Underwater Warfare Systems Market Size, Share & Industry Analysis, 2026–2032

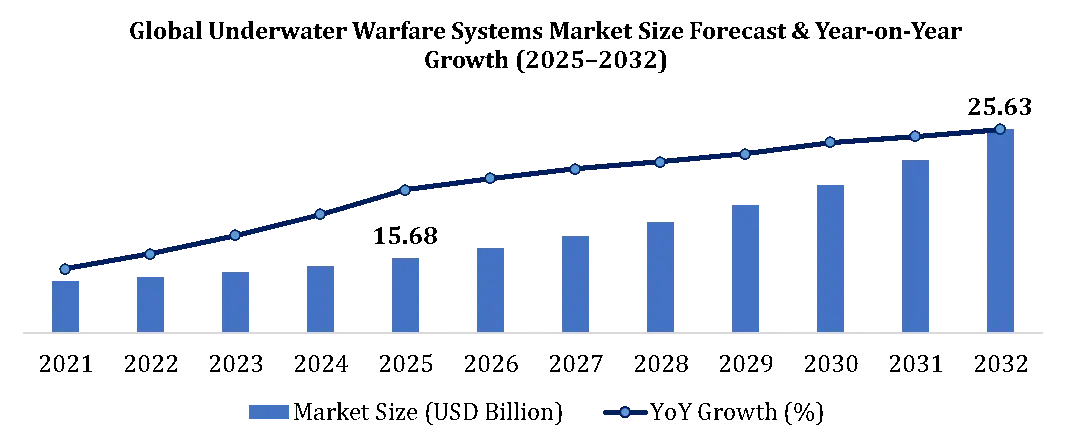

The Underwater Warfare Systems Market was valued at USD 15.68 Billion in 2025 and is projected to reach USD 25.63 Billion by 2032, registering a steady CAGR of 7.3% during the forecast period.

The market is emerging as one of the most strategically critical and budget-resilient segments within the broader defense and maritime security ecosystem, witnessing sustained expansion driven by AI-powered sonar systems, autonomous underwater vehicles (AUVs), anti-submarine warfare (ASW) technologies, unmanned underwater vehicles (UUVs), and real-time undersea domain awareness solutions. With increasing procurement across naval forces, coast guards, and defense ministries spanning North America, Europe, Asia Pacific, and the Middle East, the Underwater Warfare Systems Market Size is expected to experience significant growth between 2025 and 2032.

To get more Insights: Request Free Sample Report

The growth of the Underwater Warfare Systems Market is driven by rising geopolitical tensions across contested maritime zones, evolving naval modernization programs, and growing demand for autonomous undersea combat capabilities. Nations are rapidly shifting from legacy manned submarine fleets toward next-generation UUV platforms, AI-integrated sonar arrays, and network-centric undersea warfare architectures, enhancing operational effectiveness and compressing threat detection-to-engagement cycles.

Underwater Warfare Systems Market Key Highlights

|

Market Parameter |

Value / Insight |

Trend |

|

Global Market Size (2025) |

USD 15.68 Billion |

↑ Strong |

|

Forecast Market Size (2032) |

USD 25.63 Billion |

↑ Expanding |

|

CAGR (2026–2032) |

7.3% |

↑ Stable Growth |

|

Largest Region (2025) |

North America (38%) |

↑ Dominant |

|

Fastest Growing Region |

Asia Pacific |

↑ Strategic Expansion |

|

Leading Segment |

Sonar & Detection Systems |

↑ Core Technology |

|

Key Platform |

Submarines (SSN/SSBN/SSK) |

↑ Strategic Backbone |

|

Key Technology Driver |

AI + Multi-Sensor Fusion |

↑ Disruptive |

|

Operational Focus |

Anti-Submarine Warfare (ASW) |

↑ Rising Priority |

|

Naval Threat Incidents |

Increasing submarine activity globally |

↑ Escalating |

Underwater Warfare Systems Industry Ecosystem Map

The Underwater Warfare Systems ecosystem includes a highly integrated defense-industrial value chain spanning sonar technology developers, naval defense contractors, autonomous system manufacturers, and government defense agencies.

