Automotive Power Distribution Block Market Global Industry Analysis and Forecast (2026-2032)

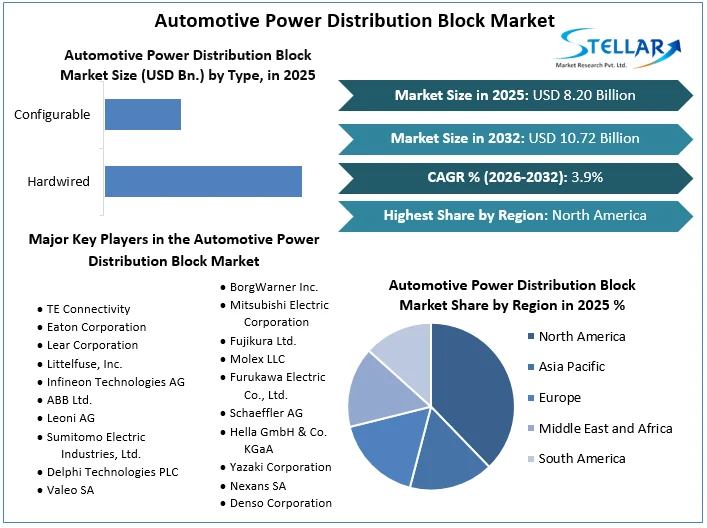

Automotive Power Distribution Block Market size was valued at USD 8.20 Bn. in 2025 and the total Automotive Power Distribution Block revenue is expected to grow at a CAGR of 3.90% from 2026 to 2032, reaching nearly USD 10.72 Bn. by 2032.

Automotive Power Distribution Block Market Overview:

Power Distribution Blocks allow easy connection of conductors to distribute power from one load into multiple smaller loads. The Automotive Power Distribution Block Market is a crucial component of the automotive electrical system, responsible for distributing electrical power from the battery and alternator to various vehicle functions. This market is experiencing significant growth driven by the increasing adoption of electric vehicles (EVs) and the advancement of automotive electronics. In terms of market size, the global automotive power distribution block market is projected to reach USD 10.73 billion by 2032, with a compound annual growth rate (CAGR) of 3.90%.

Asia Pacific region is expected to be a major growth area over the forecast period due to rapid urbanization, increasing automotive production, and supportive government policies promoting EV adoption. Examples include China, where government initiatives and subsidies have significantly boosted the market for power distribution blocks, with companies like BYD leading the way in adopting advanced power distribution systems for their Electric Vehicle Power Distribution.

The market is segmented based on type, component, electric vehicle (EV) type, and region. Key players in the market include TE Connectivity, Lear Corporation, Eaton Corporation, and Leoni. These companies are focused on innovations and strategic partnerships to enhance their market position. For instance, TE Connectivity has developed a new generation of smart power distribution units (PDUs) that integrate advanced diagnostics and telematics capabilities, providing real-time monitoring and control of electrical systems in vehicles.

To get more Insights: Request Free Sample Report

Automotive Power Distribution Block Market Dynamics:

The Increasing development of electric vehicles

The electric vehicle market is mainly driven by the continued use of electric vehicles and the development of electric vehicles (EVs). As the automotive industry shifts to sustainable solutions, the demand for efficient power systems is increasing. Additionally, advancements in automotive electronics such as advanced driver assistance systems (ADAS) and infotainment systems require reliable electronics to control the electrical systems in modern cars. Regulatory requirements to improve vehicle safety and energy efficiency are also contributing to the growth of the sector as companies produce more Electric Vehicle Power Distribution to meet these standards.

Furthermore, the increasing consumer preference for luxury vehicles with attractive electronics is increasing the demand for powerful electronics. Emerging markets, particularly the Asia Pacific region, are showing potential growth due to increasing vehicle production and the popularity of electric vehicles. Furthermore, the advancement of technology in electric distribution, and the development of smart and sets are increasing their business and attractiveness. The automotive industry’s efforts to reduce vehicle weight and improve fuel efficiency by optimizing electrical systems are also playing a significant role in supporting the economy. Overall, these factors together underline the strong growth trajectory of the electric vehicle distribution block market.

