into these markets by tailoring their products to the unique requirements and pricing ranges of these areas. Within the healthcare ecosystem, partnerships and collaborations can spur innovation and market expansion. Collaboration among producers of orthopedic devices, medical professionals, and research organizations can result in the creation of novel medicines and treatments.

These collaborations may also speed up regulatory procedures and ease the adoption of innovative technology, which will eventually benefit patients and the sector as a whole. In general, the orthopedic extremities industry has promising opportunities for those prepared to make investments in research, technology, and international growth.

Orthopedic Extremity Market Restraint:

The dic extremity market is hindered by a number of fundamental obstacles. The mounting need to reduce healthcare expenses is one of the main obstacles. Cost-effectiveness and value-based treatment are becoming increasingly important as healthcare systems around the world struggle with rising costs. Orthopedic extremities treatments, which frequently entail pricey implants and surgeries, are being examined for their potential financial effects. This has boosted price competition among manufacturers and prompted healthcare providers to demand cost minimization, potentially reducing profit margins and R&D expenditures.

The intricate and dynamic regulatory environment is another impediment. To ensure patient safety and efficacy, orthopedic extremities goods must adhere to strict restrictions. It can take a lot of time and effort to navigate these regulatory requirements, secure permissions, and adhere to continuing modifications.

Orthopedic Extremity Market Segment Analysis:

By Type, The orthopedic extremities market's key component, the joint reconstruction segment, includes methods and equipment designed to repair damaged joints and lessen pain. This section covers a broad range of surgical treatments, such as wrist and ankle operations, shoulder and elbow reconstructions, and hip and knee replacements. Joint reconstruction continues to be a crucial growth sector due to the aging global population and the frequency of illnesses like osteoarthritis. In order to improve patient outcomes and match the rising demand for these operations, the market is characterized by constant innovation, such as the creation of cutting-edge implant materials and minimally invasive surgical techniques.

In the orthopedic extremity market, spinal devices are a significant subsegment that serve patients with injuries and illnesses of the spine. This market includes a wide range of items, such as apparatus for the repair of spinal abnormalities, intervertebral disc implants, and spinal fusion devices. Growth in this market is being driven by factors such the rise in spinal problems brought on by aging, sedentary lifestyles, and growing awareness of spinal health. The market for spinal devices is also growing as a result of improvements in minimally invasive spine surgery methods.

The category for trauma devices deals with the immediate medical requirements brought on by fractures, dislocations, and other traumatic injuries to the extremities. This section covers a variety of orthopedic implants used to support and speed the healing of fractured bones, including plates, screws, and intramedullary nails. Because they are so intimately related to unplanned accidents, sports injuries, and trauma cases, trauma devices are in relatively constant demand. Because such injuries are unpredictable, the market must continue to be supplied with trauma-related medical products.

By End Use, A crucial and fundamental end-use market area for orthopedic extremities is hospitals. These facilities act as centers for a variety of orthopedic operations, including arthroscopic interventions, spinal surgeries, and joint replacements. Hospitals gain from having complete facilities, orthopedic departments that are focused, and the capacity to manage challenging situations. Major orthopedic procedures involving substantial medical resources and inpatient care sometimes take place in a hospital setting. The integration of cutting-edge orthopedic technologies within hospitals and the ongoing construction of the healthcare infrastructure are the main drivers of this market's growth.

Orthopedic clinics are specialized settings with a focus on musculoskeletal care, making them a large end-use market for orthopedic extremities. Numerous services, such as consultations, diagnostic imaging, physical therapy, and outpatient procedures, are provided by these clinics. They are in a good position to offer patients with orthopedic disorders individualized orthopedic care with an emphasis on non-surgical therapies, rehabilitation, and follow-up care. Orthopedic clinics continue to experience growth in demand as patient preference for outpatient care increases. Additionally, clinics frequently use the most recent developments in orthopedic technology, increasing their appeal to clients looking for specialist care.

Ambulatory surgical facilities, which include many orthopedic extremities surgery, are specialist facilities built to offer same-day surgical treatments. Compared to typical hospital settings, ASCs have the advantage of less hospitalization, quicker recovery times, and perhaps lower expenses. With the ability to perform a variety of orthopedic treatments in an outpatient setting thanks to improvements in minimally invasive techniques and anesthesia, this end-use segment is becoming more and more important. Convenience is another factor fueling the rise of ASCs, both for patients and healthcare professionals.