|

Layer |

Key Participants |

|

Sensor & Component Suppliers |

Sonar modules, hydrophones, acoustic sensors, pressure-resistant materials |

|

Technology Developers |

AI sonar analytics, UUV autonomy systems, signal processing platforms |

|

System Integrators |

Naval OEMs, defense primes, submarine manufacturers |

|

Platform Providers |

Submarines, destroyers, frigates, unmanned underwater vehicles |

|

Regulatory Bodies |

NATO, U.S. Navy, MoD (India, UK, France), maritime security agencies |

|

End Users |

Naval forces, defense ministries, coast guards |

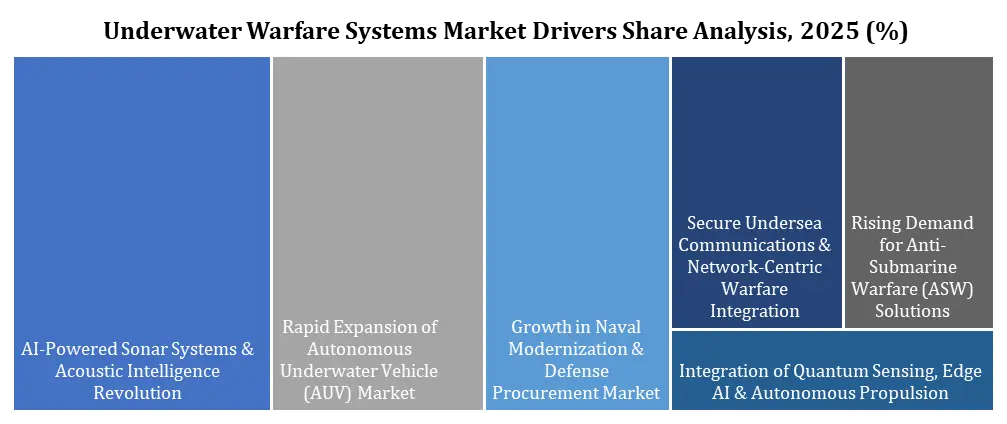

Key Market Drivers for the Underwater Warfare Systems Market

AI-Powered Sonar Systems & Acoustic Intelligence Revolution

The integration of AI-driven sonar analytics is transforming how naval forces detect, classify, and engage sub-surface threats. Advanced machine learning algorithms process multi-layered acoustic signatures, thermal layer data, and hydrophone array outputs to deliver real-time threat identification and predictive engagement recommendations.

AI enables:

- Automated submarine classification and real-time acoustic signature matching

- Predictive threat tracking across complex multi-target undersea environments

- False-alarm reduction and signal-to-noise optimization in contested littoral zones

This shift is significantly enhancing Underwater Warfare Systems Market Trends and Insights, positioning AI-integrated sonar as the primary technology growth catalyst across all naval tiers.

Rapid Expansion of Autonomous Underwater Vehicle (AUV) Market

The AUV and UUV Market is witnessing accelerated procurement due to its ability to deliver persistent, wide-area undersea surveillance without crewed platform risk. Compared to traditional submarine-based ISR missions, autonomous underwater systems reduce per-mission operational cost by 40–60%, making them the preferred solution for continuous maritime domain awareness operations.

Applications include:

- Anti-submarine warfare (ASW) patrol and threat cueing

- Underwater mine detection and neutralization

- Strategic chokepoint surveillance and undersea infrastructure protection

Growth in Naval Modernization & Defense Procurement Market

The Naval Modernization Market is expanding at an accelerating pace as sovereign defense budgets prioritize undersea warfare capability upgrades. Nations across NATO, Indo-Pacific, and the Middle East are leveraging underwater warfare systems for submarine fleet recapitalization, anti-access/area-denial (A2/AD) capability development, and joint undersea battlespace integration.

Secure Undersea Communications & Network-Centric Warfare Integration is gaining strategic priority as navies require real-time, low-latency data links between submerged platforms, surface combatants, and joint command centers.