Competition between different vehicles with the increasing complexity of electric vehicles

Automotive power distribution blocks face some challenges during the growth of the market. The increasing complexity of electric vehicles is a major challenge due to the increasing demand for electronic components and connections in today's vehicles. This challenge requires stronger and more efficient power distribution solutions to handle greater flows of electricity and water while maintaining reliability and safety standards. According to recent market reports, the electric vehicle market is expected to grow at a compound annual growth rate (CAGR) of approximately 4.15% from 2018 to 2025, to approximately 100,000 large businesses. This development brings with it another challenge: innovation is needed to create strong distribution blocks that can be combined with different vehicle modifications.

Additionally, stringent regulations regarding vehicle safety and emissions introduce more complex processes that affect the design and implementation of energy solutions. In addition, market segmentation shows the different competition between different vehicles, where passenger cars, light commercial vehicles, and high-speed commercial vehicles all have special needs regarding electrical distribution and durability. Solving these challenges requires ongoing research and development to adapt to changing markets and consumer expectations. Overall, while the automobile electrical distribution block market is showing good growth, overcoming these issues is important to maintain power and meet future business expectations.

Opportunities

Automotive Power Distribution Block Market Driven by the advancement of technology and the popularity of electric vehicles (EVs), the electric vehicle distribution block market has great growth opportunities. According to market estimates, the Automotive Power Distribution Block market is expected to grow from USD 7.90 billion in 2024 at a CAGR of 3.90%, reaching a significant value by 2032.

The shift to electric and hybrid vehicles is a major driver because these cars need more electric motors to maintain good electrical equipment. Also, strict international regulations make it difficult for energy producers to obtain electricity, along with the need for different energy sources. The growth penetration of electric vehicles in the consumer market and category. Light commercial vehicles (LCVs) and heavy commercial vehicles (HCVs) have good growth potential due to the increasing use of electricity in the commercial fleet to reduce operating costs and comply with environmental standards.

Automotive Power Distribution Block Market Segment Analysis

By Types, The Automotive Power Distribution Block Market is segmented primarily into hardwired and configurable types, each catering to distinct needs within the automotive sector. Hardwired Power Distribution Blocks are robust systems that are very safe and reliable and cover a large part of the market. They are recommended for applications where safety and flexibility are important, such as heavy commercial vehicles (HCVs) and commercial machinery. According to the latest market data, wired modules account for approximately 60% of the market.

Configurable power distribution blocks are gaining interest due to their simplicity and optionality. This model makes it easy to integrate electronic components and switches to meet the needs of passenger cars and light commercial vehicles (LCVs). With advances in automotive electronics and increased use of electric vehicles, the installation segment is expected to grow at a CAGR of 3.90 % from 2026 to 2032.

Automotive Power Distribution Block Market Regional Analysis

In North America, The Hardwired Power Distribution Blocks segment dominates this market, given its cost-effectiveness and ease of installation. The market is bolstered by a strong automotive industry and increasing adoption of EVs. The region's market size is projected to reach USD XX billion by 2032, growing at a compound annual growth rate (CAGR) of XX % from 2026 to 2032. This growth is driven by technological advancements, government regulations promoting EV adoption, and increasing consumer awareness of sustainable transportation.

The U.S. leads the North American market due to its robust automotive infrastructure and substantial investments in research and development. This growth is attributed to the increasing adoption of advanced automotive technologies and the strong presence of leading automakers like Ford, General Motors, and Tesla. For example, Tesla's continuous innovation in EV Power Distribution Technologies requires advanced power distribution systems, boosting the market for power distribution blocks.

The Asia Pacific region, encompassing major automotive markets like China, Japan, and South Korea, is expected to witness robust growth in the automotive power distribution block market. This region accounts for 60% of the world's population, making it a significant consumer base for automobiles. The market is projected to register a CAGR of XX% and reach USD XX billion by 2032. China's rapid urbanization and government initiatives to promote EV adoption, such as subsidies and favourable policies, are key factors driving the market growth. For instance, BYD, a leading Chinese EV manufacturer, heavily relies on advanced power distribution systems to enhance vehicle efficiency and safety.

Automotive Power Distribution Block Market Competitive Landscape:

The Automotive Power Distribution Block Market is characterized by competition among key players, focusing on innovation, strategic partnerships, and regional expansions. Major players such as TE, have been front-runners in developing advanced power distribution solutions, focusing on compact and high-performance components. Connectivity, Eaton Corporation, and Lear Corporation dominate the market, leveraging their extensive experience and broad product portfolios.

