Aerospace Robots Market: AI-Enabled Aerospace Robots, Collaborative Aerospace Robots, Space Robotics Technologies Outlook (2026–2034)

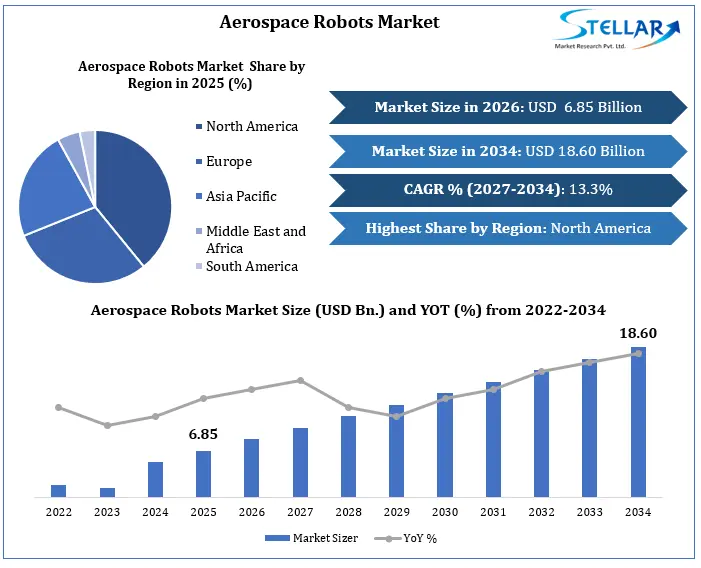

The Aerospace Robots Market was projected to grow from USD 6.85 billion in 2025 to USD 18.60 billion by 2034 at 13.3% CAGR, supported by the growing use of robotic automation in aircraft manufacturing, aerospace assembly, inspection, and precision production to improve efficiency, product quality, and manufacturing accuracy.

Aerospace Robots Market Overview

An aerospace robot is a robot designed to operate in an aerospace manufacturing environment. These robots are highly specialised to handle delicate components and materials used in building aircraft and spacecraft. Aerospace robots are typically articulated arms with multiple joints that have a high degree of skill and precision.

The increasing adoption of robotic automation by aircraft makers, spacecraft manufacturers, and aerospace components suppliers is driven by improved accuracy, efficiency, and quality during manufacturing processes. Robotic applications are found widely used in aerospace industries for performing tasks such as welding, drilling, riveting, assembling, coating, sealing and bonding, cutting, inspection, material handling, tending CNC machines, and transporting components. With the aid of robots, manufacturers can efficiently execute complicated tasks with improved accuracy while reducing production lead time, personnel needs, and other risks involved in the process.

To get more Insights: Request Free Sample Report

Global Aerospace Robots Market Definition

The Aerospace Robots Market encompasses robotic equipment, automation tools, software, sensors, controls, and other associated services that have been built specifically for use in aerospace manufacturing, maintenance, testing, and space activities. This market comprises industrial robots, collaborative robots, autonomous robotics, and automated solutions specifically suited for use in the aerospace industry.

This market involves the design, development, integration, implementation, and maintenance of robotic technologies utilised by aerospace equipment manufacturers, aerospace parts suppliers, aerospace companies, aircraft maintenance providers, and other space agencies. It involves both earth-based robotic applications for aerospace, as well as advanced robotics for satellite operation, orbiting, and space flights.

Global Aerospace Robots Market Driver

Rising Adoption of Automation for Complex Aerospace Assembly Operations

The growing complexity associated with the production of aircraft, spaceships, and parts of aerospace vehicles is fuelling the trend toward using robotics in production centres. The aerospace industry needs high precision in operations like drilling, fastening, riveting, composites laying up, and assembly, as any errors may impact the final product quality and safety. The use of robotics in aerospace contributes to increased precision, reduced assembly time, and the maintenance of quality standards in manufacturing advanced aerospace vehicles.