Secure undersea communications enable:

- Real-time UUV swarm coordination and autonomous mission tasking

- Encrypted data transmission between submarine and surface warfare assets

- Multi-domain operational integration across air, surface, and subsurface forces

- Network-centric undersea battlespace management and threat fusion

This significantly accelerates the Underwater Warfare Systems Market Growth Rate across all platform categories.

Rising Demand for Anti-Submarine Warfare (ASW) Solutions

The Anti-Submarine Warfare Market is gaining decisive traction as adversarial submarine proliferation forces counter-investment across allied naval forces. Underwater warfare systems offer unmatched detection and engagement precision compared to surface-only maritime patrol operations.

Integration of Quantum Sensing, Edge AI, and Autonomous Propulsion the convergence of quantum acoustic detection, Edge AI onboard processing, and advanced lithium-ion and air-independent propulsion (AIP) systems is revolutionizing the Autonomous Undersea Systems Market. Real-time onboard threat assessment and autonomous engagement capability enable faster operational responses and reduced human-in-the-loop dependency.

Emerging Trends Shaping the Underwater Warfare Systems Industry

UUV-as-a-Capability (UaaC) & Modular Payload Architecture Expansion the shift toward modular, mission-reconfigurable UUV platforms is reducing per-capability acquisition costs for mid-tier navies. Defense forces can now access advanced undersea intelligence, surveillance, and strike capabilities through scalable, payload-swappable autonomous platforms without full submarine program investment.

AI and Machine Learning Integration in Undersea Warfare

- Automated acoustic threat classification and engagement recommendation

- Anomaly detection across underwater infrastructure and cable networks

- Real-time undersea battlespace dashboards for fleet command decision support

This is fast-tracking the evolution of the Undersea Warfare Technology Market at an unprecedented pace.

Digital Twin & Undersea Environment Modelling Technologies the integration of digital twin oceanographic models with real-time sensor data is transforming submarine tactical planning and UUV mission design by enabling accurate acoustic propagation prediction, thermal layer mapping, and adversary movement simulation before operational deployment.

Undersea Critical Infrastructure Protection Applications Underwater warfare systems are increasingly deployed for:

- Subsea cable and pipeline protection against sabotage and hostile surveillance

- Offshore energy asset defense and perimeter monitoring

- Seabed warfare and strategic domain denial operations

This supports evolving demand for Undersea Infrastructure Defense and Maritime Security Systems globally.

Technology Disruption & Defense Transformation Strategy

Defense transformation is at the core of the Underwater Warfare Systems Market Outlook. The convergence of:

- AI-powered sonar analytics and acoustic intelligence platforms

- Edge AI-enabled onboard UUV decision-making architectures

- Quantum sensing systems for next-generation underwater detection

- Secure undersea communications and network-centric warfare integration

is transforming the market from single-platform procurement into a connected, autonomous, multi-domain undersea battlespace ecosystem.

The Undersea Warfare Systems Market is transitioning from legacy crewed submarine dominance to autonomous, networked underwater combat platforms, offering:

- Persistent multi-domain maritime domain awareness

- Real-time undersea threat intelligence dashboards

- Automated mission execution and ROE-compliant engagement protocols

- AI-driven acoustic signature libraries and predictive threat modeling

This evolution is shifting the market from individual platform acquisition to integrated undersea warfare architecture investment

Edge AI & Real-Time Undersea Intelligence Revolution

The integration of Edge AI in Underwater Warfare Systems is enabling real-time threat processing directly onboard UUV and submarine platforms, eliminating the communication latency and signal exposure risk associated with surface-dependent data workflows. This advancement is transforming mission-critical applications such as covert ISR operations, mine countermeasures, and undersea infrastructure defense, where immediate onboard decision-making is operationally non-negotiable.

Edge AI enables:

- Onboard acoustic threat classification and autonomous engagement authorization

- Reduced acoustic and electromagnetic signature exposure during data transmission

- Enhanced operational endurance in communications-denied deep-ocean environments

This trend is significantly strengthening Underwater Warfare Systems Market Trends, shifting the industry toward fully autonomous undersea intelligence and lethal decision-support architectures.

