Software Defined Vehicle Market Size, Share, Growth Trends, Research Insights , Industry Analysis and Forecast 2026–2034

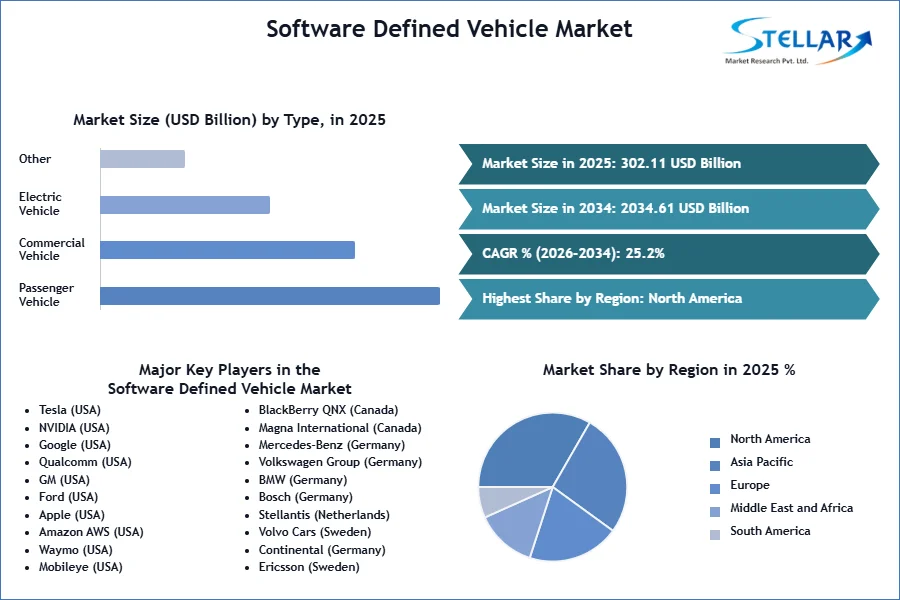

Software Defined Vehicle Market was valued at USD 302.11 bn in 2025, and its total revenue is expected to grow at a CAGR of 25.2% from 2026 to 2034, reaching nearly USD 2034.61 bn by 2034.

Software-Defined Vehicle Market Overview

A Software Defined Vehicle is a vehicle that uses software to perform its operation and improve functionality. It makes a significant evolution in the automotive industry. The Software Defined Vehicle Market is all about the software, with cars getting regular updates like smartphones.

The Software Defined market is rapidly expanding due to better batteries, autonomous driving technologies, and the development of electric vehicles (EVS). Customers now guess that their automobiles act like smart devices, which have underlying software and frequent updates. With its fully integrated software and hardware strategy, Tesla is leading this change, while installed vehicle manufacturers such as General Motors and Volkswagen are trying to remain competitive by collaborating with technical firms such as Google and NVIDIA. Companies like Xiaomi and BYD, located in the China, are rapidly developing EVs with state-of-the-art software and are growing rapidly in the Asia. Automobiles that continuously develop through software upgrades and combine rapid technology and dynamic domains are the future vehicles.

The success of some businesses is being slowed down by cybersecurity threats, expensive R&D, and ancient car design. Despite these challenges, the potential benefits are sufficient. Automakers now use the data-driven services to a create new revenue streams and offer a membership-based features, such as monthly fees for better performance or self-driving capabilities.

The Mercedes-Benz and Arm partnered in a January 2025 to incorporate Arm's semiconductor technology into the upcoming software defined automobiles. Through this collaboration, Arm's compute architecture is used for the safety, automation, and over-the-air upgrades, allowing for a more sophisticated autonomous capability and the customization in the future models, such as a high-end electric van scheduled for release in the spring.