For example, Eaton Corporation’s introduction of its "smart" power distribution units, which incorporate advanced diagnostics and connectivity features, provides real-time monitoring and control over vehicle electrical systems. This innovation not only improves vehicle performance and safety but also positions Eaton as a leader in automotive power distribution technology.

Automotive Power Distribution Block Market Scope:

|

Automotive Power Distribution Block Market |

|

|

Market Size in 2025 |

USD 8.20 Bn. |

|

Market Size in 2032 |

USD 10.72 Bn. |

|

CAGR (2026-2032) |

3.90% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Type Hardwired Configurable |

|

By Vehicle Type Passenger Vehicle Light Commercial Vehicles (LCVs) Heavy Commercial Vehicles (HCVs) |

|

|

By Material Metallic Power Distribution Block Non-metallic/ Plastic Power Distribution Block |

|

|

By Application Engine Control System Lighting System Infotainment and Navigation System Safety and Security System Battery Management System |

|

Automotive Power Distribution Block Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, 8.3.3. Nigeria, Rest of ME & A)

South America (Brazil, Argentina Rest of South America)

Automotive Power Distribution Block Market Key Players:

- TE Connectivity

- Eaton Corporation

- Lear Corporation

- Littelfuse, Inc.

- Infineon Technologies AG

- ABB Ltd.

- Leoni AG

- Sumitomo Electric Industries, Ltd.

- Delphi Technologies PLC

- Valeo SA

- BorgWarner Inc.

- Mitsubishi Electric Corporation

- Fujikura Ltd.

- Molex LLC

- Furukawa Electric Co., Ltd.

- Schaeffler AG

- Hella GmbH & Co. KGaA

- Yazaki Corporation

- Nexans SA

- Denso Corporation

Frequently Asked Questions

Language Learning Market size is expected to reach USD 10.72 Billion by 2032.

The segments covered in the market report are Type, Competitive Landscape, Regional Analysis.

North America had the largest share of the market.

1. Automotive Power Distribution Block Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market breakdown and Data Triangulation

1.4. Assumptions

2. Automotive Power Distribution Block Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Automotive Power Distribution Block Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

4. Automotive Power Distribution Block Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape

4.10.1. Market Regulation by Region

4.10.1.1. North America

4.10.1.2. Europe

4.10.1.3. Asia Pacific

4.10.1.4. Middle East and Africa

4.10.1.5. South America

4.10.2. Impact of Regulations on Market Dynamics

5. Automotive Power Distribution Block Market Size and Forecast by Segments (by Value USD Million and Volume in Units)

5.1. Automotive Power Distribution Block Market Size and Forecast, By Type (2025-2032)

5.1.1. Hardwired

5.1.2. Configurable

5.2. Automotive Power Distribution Block Market Size and Forecast, By Vehicle Type (2025-2032)

5.2.1. Passenger Vehicle

5.2.2. Light Commercial Vehicles (LCVs)

5.2.3. Heavy Commercial Vehicles (HCVs)

5.3. Automotive Power Distribution Block Market Size and Forecast, By Material (2025-2032)

5.3.1. Metallic Power Distribution Block

5.3.2. Non-metallic/ Plastic Power Distribution Block

5.4. Automotive Power Distribution Block Market Size and Forecast, By Application (2025-2032)

5.4.1. Engine Control System

5.4.2. Lighting System

5.4.3. Infotainment and Navigation System

5.4.4. Safety and Security System

5.4.5. Battery Management System

5.5. Automotive Power Distribution Block Market Size and Forecast, by Region (2025-2032)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Automotive Power Distribution Block Market Size and Forecast (by Value USD Million and Volume in Units)