Integration of Underwater Warfare Systems with Joint Defense Digital Platforms

The increasing integration of undersea warfare data with joint force command systems, maritime situational awareness platforms, and national defense digital architectures is redefining how naval commands utilize sub-surface intelligence. Defense establishments are embedding UUV sensor data, sonar threat feeds, and submarine tactical intelligence directly into joint operational planning workflows, enabling seamless multi-domain decision-making at fleet command level.

This integration supports:

- End-to-end multi-domain operational integration across submarine, surface, and air warfare assets

- Enhanced maritime domain awareness through AI-fused undersea sensor networks

- Data-driven submarine fleet lifecycle management and predictive maintenance optimization

As a result, Underwater Warfare Systems Market Growth is increasingly driven by its role as the foundational intelligence layer within national multi-domain defense transformation strategies, rather than standalone naval platform procurement.

Strategic Defense ROI & Capability Value Analysis in the Underwater Warfare Systems Market

One of the defining procurement justification frameworks in the Global Underwater Warfare Systems Market is Capability Return on Investment — the measurable improvement in maritime deterrence, threat detection speed, and operational endurance delivered per defense dollar invested.

Naval forces and defense ministries achieve strategic value through:

- UUV Lifecycle Cost Reduction (40–60% vs. crewed submarine equivalents)

- Detection Cycle Compression (up to 70% faster threat classification via AI sonar)

- Reduced Crew Risk Exposure through autonomous platform deployment

- Improved Acoustic Intelligence Accuracy (up to 90%+ via ML-enhanced signal processing)

The Underwater Warfare Systems Market Analysis indicates that navies deploying integrated AI-sonar and UUV architectures achieve full operational capability within 24–36 month procurement and integration cycles, representing highly defensible return on sovereign defense investment.

The adoption of AI in the Underwater Warfare Systems Market further enhances mission cost-efficiency by reducing crewed platform exposure, extending operational endurance, and improving predictive threat intelligence accuracy across all deployment scenarios.

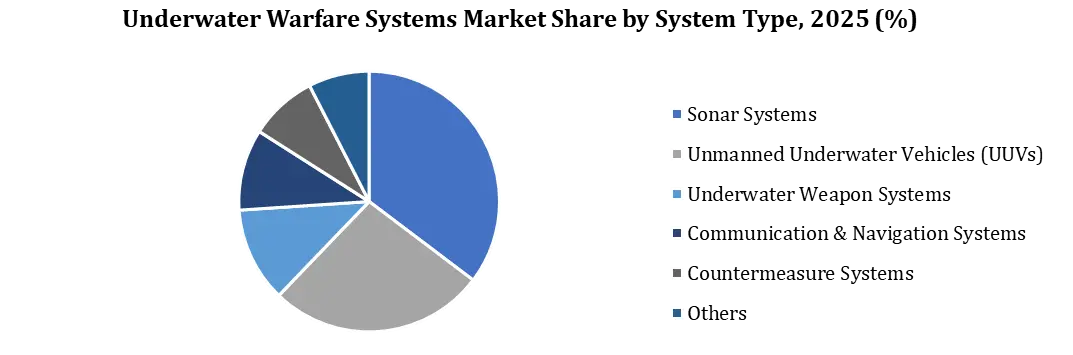

Underwater Warfare Systems Market Segmentation Analysis

The Weapon Systems segment dominated the Underwater Warfare Systems Market in 2025 and accounted for the largest market share due to rising naval modernization programs, increasing procurement of heavyweight torpedoes, anti-torpedo defense systems, and underwater missile platforms by major naval powers including the U.S., China, Russia, and India. Modern naval forces are heavily investing in precision-guided underwater weapons to strengthen anti-submarine warfare (ASW) capabilities and maritime deterrence operations. The increasing deployment of advanced submarines and underwater combat platforms across strategic maritime regions such as the Indo-Pacific and North Atlantic further accelerated the adoption of underwater weapon systems.