To get more Insights: Request Free Sample Report

Software-Defined Vehicle Market Dynamics

Rise of Electric Vehicles (EVs) to Drive Software-Defined Vehicle Market Growth

Software-defined vehicle market growth is inspired by many major factors. The rise of electric vehicles (EVS) demands advanced software for battery management, energy efficiency, and autonomous functionality. Additionally, push towards autonomous driving (ADAS) requires refined AI and machine learning algorithms, increasing dependence on software-defined vehicle platforms. Connected car technologies, including 5G, V2X (vehicle-to-something-to-something), and over-the-air (OTA) updates, are able to improve real-time enhancement and cybersecurity. Consumer expectations for individual in-car experiences, such as AI-powered infotainment and adaptive driving mode, increase the demand. In addition, automakers benefit from cost capacity, as software update feature reduces the need for expensive hardware modifications when opening new revenue channels through feature subscription.

Adoption of Software-Defined Vehicle to Restrain the Market

Despite its rapid growth, the Software Defined Vehicle Market faces significant challenges in the market. Cybersecurity hazards pose a major risk, as an increase in connectivity makes vehicles more vulnerable to hacking and data breaches. The high cost of R&D for AI, autonomous systems, and cloud-based platforms creates financial barriers, especially for traditional vehicle manufacturers transition to hardware-centric models. Regulatory complications, including compliance with functional security and data privacy law, slow down deployment. Additionally, tradition vehicle manufacturers struggle with older vehicle architecture, making modern software solutions basically difficult to integrate.

Subscription-based Model to Boost Software-Defined Vehicle Market

The Software Defined Vehicle market offers a attractive opportunities for innovation and the revenue creation. Subscription-based models allow autonomous driving upgrades, add premium features like a performance boost, AI and machine learning, futuristic maintenance, individual driver help, and enhanced safety features. Strategic partnership between automakers and tech firms (eg, Nvidia, Microsoft, Qualcomm) accelerate software development and deployment. The edge of computing and the expansion of cloud platforms support real-time data processing to make autonomous decisions. In addition, government incentives for emerging markets and EV adoption in Asia-Pacific (China, India) create new development avenues. Since software becomes the main discriminator in automotive innovation, companies investing in scalable Software Defined Vehicle platforms gain a competitive lead.

Software-Defined Vehicle Market Segmentation

Based on Vehicle, passenger vehicles currently dominate the Software Defined Vehicle market landscape. This section is being converted by consumer expectations for connected car features, advanced driver-assessment system (ADAS), and individual in-vehicle experiences. Luxury automakers such as Tesla, BMW, and Mercedes-Benz are at the forefront, which integrate sophisticated AI-powered infotainment systems, voice assistants and autonomous driving capabilities. Trucks manufacturers such as Volvo, Daimler and Scania are investing heavy in cloud-connected platforms that enable fleet-wide software updates and data analytics. Electric vehicles (EVS) represent the fastest growing segment in the Software Defined Vehicle market. Unlike traditional vehicles, EVS requires special software for battery management systems (BMS), thermal regulation and energy optimization. Companies such as Tesla, and Rivian are predicting vehicle-to-grid integration and AI-run range, making the software an important discrimination in EV performance. As a global EV adoption, this section is expected to run the most innovation in over-the-air (OTA) updates and autonomous driving features.

Based on Deployment Model, Embedded software segment dominates with most of market share, handling important vehicle functions through Electronic Control Units and Advanced Driver Assistance Systems, incorporating Over-the-Air update capabilities for frequent improvement. Cloud-based solutions are rapidly experiencing development, which are enabling advanced features such as analytics and connected services of the AI-managed fleet through partnership with major cloud providers such as AWS and Azure. The newest approach combines both methods in hybrid instance, where the edge computing handles real-time autonomous decisions, while cloud systems manage data-intensive tasks-a strategy leading by leaders such as Tesla and Waymo. As the market develops, automakers are implementing mixed deployment strategies that balance real-time performance needs with cloud scalability, while all addressed the increasing cyber security concerns through zero-trust architecture and comply with regional data rules. This multi -layered perfect approach is enables unprecedented flexibility in vehicle software management and facilitates upgradation in the life cycle of a vehicle.

