Medical Membrane Devices Market- Global Industry Analysis and Forecast (2026-2032) Trends, Statistics, Dynamics, Segment Analysis

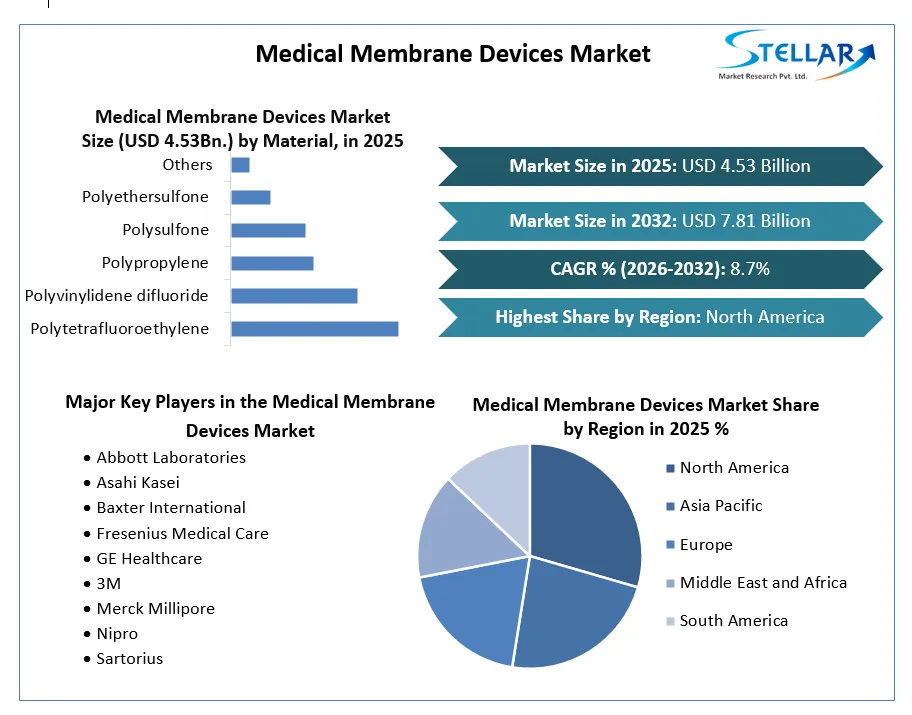

The Global Medical Membrane Devices Market size reached USD 4.53 billion in 2024 and expects the market to reach USD 7.81 billion by 2032, exhibiting a CAGR of 8.07% during 2026-2032.

Medical Membrane Devices Market Overview:

A membrane is a very thin layer of tissue that separates one organ from another, lines a cavity, or covers its surface. A cell or organelle must have this type of selectively permeable structure to effectively separate from its environment. Medical uses for membranes include drug delivery, prosthetic organs, tissue regeneration, diagnostic tools, coatings for medical equipment, bio-separations, etc. Medical membranes are instruments constructed of organic and inorganic polymers that are frequently utilized in therapeutic procedures.

One of the primary drivers of the medical membranes market's expansion is the quick increase in the use of medical membranes in the healthcare sector, the rising demand for high-purity products as a result of biotechnology advancements, the rising incidence of diseases worldwide, and the expanding life science and healthcare sectors. Furthermore, a number of benefits medical membranes provide, such as filtration methods to recover components such as concentrated proteins and enzymes, are boosting demand for the medical membrane market globally.

Another factor influencing the growth of the Medical Membranes Market is the rising demand for high-purity products in the pharmaceutical and healthcare sectors. Pre-filtration, sample preparation, and infusion therapy, venting and gas filtration, and sterile filtration are also common uses for medical membranes. Thus, it is projected that during the course of the forecast period, the use of medical membranes in hemodialysis and pharmaceutical filtration will increase.

Despite the medical membrane's many benefits, certain elements limit and pose challenges to the market's expansion as a whole. The global medical membranes market could be hampered by factors such as the fact that, despite the high demand for medical products and equipment, producers are now constrained by the FDA's complicated regulations. Another important factor impeding the growth of the medical membranes market is the protracted validation process for medical membranes, which delays their commercialization.