The Unmanned Underwater Vehicles (UUVs) segment is projected to be the fastest-growing segment during the forecast period owing to increasing adoption of autonomous underwater surveillance, mine countermeasure missions, seabed warfare, and intelligence gathering operations. Defense agencies are increasingly integrating AI-enabled autonomous underwater systems to reduce operational risk and improve underwater situational awareness. Growing investments in autonomous naval warfare technologies and underwater drone development are expected to drive strong future demand for UUV systems globally.

Underwater Warfare Systems Market Regional Insights

North America Underwater Warfare Systems Market – Market Leader

North America dominates global market revenue, anchored by the U.S. Navy's unmatched defense budget, Virginia-class submarine program expansion, and USD 1.2 billion specifically earmarked for advanced undersea technologies in fiscal 2025. Deep industrial integration across Lockheed Martin, Northrop Grumman, Raytheon, and General Dynamics sustains a procurement pipeline with multi-decade structural depth.

Europe Underwater Warfare Systems Market – Alliance-Driven Modernization

Europe advances on NATO collective defense commitments, UK Astute and SSNR submarine fleet investment, French nuclear deterrence modernization, and accelerating German naval rearmament. Collaborative EU defense industrial frameworks and bilateral Anglo-French maritime programs are systematically upgrading ASW capability, autonomous undersea systems, and next-generation torpedo technology across the region.

Asia Pacific Underwater Warfare Systems Market – Fastest Growing Region

China's 60+ hull submarine fleet expansion, India's P-75I submarine program and DRDO-led AUV development, Japan's historic defense budget reorientation, South Korea's indigenous submarine programs, and Australia's AUKUS nuclear submarine acquisition are simultaneously active creating the highest-concentration of structural, government-mandated undersea warfare procurement demand in the world. Every unresolved maritime territorial dispute in the region converts directly into underwater warfare systems investment.

Middle East & Africa Underwater Warfare Systems Market – Emerging Strategic Opportunity

Gulf state naval modernization programs, strategic chokepoint defense requirements across the Strait of Hormuz, Bab-el-Mandeb, and Red Sea corridors, and growing GCC investment in mine countermeasure and coastal submarine defense capabilities are driving accelerating adoption of underwater warfare systems across the region.

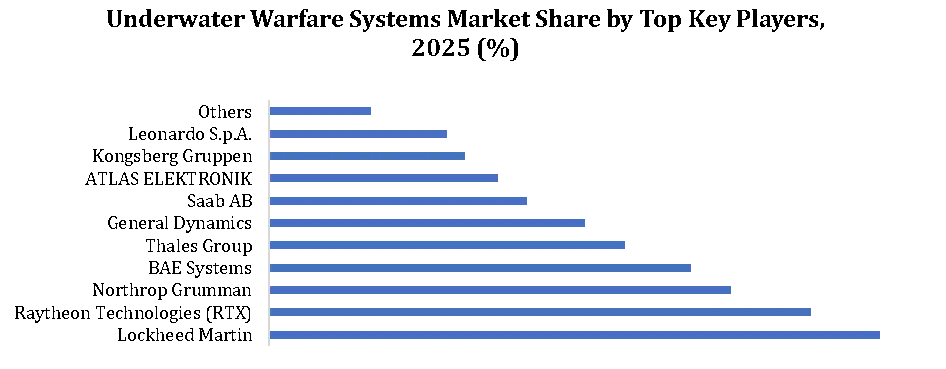

Underwater Warfare Systems Market Competitive Landscape

The Global Underwater Warfare Systems Market Competitive Landscape is a concentrated, high-barrier, sovereign-aligned ecosystem where market leaders hold structural advantages through classified technology depth, export licensing positions, and government-mandated program incumbency that no commercial entrant can replicate on conventional timelines.

These companies are driving innovation in the Undersea Warfare Systems Market, enhancing competitive positioning through AI integration, autonomous platform development, and multi-domain defense architecture contracts.