Software Defined Vehicle Market Regional Analysis

North America

The North America leads the Software Defined Vehicle market, inspired by the strong appearance of technical giants such as Tesla, google (Vaymo), and Nvidia, which are sharping the progress in autonomous driving and AI-operated dynamics. The region benefits from strong 5G infrastructure, which enables spontaneous vehicle-to-everything (V2X) communication, and high consumer demand for high consumer vehicles (EVS) connected with advanced software facilities.

Software Defined Vehicle Market Competitive Landscape

The Software Defined Vehicle market has a profound rivalry among key players in the competitive landscape of the market, and each developed automotive software brings different forces to the ecosystem. Tesla stands as an undisputed pioneer with its vertical integrated approach, controlling everything from its full self-driving AI to proprietary operating system, although its closed ecosystem limits the partnership. NVIDIA dominates the significant AI hardware space, its powerful drive through computing platform has become a brain for the next generation of vehicles of Mercedes-Benz and other automakers, although its success depends on the adoption deadline of the vehicle manufacturers. Qualcomm brings hardware and software through its Snapdragon Digital Chassis, provides a complete connectivity and autonomy solution to automakers such as BMW and Honda, although it directly competes with Nvidia's motor vehicle ambitions.

General Motors represent racing to replace traditional automakers, to distribute competitive OTA capabilities with their software platform and strategic Google partnership, but conflicts with the vehicle manufacturers compared to Tesla. This dynamic competition between tech giants and transforming automakers is intensifying innovation in vehicle operating system, autonomous driving and connected services, dying to control various layers of software defined vehicle price chain. Landscape remains liquid as fluid as companies balance ownership development with partnership, where success depends on giving spontaneous, safe and scalable software solutions.

|

Software Defined Vehicle Market Scope |

|

|

Market Size in 2025 |

USD 302.11 Bn. |

|

Market Size in 2034 |

USD 2034.61 Bn |

|

CAGR (2026-2034) |

25.2% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Vehicle Type Passenger Vehicle Commercial Vehicle Electric Vehicle |

|

By Software Layer Operating Systems Middleware Application Software |

|

|

By Deployment Model Embedded Software Cloud-Based Solutions Hybrid Models |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, Indonesia, Philippines, Malaysia, Vietnam, Thailand, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Software Defined Vehicle Market Key Players

North America

- Tesla (USA)

- NVIDIA (USA)

- Google (USA)

- Qualcomm (USA)

- GM (USA)

- Ford (USA)

- Apple (USA)

- Amazon AWS (USA)

- Waymo (USA)

- Mobileye (USA)

- BlackBerry QNX (Canada)

- Magna International (Canada)

Europe

- Mercedes-Benz (Germany)

- Volkswagen Group (Germany)

- BMW (Germany)

- Bosch (Germany)

- Stellantis (Netherlands)

- Volvo Cars (Sweden)

- Continental (Germany)

- Ericsson (Sweden)

Asia-Pacific

- Huawei (China)

- BYD (China)

- Toyota (Japan)

- Hyundai Motor Group (South Korea)

- Baidu (China)

- Xiaomi (China)

- Sony Honda Mobility (Japan)

- Tata Motors (India)

Middle East & Africa

- CEER (Saudi Arabia)

South America

- BYD Brasil (Brazil)

Frequently Asked Questions

EVs rely on software for battery and energy management. Their tech-heavy design accelerates Software Defined Vehicle integration.

Cybersecurity risks and high R&D costs hinder growth. Legacy car architectures resist software upgrades.

North America dominates with Tesla, NVIDIA, and 5G infrastructure. Asia-Pacific grows fast via China’s EV makers.

