US Aerospace Robots Market: AI-Enabled Aerospace Robots, Collaborative Aerospace Robots, Space Robotics Technologies Outlook (2026–2032)

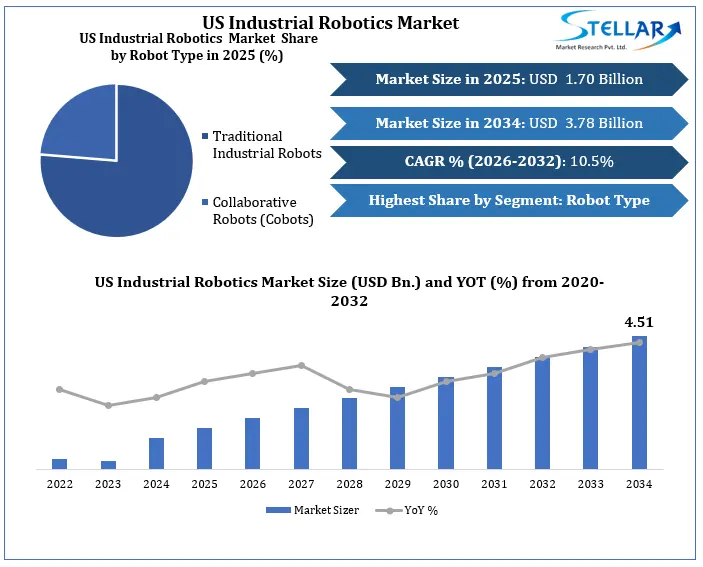

The US Aerospace Robots Market was projected to grow from USD 1.70 billion in 2025 to USD 3.78 billion by 2034 at 10.5% CAGR, supported by the growing use of robotic automation in aircraft manufacturing, aerospace assembly, inspection, and precision production to improve efficiency, product quality, and manufacturing accuracy.

US Aerospace Robots Market Overview

An aerospace robot is designed to operate in an aerospace manufacturing environment. These robots are highly specialised to handle delicate components and materials used in building aircraft and spacecraft. Aerospace robots in the US are typically articulated arms with multiple joints that have a high degree of skill and precision.

Boeing, Textron Aviation, Gulfstream Aerospace, Lockheed Martin, RTX and Northrop Grumman, these big giants of companies are constantly looking for advanced technologies that improve their product & service efficiency. Therefore, they are investing a massive amount of capital in the development of their product portfolios.

For instance, on March 2025, GE Aerospace announced an additional $1 billion investment across its US operations to expand commercial and defense aerospace production. The investment will support manufacturing upgrades in 17 states and is expected to strengthen the company’s production capacity and advanced aerospace manufacturing capabilities. In addition, on June 2026, Misumi Group launched Misumi Americas and announced a $1 billion global investment program to expand digital manufacturing and supply chain capabilities.

Robotic applications are found widely used in aerospace industries for performing tasks such as welding, drilling, riveting, assembling, coating, sealing and bonding, cutting, inspection, material handling, tending CNC machines, and transporting components. With the aid of robots, manufacturers can efficiently execute complicated tasks with improved accuracy while reducing production lead time, personnel needs, and other risks involved in the process.

To get more Insights: Request Free Sample Report

US Aerospace Robots Market Definition

The Aerospace Robots Market encompasses robotic equipment, automation tools, software, sensors, controls, and other associated services that have been built specifically for use in aerospace manufacturing, maintenance, testing, and space activities. This market comprises industrial robots, collaborative robots, autonomous robotics, and automated solutions specifically suited for use in the aerospace industry.

This market involves the design, development, integration, implementation, and maintenance of robotic technologies utilised by aerospace equipment manufacturers, aerospace parts suppliers, aerospace companies, aircraft maintenance providers, and other space agencies. It involves both earth-based robotic applications for aerospace, as well as advanced robotics for satellite operation, orbiting, and space flights.

US Aerospace Robots Market Driver

Increasing Investment in Domestic Aerospace Manufacturing Facilities

Increasing capital spending on aerospace manufacturing plants in the US is leading to the superior use of robotic technology. Aerospace component makers, plane manufacturers, and aerospace engine manufacturers have been boosting their production capabilities through new plants, plant renovations, and other initiatives to satisfy increasing demand from the commercial and military aerospace industry.

Firms such as GE Aerospace, Boeing, and Lockheed Martin are continually investing in cutting-edge manufacturing facilities across the nation. The increasing focus on boosting production capabilities, making supply chains more resilient, and creating more space for manufacturing aerospace technology in the country is resulting in widespread use of robots within the sector.