To get more Insights: Request Free Sample Report

Medical Membrane Devices Market Dynamics:

Growing Prevalence of Chronic Diseases, Increasing Geriatric Population, Rising Demand for Biopharmaceuticals, etc.

There is now a greater demand for dialysis and filtration systems, which heavily rely on medical membranes, as a result of the rising prevalence of chronic diseases like diabetes, kidney problems, and cardiovascular diseases.

Age-related eye illnesses and kidney failure are two medical conditions that are more common in the aging population. Medical membrane devices like prosthetic kidneys and intraocular lenses are in high demand due to this demographic shift. For procedures like protein purification and medication development, the biopharmaceutical sector depends on membrane technology. The need for cutting-edge membrane devices rises along with the need for biopharmaceuticals.

Organ transplants are one of the increasingly common surgical procedures. Organ preservation, tissue engineering, and regenerative medicine applications all depend on medical membrane devices. Applications like blood glucose monitoring and lipid profile testing frequently use membrane-based technology in point-of-care testing devices. The demand for quick and accurate diagnostic tests is growing, which helps the market expand.

Medical Membrane Devices Market Restraints:

Stringent Regulatory Approval Process, High Manufacturing Costs, etc.

Medical membrane devices must pass rigorous regulatory inspections and approval procedures, which can take a long time and be costly. This may result in new product introduction delays and higher development expenses.

High production costs are a result of the use of sophisticated materials and exacting manufacturing techniques in the manufacture of high-quality medical membrane devices. These expenses may make it difficult for smaller businesses to enter the market and may have an impact on how much the devices cost. Medical membrane device costs may not be fully covered by reimbursement policies in many healthcare systems, and their use may therefore be constrained. This could limit the use of these gadgets and shrink the size of the potential market.

Advanced medical membrane device development and upkeep demand a high level of technical proficiency. It can be difficult for manufacturers to keep up with the quickly changing technology while maintaining the durability of their products. The failure or contamination of medical membrane devices, which are frequently utilized in crucial medical applications, could have major negative effects on patients. To reduce this danger, manufacturers must invest in strict quality control and testing procedures.

Medical Membrane Devices Market Opportunities:

Growing Aging Population, Global Healthcare Infrastructure Expansion, etc.

As the world's population ages, chronic diseases like diabetes and renal disease are becoming more common. This increases the need for hemodialysis membranes and other medical membrane devices, which are crucial for treating these disorders.

New healthcare infrastructure is being developed in emerging economies. The need for medical membrane devices in these areas will rise as access to healthcare increases. Healthcare facilities produce a lot of wastewater, which needs to be treated to prevent environmental contamination. Wastewater can be treated using medical membrane devices, providing healthcare professionals with a long-lasting and economical option.

Advances in genomics and proteomics are driving the demand for personalized medicine. Medical membrane devices are used in various applications, such as DNA sequencing and protein separation, supporting the development of personalized treatment plans.

Medical Membrane Devices Market Challenges:

Product Development and Customization, Quality Control and Assurance, etc.

Customized solutions are frequently needed to address the unique needs of healthcare professionals and patients. Customized product development and delivery can be difficult and time-consuming.

Medical membrane device quality and dependability must be guaranteed. To avoid flaws and recalls, manufacturers must put in place effective quality control and assurance procedures.

Devices made of medical membranes must be biocompatible in order to avoid negative reactions when they come into touch with the body. It can be difficult to find materials that are both functional and biocompatible.

Medical Membrane Devices Market Trends

There was a growing interest in advanced wound care products, including wound dressings with semi-permeable membranes. These membranes help maintain a moist wound environment, facilitate healing, and prevent infections.

Medical Membrane Devices Market Regional Insights:

The market for medical membrane devices in North America is dominated by the United States, which holds more than 80% of the regional market share. The expansion of the market in this area is attributed to the rise in the incidence of chronic illnesses such as kidney disease and diabetes as well as the rising demand for hemodialysis and other medical treatments that require membrane devices.

The European market for medical membrane devices is the second largest in the world, accounting for nearly 30% of the global market. The aging population in this region and the rising prevalence of chronic diseases are both thought to be driving forces behind the market's rise.

The market for medical membrane devices in Asia Pacific is growing at the fastest rate worldwide, with a CAGR of over 10% throughout the duration of the projection. The market is expanding in this area due to reasons such as the rising prevalence of chronic diseases, the rising demand for healthcare services, and the rising disposable incomes of the population.

The market for medical membrane devices in Latin America, which is currently relatively modest, is anticipated to grow significantly over the next few years due to the rising incidence of chronic diseases and the expanding need for healthcare services in this region.

Although the market for medical membrane devices in the Middle East and Africa is still modest, it is predicted to increase moderately over the next several years as a result of the region's rising demand for healthcare services and rising prevalence of chronic diseases.

Medical Membrane Devices Market Segment Analysis:

By Process Technology, The ultrafiltration (UF) segment will likely dominate the market for medical membrane devices throughout the anticipated time frame. This is due to the increased usage of UF technology in hemodialysis and drug delivery applications. UF membranes have a wide range of medical applications, including the treatment of wounds, blood filtration, and water filtration.

By Application, The market for medical membrane devices is anticipated to be dominated by the hemodialysis segment during the forecasted period. This is brought on by the rising incidence of end-stage renal disease (ESRD) and chronic kidney disease (CKD) globally. Medical membrane devices are essential to hemodialysis, a procedure that can save the lives of ESRD patients.

By Material, The PTFE category is expected to hold the largest market share for medical membrane devices during the projection period. This is caused by the outstanding biocompatibility and chemical resistance of PTFE membranes. PTFE membranes are also used in several medical operations, including hemodialysis, drug delivery, and wound treatment.

Medical Membrane Devices Market Competitive Landscape:

In September 2023, Abbott acquired Bigfoot Biomedical, a company that develops automated insulin delivery systems for people with diabetes. This acquisition is part of Abbott's efforts to develop more personalized and connected solutions for people with diabetes.

On August 2, 2023, Fresenius Medical Care announced strong operational performance in the first half of 2023, with revenue increasing by 8.1% year-over-year to EUR 17.2 billion and EBIT increasing by 7.0% to EUR 1.6 billion. The company also narrowed its guidance range for the full year, expecting revenue of EUR 34.5 billion to EUR 35.5 billion and EBIT of EUR 3.1 billion to EUR 3.3 billion.

|

Medical Membrane Devices Market Scope |

|

|

Market Size in 2025 |

USD 4.53 Billion. |

|

Market Size in 2032 |

USD 7.81 Billion. |

|

CAGR (2026-2032) |

8.07% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

By Process Technology:

|

|

By Application:

|

|

|

By Material:

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Medical Membrane Devices Market Key Players:

- Abbott Laboratories

- Asahi Kasei

- Baxter International

- Fresenius Medical Care

- GE Healthcare

- 3M

- Merck Millipore

- Nipro

- Sartorius

- Toray Industries

- W.L. Gore & Associates

Frequently Asked Questions

The Medical Membrane Devices Market size is expected to reach US$ 7.81 billion by 2032.

The major players in the Cancer Vaccines Drug Pipeline Market include Abbott Laboratories Asahi Kasei Baxter International Fresenius Medical Care GE Healthcare 3M Merck Millipore Nipro Sartorius Toray Industries W.L. Gore & Associates.

The expected CAGR of the Medical Membrane Devices Market is 8.07% from 2026 to 2032.

The North American market dominated the Medical Membrane Devices Market by Region in 2025.