Subscription models (e.g., autonomous upgrades) unlock revenue. Data-driven services and OTA updates add value.

1. Software Defined Vehicle Market Introduction

1.1. Study Assumption and Market Definition

1.2. Scope of the Study

1.3. Executive Summary

2. Global Software Defined Vehicle Market: Competitive Landscape

2.1. SMR Competition Matrix

2.2. Competitive Landscape

2.3. Key Players Benchmarking

2.3.1. Company Name

2.3.2. Product Segment

2.3.3. End-user Segment

2.3.4. Revenue (2025)

2.4. Leading Software Defined Vehicle Market Companies, by Market Capitalization

2.5. Market Structure

2.5.1. Market Leaders

2.5.2. Market Followers

2.5.3. Emerging Players

2.6. Mergers and Acquisitions Details

3. Software Defined Vehicle Market: Dynamics

3.1. Software Defined Vehicle Market Trends by Region

3.1.1. North America Software Defined Vehicle Market Trends

3.1.2. Europe Software Defined Vehicle Market Trends

3.1.3. Asia Pacific Software Defined Vehicle Market Trends

3.1.4. Middle East & Africa Software Defined Vehicle Market Trends

3.1.5. South America Software Defined Vehicle Market Trends

3.2. Software Defined Vehicle Market Dynamics by Global

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

3.5. Value Chain Analysis

3.6. Regulatory Landscape by Region

3.6.1. North America

3.6.2. Europe

3.6.3. Asia Pacific

3.6.4. Middle East & Africa

3.6.5. South America

3.7. Analysis of Government Schemes and Initiatives for the Software Defined Vehicle Industry

4. Software Defined Vehicle Market: Global Market Size and Forecast by Segmentation (by Value USD Bn) (2026-2034)

4.1. Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

4.1.1. Passenger Vehicle

4.1.2. Commercial Vehicle

4.1.3. Electric Vehicle

4.2. Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

4.2.1. Operating Systems

4.2.2. Middleware

4.2.3. Application Software

4.3. Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

4.3.1. Embedded Software

4.3.2. Cloud-Based Solutions

4.3.3. Hybrid Model

4.4. Software Defined Vehicle Market Size and Forecast, By Region (2026-2034)

4.4.1. North America

4.4.2. Europe

4.4.3. Asia Pacific

4.4.4. Middle East & Africa

4.4.5. South America

5. North America Software Defined Vehicle Market Size and Forecast by Segmentation by Segmentation (by Value USD Bn) (2026-2034)