Recent Key Developments

|

Date |

Company |

Development |

Impact |

|

Jan-25 |

Lockheed Martin |

Awarded USD 502M contract for Hypervisor Technology Zero Surface Ship Undersea Warfare combat systems |

Strengthened U.S. Navy surface ASW modersnization pipeline |

|

Jan-25 |

Mazagon Dock / thyssenkrupp Marine Systems |

Secured approval to jointly build six advanced conventional submarines for Indian Navy |

Accelerated Indo-Pacific undersea capability expansion |

|

Oct-25 |

Kongsberg Gruppen |

Proposed independent listing of maritime business on Oslo Stock Exchange |

Sharpened defense operational focus and capital strategy |

|

Sep-25 |

Inmarsat / Pulsar International |

Expanded NexusWave maritime connectivity across 300+ vessels |

Enhanced undersea and surface fleet digital integration |

|

Jun-24 |

BAE Systems |

Completed sea trials for next-generation submarine with advanced sonar and AUV integration |

Validated next-generation undersea combat system architecture |

Report Coverage

|

Global Underwater Warfare Systems Market |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026 -2032 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 15.68 Bn |

|

Forecast Period 2025 to 2032 CAGR: |

7.3% |

Market Size in 2032: |

USD 25.63 Bn. |

|

Segments |

By System Type |

Sonar Systems Unmanned Underwater Vehicles (UUVs) Underwater Weapon Systems Communication & Navigation Systems Countermeasure Systems Others |

|

|

By Platform |

Submarines Surface Combatants Naval Helicopters Maritime Patrol Aircraft Airborne ASW Platforms Unmanned Platforms Others |

||

|

By Operation Type |

Manned Systems Unmanned Systems Autonomous Systems |

||

|

By Application |

Anti-Submarine Warfare (ASW) Surveillance & Reconnaissance Combat Operations Intelligence, Surveillance & Reconnaissance (ISR) Mine Countermeasure (MCM) Seabed Warfare Infrastructure Protection Others |

||

|

By End User |

Navy Coast Guard Special Defense Forces Homeland Security Agencies |

||

By Geography:

North America (United States, Canada, Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Netherlands, Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Rest of APAC)

Middle East and Africa (South Africa, Saudi Arabia, UAE, Egypt, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Key Players / Competitor Profiles Covered in the Underwater Warfare Systems Market Report

Tier 1 – Market Leaders (Submarine & Integrated Undersea Warfare Primes)

- Lockheed Martin Corporation

- Raytheon Technologies (RTX)

- Northrop Grumman Corporation

- BAE Systems plc

- General Dynamics Corporation

- Thales Group

- Saab AB

- Leonardo S.p.A.

- Huntington Ingalls Industries

- Naval Group

Tier 2 – Weapons, Torpedo & Electronic Warfare Systems Providers

12. Kongsberg Gruppen AS

13. L3Harris Technologies

14. Elbit Systems Ltd.

15. Israel Aerospace Industries (IAI)

16. Rafael Advanced Defense System

17. ASELSAN A.?.

18. Fincantieri S.p.A.

19. Navantia S.A.

20. Babcock International Group

Tier 3 – Sonar, Acoustic Sensing & Undersea Communications Specialists

21. Sonardyne International Ltd.

22. Ultra Electronics Holdings

23. QinetiQ Group plc

24. ECA Group

25. S.A. de Electronica Submarina (SAES)

26. Hydroid Inc.

(Kongsberg subsidiary)

27. Kraken Robotics Inc.

28. Covelya Group (formerly SEA)

29. Curtiss-Wright Corporation

30. DRS Technologies

Tier 4 – Autonomous Underwater Vehicle (AUV/UUV) & Robotics Focused Players

31. Bluefin Robotics (General Dynamics)

32. Iver AUV Systems

33. Ocean Aero Inc.

34. Saildrone Inc.

35. Aquabotix Technology Corporation

36. Teledyne Marine

37. iXblue (EXAIL Technologies)

38. EvoLogics GmbH

39. VideoRay LLC

40. Liquid Robotics (Boeing subsidiary)

Frequently Asked Questions

The growth of the Underwater Warfare Systems Market is driven by rising geopolitical tensions, increasing anti-submarine warfare (ASW) requirements, naval fleet modernization, and growing deployment of autonomous underwater vehicles (AUVs) and unmanned underwater vehicles (UUVs). The integration of AI-powered sonar systems, edge AI, quantum sensing, and real-time maritime domain awareness technologies is also accelerating market expansion.