6.1. North America Automotive Power Distribution Block Market Size and Forecast, By Type (2025-2032)

6.1.1. Hardwired

6.1.2. Configurable

6.2. North America Automotive Power Distribution Block Market Size and Forecast, By Vehicle Type (2025-2032)

6.2.1. Passenger Vehicle

6.2.2. Light Commercial Vehicles (LCVs)

6.2.3. Heavy Commercial Vehicles (HCVs)

6.3. North America Automotive Power Distribution Block Market Size and Forecast, By Material (2025-2032)

6.3.1. Metallic Power Distribution Block

6.3.2. Non-metallic/ Plastic Power Distribution Block

6.4. North America Automotive Power Distribution Block Market Size and Forecast, By Application (2025-2032)

6.4.1. Engine Control System

6.4.2. Lighting System

6.4.3. Infotainment and Navigation System

6.4.4. Safety and Security System

6.4.5. Battery Management System

6.5. North America Automotive Power Distribution Block Market Size and Forecast, by Country (2025-2032)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Automotive Power Distribution Block Market Size and Forecast (by Value USD Million and Volume in Units)

7.1. Europe Automotive Power Distribution Block Market Size and Forecast, By Type (2025-2032)

7.2. Europe Automotive Power Distribution Block Market Size and Forecast, By Vehicle Type (2025-2032)

7.3. Europe Automotive Power Distribution Block Market Size and Forecast, By Material (2025-2032)

7.4. Europe Automotive Power Distribution Block Market Size and Forecast, By Application (2025-2032)

7.5. Europe Automotive Power Distribution Block Market Size and Forecast, by Country (2025-2032)

7.5.1. UK

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Austria

7.5.8. Rest of Europe

8. Asia Pacific Automotive Power Distribution Block Market Size and Forecast (by Value USD Million and Volume in Units)

8.1. Asia Pacific Automotive Power Distribution Block Market Size and Forecast, By Type (2025-2032)

8.2. Asia Pacific Automotive Power Distribution Block Market Size and Forecast, By Vehicle Type (2025-2032)

8.3. Asia Pacific Automotive Power Distribution Block Market Size and Forecast, By Material (2025-2032)

8.4. Asia Pacific Automotive Power Distribution Block Market Size and Forecast, By Application (2025-2032)

8.5. Asia Pacific Automotive Power Distribution Block Market Size and Forecast, by Country (2025-2032)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. Indonesia

8.5.7. Malaysia

8.5.8. Vietnam

8.5.9. Taiwan

8.5.10. Bangladesh

8.5.11. Pakistan

8.5.12. Rest of Asia Pacific

9. Middle East and Africa Automotive Power Distribution Block Market Size and Forecast (by Value USD Million and Volume in Units)

9.1. Middle East and Africa Automotive Power Distribution Block Market Size and Forecast, By Type (2025-2032)

9.2. Middle East and Africa Automotive Power Distribution Block Market Size and Forecast, By Vehicle Type (2025-2032)

9.3. Middle East and Africa Automotive Power Distribution Block Market Size and Forecast, By Material (2025-2032)

9.4. Middle East and Africa Automotive Power Distribution Block Market Size and Forecast, By Application (2025-2032)

9.5. Middle East and Africa Automotive Power Distribution Block Market Size and Forecast, by Country (2025-2032)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Egypt

9.5.4. Nigeria

9.5.5. Rest of ME&A

10. South America Automotive Power Distribution Block Market Size and Forecast (by Value USD Million and Volume in Units)

10.1. South America Automotive Power Distribution Block Market Size and Forecast, By Type (2025-2032)

10.2. South America Automotive Power Distribution Block Market Size and Forecast, By Vehicle Type (2025-2032)

10.3. South America Automotive Power Distribution Block Market Size and Forecast, By Material (2025-2032)

10.4. South America Automotive Power Distribution Block Market Size and Forecast, By Application (2025-2032)

10.5. South America Automotive Power Distribution Block Market Size and Forecast, by Country (2025-2032)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest of South America

11. Company Profile: Key players

11.1. TE Connectivity

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc.)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Eaton Corporation

11.3. Lear Corporation

11.4. Littelfuse, Inc.

11.5. Infineon Technologies AG

11.6. ABB Ltd.

11.7. Leoni AG

11.8. Sumitomo Electric Industries, Ltd.

11.9. Delphi Technologies PLC

11.10. Valeo SA

11.11. BorgWarner Inc.

11.12. Mitsubishi Electric Corporation

11.13. Fujikura Ltd.

11.14. Molex LLC

11.15. Furukawa Electric Co., Ltd.

11.16. Schaeffler AG

11.17. Hella GmbH & Co. KGaA

11.18. Yazaki Corporation

11.19. Nexans SA

11.20. Denso Corporation

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook