Automotive Drivetrain Market: Perspective on Upcoming Impacts and Forecast Analysis (2026-2032) by Vehicle Type, Drive Type, and Region

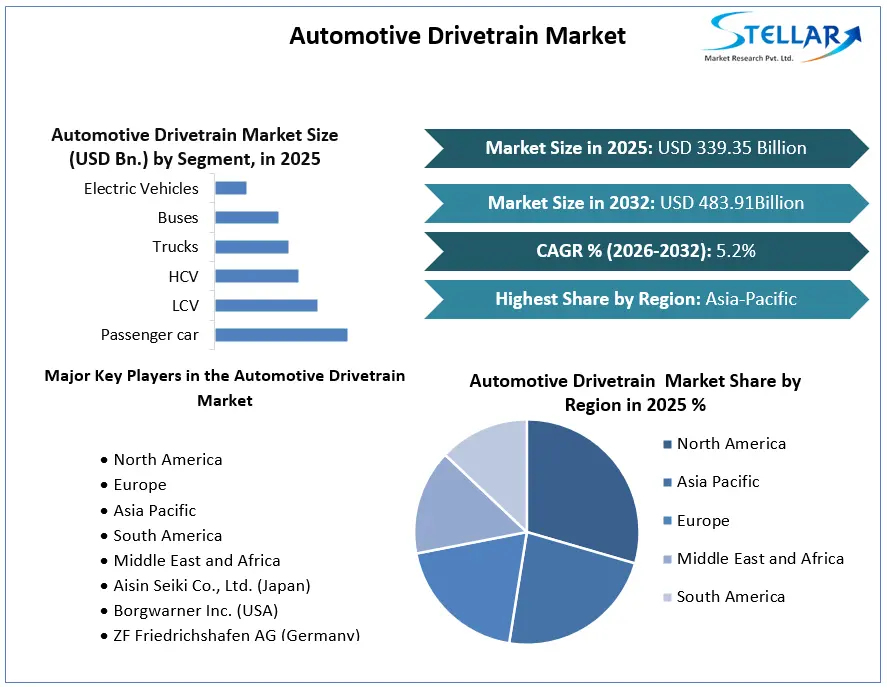

Automotive Drivetrain Market size was valued at USD 339.35 Billion in 2025 and the total Automotive Drivetrain Market revenue is expected to grow at 5.2% through 2025 to 2032, reaching nearly USD 483.91 Billion.

Automotive Drivetrain Market Overview:

The Automotive Drivetrain is responsible for transmitting power to the vehicle's steering wheel. It is also known as the powertrain or driveline. It is in charge of the vehicle's mobility, engine performance, and wheel performance. Improved vehicle performance and increased fuel efficiency are among the benefits of this type of technology. The drive train system is made up of several components such as wheels, drive shafts, U joints, and CV joints. Automotive Drivetrain market is expected to register CAGR of 40% during the forecast period.

To get more Insights: Request Free Sample Report

Automotive Drivetrain Market Dynamics:

Electric and hybrid vehicle sales are on the rise all around the world:

With rising worries about global emissions, the COP21 Paris agreement was drafted, with the goal of reducing the impact of emissions from various businesses. To capture unexplored regions, multiple major competitors are following the automotive drivetrain technology market trends. Furthermore, several countries that rely on automobile manufacture and sales have adopted or are on the cusp of implementing strict emission rules. For example, in India, the BS IV emission norms were implemented in 2017-2018, and the BS VI is expected to be implemented after 2020. Manufacturers in the Indian automotive drivetrain market have changed their focus to product development and sales of electric vehicles as a result of this.

Many governments and environmental agencies are establishing strict emission rules and laws in response to growing environmental concerns, which are projected to raise the production cost of fuel-efficient diesel engines in the future years. As a result, growth in the new commercial vehicle diesel engines category is projected to be slow in the near term. Furthermore, traditional fossil fuel-powered commercial vehicles, particularly trucks and buses, are contributing to rising transportation emissions. The introduction of fuel cell commercial vehicles, which are considered low- or zero-emission cars, is expected to cut heavy commercial vehicle emissions. E.g. Beiqi Foton Motor, a Chinese truck and bus manufacturer supported by the Chinese government, said in November 2019 that it would invest USD 2.6 billion in alternative energy vehicles, including fuel cell engines. By 2025, the business hopes to have deployed 200,000 new-energy commercial vehicles.

Globalization is causing fast changes in the automotive industry. The usage of electric vehicles has decreased pollutants to some extent, and this is projected to be a major contributor in the growth of the automotive drivetrain market. Furthermore, government incentives such as tax breaks, free parking, and other subsidies are driving up demand for electric vehicles. Furthermore, strong infrastructure development expenditure in most rising countries, such as China, India, and Brazil, enhances electric and hybrid car sales. According to the World Economic Forum, the UK government stated in July 2017 that it would stop producing new gasoline and diesel.

Increased technological progress:

Automobile manufacturers are concentrating their efforts on the development of superior electric vehicle systems with the maximum possible mileage and cheap costs. Companies have already begun creating reduced engines for use in vehicles, as smaller engines aid in meeting the forthcoming Bharat Stage VI emission standards. This is due to the fact that they emit fewer pollutants than heavier and larger engines. Furthermore, in comparison to electric vehicles, the drivetrain system in a fuel cell vehicle serves as the primary power source. Allison, for example, has produced a new AXE series e-axle for MD and HD trucks that is compatible with fuel cell range extenders (FCEV) or turbine generator range extenders (REV). Furthermore, a number of corporations are concentrating their R&D efforts on drivetrains. NSK Ltd., for example, has successfully demonstrated the world's first transmission-equipped wheel hub motor to increase vehicle environmental efficiency, safety, and comfort. Modern approaches for commercial vehicles, passenger vehicles, and three- and two-wheelers are available in the automotive drivetrain market.

Electric vehicles are expensive and have a small scale economy:

With growing worries about global emissions, governments and manufacturers have been working hard to cut emissions at the fleet level. This has had an impact on the uptake of electric automobiles. Although, due to a lack of EV charging infrastructure and a high vehicle price, sales volume is modest when compared to ICE automobiles. Furthermore, the high cost of electric vehicle components such as batteries and drivetrain, which account for over 60% of the market, is impeding the growth of the automotive drivetrain market. Different types of vehicles, such as passenger automobiles, light commercial vehicles, heavy commercial vehicles, fuel-cell vehicles, and electric vehicles, all employ the electric drivetrain system. Furthermore, the drivetrain's efficient operation is made up of a number of components, including electronic motors (synchronous and asynchronous), power electronic components, and various transmission units, depending on the vehicle's system. These elements are more expensive, which raises the total cost of the electric drive system. One of the reasons for the increase in car pricing is the high cost of the drivetrain system.

Automotive Drivetrain Market Segmentation:

The market is divided into three categories based on drive type: all-wheel drive, front-wheel drive, and rear-wheel drive. During the projected period, the All-Wheel-Drive sector is expected to grow at the fastest rate. AWD systems give superior traction and control, as well as high power; AWD is standard on most sports utility vehicles, contributing to the segment's rise (SUVs). In conjunction with AWD, it has counting stability control and anti-slip. Because of the reduced drag on the drivetrain, this type also helps to reduce fuel consumption. Currently, the AWD system is being used in small passenger cars and hybrid vehicles, which are leading the industry in terms of growth. This system was previously only available in high-end vehicles. Consumer purchasing power has increased in emerging markets like as China and Japan, resulting in increased demand for luxury and high-end automobiles in the Asia-Pacific region's automotive all-wheel-drive market.

The market is divided into Heavy Commercial Vehicles, Light Commercial Vehicles, Passenger Cars, and Electric Vehicles based on vehicle type. During the projection period, the Electric Vehicle segment is expected to develop significantly in terms of volume and has the highest CAGR. The issues can be ascribed to strict emission regulations, environmental concerns, and technological innovation.