North America dominates the Underwater Warfare Systems Market due to the strong presence of major defense contractors, high U.S. naval defense spending, Virginia-class submarine expansion programs, and advanced investments in undersea warfare technologies. Asia Pacific is expected to emerge as the fastest-growing region during the forecast period due to rising defense budgets and increasing submarine procurement activities across China, India, Japan, South Korea, and Australia.

Autonomous Underwater Vehicles (AUVs) are unmanned, self-operating underwater systems designed for surveillance, reconnaissance, mine detection, anti-submarine warfare, seabed mapping, and underwater intelligence missions. These systems operate without continuous human control and use advanced sensors, AI-based navigation, sonar technologies, and real-time data processing to perform complex underwater operations efficiently.

Major companies operating in the Underwater Warfare Systems Market include Lockheed Martin Corporation, Raytheon Technologies (RTX), Northrop Grumman Corporation, BAE Systems plc, General Dynamics Corporation, Thales Group, Saab AB, Leonardo S.p.A., Huntington Ingalls Industries, Naval Group, Kongsberg Gruppen, ATLAS ELEKTRONIK GmbH, L3Harris Technologies, Teledyne Marine, and Kraken Robotics Inc. These companies are heavily investing in AI-powered sonar systems, autonomous underwater platforms, and next-generation naval combat technologies.

1. Underwater Warfare Systems Market: Research Methodology

2. Underwater Warfare Systems Market Introduction

2.1 Study Assumptions and Market Definition

2.2 Scope of the Study

2.3 Executive Summary

3. Global Underwater Warfare Systems Market: Competitive Landscape

3.1 Competition Matrix

3.2 Competitive Positioning of Key Players

3.3 Key Players Benchmarking (Company Name · Headquarters · Business Segment · End User · Revenue 2025 · Profit Margin · Growth Rate · R&D Expenditure · Certifications · Geographical Presence)

