Hemangioblastoma Market Global Industry Analysis and Forecast (2026-2032)

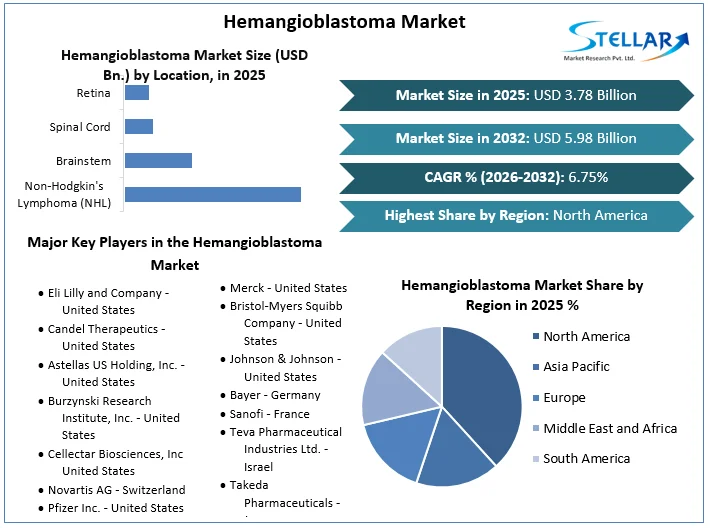

The Hemangioblastoma Market size was valued at USD 3.78 Bn. in 2025 and the total Hemangioblastoma Market size is expected to grow at a CAGR of 6.75% from 2026 to 2032, reaching nearly USD 5.98 Bn. by 2032.

Hemangioblastoma Market Overview

Hemangioblastoma is a rare brain tumor rising from blood vessel cells. Market elements for hemangioblastoma are influenced by factors such as prevalence, treatment choices, research advancements, and patient outcomes. The market is partial by the prevalence and incidence rates of hemangioblastomas, with a focus on understanding the patient population and potential market size. Advancements in imaging techniques and hereditary testing are crucial for effective management, while research in diagnostics promotes growth. Treatment options for hemangioblastoma include careful resection, radiation treatment, and sometimes designated treatment.

The market is also influenced by financial considerations, such as medicine costs, insurance coverage, and repayment contracts. The future of the hemangioblastoma market is expected to be shaped by research advancements, innovative treatment approaches, and collaboration among partners. As the understanding of the disease increases, market elements are expected to evolve to better address the needs of patients and healthcare providers.

To get more Insights: Request Free Sample Report

Hemangioblastoma Market Dynamics:

The Hemangioblastoma market is driven by the increasing prevalence and awareness of the condition, with an estimated 1-2 cases per million people per year. Organizations like the National Brain Tumor Society and the American Brain Tumor Association are raising awareness and providing resources, support, and funding for research. Advances in analytical methods, such as magnetic resonance imaging (MRI) and computed tomography (CT), have enabled more precise and early detection. The genetic basis of hemangioblastoma has become a key focus, with a significant number of cases related to von Hippel-Lindau (VHL) disease, a genetic condition linked to changes in VHL quality.

The Hemangioblastoma Market patterns reflect a multidisciplinary approach to treating hemangioblastoma, with medical procedures being the primary treatment. Advances in radiation treatment and targeted drug treatments are emerging as alternatives, offering more personalized treatment plans. Increased awareness among medical professionals and the general public has contributed to early detection, impacting patient outcomes.

The market of Hemangioblastoma is facing significant difficulties because of the high cost of treatment, limited reimbursement policies, and geographical incompatibilities. Despite progress, challenges persist in admitting individuals with rare brain tumors. Geographic incompatibilities, limited skills, and financial requirements pose challenges to management. However, advancements in exploration, diagnostics, and treatment modalities are expected to drive market growth.

As awareness and cooperation increase, the future of hemangioblastoma management is expected to improve. Also, many insurance plans have limited coverage for rare diseases like Hemangioblastoma, leaving patients with high out-of-pocket expenses. The lack of comprehensive reimbursement policies and financial burden hinder the adoption of advanced treatments and technologies in the Hemangioblastoma market.

The Hemangioblastoma market has a great deal of opportunity because of the advancement of customized medicine and targeted therapy. Researchers are looking at new therapeutic targets and biomarkers unique to hemangioblastoma, which result in the creation of more specialized and potent therapies. For instance, a research that was published in the journal Nature Communications identified the hypoxia-inducible factor 2a (HIF-2a) as a possible therapeutic target that is used in the treatment of hemangioblastoma.

The effectiveness and safety of Hemangioblastoma therapies are expected to increase with the emerging trend of personalized medicine, which customizes treatments based on a patient's genetic profile and tumor features. The Hemangioblastoma market is expected to increase in the upcoming years because of the use of precision medicine techniques, which are encouraged by programs like the National Institutes of Health's (NIH) Precision Medicine Initiative.

Hemangioblastoma Market Segment Analysis:

Based on Type, The Hemangioblastoma market is segmented by type, with Sporadic Hemangioblastoma being the largest sub-segment in 2025. Sporadic Hemangioblastomas are non-hereditary tumors that account for 75% of all Hemangioblastoma cases, typically solitary and occurring in various locations within the central nervous system, with the cerebellum being the most common site. The higher prevalence of sporadic Hemangioblastomas compared to VHL-associated cases has contributed to its dominant market position. The fastest-growing sub-segment is predicted to be Von Hippel-Lindau (VHL) Disease-Associated Hemangioblastoma, a rare genetic disorder characterized by multiple tumors in various organs.

Advancements in genetic testing and targeted therapies, such as anti-angiogenic agents and HiF inhibitors, have shown promise in treating VHL-associated Hemangioblastomas. As research continues to unravel the underlying mechanisms of VHL-associated Hemangioblastomas and more targeted treatments become available, this sub-segment is expected to witness significant growth in the upcoming years.

Hemangioblastoma Market Regional Insight:

The North American Hemangioblastoma Market held an XX% market share in 2025, driven by developed healthcare systems, rising healthcare costs, and the presence of major competitors. The increasing female and senior population contributes to the progress of the regional market. The United States had the largest market share, while Canada experienced the fastest growth. North America's high healthcare expenditure, advanced medical infrastructure, and increasing prevalence of brain tumors contribute to its dominance.

The incidence rate of primary central nervous system tumors, including Hemangioblastoma, in the United States was 24.8 per 100,000 with steady growth over the past few decades. The presence of well-established healthcare systems, favorable reimbursement policies, and a strong focus on research and development have contributed to the growth of the Hemangioblastoma market in North America.

Hemangioblastoma Market Competitive Landscape:

- May 22, 2024, Candel Therapeutics, Inc. a clinical-stage biopharmaceutical company focused on developing multimodal biological immunotherapies to help patients fight cancer.

- May 29, 2024, Cellectar Biosciences, Inc. (NASDAQ: CLRB), a late-stage clinical biopharmaceutical company focused on the discovery, development, and commercialization of targeted drugs for the treatment of cancer, announced today a strategic partnership with City of Hope Cancer Center, one of the largest cancer research and treatment organizations in the United States.

- June 11, 2024, Takeda Invests 230 Million US Dollars in Expanding Production Capacity for Plasma-Derived Therapies at Los Angeles Manufacturing Site.

|

Hemangioblastoma Market Scope |

|

|

Market Size in 2025 |

USD 3.78 Bn. |

|

Market Size in 2032 |

USD 5.98 Bn. |

|

CAGR (2026-2032) |

6.75 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Type Sporadic Hemangioblastoma Von Hippel-Lindau (VHL) Disease-Associated Hemangioblastoma |

|

By Location Non-Hodgkin's Lymphoma (NHL) Brainstem Spinal Cord Retina |

|

|

By Diagnosis Magnetic Resonance Imaging (MRI) Computed Tomography (CT) Scan Angiography Biopsy Others |

|

|

By End User Hospitals Specialty Clinics Ambulatory Surgical Centers Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Hemangioblastoma Market

- Eli Lilly and Company - United States

- Candel Therapeutics - United States

- Astellas US Holding, Inc. - United States

- Burzynski Research Institute, Inc. - United States

- Cellectar Biosciences, Inc - United States

- Novartis AG - Switzerland

- Pfizer Inc. - United States

- Roche - Switzerland

- AstraZeneca plc - United Kingdom

- Merck - United States

- Bristol-Myers Squibb Company - United States

- Johnson & Johnson - United States

- Bayer - Germany

- Sanofi - France

- Teva Pharmaceutical Industries Ltd. - Israel

- Takeda Pharmaceuticals - Japan

- Amgen Inc. - United States

- Eisai Co., Ltd. - Japan

- Integra LifeSciences - United States

- Apple Pharmaceuticals - United States

Frequently Asked Questions

North America is expected to lead the Hemangioblastoma Market during the forecast period.

An analysis of profit trends and projections for companies in the Hemangioblastoma Market is included, offering insights into factors driving profitability, cost management strategies, and financial performance metrics.

The Hemangioblastoma Market size was valued at USD 3.78 Billion in 2025 and the total Hemangioblastoma Market size is expected to grow at a CAGR of 6.75% from 2026 to 2032, reaching nearly USD 5.98 Billion by 2032.

The segments covered in the market report are by Type, by Location, by Diagnosis, and by End-user.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Hemangioblastoma Market Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Hemangioblastoma Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

4. Hemangioblastoma Market: Dynamics

4.1. Hemangioblastoma Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Hemangioblastoma Market Drivers

4.3. Hemangioblastoma Market Restraints

4.4. Hemangioblastoma Market Opportunities

4.5. Hemangioblastoma Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Hemangioblastoma Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