Recent Developments by key players:

- CNH Industries stated in January 2020 that it would split in half and list its truck, bus, and engine divisions separately. It aims to merge agriculture and construction brands like Case and New Holland into one business, with a separate division to operate Iveco trucks, Iveco and Heuliez buses, and FPT powertrains. The separation is expected to be completed by early 2021.

- In February 2018, BMW unveiled its new i-lineup, which included a Roadster version of the i8, as well as i3s models with plug-in hybrid and electric powertrains.

- Tata Motors debuted the Tiago and Tigor with Electra EV powertrains in February 2018.

Automotive Drivetrain Market Regional Insights:

Asia Pacific Region is expected to grow at a significant rate:

In terms of value, the Asia-Pacific region has the largest powertrain market. The expanding vehicle production and the increase in passenger car penetration in the region are the key factors driving the growth of the automotive drivetrain market in the region. The cost of powertrain systems has increased as the market has grown, which is one of the key limitations.

The automotive drivetrain market examined is predicted to be driven by rising demand for luxury cars in places such as Europe and Asia-Pacific. The market for all-wheel-drive systems is projected to be heavily influenced by impending laws in several nations. The Asia-Pacific region's increased demand for AWD-equipped vehicles is expected to boost the market for all-wheel-drive systems.

The Asia-Pacific area has seen a tremendous increase in sales of new automobiles fitted with high-demand powertrain technologies. The market's growth has been aided by the increased use of all-wheel drive in SUVs from this region. The Asia-Pacific region is expected to drive the market for all-wheel-drive systems. In 2019, the total number of automobiles sold in the world was 89.36 million, down 4.9 percent from 2018. Despite a drop in vehicle sales in 2019 and the first quarter of 2020 due to the economy's collapse and the emergence of the Corona virus, sales are predicted to rebound by the end of 2021.

The objective of the report is to present a comprehensive analysis of the Automotive Drivetrain Market to the stakeholders in the industry. The report provides trends that are most dominant in the Automotive Drivetrain Market and how these trends will influence new business investments and market development throughout the forecast period. The report also aids in the comprehension of the market dynamics and competitive structure of the market by analyzing market leaders, market followers, and regional players.

The qualitative and quantitative data provided in the Automotive Drivetrain Market report is to help understand which market segments, regions are expected to grow at higher rates, factors affecting the market, and key opportunity areas, which will drive the industry and market growth through the forecast period. The report also includes the competitive landscape of key players in the industry along with their recent developments in the Automotive Drivetrain Market. The report studies factors such as company size, market share, market growth, revenue, production volume, and profits of the key players in the market.

The report provides Porter's Five Force Model, which helps in designing the business strategies in the market. The report helps in identifying how many rivals are existing, who they are, and how their product quality is in the Market. The report also analyses if the Automotive Drivetrain Market is easy for a new player to gain a foothold in the market, do they enter or exit the market regularly if the market is dominated by a few players, etc.

The report also includes a PESTEL Analysis, which aids in the development of company strategies. Political variables help in figuring out how much a government can influence the Market. Economic variables aid in the analysis of economic performance drivers that have an impact on the Market. Understanding the impact of the surrounding environment and the influence of environmental concerns on the Automotive Drivetrain Market is aided by legal factors.

Automotive Drivetrain Market Scope:

|

Automotive Drivetrain Market |

|

|

Market Size in 2025 |

USD 339.35 Bn. |

|

Market Size in 2032 |

USD 483.91 Bn. |

|

CAGR (2026-2032) |

5.2% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

by Vehicle type

|

|

by Drive Type

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Automotive Drivetrain Market Regional Analysis:

- North America

- Europe

- Asia Pacific

- South America

- Middle East and Africa

Automotive Drivetrain Market Players:

- Aisin Seiki Co., Ltd. (Japan)

- Borgwarner Inc. (USA)

- ZF Friedrichshafen AG (Germany)

- Dana Holding Corporation (USA)

- Showa Corporation (Japan)

- Schaeffler Group (Germany)

- American Axle & Manufacturing, Inc. (USA)

- GKN PLC (UK)

- Magna International Inc. (Canada)

- JTEKT Corporation. (Japan)

- UNIVANCE CORPORATION (Japan)

- Meritor, Inc. (USA)

- TREMEC. (USA)

- Eaton. (Ireland)

- AVTEC (India)

Frequently Asked Questions

Asia Pacific region have the highest growth rate in the Automotive Drivetrain market.