3.4 Market Structure (Market Leaders · Market Followers · Emerging Players)

3.5 Mergers, Acquisitions & Strategic Partnerships

3.6 Recent Developments

4. Global Underwater Warfare Systems Market: Dynamics

4.1 Market Trends

4.2 Market Dynamics (Drivers · Restraints · Opportunities · Challenges)

4.3 PORTER's Five Forces Analysis

4.4 PESTLE Analysis

4.5 Key Opinion Leader Analysis

5. Emerging Trends Shaping the Underwater Warfare Systems Industry

5.1 UUV-as-a-Capability (UaaC) and modular autonomous undersea platform adoption

5.2 AI and Machine Learning integration in sonar signal processing and threat classification

5.3 Automated acoustic signature recognition, anomaly detection, and real-time ASW dashboards

5.4 Digital twin and undersea environment modeling for submarine tactical planning

5.5 Real-time oceanographic simulation and mission rehearsal using sensor-fused data models

5.6 Undersea critical infrastructure protection for submarine cables, pipelines, and offshore assets

5.7 Seabed warfare, strategic domain denial, and mine countermeasure system advancements

6. Technology Disruption & Defense Transformation Strategy

6.1 AI-powered sonar analytics and predictive acoustic intelligence platforms

6.2 Edge AI-enabled onboard UUV decision-making and autonomous engagement architectures

6.3 Quantum sensing systems and next-generation underwater detection capabilities

6.4 Secure undersea communications and low-probability-of-intercept data link architectures

6.5 Transition from single-platform procurement to integrated undersea battlespace architecture

6.6 Predictive threat modeling and real-time decision support systems in naval operations

6.7 Automated mission execution and AI-driven ROE-compliant engagement protocols

6.8 Shift from platform acquisition to multi-domain undersea warfare architecture investment

7. Advanced Autonomy & Edge Computing Evolution in Undersea Warfare

7.1 Edge AI revolution in onboard UUV and submarine data processing

7.2 Autonomous threat classification and instant engagement decision-making capabilities

7.3 Reduced acoustic and electromagnetic exposure through onboard processing architectures

7.4 Real-time applications in covert ISR, mine countermeasures, and undersea strike operations

7.5 Next-generation autonomous undersea weapons systems and swarming UUV architectures

8. Joint Defense Integration & Multi-Domain Ecosystem Expansion

8.1 Integration of undersea warfare data with joint force command and maritime situational awareness platforms

8.2 End-to-end multi-domain operational integration across submarine, surface, and air warfare assets

8.3 AI-fused undersea sensor networks and enhanced maritime domain awareness

8.4 Data-driven submarine fleet lifecycle management and predictive maintenance models

8.5 Role of undersea warfare systems as foundational intelligence layer in national defense transformation

9. Strategic Defense ROI & Capability Value Analysis

9.1 Capability Return on Investment (ROI) benchmarking in Underwater Warfare Systems Market

9.2 UUV lifecycle cost reduction potential (40–60% vs. crewed equivalents)

9.3 Detection cycle compression and operational tempo improvement via AI sonar

9.4 Crew risk reduction and platform survivability improvement through autonomous deployment

9.5 High acoustic intelligence accuracy levels (up to 90%+) via ML-enhanced signal processing

9.6 Full operational capability realization cycle (24–36 month integration benchmark)

9.7 AI in Underwater Warfare Systems enhancing mission cost-efficiency and predictive capability

10. Underwater Warfare Systems Market: Global Market Size and Forecast by Segmentation (by Value in USD Billion) (2025–2032)

10.1 By System (2025–2032)

10.2 By Platform (2025–2032)

10.3 By Mode of Operation (2025–2032)

10.4 By Application (2025–2032)

10.5 By End User (2025–2032)

11. North America Underwater Warfare Systems Market (2025–2032)

11.1 United States

11.1.1 By System (2025–2032)

11.1.2 By Platform (2025–2032)

11.1.3 By Mode of Operation (2025–2032)

11.1.4 By Application (2025–2032)

11.1.5 By End User (2025–2032)

11.2 Canada

11.3 Mexico

12. Europe Underwater Warfare Systems Market (2025–2032)

12.1 UK

12.2 France

12.3 Germany

12.4 Italy

12.5 Spain

12.6 Sweden

12.7 Netherlands

12.8 Rest of Europe

13. Asia Pacific Underwater Warfare Systems Market (2025–2032)

13.1 China

13.2 South Korea

13.3 Japan

13.4 India

13.5 Australia

13.6 Indonesia

13.7 Malaysia

13.8 Vietnam

13.9 Taiwan

13.10 Rest of APAC

14. Middle East and Africa Underwater Warfare Systems Market (2025–2032)

14.1 South Africa

14.2 Saudi Arabia

14.3 UAE

14.4 Egypt

14.5 Nigeria

14.6 Rest of ME&A

15. South America Underwater Warfare Systems Market (2025–2032)

15.1 Brazil

15.2 Argentina

15.3 Rest of South America

16. Company Profiles: Key Players

16.1 Lockheed Martin Corporation

16.2 Raytheon Technologies (RTX)

16.3 Northrop Grumman Corporation

16.4 BAE Systems plc

16.5 General Dynamics Corporation

16.6 Thales Group

16.7 Saab AB

16.8 Leonardo S.p.A.

16.9 Huntington Ingalls Industries

16.10 Naval Group

16.11 ATLAS ELEKTRONIK GmbH

16.12 Kongsberg Gruppen AS

16.13 L3Harris Technologies

16.14 Elbit Systems Ltd.

16.15 Israel Aerospace Industries (IAI)

16.16 Rafael Advanced Defense Systems

16.17 ASELSAN A.?.

16.18 Fincantieri S.p.A.

16.19 Navantia S.A.

16.20 Babcock International Group

16.21 Sonardyne International Ltd.

16.22 Ultra Electronics Holdings

16.23 QinetiQ Group plc

16.24 ECA Group

16.25 S.A. de Electronica Submarina (SAES)

16.26 Hydroid Inc.

16.27 Kraken Robotics Inc.

16.28 Covelya Group

16.29 Curtiss-Wright Corporation

16.30 DRS Technologies

17. Key Findings

18. Strategic Recommendations