For instance, On April 2026, Boeing announced a CAD 36 million investment in aerospace manufacturing R&D at its Winnipeg facility, focusing on process automation and collaborative robotics to advance composite manufacturing capabilities and improve production efficiency.

Robotics technology enables manufacturers to enhance consistency and efficiency in their manufacturing processes by adhering to strict aerospace quality standards. Automation technologies are now being adopted in areas such as precision machining, components production, automated production lines, and quality assurance procedures, which allow manufacturers to boost productivity without compromising on accuracy and dependability.

Expanding Defence and Military Modernisation Programs

Increasing investments in military planes, helicopters, UAVs, and future defence systems have spurred demand for robotics in the aerospace industry in the United States. Manufacturing defence products requires great precision, the use of special materials, and controlled conditions; hence, automation of some parts of the process is crucial.

The use of robotics is becoming more common among defence contractors in America to manufacture components through techniques such as precise welding, inspection, surface finishing, and high-end assembly processes for aerospace products. Robotics enables manufacturers to adhere to strict defence standards in an efficient manner.

Increasing levels of modernisation efforts, along with the growing number of purchases of cutting-edge aerospace systems, are driving the uptake of robotics technology within the US aerospace manufacturing industry. The constant need to ensure the maintenance of quality in production, along with defence-related requirements, continues to push automation efforts forward.

US Aerospace Robots Market Opportunities

Expansion of Aircraft Maintenance, Repair, and Overhaul (MRO) Automation

The increasing need to enhance the efficiency of aircraft maintenance is leading to a rising use of robots by all the MRO establishments in the United States of America. This has involved their usage in surface preparation, stripping, non-destructive testing, and even inspections. The increase in commercial aircraft fleet and, hence, the maintenance needs is fuelling the increased usage of robotics in MRO activities. Robotic inspection systems are expected to help in enhancing accuracy in defect detection while reducing the reliance on human inspection systems.

Growth of Commercial Space and Satellite Manufacturing Programs

Growing investment in the production of satellites, launch vehicles, and commercial space missions is resulting in the increased use of robotics in the American space industry. Robotic technology aids precision assembly, component manipulation, testing, and manufacturing of complicated space hardware that demands a high degree of accuracy and dependability. The growing number of space enterprises in the private sector and government-sponsored space projects is fuelling the demand for superior aerospace robotics technology. The growing manufacture of small satellites and futuristic space hardware is boosting the demand for automation processes within the space industry.

US Aerospace Robots Market Trends

Growing Adoption of AI-Enabled Aerospace Robotics

Aerospace companies in the US are using AI, machine vision, and analytics in robots in their production lines to increase accuracy, perform quality checks automatically, and optimise their manufacturing processes. The employment of AI in robots contributes to enhancing precision and automation within manufacturing plants for both aeroplanes and space vehicles. Predictive maintenance and optimisation of manufacturing processes are other benefits associated with the employment of AI. The development of smart factories and digital manufacturing is also contributing to the adoption of AI-based robots.

Rising Deployment of Collaborative and Autonomous Robots

Increasing application of collaborative and autonomous robotic systems in US aerospace manufacturing and maintenance operations. Collaborative robots help in improving efficiency, ensuring safety at workplaces, and providing flexibility to manufacturers by performing assembly, drilling, fastening, inspecting, and material handling activities alongside technicians. Moreover, the use of autonomous robotic systems is increasing in aircraft inspection and maintenance procedures to minimise the efforts and time taken for the inspection process. Increased interest in flexible automation systems leads to wider usage of collaborative and autonomous robotics in aerospace manufacturing companies.

US Aerospace Robots Market Segmentation (2025)