Orthopedic Extremity Market Regional Insight:

The orthopedic extremities market is dominated by North America, in especially the United States. The area benefits from a developed healthcare system, high healthcare spending, and an elderly population that is on the rise. Additionally, cutting-edge technologies and a strong emphasis on R&D help to accelerate the introduction of novel orthopedic treatments. Ambulatory surgery centers are expanding as the popularity of minimally invasive procedures rises across North America. Cost constraints and problems with healthcare reimbursement, however, continue to be problems in this area.

Another key competitor in the orthopedic extremity market is Europe, which is distinguished by a strong healthcare system and an aging populace. The European market places a strong emphasis on value-based treatment and cost-effectiveness, which encourages the use of outpatient and minimally invasive procedures. Manufacturers now have easier access to markets thanks to regulatory harmonization within the European Union. The orthopedic extremities market in the area is heavily influenced by nations like Germany, the United Kingdom, and France.

The orthopedic extremities market is expanding quickly in the Asia-Pacific region, driven by factors such as an aging population, rising musculoskeletal health awareness, and improved healthcare infrastructure. As the middle class grows and healthcare costs rise, emerging economies like China and India are seeing tremendous market expansion. Additionally, these nations serve as major orthopedic device production centers, adding to the world supply. However, there are still issues with reimbursement systems and regulatory compliance in various areas of the region.

An aging population and an increase in the prevalence of orthopedic problems are the main drivers of the growing need for orthopedic extremities treatments in Latin America. Brazil and Mexico are significant industry participants, and market growth has been significantly aided by investments in healthcare and developments in medical technology. In several Latin American nations, it is still difficult to access orthopedic care in rural areas.

Due to better healthcare infrastructure and rising investments in the healthcare industry, orthopedic extremity market growth is picking up in the Middle East and Africa. The demand for orthopedic treatments is driven by the frequency of orthopedic problems, particularly in elderly populations. Comprehensive market development is hampered in some areas, nevertheless, by healthcare inequities and economic issues.

|

Orthopedic Extremity Market Scope |

|

|

Market Size in 2025 |

USD 69.57 billion |

|

Market Size in 2032 |

USD 94.68 billion |

|

CAGR (2026-2032) |

4.5% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

by Type

|

|

by End Use

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Orthopedic Extremity Market Key Players:

- Johnson & Johnson

- Stryker Corporation

- Zimmer Biomet Holdings, Inc.

- Medtronic PLC

- Smith & Nephew PLC

- DePuy Synthes (a subsidiary of Johnson & Johnson)

- Wright Medical Group N.V. (now part of Stryker)

- Arthrex, Inc.

- NuVasive, Inc.

- Globus Medical, Inc.

- DJO Global, Inc. (a subsidiary of Colfax Corporation)

- ConMed Corporation

- Acumed, LLC (a subsidiary of Colfax Corporation)

- Extremity Medical, LLC (now part of Wright Medical Group N.V.)

- Integra LifeSciences Holdings Corporation

- Medartis Holding AG

- Orthofix Medical Inc.

- Bioventus LLC

- LimaCorporate S.p.A.

- Tornier, Inc. (now part of Wright Medical Group N.V.)

Frequently Asked Questions

The global Orthopedic Extremity Market is studied from 2025 to 2032.

North America region held the highest share in 2025.

The CAGR for the Orthopedic Extremity Market is 4.5%.

The segments covered in the market report are by type, end use, and region.

1. Orthopedic Extremity Market: Research Methodology

2. Orthopedic Extremity Market: Executive Summary

3. Orthopedic Extremity Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Consolidation of the Market

4. Orthopedic Extremity Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers by Region

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.7. PESTLE Analysis

4.8. Value Chain Analysis

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Orthopedic Extremity Market Size and Forecast by Segments (by Value USD and Volume Units)

5.1. Orthopedic Extremity Market Size and Forecast, by type(2025-2032)

5.1.1. Joint reconstrucation

5.1.2. Spinal devices

5.1.3. Trauma devices

5.1.4. Arthroscopy devices

5.2. Orthopedic Extremity Market Size and Forecast, by end use (2025-2032)

5.2.1. Hospital

5.2.2. Orthopedic

5.2.3. Ambulatory surgical centers

5.3. Orthopedic Extremity Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Orthopedic Extremity Market Size and Forecast (by Value USD and Volume Units)

6.1. North America Orthopedic Extremity Market Size and Forecast, by type(2025-2032)

6.1.1. Joint reconstrucation

6.1.2. Spinal devices

6.1.3. Trauma devices

6.1.4. Arthroscopy devices

6.2. North America Orthopedic Extremity Market Size and Forecast, by end use (2025-2032)

6.2.1. Hospital

6.2.2. Orthopedic

6.2.3. Ambulatory surgical centers

6.3. North America Orthopedic Extremity Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Orthopedic Extremity Market Size and Forecast (by Value USD and Volume Units)

7.1. Europe Orthopedic Extremity Market Size and Forecast, by type(2025-2032)

7.1.1. Joint reconstrucation

7.1.2. Spinal devices

7.1.3. Trauma devices

7.1.4. Arthroscopy devices

7.2. Europe Orthopedic Extremity Market Size and Forecast, by end use (2025-2032)

7.2.1. Hospital

7.2.2. Orthopedic

7.2.3. Ambulatory surgical centers

7.3. Europe Orthopedic Extremity Market Size and Forecast, by Country (2025-2032)

7.3.1. UK

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Orthopedic Extremity Market Size and Forecast (by Value USD and Volume Units)

8.1. Asia Pacific Orthopedic Extremity Market Size and Forecast, by type(2025-2032)

8.1.1. Joint reconstrucation

8.1.2. Spinal devices

8.1.3. Trauma devices

8.1.4. Arthroscopy devices

8.2. Asia Pacific Orthopedic Extremity Market Size and Forecast, by end use (2025-2032)

8.2.1. Hospital

8.2.2. Orthopedic

8.2.3. Ambulatory surgical centers

8.3. Asia Pacific Orthopedic Extremity Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Bangladesh

8.3.11. Pakistan

8.3.12. Rest of Asia Pacific

9. Middle East and Africa Orthopedic Extremity Market Size and Forecast (by Value USD and Volume Units)

9.1. Middle East and Africa Orthopedic Extremity Market Size and Forecast, by type(2025-2032)

9.1.1. Joint reconstrucation

9.1.2. Spinal devices

9.1.3. Trauma devices

9.1.4. Arthroscopy devices

9.2. Middle East and Africa Orthopedic Extremity Market Size and Forecast, by end use (2025-2032)

9.2.1. Hospital

9.2.2. Orthopedic

9.2.3. Ambulatory surgical centers

9.3. Middle East and Africa Orthopedic Extremity Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Egypt

9.3.4. Nigeria

9.3.5. Rest of ME&A

10. South America Orthopedic Extremity Market Size and Forecast (by Value USD and Volume Units)

10.1. South America Orthopedic Extremity Market Size and Forecast, by type(2025-2032)

10.1.1. Joint reconstrucation

10.1.2. Spinal devices

10.1.3. Trauma devices

10.1.4. Arthroscopy devices

10.2. South America Orthopedic Extremity Market Size and Forecast, by end use (2025-2032)

10.2.1. Hospital

10.2.2. Orthopedic

10.2.3. Ambulatory surgical centers

10.3. South America Orthopedic Extremity Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest of South America

11. Company Profile: Key players

11.1. Johnson & Johnson

11.1.1. Company Overview

11.1.2. Financial Overview

11.1.3. Business Portfolio

11.1.4. SWOT Analysis

11.1.5. Business Strategy

11.1.6. Recent Developments

11.2. Stryker Corporation

11.3. Zimmer Biomet Holdings, Inc.

11.4. Medtronic PLC

11.5. Smith & Nephew PLC

11.6. DePuy Synthes (a subsidiary of Johnson & Johnson)

11.7. Wright Medical Group N.V. (now part of Stryker)

11.8. Arthrex, Inc.

11.9. NuVasive, Inc.

11.10. Globus Medical, Inc.

11.11. DJO Global, Inc. (a subsidiary of Colfax Corporation)

11.12. ConMed Corporation

11.13. Acumed, LLC (a subsidiary of Colfax Corporation)

11.14. Extremity Medical, LLC (now part of Wright Medical Group N.V.)

11.15. Integra LifeSciences Holdings Corporation

11.16. Medartis Holding AG

11.17. Orthofix Medical Inc.

11.18. Bioventus LLC

11.19. LimaCorporate S.p.A.

11.20. Tornier, Inc. (now part of Wright Medical Group N.V.)

12. Key Findings

13. Industry Recommendation