Aisin Seiki Co., Ltd. (Japan), Borgwarner Inc. (USA), ZF Friedrichshafen AG (Germany), Dana Holding Corporation (USA), Showa Corporation (Japan), Schaeffler Group (Germany), American Axle & Manufacturing, Inc. (USA), GKN PLC (UK), Magna International Inc. (Canada), JTEKT Corporation. (Japan), UNIVANCE CORPORATION (Japan), Meritor, Inc. (USA), TREMEC. (USA), Eaton. (Ireland), AVTEC (India) and others are the key players in the Automotive Drivetrain market.

Commercial cars segment is dominating the market owing to increasing penetration of fuel cell technology in LCVs across Europe and North America.

- Chapter 1 Scope of the Report

Chapter 2 Research Methodology

2.1.Research Process

2.2.Global Automotive Drivetrain Market: Target Audience

2.3.Global Automotive Drivetrain Market: Primary Research (As per Client Requirement)

2.4.Global Automotive Drivetrain Market: Secondary Research

Chapter 3 Executive Summary

Chapter 4 Competitive Landscape

4.1.Market Share Analysis, By Region, 2025-2032(In %)

4.1.1.North America Market Share Analysis, By Value, 2025-2032 (In %)

4.1.2.Europe Market Share Analysis, By Value, 2025-2032 (In %)

4.1.3.Asia Pacific Market Share Analysis, By Value, 2025-2032 (In %)

4.1.4.South America Market Share Analysis, By Value, 2025-2032 (In %)

4.1.5.Middle East and Africa Market Share Analysis, By Value, 2025-2032 (In %)

4.2.Market Dynamics

4.2.1.Market Drivers

4.2.2.Market Restraints

4.2.3.Market Opportunities

4.2.4.Market Challenges

4.2.5.PESTLE Analysis

4.2.6.PORTERS Five Force Analysis

4.2.7.Value Chain Analysis

4.3.Global Automotive Drivetrain Market Segmentation Analysis, 2026-2032 (Value USD Bn)

4.3.1.Global Market Share Analysis, By Drive Type, 2025-2032 (Value USD Bn)

4.3.1.1.AWD

4.3.1.2.FWD

4.3.1.3.RWD

4.3.2.Global Market Share Analysis, By Vehicle Type, 2025-2032 (Value USD Bn)

4.3.2.1.Passenger car

4.3.2.2.LCV

4.3.2.3.HCV

4.3.2.4.Trucks

4.3.2.5.Buses

4.3.2.6.Electric Vehicles

4.3.2.6.1.BEV

4.3.2.6.2.HEV

4.3.2.6.3.PHEV

4.4.North America Automotive Drivetrain Market Segmentation Analysis, 2026-2032 (Value USD Bn)

4.4.1.North America Market Share Analysis, By Drive Type, 2025-2032 (Value USD Bn)

4.4.1.1.AWD

4.4.1.2.FWD

4.4.1.3.RWD

4.4.2.North America Market Share Analysis, By Vehicle Type, 2025-2032 (Value USD Bn)

4.4.2.1.Passenger car

4.4.2.2.LCV

4.4.2.3.HCV

4.4.2.4.Trucks

4.4.2.5.Buses

4.4.2.6.Electric Vehicles

4.4.2.6.1.BEV

4.4.2.6.2.HEV

4.4.2.6.3.PHEV

4.4.3.North America Market Share Analysis, By Country, 2025-2032 (Value USD Bn)

4.4.3.1.US

4.4.3.2.Canada

4.4.3.3.Mexico

4.5.Europe Automotive Drivetrain Market Segmentation Analysis, 2026-2032 (Value USD Bn)

4.5.1.Europe Market Share Analysis, By Drive Type, 2025-2032 (Value USD Bn)