Robotic applications in aerospace manufacturing can be witnessed in the form of robots developed by companies such as Electroimpact, Inc., Broetje-Automation GmbH, and KUKA AG that cater to the requirements of aircraft assembly and aerospace manufacturing.

Aircraft backlog, increased production rates, and the necessity for efficient manufacturing processes will continue to increase the pace of robot adoption in the aerospace industry. Moreover, the implementation of automation technology is aimed at achieving scalable production processes while retaining the necessary precision required in aerospace manufacturing processes.

Expanding Defence and Space Program Investments

An increase in funding toward defence modernisation initiatives, military aircraft assembly lines, satellite placement, and space exploration is leading to an increased need for aerospace robots. The aerospace industry is adopting robotic technology to aid in producing sophisticated defence vehicles, space structures, launch vehicles, and satellites. Such robotic technology helps in increasing accuracy in production and minimising the variations during manufacture that are essential for aerospace and defence applications.

Firms such as Northrop Grumman Corporation, MDA Space Ltd., and Maxar Technologies Inc. are working to advance robot technology employed within the aerospace and space manufacturing industries. Their technologies assist with precise manufacturing processes, complex assembly operations, and increasingly stringent needs for government and commercial aerospace initiatives.

The rise in government spending on defensive capabilities, increase in satellite launch activities, and growth in investments in space-related operations by nations are driving the demand for aerospace robotics. With advancements in technology and increases in size in aerospace ventures, robotics is playing a critical part in production efficiencies and quality.

Global Aerospace Robots Market Opportunities

Expansion of Aerospace Manufacturing Facilities in Emerging Markets

The rising investments in aerospace plants in countries such as India, China, Mexico, and the UAE are resulting in the extensive use of robotic automation in the production process of assembling aircraft and their parts. Factories are ramping up production to fulfil the growing demand by consumers for aircraft and aerospace products without compromising on the level of accuracy and precision in their operations. Robots are being utilized in drilling, fastening, assembling, material handling, and inspecting during the production process. The development of aerospace manufacturing centres in developing nations drives the demand for robots in aerospace engineering.

Increasing Automation of Aircraft Maintenance, Repair, and Overhaul (MRO) Operations

Aircraft maintenance providers are increasingly adopting robotic technologies to improve maintenance efficiency, reduce aircraft downtime, and support higher service volumes. Robotic systems are being utilized for inspection, painting, surface preparation, coating removal, and other repetitive maintenance activities that require accuracy and consistency. These technologies help improve worker safety, reduce labor-intensive processes, and maintain service quality across maintenance facilities. As global aircraft fleets continue to expand and aging aircraft require more frequent maintenance, robotic automation is gaining greater importance within MRO operations.

Global Aerospace Robots Market Trends

Rising Use of AI-Based Robotic Inspection and Precision Automation

AI-powered robotic machines featuring machine vision and sophisticated sensors, along with inspection capabilities, are being embraced by aerospace manufacturers for improving precision and quality management within manufacturing operations. These robots are commonly employed for operations including drilling, fastening, composite inspection, surface scanning, and defect identification. This technology assists in monitoring quality levels, predicting potential maintenance needs, and detecting any manufacturing defects instantly. With the increase in the complexity of aircraft structures and quality standards, intelligent robotic systems are becoming more common in aerospace manufacturing units.

Growing Adoption of Space Robotics for In-Orbit Servicing and Assembly

Space robotics is witnessing a growing interest among space organisations due to their increasing investment in robotic technology, which can be used for satellite maintenance, assembly, and manufacturing in orbit. The use of robotics is increasing as this technology can perform complex tasks in outer space, including inspection, repair, refuelling, and even assembly, reducing the dependence of space agencies on costly manned missions to accomplish these activities. This will allow space organisations to increase the lifespan of satellites and carry out missions more efficiently while planning long-term space exploratory projects.