1. Global Medical Membrane Devices Market: Research Methodology

2. Global Medical Membrane Devices Market: Executive Summary

3. Global Medical Membrane Devices Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Consolidation of the Market

4. Global Medical Membrane Devices Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers by Region

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.7. PESTLE Analysis

4.8. Value Chain Analysis

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Global Medical Membrane Devices Market Size and Forecast by Segments (by Value USD and Volume Units)

5.1. Global Medical Membrane Devices Market Size and Forecast, by Process Technology (2026-2032)

5.1.1. Ultrafiltration (UF)

5.1.2. Microfiltration (MF)

5.1.3. Nanofiltration (NF)

5.1.4. Reverse osmosis (RO)

5.1.5. Dialysis

5.1.6. Gas filtration

5.1.7. Others

5.2. Global Medical Membrane Devices Market Size and Forecast, by Application(2026-2032)

5.2.1. Hemodialysis

5.2.2. Drug delivery

5.2.3. Intravenous (IV) infusion & sterile filtration

5.2.4. Bio-artificial processes

5.2.5. Others

5.3. Global Medical Membrane Devices Market Size and Forecast, by Material (2026-2032)

5.3.1. Polytetrafluoroethylene (PTFE)

5.3.2. Polyvinylidene difluoride (PVDF)

5.3.3. Polypropylene (PP)

5.3.4. Polysulfone (PSU)

5.3.5. Polyethersulfone (PESU)

5.3.6. Others

5.4. Global Medical Membrane Devices Market Size and Forecast, by Region (2026-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Global Medical Membrane Devices Market Size and Forecast (by Value USD and Volume Units)

6.1. North America Global Medical Membrane Devices Market Size and Forecast, by Process Technology (2026-2032)

6.1.1. Ultrafiltration (UF)

6.1.2. Microfiltration (MF)

6.1.3. Nanofiltration (NF)

6.1.4. Reverse osmosis (RO)

6.1.5. Dialysis

6.1.6. Gas filtration

6.1.7. Others

6.2. North America Global Medical Membrane Devices Market Size and Forecast, by Application(2026-2032)

6.2.1. Hemodialysis

6.2.2. Drug delivery

6.2.3. Intravenous (IV) infusion & sterile filtration

6.2.4. Bio-artificial processes

6.2.5. Others

6.3. North America Global Medical Membrane Devices Market Size and Forecast, by Material (2026-2032)

6.3.1. Polytetrafluoroethylene (PTFE)

6.3.2. Polyvinylidene difluoride (PVDF)

6.3.3. Polypropylene (PP)

6.3.4. Polysulfone (PSU)

6.3.5. Polyethersulfone (PESU)

6.3.6. Others

6.4. North America Global Medical Membrane Devices Market Size and Forecast, by Country (2026-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Global Medical Membrane Devices Market Size and Forecast (by Value USD and Volume Units)

7.1. Europe Global Medical Membrane Devices Market Size and Forecast, by Process Technology (2026-2032)

7.1.1. Ultrafiltration (UF)

7.1.2. Microfiltration (MF)

7.1.3. Nanofiltration (NF)

7.1.4. Reverse osmosis (RO)

7.1.5. Dialysis

7.1.6. Gas filtration

7.1.7. Others

7.2. Europe Global Medical Membrane Devices Market Size and Forecast, by Application(2026-2032)

7.2.1. Hemodialysis

7.2.2. Drug delivery

7.2.3. Intravenous (IV) infusion & sterile filtration

7.2.4. Bio-artificial processes

7.2.5. Others

7.3. Europe Global Medical Membrane Devices Market Size and Forecast, by Material (2026-2032)

7.3.1. Polytetrafluoroethylene (PTFE)

7.3.2. Polyvinylidene difluoride (PVDF)

7.3.3. Polypropylene (PP)

7.3.4. Polysulfone (PSU)

7.3.5. Polyethersulfone (PESU)

7.3.6. Others

7.4. Europe Global Medical Membrane Devices Market Size and Forecast, by Country (2026-2032)

7.4.1. UK

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Global Medical Membrane Devices Market Size and Forecast (by Value USD and Volume Units)

8.1. Asia Pacific Global Medical Membrane Devices Market Size and Forecast, by Process Technology (2026-2032)

8.1.1. Ultrafiltration (UF)

8.1.2. Microfiltration (MF)

8.1.3. Nanofiltration (NF)

8.1.4. Reverse osmosis (RO)

8.1.5. Dialysis

8.1.6. Gas filtration

8.1.7. Others

8.2. Asia Pacific Global Medical Membrane Devices Market Size and Forecast, by Application(2026-2032)

8.2.1. Hemodialysis

8.2.2. Drug delivery

8.2.3. Intravenous (IV) infusion & sterile filtration

8.2.4. Bio-artificial processes

8.2.5. Others

8.3. Asia Pacific Global Medical Membrane Devices Market Size and Forecast, by Material (2026-2032)

8.3.1. Polytetrafluoroethylene (PTFE)

8.3.2. Polyvinylidene difluoride (PVDF)

8.3.3. Polypropylene (PP)

8.3.4. Polysulfone (PSU)

8.3.5. Polyethersulfone (PESU)

8.3.6. Others

8.4. Asia Pacific Global Medical Membrane Devices Market Size and Forecast, by Country (2026-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Bangladesh

8.4.11. Pakistan

8.4.12. Rest of Asia Pacific

9. Middle East and Africa Global Medical Membrane Devices Market Size and Forecast (by Value USD and Volume Units)

9.1. Middle East and Africa Global Medical Membrane Devices Market Size and Forecast, by Process Technology (2026-2032)

9.1.1. Ultrafiltration (UF)

9.1.2. Microfiltration (MF)

9.1.3. Nanofiltration (NF)

9.1.4. Reverse osmosis (RO)

9.1.5. Dialysis

9.1.6. Gas filtration

9.1.7. Others

9.2. Middle East and Africa Global Medical Membrane Devices Market Size and Forecast, by Application(2026-2032)

9.2.1. Hemodialysis

9.2.2. Drug delivery

9.2.3. Intravenous (IV) infusion & sterile filtration

9.2.4. Bio-artificial processes

9.2.5. Others

9.3. Middle East and Africa Global Medical Membrane Devices Market Size and Forecast, by Material (2026-2032)

9.3.1. Polytetrafluoroethylene (PTFE)

9.3.2. Polyvinylidene difluoride (PVDF)

9.3.3. Polypropylene (PP)

9.3.4. Polysulfone (PSU)

9.3.5. Polyethersulfone (PESU)

9.3.6. Others

9.4. Middle East and Africa Global Medical Membrane Devices Market Size and Forecast, by Country (2026-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Egypt

9.4.4. Nigeria

9.4.5. Rest of ME&A

10. South America Global Medical Membrane Devices Market Size and Forecast (by Value USD and Volume Units)

10.1. South America Global Medical Membrane Devices Market Size and Forecast, by Process Technology (2026-2032)

10.1.1. Ultrafiltration (UF)

10.1.2. Microfiltration (MF)

10.1.3. Nanofiltration (NF)

10.1.4. Reverse osmosis (RO)

10.1.5. Dialysis

10.1.6. Gas filtration

10.1.7. Others

10.2. South America Global Medical Membrane Devices Market Size and Forecast, by Application(2026-2032)

10.2.1. Hemodialysis

10.2.2. Drug delivery

10.2.3. Intravenous (IV) infusion & sterile filtration

10.2.4. Bio-artificial processes

10.2.5. Others

10.3. South America Global Medical Membrane Devices Market Size and Forecast, by Material (2026-2032)

10.3.1. Polytetrafluoroethylene (PTFE)

10.3.2. Polyvinylidene difluoride (PVDF)

10.3.3. Polypropylene (PP)

10.3.4. Polysulfone (PSU)

10.3.5. Polyethersulfone (PESU)

10.3.6. Others

10.4. South America Global Medical Membrane Devices Market Size and Forecast, by Country (2026-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest of South America

11. Company Profile: Key players

11.1.1. Abbott Laboratories

11.1.2. Company Overview

11.1.3. Financial Overview

11.1.4. Business Portfolio

11.1.5. SWOT Analysis

11.1.6. Business Strategy

11.1.7. Recent Developments

11.2. Asahi Kasei

11.3. Baxter International

11.4. Fresenius Medical Care

11.5. GE Healthcare

11.6. 3M

11.7. Merck Millipore

11.8. Nipro

11.9. Sartorius

11.10. Toray Industries

11.11. W.L. Gore & Associates

12. Key Findings

13. Industry Recommendation