4.5.2.Europe Market Share Analysis, By Vehicle Type, 2025-2032 (Value USD Bn)

4.5.3.Europe Market Share Analysis, By Country, 2025-2032 (Value USD Bn)

4.5.3.1.UK

4.5.3.2.France

4.5.3.3.Germany

4.5.3.4.Italy

4.5.3.5.Spain

4.5.3.6.Sweden

4.5.3.7.Austria

4.5.3.8.Rest Of Europe

4.6.Asia Pacific Automotive Drivetrain Market Segmentation Analysis, 2026-2032 (Value USD Bn)

4.6.1.Asia Pacific Market Share Analysis, By Drive Type, 2025-2032 (Value USD Bn)

4.6.2.Asia Pacific Market Share Analysis, By Vehicle Type, 2025-2032 (Value USD Bn)

4.6.3.Asia Pacific Market Share Analysis, By Country, 2025-2032 (Value USD Bn)

4.6.3.1.China

4.6.3.2.India

4.6.3.3.Japan

4.6.3.4.South Korea

4.6.3.5.Australia

4.6.3.6.ASEAN

4.6.3.7.Rest Of APAC

4.7.South America Automotive Drivetrain Market Segmentation Analysis, 2026-2032 (Value USD Bn)

4.7.1.South America Market Share Analysis, By Drive Type, 2025-2032 (Value USD Bn)

4.7.2.South America Market Share Analysis, By Vehicle Type, 2025-2032 (Value USD Bn)

4.7.3.South America Market Share Analysis, By Country, 2025-2032 (Value USD Bn)

4.7.3.1.Brazil

4.7.3.2.Argentina

4.7.3.3.Rest Of South America

4.8.Middle East and Africa Automotive Drivetrain Market Segmentation Analysis, 2026-2032 (Value USD Bn)

4.8.1.Middle East and Africa Market Share Analysis, By Drive Type, 2025-2032 (Value USD Bn)

4.8.2.Middle East and Africa Market Share Analysis, By Vehicle Type, 2025-2032 (Value USD Bn)

4.8.3.Middle East and Africa Market Share Analysis, By Country, 2025-2032 (Value USD Bn)

4.8.3.1.South Africa

4.8.3.2.GCC

4.8.3.3.Egypt

4.8.3.4.Nigeria

4.8.3.5.Rest Of ME&A

Chapter 5 Stellar Competition Matrix

5.1.Global Stellar Competition Matrix

5.2.North America Stellar Competition Matrix

5.3.Europe Stellar Competition Matrix

5.4.Asia Pacific Stellar Competition Matrix

5.5.South America Stellar Competition Matrix

5.6.Middle East and Africa Stellar Competition Matrix

5.7.Key Players Benchmarking

5.7.1.Key Players Benchmarking By Drive Type, Pricing, Market Share, Investments, Expansion Plans, Physical Presence and Presence in the Market.

5.8.Mergers and Acquisitions in Operating Miles

5.8.1. M&A by Region, Value and Strategic Intent

Chapter 6 Company Profiles

6.1.Key Players

6.1.1.Aisin Seiki Co. Ltd. (Japan)

6.1.1.1.Company Overview

6.1.1.2.Source Portfolio

6.1.1.3.Financial Overview

6.1.1.4.Business Strategy

6.1.1.5.Key Developments

6.1.2.Borgwarner Inc. (USA)

6.1.3.ZF Friedrichshafen AG (Germany)

6.1.4.Dana Holding Corporation (USA)

6.1.5.Showa Corporation (Japan)

6.1.6.Schaeffler Group (Germany)

6.1.7.American Axle & Manufacturing, Inc. (USA)

6.1.8.GKN PLC (UK)

6.1.9.Magna International Inc. (Canada)

6.1.10.JTEKT Corporation. (Japan)

6.1.11.UNIVANCE CORPORATION (Japan)

6.1.12.Meritor, Inc. (USA)

6.1.13.TREMEC. (USA)

6.1.14.Eaton. (Ireland)

6.1.15.AVTEC (India)

6.2. Key Findings

6.3. Recommendations