US Aerospace Robots Market by Robot Type

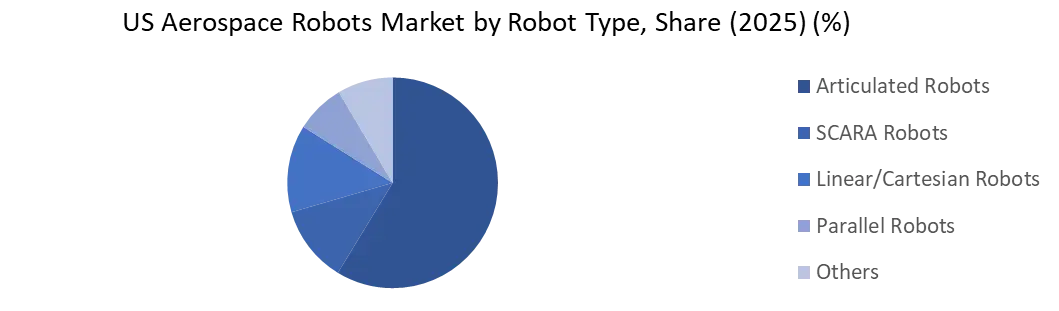

Articulated robots have the highest market share of 58.7% because of their versatility as well as usage in drilling, fastening, assembly, inspection, and material handling processes. The SCARA robots represent the fastest-growing category, due to increasing demand from high-speed and precise assembly processes. The linear/cartesian robots continue to grow at a steady pace due to their accuracy and repeatability, whereas parallel robots are growing fast due to their usage in lightweight components handling and specialised assembly processes.

US Aerospace Robots Market by Application

Drilling & Fastening holds the largest market share, accounting for 24.6% of the total share, owing to its importance in the construction process of aircraft and aerospace structures, where precision and consistency are key. Assembly is currently the fastest-growing segment due to the increased adoption of automation systems in the assembly of aerospace products. The material handling segment is experiencing a constant surge in market size due to the rising demand for efficient material and component movement within production plants. Non-Destructive Testing & Inspection is one of the segments with fast-growing revenue since the major players are increasingly concentrating on quality management and compliance. Surface Treatment, Sealing & Dispensing is registering consistent growth on account of the growing adoption of automated surface treatment processes. The other segment represents niche robotic applications across the aerospace industry.

US Aerospace Robots Market by Technology

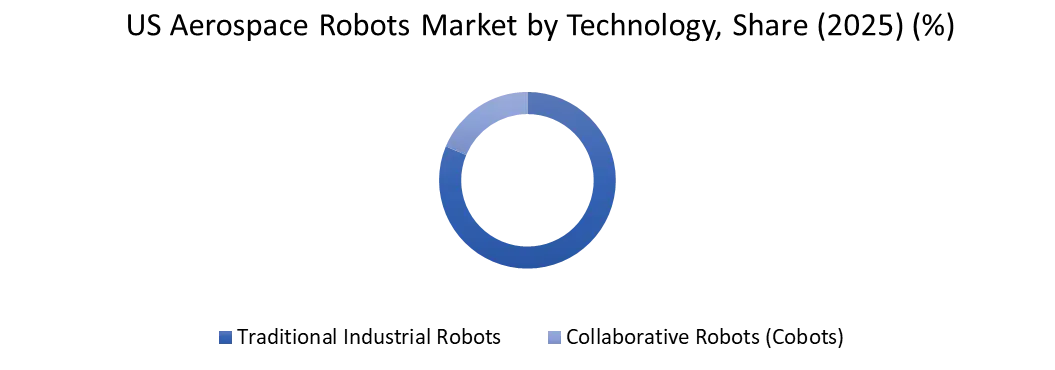

The Traditional Industrial Robots have the highest market share, accounting for 76.3%, due to the wide range of uses in various aerospace manufacturing processes like drilling, fastening, assembly, welding, and materials handling. Cobots are experiencing the fastest growth because of their collaborative nature in which they operate alongside human workers and increase efficiency inassembly, inspection, and maintenance operations.

US Aerospace Robots Market by Payload Capacity

The 16 – 60 kg category comprises 22.4% of the market share because of the versatile use of such machines in the aerospace industry for tasks like assembly, fastening, inspection, and material handling. Robots capable of handling loads up to 16 kg are the fastest-growing segment due to rising demand for small component operations in the aerospace industry. Meanwhile, the 61 – 225 kg category is experiencing consistent growth due to its usage in handling large aerospace assemblies. Lastly, the >225 kg category remains consistent in terms of its growth rate because of its usage in heavy-duty aerospace assemblies.

US Aerospace Robots Market by End-User

Commercial Aviation holds the biggest market share of 41% as a result of extensive robotics automation involved in the production, manufacturing, inspection, and assembly of aircraft. The fastest growing sector in the industry is Space & Satellite because of increased investment in satellites and space technology applications. Aerospace Component Manufacturing experiences growth owing to the demand for engineered aerospace components. Defence & Military Aerospace is steadily growing owing to investments made in military aircraft and defence technology. MRO grows moderately owing to the application of robotic technologies by aerospace firms to enhance aircraft maintenance services.

US Aerospace Robots Competitive Landscape 2025

The US Aerospace Robots Market is distinct by the presence of leading aerospace robotics suppliers, industrial robots manufacturers, and defence technology innovators who compete for market share through the provision of aerospace manufacturing, inspection, maintenance, and space industry services. Leading firms like Rockwell Automation, Teradyne’s Robotics Group, NVIDIA, Boston Dynamics, and Honeywell International are deploying cutting-edge robots, artificial intelligence (AI), machine vision, and automation technologies to boost manufacturing precision, efficiency, and productivity.

Competition is spurred by rising demand for automatic assembly, robotic drilling, robotic fastening, autonomous inspection, digital twins, and manufacturing enabled by AI. Companies in this market continue to develop intelligent robots, collaborative robots, vision systems, and predictive maintenance tools to increase their competitive edge in the commercial aviation, defence aerospace, and space manufacturing sectors. Strategic alliances with aerospace manufacturing firms and ongoing advancements in automation technologies are important factors that influence competition in this market.

US Aerospace Robots Market Recent Developments:

On July 2024, FANUC Corporation strengthened aerospace manufacturing automation through its collaboration with Airbus, deploying the M-800iA/60 six-axis robot in automated aircraft drilling operations. The solution improved drilling accuracy, increased productivity, and supported higher aircraft production rates to help address growing industry order backlogs.

On March 2026, FANUC plans to invest $90 million to build a new 840,000-square-foot plant in Pontiac, Michigan, expanding its U.S. production to meet booming demand for onshoring and automation by automakers and aerospace customers. Expected to create 225 jobs and be completed by 2027. FANUC has 400,000 robots installed worldwide and is the world's largest industrial robot manufacturer.

On October 2025, SoftBank Group agreed to acquire ABB's robotics business for $5.4 billion, marking a major step in its strategy to combine artificial intelligence with advanced robotics. The acquisition will add ABB's industrial robotics operations, which generated $2.3 billion in annual sales, to SoftBank's growing AI and automation portfolio. The deal highlights increasing global investment in intelligent robotics and automation technologies across manufacturing and industrial sectors.

US Aerospace Robots Regional Analysis

The US Aerospace Robots Market is highly dominated by the South US region, owing to the presence of aircraft manufacturing units, defence contractors, and space industry operations. States like Texas, Florida, and Alabama account for the demand generated by robotic systems in assembling, welding, drilling, inspecting, and material handling. The West US holds a higher growth rate owing to increasing investments in the development of aerospace manufacturing technologies and space-related products.

The Midwest US is experiencing stable growth as a result of its existing aerospace component manufacturing, along with industrial automation operations, whereas the Northeast US is growing because of investments made in aircraft engine manufacturing, defence aerospace, and innovative aerospace. Growth in the use of robotics for automated manufacturing and inspection processes is fueling the development in these markets.

|

Aerospace Robots Market |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2034 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 1.70 Bn. |

|

Forecast Period 2026 to 2034 CAGR: |

10.5% |

Market Size in 2034: |

USD 3.78 Bn. |

|

Segments

|

By Robot Type |

Articulated Robots SCARA Robots Linear/Cartesian Robots Parallel Robots Others |

|

|

By Application

|

Drilling & Fastening Assembly Welding & Soldering Non-Destructive Testing & Inspection Material Handling Surface Treatment, Sealing & Dispensing Others |

||

|

By Technology |

Traditional Industrial Robots Collaborative Robots (Cobots) |

||

|

By Payload Capacity |

Up to 16 kg 16–60 kg 61–225 kg Above 225 kg |

||

|

|

By End User |

Commercial Aviation Defense & Military Aerospace Space & Satellite Maintenance, Repair & Overhaul (MRO) Aerospace Components Manufacturing |

|

Key Players Profiles Covered in the Report

- Boston Dynamics

- ABB

- KUKA

- Fanuc

- Yaskawa Electric

- Rockwell Automation

- NVIDIA

- Universal Robots

- The Boeing Company

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- RTX Corporation

- L3Harris Technologies, Inc.

- Honeywell International Inc.

- Electroimpact, Inc.

Frequently Asked Questions

Aerospace robots are widely used for drilling and fastening, assembly, welding, inspection, material handling, surface treatment, sealing, and automated quality control processes in aircraft and spacecraft manufacturing.

Commercial aviation, defence and military aerospace, space and satellite programs, aerospace component manufacturing, and maintenance, repair, and overhaul (MRO) facilities are the major end users of aerospace robots.

Collaborative robots are enabling safer human-robot interaction and improving production flexibility by assisting workers with precision assembly, inspection, and maintenance tasks in aerospace facilities.

The Southern United States holds a leading position due to its concentration of aerospace manufacturing facilities, defence contractors, aircraft assembly plants, and growing investments in aerospace production and automation technologies.

1. US Industrial Robotics Market: Introduction

2. US Industrial Robotics Market: Executive Summary

2.1. US Industrial Robotics Market Size And Forecast (USD Billion)

2.2 Market Definition

2.3 Market Segmentation

2.4 Research Timelines

2.5 Assumptions

2.6 Limitation

3. US Industrial Robotics Market: Research Methodology

3.1 Data Mining

3.2 Secondary Research

3.3 Primary Research

3.4 Subject Matter Expert Advice

3.5 Quality Check

3.6 Final Review

3.7 Data Triangulation

3.8 Top-Down Approach

3.9 Bottom-Up Approach

3.10 Research Flow

3.11 Data Sources

4. US Industrial Robotics Market: Market Attractiveness Mapping

4. 1 US Industrial Robotics Market Overview

4.2 Competitive Analysis: Funnel Diagram (Tier 1, Tier 2, Tier 3)

4.3 US Industrial Robotics Market Absolute Market Opportunity

4.4 US Industrial Robotics Market Attractiveness Analysis, By Region

4.5 US Industrial Robotics Market Attractiveness Analysis, By Robot Type

4.6 US Industrial Robotics Market Attractiveness Analysis, By Application

4.7 US Industrial Robotics Market Attractiveness Analysis, By Payload Capacity

4.8 US Industrial Robotics Market Attractiveness Analysis, By Industry

4.9 Future Market Opportunities

5. US Industrial Robotics Market: Market Outlook

5.1 US Industrial Robotics Market Evolution

5.2 Industrial Robotics Adoption Analysis

5.3 Market Trends

5.4 Market Dynamics

5.4.1 Market Drivers

5.4.2 Market Restraints

5.4.3 Market Trends

5.4.4 Market Opportunity

5.5 Porter’s Five Forces Analysis

5.5.1 Threat Of New Entrants

5.5.2 Bargaining Power Of Suppliers

5.5.3 Bargaining Power Of Buyers

5.5.4 Threat Of Substitute Products

5.5.5 Competitive Rivalry Of Existing Competitors

5.6 PESTEL Analysis

5.7 Value Chain Analysis

5.8 Industrial Robotics Infrastructure Development Analysis

5.9 Pricing Analysis

5.10 Geopolitical Impact Assessment

5.11 Regulatory Framework and Policy Impact Assessment

5.12 Technology Landscape

6. US Industrial Robotics Market: By Robot Type, 2026-2032 (USD Billion)

6.1 Articulated

6.2 SCARA

6.3 Cylindrical

6.4 Cartesian/Linear

6.5 Parallel

6.6 Others

7. US Industrial Robotics Market: By Application, 2026-2032 (USD Billion)

7.1 Pick and Place

7.2 Welding & Soldering

7.3 Material Handling

7.4 Assembling

7.5 Cutting & Processing

7.6 Others

8. US Industrial Robotics Market: By Payload Capacity, 2026-2032 (USD Billion)

8.1 Up to 16 KG

8.2 16 to 20 KG

8.3 61 to 225 KG

8.4 Above 225 KG

9. US Industrial Robotics Market: By Industry, 2026-2032 (USD Billion)

9.1 Automotive

9.2 Healthcare & Pharmaceutical

9.3 Food & Beverages

9.4 Metals & Machinery

9.5 Others

10. US Industrial Robotics Competitive Matrix

11. US Industrial Robotics Market: Company Benchmarking

12. Merger & Acquisition

13. US Industrial Robotics Market: Company Profiles

1. Boston Dynamics

2. ABB

3. KUKA

4. Fanuc

5. Yaskawa Electric

6. Rockwell Automation

7. NVIDIA

8. Universal Robots

9. The Boeing Company

10. Lockheed Martin Corporation

11. Northrop Grumman Corporation

12. RTX Corporation

13. L3Harris Technologies, Inc.

14. Honeywell International Inc.

15. Electroimpact, Inc.

14. Risk Assessment and Scenario Analysis

15. Strategic Opportunity

16. Investments & Funding Analysis

17. Strategic Roadmap

18. Analyst Recommendations