Global Aerospace Robots Market Segmentation (2025)

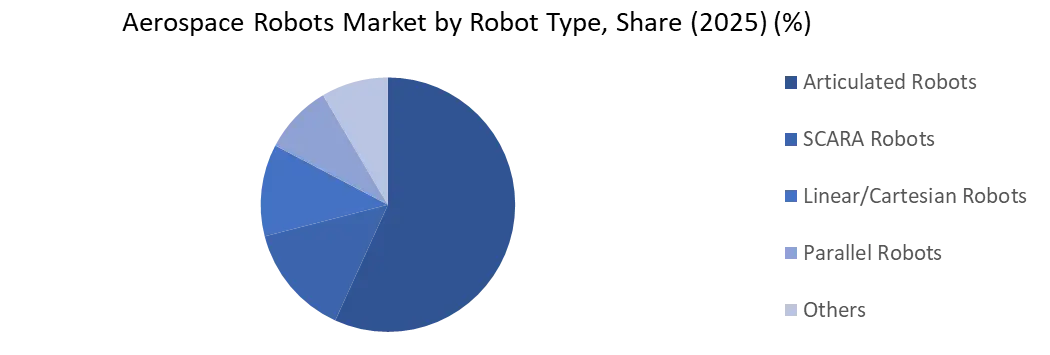

Global Aerospace Robots Market by Robot Type

Articulated robots have the highest market share of 56.8% because of their versatility as well as usage in drilling, fastening, assembly, inspection, and material handling processes. The SCARA robots represent the fastest-growing category, due to increasing demand from high-speed and precise assembly processes. The linear/cartesian robots continue to grow at a steady pace due to their accuracy and repeatability, whereas parallel robots are growing fast due to their usage in lightweight components handling and specialised assembly processes.

Global Aerospace Robots Market by Application

Drilling & Fastening holds the largest market share, accounting for 24.6% of the total share, owing to its importance in the construction process of aircraft and aerospace structures, where precision and consistency are key. Assembly is currently the fastest-growing segment due to the increased adoption of automation systems in the assembly of aerospace products. The material handling segment is experiencing a constant surge in market size due to the rising demand for efficient material and component movement within production plants. Non-Destructive Testing & Inspection is one of the segments with fast-growing revenue since the major players are increasingly concentrating on quality management and compliance. Surface Treatment, Sealing & Dispensing is registering consistent growth on account of the growing adoption of automated surface treatment processes. The other segment represents niche robotic applications across the aerospace industry.

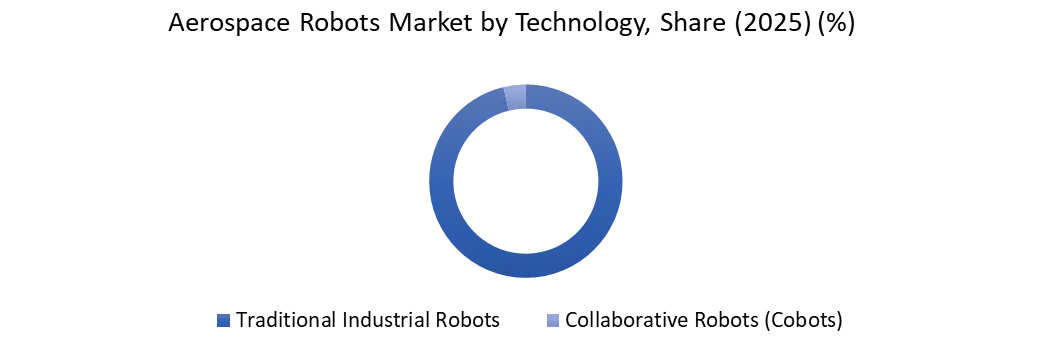

Global Aerospace Robots Market by Technology

The Traditional Industrial Robots have the highest market share, accounting for 82.4%, due to the wide range of uses in various aerospace manufacturing processes like drilling, fastening, assembly, welding, and materials handling. Cobots are experiencing the fastest growth because of their collaborative nature in which they operate alongside human workers and increase efficiency inassembly, inspection, and maintenance operations.

Global Aerospace Robots Market by Payload Capacity

The 16 – 60 kg category comprises 34.8% of the market share because of the versatile use of such machines in the aerospace industry for tasks like assembly, fastening, inspection, and material handling. Robots capable of handling loads up to 16 kg are the fastest-growing segment due to rising demand for small component operations in the aerospace industry. Meanwhile, the 61 – 225 kg category is experiencing consistent growth due to its usage in handling large aerospace assemblies. Lastly, the >225 kg category remains consistent in terms of its growth rate because of its usage in heavy-duty aerospace assemblies.

Global Aerospace Robots Market by End-User

Commercial Aviation holds the biggest market share of 41.2% as a result of extensive robotics automation involved in the production, manufacturing, inspection, and assembly of aircraft. The fastest growing sector in the industry is Space & Satellite because of increased investment in satellites and space technology applications. Aerospace Component Manufacturing experiences growth owing to the demand for engineered aerospace components. Defence & Military Aerospace is steadily growing owing to investments made in military aircraft and defence technology. MRO grows moderately owing to the application of robotic technologies by aerospace firms to enhance aircraft maintenance services.

Global Aerospace Robots Competitive Landscape 2025

The key feature of the Aerospace Robots market is the involvement of industrial robotic companies across the globe, specialist aerospace automation firms, and space robotics firms competing against each other based on technical expertise, automation, precision, and application-based solutions. Some prominent players in the market include ABB Ltd., KUKA AG, FANUC Corporation, Yaskawa Electric Corporation, and Stäubli International AG, which offer robotic solutions in areas of aircraft assembly, drilling, fastening, welding, and inspection, among others.

In addition, there is an increase in the participation of companies specialized in aerospace robotics technology, including Electroimpact, Inc., Broetje-Automation GmbH, MDA Space Ltd., Maxar Technologies Inc., and Honeybee Robotics. Companies are developing AI-powered robots, machine vision, autonomous robots, digital twin technology, and satellite servicing robots in order to maintain their competitive edge in the market. Strategic collaborations with aircraft makers, defence entities, and space agencies still play a significant role in the competitiveness of the aerospace robotics market.

Global Aerospace Robots Market Recent Developments:

On April 2024, MDA Space was awarded a $250 million contract extension from the Canadian Space Agency (CSA) to continue supporting robotics operations on the International Space Station (ISS) from 2025 to 2030. As part of the contract, MDA Space fulfils robotics flight controller duties to support mission operations on the ISS.

On April 2025, ABB Ltd. announced plans to spin off and list its robotics unit in Q2 as a separate publicly traded company. The robotics business, which makes industrial robots and related software, is valued at approximately USD 5.375 billion. The business will start trading in the second quarter of 2026, with likely listing venues in Switzerland and Sweden.

On May 2024, Mitsubishi Electric Corporation led a Series B investment in Realtime Robotics, Inc., a Massachusetts-based startup pioneering motion-planning technology for factory automation equipment. The investment supports collision-free autonomous motion planning applicable to aerospace manufacturing. Mitsubishi has 70,000 robots installed worldwide.

On April 2024, MDA Space was awarded a $250 million contract extension from the Canadian Space Agency (CSA) to continue supporting robotics operations on the International Space Station (ISS). As part of the contract, MDA Space fulfils robotics flight controller duties to support mission operations on the ISS.

Global Aerospace Robots Regional Analysis

North America is leading the Aerospace Robots Market because of its well-developed aerospace industry, powerful military industry, and space exploration activities. The increasing presence of major aerospace companies such as Boeing, Lockheed Martin Corporation, and Northrop Grumman Corporation, which are making use of robotic systems for the production of aircraft through the process of drilling, fastening, welding, painting, and inspecting the aircraft. Another large market is represented by Europe, owing to its high-level manufacturing of aerospace products and the existence of Airbus SE, in addition to other aerospace companies.

There is considerable growth in South America, especially as Brazil’s contribution to the aerospace industry as far as manufacturing and MRO activities are concerned. Investments in manufacturing aircraft and components have led to greater adoption of robotic automation in order to increase productivity and enhance product quality. The Middle East & Africa can be considered as an innovative market for this technology, owing to investments made by several countries, such as the UAE and Saudi Arabia, in the aviation, defence, and space sectors.

|

Aerospace Robots Market |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2034 |

|

Historical Data: |

2022 to 2025 |

Market Size in 2025: |

USD 6.85 Bn. |

|

Forecast Period 2026 to 2034 CAGR: |

13.3% |

Market Size in 2034: |

USD 18.60 Bn. |

|

Segments

|

By Robot Type |

Articulated Robots SCARA Robots Linear/Cartesian Robots Parallel Robots Others |

|

|

By Application

|

Drilling & Fastening Assembly Welding & Soldering Non-Destructive Testing & Inspection Material Handling Surface Treatment, Sealing & Dispensing Others |

||

|

By Technology |

Traditional Industrial Robots Collaborative Robots (Cobots) |

||

|

By Payload Capacity |

Up to 16 kg 16–60 kg 61–225 kg Above 225 kg |

||

|

|

By End User |

Commercial Aviation Defense & Military Aerospace Space & Satellite Maintenance, Repair & Overhaul (MRO) Aerospace Components Manufacturing |

|

Key Players Profiles Covered in the Report

- ABB Ltd.

- KUKA AG

- FANUC Corporation

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Kawasaki Heavy Industries, Ltd.

- Stäubli International AG

- Comau S.p.A.

- Electroimpact, Inc.

- Broetje-Automation GmbH

- Güdel Group AG

- MDA Space Ltd.

- Northrop Grumman Corporation

- Maxar Technologies Inc.

- Honeybee Robotics

- Astrobotic Technology, Inc.

- The Boeing Company

- Airbus SE

Frequently Asked Questions

Aerospace robots support satellite assembly, testing, servicing, and orbital operations. They are also increasingly used in space exploration missions for autonomous navigation, maintenance, sample collection, and remote operations in challenging environments.

Key automated activities include fuselage assembly, composite layup, drilling and riveting, welding, painting, surface treatment, quality inspection, and material handling of large aerospace components.

Collaborative robots are enabling safer human-robot interaction on production floors. They help manufacturers improve flexibility, support low-volume high-mix production, and assist workers with precision assembly and inspection tasks.

Artificial intelligence, machine vision, digital twins, autonomous mobile robots, advanced sensing systems, and robotic technologies for in-space manufacturing and satellite servicing are expected to drive the next phase of market growth.

1. Aerospace Robots Market: Introduction

2. Aerospace Robots Market: Executive Summary

2.1. Global Aerospace Robots Market Size and Forecast (USD Billion)

2.2 Market Definition

2.3 Market Segmentation

2.4 Research Timelines

2.5 Assumptions

2.6 Limitation

3. Aerospace Robots Market: Research Methodology

3.1 Data Mining

3.2 Secondary Research

3.3 Primary Research

3.4 Subject Matter Expert Advice

3.5 Quality Check

3.6 Final Review

3.7 Data Triangulation

3.8 Top-Down Approach

3.9 Bottom-Up Approach

3.10 Research Flow

3.11 Data Sources

4. Aerospace Robots Market: Market Attractiveness Mapping

4. 1 Global Aerospace Robots Market Overview

4.2 Competitive Analysis: Funnel Diagram (Tier 1, Tier 2, Tier 3)

4.3 Global Aerospace Robots Market Absolute Market Opportunity

4.4 Global Aerospace Robots Market Attractiveness Analysis, By Region

4.5 Global Aerospace Robots Market Attractiveness Analysis, By Robot Type

4.6 Global Aerospace Robots Market Attractiveness Analysis, By Application

4.7 Global Aerospace Robots Market Attractiveness Analysis, By Payload Capacity

4.8 Global Aerospace Robots Market Attractiveness Analysis, By Industry

4.9 Future Market Opportunities

5. Aerospace Robots Market: Market Outlook

5.1 Global Aerospace Robots Market Evolution

5.2 Aerospace Robots Adoption Analysis

5.3 Market Trends

5.4 Market Dynamics

5.4.1 Market Drivers

5.4.2 Market Restraints

5.4.3 Market Trends

5.4.4 Market Opportunity

5.5 Porter’s Five Forces Analysis

5.5.1 Threat Of New Entrants

5.5.2 Bargaining Power Of Suppliers

5.5.3 Bargaining Power Of Buyers

5.5.4 Threat Of Substitute Products

5.5.5 Competitive Rivalry Of Existing Competitors

5.6 PESTEL Analysis

5.7 Value Chain Analysis

5.8 Aerospace Robots Infrastructure Development Analysis

5.9 Pricing Analysis

5.10 Geopolitical Impact Assessment

5.11 Regulatory Framework and Policy Impact Assessment

5.12 Technology Landscape

6. Aerospace Robots Market: By Robot Type, 2026-2034 (USD Billion)

6.1 Articulated Robots

6.2 SCARA Robots

6.3 Linear/Cartesian Robots

6.4 Parallel Robots

6.5 Others

7. Aerospace Robots Market: By Application, 2026-2034 (USD Billion)

7.1 Drilling & Fastening

7.2 Assembly

7.3 Welding & Soldering

7.4 Non-Destructive Testing & Inspection

7.5 Material Handling

7.6 Surface Treatment, Sealing & Dispensing

7.7 Others

8. Aerospace Robots Market: By Technology 2026-2034 (USD Billion)

8.1 Traditional Industrial Robots

8.2 Collaborative Robots (Cobots)

9. Aerospace Robots Market: By Payload Capacity, 2026-2034 (USD Billion)

9.1 Up to 16 kg

9.2 16–60 kg

9.3 61–225 kg

9.4 Above 225 kg

10. Aerospace Robots Market: By End User, 2026-2034 (USD Billion)

10.1 Commercial Aviation

10.2 Defense & Military Aerospace

10.3 Space & Satellite

10.4 Maintenance, Repair & Overhaul (MRO)

10.5 Aerospace Components Manufacturing

11. Aerospace Robots Market: Geography, 2026-2034 (USD Billion)

11.1 North America Aerospace Robots Market

11.2 Europe Aerospace Robots Market

11.3 Asia Pacific Aerospace Robots Market

11.4 South America Aerospace Robots Market

11.5 Middle East And Africa Aerospace Robots Market

12. Aerospace Robots Competitive Matrix

13. Aerospace Robots Market: Company Benchmarking

14. Merger & Acquisition

15. Aerospace Robots Market: Company Profiles

19. ABB Ltd.

20. KUKA AG

21. FANUC Corporation

22. Yaskawa Electric Corporation

23. Mitsubishi Electric Corporation

24. Kawasaki Heavy Industries, Ltd.

25. Stäubli International AG

26. Comau S.p.A.

27. Electroimpact, Inc.

28. Broetje-Automation GmbH

29. Güdel Group AG

30. MDA Space Ltd.

31. Northrop Grumman Corporation

32. Maxar Technologies Inc.

33. Honeybee Robotics

34. Astrobotic Technology, Inc.

35. The Boeing Company

36. Airbus SE

16. Risk Assessment and Scenario Analysis

17. Strategic Opportunity

18. Investments & Funding Analysis

19. Strategic Roadmap

20. Analyst Recommendations