5.1. North America Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

5.1.1. Passenger Vehicle

5.1.2. Commercial Vehicle

5.1.3. Electric Vehicle

5.2. North America Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

5.2.1. Operating Systems

5.2.2. Middleware

5.2.3. Application Software

5.3. North America Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

5.3.1. Embedded Software

5.3.2. Cloud-Based Solutions

5.3.3. Hybrid Models

5.4. North America Software Defined Vehicle Market Size and Forecast, by Country (2026-2034)

5.4.1. United States

5.4.1.1. United States Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

5.4.1.1.1. Passenger Vehicle

5.4.1.1.2. Commercial Vehicle

5.4.1.1.3. Electric Vehicle

5.4.1.2. United States United States Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

5.4.1.2.1. Operating Systems

5.4.1.2.2. Middleware

5.4.1.2.3. Application Software

5.4.1.3. United States Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

5.4.1.3.1. Embedded Software

5.4.1.3.2. Cloud-Based Solutions

5.4.1.3.3. Hybrid Models

5.4.2. Canada

5.4.2.1. Canada Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

5.4.2.1.1. Passenger Vehicle

5.4.2.1.2. Commercial Vehicle

5.4.2.1.3. Electric Vehicle

5.4.2.2. Canada Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

5.4.2.2.1. Operating Systems

5.4.2.2.2. Middleware

5.4.2.2.3. Application Software

5.4.2.3. Canada Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

5.4.2.3.1. Embedded Software

5.4.2.3.2. Cloud-Based Solutions

5.4.2.3.3. Hybrid Models

5.4.3. Mexico

5.4.3.1. Mexico Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

5.4.3.1.1. Passenger Vehicle

5.4.3.1.2. Commercial Vehicle

5.4.3.1.3. Electric Vehicle

5.4.3.2. Mexico Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

5.4.3.2.1. Operating Systems

5.4.3.2.2. Middleware

5.4.3.2.3. Application Software

5.4.3.3. Mexico Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

5.4.3.3.1. Embedded Software

5.4.3.3.2. Cloud-Based Solutions

5.4.3.3.3. Hybrid Models

6. Europe Software Defined Vehicle Market Size and Forecast by Segmentation by Segmentation (by Value USD Bn) (2026-2034)

6.1. Europe Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

6.2. Europe Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

6.3. Europe Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

6.4. Europe Software Defined Vehicle Market Size and Forecast, by Country (2026-2034)

6.4.1. United Kingdom

6.4.1.1. United Kingdom Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

6.4.1.2. United Kingdom Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

6.4.1.3. United Kingdom Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

6.4.2. France

6.4.2.1. France Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

6.4.2.2. France Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

6.4.2.3. France Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

6.4.3. Germany

6.4.3.1. Germany Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

6.4.3.2. Germany Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

6.4.3.3. Germany Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

6.4.4. Italy

6.4.4.1. Italy Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

6.4.4.2. Italy Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

6.4.4.3. Italy Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

6.4.5. Spain

6.4.5.1. Spain Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

6.4.5.2. Spain Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

6.4.5.3. Spain Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

6.4.6. Sweden

6.4.6.1. Sweden Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

6.4.6.2. Sweden Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

6.4.6.3. Sweden Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

6.4.7. Austria

6.4.7.1. Austria Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

6.4.7.2. Austria Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

6.4.7.3. Austria Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

6.4.8. Rest of Europe

6.4.8.1. Rest of Europe Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

6.4.8.2. Rest of Europe Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

6.4.8.3. Rest of Europe Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

7. Asia Pacific Software Defined Vehicle Market Size and Forecast by Segmentation by Segmentation (by Value USD Bn) (2026-2034)

7.1. Asia Pacific Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

7.2. Asia Pacific Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

7.3. Asia Pacific Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

7.4. Asia Pacific Software Defined Vehicle Market Size and Forecast, by Country (2026-2034)

7.4.1. China

7.4.1.1. China Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

7.4.1.2. China Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

7.4.1.3. China Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

7.4.2. S Korea

7.4.2.1. S Korea Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

7.4.2.2. S Korea Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

7.4.2.3. S Korea Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

7.4.3. Japan

7.4.3.1. Japan Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

7.4.3.2. Japan Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

7.4.3.3. Japan Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

7.4.4. India

7.4.4.1. India Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

7.4.4.2. India Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

7.4.4.3. India Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

7.4.5. Australia

7.4.5.1. Australia Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

7.4.5.2. Australia Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

7.4.5.3. Australia Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

7.4.6. Indonesia

7.4.6.1. Indonesia Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

7.4.6.2. Indonesia Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

7.4.6.3. Indonesia Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

7.4.7. Philippines

7.4.7.1. Philippines Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

7.4.7.2. Philippines Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

7.4.7.3. Philippines Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

7.4.8. Malaysia

7.4.8.1. Malaysia Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

7.4.8.2. Malaysia Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

7.4.8.3. Malaysia Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

7.4.9. Vietnam

7.4.9.1. Vietnam Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

7.4.9.2. Vietnam Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

7.4.9.3. Vietnam Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

7.4.10. Thailand

7.4.10.1. Thailand Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

7.4.10.2. Thailand Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

7.4.10.3. Thailand Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

7.4.11. Rest of Asia Pacific

7.4.11.1. Rest of Asia Pacific Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

7.4.11.2. Rest of Asia Pacific Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

7.4.11.3. Rest of Asia Pacific Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

8. Middle East and Africa Software Defined Vehicle Market Size and Forecast by Segmentation by Segmentation (by Value USD Bn) (2026-2034)

8.1. Middle East and Africa Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

8.2. Middle East and Africa Software Defined Vehicle Market Size and Forecast, By Software Layer Model (2026-2034)

8.3. Middle East and Africa Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

8.4. Middle East and Africa Software Defined Vehicle Market Size and Forecast, by Country (2026-2034)

8.4.1. South Africa

8.4.1.1. South Africa Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

8.4.1.2. South Africa Software Defined Vehicle Market Size and Forecast, By Software Layer Model (2026-2034)

8.4.1.3. South Africa Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

8.4.2. GCC

8.4.2.1. GCC Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

8.4.2.2. GCC Software Defined Vehicle Market Size and Forecast, By Software Layer Model (2026-2034)

8.4.2.3. GCC Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

8.4.3. Nigeria

8.4.3.1. Nigeria Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

8.4.3.2. Nigeria Software Defined Vehicle Market Size and Forecast, By Software Layer Model (2026-2034)

8.4.3.3. Nigeria Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

8.4.4. Rest of ME&A

8.4.4.1. Rest of ME&A Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

8.4.4.2. Rest of ME&A Software Defined Vehicle Market Size and Forecast, By Software Layer Model (2026-2034)

8.4.4.3. Rest of ME&A Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

9. South America Software Defined Vehicle Market Size and Forecast by Segmentation by Segmentation (by Value USD Bn.) (2026-2034)

9.1. South America Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

9.2. South America Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

9.3. South America Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

9.4. South America Software Defined Vehicle Market Size and Forecast, by Country (2026-2034)

9.4.1. Brazil

9.4.1.1. Brazil Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

9.4.1.2. Brazil Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

9.4.1.3. Brazil Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

9.4.2. Argentina

9.4.2.1. Argentina Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

9.4.2.2. Argentina Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

9.4.2.3. Argentina Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

9.4.3. Rest Of South America

9.4.3.1. Rest Of South America Software Defined Vehicle Market Size and Forecast, By Vehicle Type (2026-2034)

9.4.3.2. Rest Of South America Software Defined Vehicle Market Size and Forecast, By Software Layer (2026-2034)

9.4.3.3. Rest Of South America Software Defined Vehicle Market Size and Forecast, By Deployment Model (2026-2034)

10. Company Profile: Key Players

10.1. Tesla (USA)

10.1.1.1. Company Overview

10.1.1.2. Business Portfolio

10.1.1.3. Financial Overview

10.1.1.4. SWOT Analysis

10.1.1.5. Strategic Analysis

10.1.1.6. Recent Developments

10.2. NVIDIA (USA)

10.3. Google (USA)

10.4. Qualcomm (USA)

10.5. GM (USA)

10.6. Ford (USA)

10.7. Apple (USA)

10.8. Amazon AWS (USA)

10.9. Waymo (USA)

10.10. Mobileye (USA)

10.11. BlackBerry QNX (Canada)

10.12. Magna International (Canada)

10.13. Mercedes-Benz (Germany)

10.14. Volkswagen Group (Germany)

10.15. BMW (Germany)

10.16. Bosch (Germany)

10.17. Stellantis (Netherlands)

10.18. Volvo Cars (Sweden)

10.19. Continental (Germany)

10.20. Ericsson (Sweden)

10.21. Huawei (China)

10.22. BYD (China)

10.23. Toyota (Japan)

10.24. Hyundai Motor Group (South Korea)

10.25. Baidu (China)

10.26. Xiaomi (China)

10.27. Sony Honda Mobility (Japan)

10.28. Tata Motors (India)

10.29. CEER (Saudi Arabia)

10.30. BYD Brasil (Brazil)

11. Key Findings & Analyst Recommendations

12. Software Defined Vehicle Market: Research Methodology