5.1. Hemangioblastoma Market Size and Forecast, by Type (2025-2032)

5.1.1. Sporadic Hemangioblastoma

5.1.2. Von Hippel-Lindau (VHL) Disease-Associated Hemangioblastoma

5.2. Hemangioblastoma Market Size and Forecast, by Location (2025-2032)

5.2.1. Non-Hodgkin's Lymphoma (NHL)

5.2.2. Brainstem

5.2.3. Spinal Cord

5.2.4. Retina

5.3. Hemangioblastoma Market Size and Forecast, by Diagnosis (2025-2032)

5.3.1. Magnetic Resonance Imaging (MRI)

5.3.2. Computed Tomography (CT) Scan

5.3.3. Angiography

5.3.4. Biopsy

5.3.5. Others

5.4. Hemangioblastoma Market Size and Forecast, by End User (2025-2032)

5.4.1. Hospitals

5.4.2. Specialty Clinics

5.4.3. Ambulatory Surgical Centers

5.4.4. Others

5.5. Hemangioblastoma Market Size and Forecast, by Region (2025-2032)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Hemangioblastoma Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

6.1. North America Hemangioblastoma Market Size and Forecast, by Type (2025-2032)

6.1.1. Sporadic Hemangioblastoma

6.1.2. Von Hippel-Lindau (VHL) Disease-Associated Hemangioblastoma

6.2. North America Hemangioblastoma Market Size and Forecast, by Location (2025-2032)

6.2.1. Non-Hodgkin's Lymphoma (NHL)

6.2.2. Brainstem

6.2.3. Spinal Cord

6.2.4. Retina

6.3. North America Hemangioblastoma Market Size and Forecast, by Diagnosis (2025-2032)

6.3.1. Magnetic Resonance Imaging (MRI)

6.3.2. Computed Tomography (CT) Scan

6.3.3. Angiography

6.3.4. Biopsy

6.3.5. Others

6.4. North America Hemangioblastoma Market Size and Forecast, by End User (2025-2032)

6.4.1. Hospitals

6.4.2. Specialty Clinics

6.4.3. Ambulatory Surgical Centers

6.4.4. Others

6.5. North America Hemangioblastoma Market Size and Forecast, by Country (2025-2032)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Hemangioblastoma Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

7.1. Europe Hemangioblastoma Market Size and Forecast, by Type (2025-2032)

7.2. Europe Hemangioblastoma Market Size and Forecast, by Location (2025-2032)

7.3. Europe Hemangioblastoma Market Size and Forecast, by Diagnosis (2025-2032)

7.4. Europe Hemangioblastoma Market Size and Forecast, by End User (2025-2032)

7.5. Europe Hemangioblastoma Market Size and Forecast, by Country (2025-2032)

7.5.1. United Kingdom

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Russia

7.5.8. Rest of Europe

8. Asia Pacific Hemangioblastoma Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

8.1. Asia Pacific Hemangioblastoma Market Size and Forecast, by Type (2025-2032)

8.2. Asia Pacific Hemangioblastoma Market Size and Forecast, by Location (2025-2032)

8.3. Asia Pacific Hemangioblastoma Market Size and Forecast, by Diagnosis (2025-2032)

8.4. Asia Pacific Hemangioblastoma Market Size and Forecast, by End User (2025-2032)

8.5. Asia Pacific Hemangioblastoma Market Size and Forecast, by Country (2025-2032)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. ASEAN

8.5.7. Rest of Asia Pacific

9. Middle East and Africa Hemangioblastoma Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

9.1. Middle East and Africa Hemangioblastoma Market Size and Forecast, by Type (2025-2032)

9.2. Middle East and Africa Hemangioblastoma Market Size and Forecast, by Location (2025-2032)

9.3. Middle East and Africa Hemangioblastoma Market Size and Forecast, by Diagnosis (2025-2032)

9.4. Middle East and Africa Hemangioblastoma Market Size and Forecast, by End User (2025-2032)

9.5. Middle East and Africa Hemangioblastoma Market Size and Forecast, by Country (2025-2032)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Egypt

9.5.4. Rest of ME&A

10. South America Hemangioblastoma Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

10.1. South America Hemangioblastoma Market Size and Forecast, by Type (2025-2032)

10.2. South America Hemangioblastoma Market Size and Forecast, by Location (2025-2032)

10.3. South America Hemangioblastoma Market Size and Forecast, by Diagnosis (2025-2032)

10.4. South America Hemangioblastoma Market Size and Forecast, by End User (2025-2032)

10.5. South America Hemangioblastoma Market Size and Forecast, by Country (2025-2032)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest Of South America

11. Company Profile: Key Players

11.1. Eli Lilly and Company - United States

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Candel Therapeutics - United States

11.3. Astellas US Holding, Inc. - United States

11.4. Burzynski Research Institute, Inc. - United States

11.5. Cellectar Biosciences, Inc - United States

11.6. Novartis AG - Switzerland

11.7. Pfizer Inc. - United States

11.8. Roche - Switzerland

11.9. AstraZeneca plc - United Kingdom

11.10. Merck - United States

11.11. Bristol-Myers Squibb Company - United States

11.12. Johnson & Johnson - United States

11.13. Bayer - Germany

11.14. Sanofi - France

11.15. Teva Pharmaceutical Industries Ltd. - Israel

11.16. Takeda Pharmaceuticals - Japan

11.17. Amgen Inc. - United States

11.18. Eisai Co., Ltd. - Japan

11.19. Integra LifeSciences - United States

11.20. Apple Pharmaceuticals - United States

11.21. XX.inc

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook