Fixed-Wing VTOL UAV Market: AI-Powered Autonomous Aviation, Hybrid UAV Platforms & BVLOS Drone Operations Driving Market Growth (2026–2032)

The Fixed-Wing VTOL UAV Market is valued at USD 3.94 billion in 2025 and is projected to reach USD 16.87 billion by 2032, growing at a CAGR of 23.11%. Market growth is supported by rising defence modernization programs, increasing adoption of AI-powered autonomous drones, expansion of BVLOS operations, growth in industrial aerial intelligence applications, and increasing demand for runway-independent UAV systems across commercial and military sectors.

Global Fixed-Wing VTOL UAV Market Overview

Fixed-Wing VTOL UAVs have evolved into a critical segment of modern autonomous aviation because enterprises, defence agencies, and governments increasingly require long-endurance aerial systems capable of vertical take-off, precision maneuverability, and efficient fixed-wing cruise operations. These UAV platforms combine the endurance, speed, and operational efficiency of fixed-wing aircraft with the deployment flexibility of rotary-wing drones.

The Global Fixed-Wing VTOL UAV Market is transitioning from conventional drone deployment toward fully autonomous aerial intelligence ecosystems powered by AI, edge computing, cloud-native mission management, and advanced propulsion technologies. Enterprises and defence agencies are increasingly prioritizing scalable UAV infrastructure capable of enabling persistent surveillance, predictive analytics, autonomous navigation, and real-time operational intelligence across complex mission-critical environments. The convergence of intelligent aviation systems, digital twin ecosystems, GIS integration, and BVLOS regulatory expansion is expected to fundamentally reshape the future of autonomous aerospace operations during the forecast period.

.webp)

To get more Insights: Request Free Sample Report

Global Fixed-Wing VTOL UAV Market Dynamics

Operators increasingly rely on fixed-wing VTOL UAV systems for far more than aerial imaging or surveillance. UAV platforms are now deployed for infrastructure inspection, border monitoring, tactical intelligence gathering, disaster response, logistics delivery, environmental analytics, and autonomous industrial operations. Fixed-wing VTOL UAVs have become mission-critical intelligence and operational systems across multiple industries.

Traditional market factors including regulatory approvals, battery limitations, cybersecurity concerns, payload integration complexity, and BVLOS operational restrictions continue influencing supplier selection and deployment strategies. Providers offering autonomous navigation capability, longer flight endurance, AI-powered analytics, and scalable UAV fleet management systems are expected to gain stronger demand across defence, enterprise, industrial, and government sectors.

Drivers behind the Growth of Global Fixed-Wing VTOL UAV Market

The rapid expansion of BVLOS (Beyond Visual Line of Sight) drone regulations is significantly accelerating commercial UAV deployment across industrial, enterprise, and government sectors. Aviation authorities and regulatory agencies are increasingly supporting autonomous drone corridors, remote air traffic management systems, and long-range UAV operations to enable scalable commercial drone ecosystems.

Growing defence modernization programs are further strengthening market demand for tactical ISR drones, autonomous surveillance systems, AI-enabled reconnaissance platforms, and long-endurance military UAVs capable of supporting mission-critical intelligence operations across complex operational environments. Governments are increasingly prioritizing next-generation autonomous aviation technologies to enhance border security, tactical monitoring, and real-time battlefield intelligence capabilities.

The increasing need for runway-independent aerial systems is also accelerating the adoption of fixed-wing VTOL UAV platforms across remote industrial environments, offshore inspection operations, disaster response missions, mining analytics, and precision agriculture applications. Enterprises are increasingly adopting autonomous UAV systems to improve operational efficiency, reduce manpower dependency, and enable real-time aerial intelligence generation.

In addition, advancements in autonomous flight technologies are significantly improving mission planning, route optimization, obstacle avoidance, predictive maintenance, and drone swarm coordination capabilities. The integration of edge AI analytics and intelligent flight management systems is enabling UAV platforms to process mission-critical operational data in real time while improving decision-making efficiency across industrial and defence applications.

Global Fixed-Wing VTOL UAV Market Restraints

Regulatory complexity remains a key barrier for UAV deployment across multiple regions. Operators must comply with evolving airspace management frameworks, flight permissions, UAV certification requirements, and data privacy regulations before scaling commercial operations.

Battery endurance limitations continue affecting smaller electric UAV systems, particularly in long-range missions requiring extended flight duration, high payload capacity, and adverse weather operation capability.

Cybersecurity risks remain a growing concern as autonomous UAV ecosystems increasingly depend on cloud-based mission systems, AI analytics platforms, satellite communication networks, and real-time telemetry infrastructure.

High deployment costs associated with AI-enabled autonomous UAV systems, advanced ISR payloads, hybrid propulsion architectures, and secure communication systems continue limiting adoption among smaller enterprises.

Export controls and defence-related UAV restrictions could impact global supply chains, international partnerships, and cross-border drone technology transfer.

Global Fixed-Wing VTOL UAV Market Opportunities

Hybrid-electric propulsion systems are creating significant growth opportunities for long-endurance UAV operations by improving fuel efficiency, payload optimization, operational sustainability, and mission scalability. Manufacturers are increasingly investing in advanced propulsion architectures to support next-generation UAV platforms capable of operating across complex industrial and defence environments.

The emergence of standardized modular UAV architectures is expected to accelerate enterprise adoption by simplifying payload integration, maintenance workflows, fleet scalability, and mission customization capabilities. This modular ecosystem approach is helping enterprises deploy flexible UAV intelligence platforms tailored to industry-specific operational requirements.

Drone-as-a-Service (DaaS) business models are also transforming the commercial UAV ecosystem by reducing capital expenditure barriers and enabling organizations to adopt scalable aerial intelligence services across infrastructure inspection, agriculture, logistics, environmental monitoring, and industrial automation sectors.

At the same time, global smart city development initiatives are generating strong demand for autonomous traffic monitoring UAVs, emergency response drone systems, environmental intelligence platforms, and smart infrastructure inspection solutions. The growing adoption of intelligent urban infrastructure is expected to create long-term opportunities for autonomous fixed-wing VTOL UAV deployment.

Autonomous drone swarm technologies are also emerging as a major innovation area across defence operations, perimeter security, disaster response, search-and-rescue missions, and large-area surveillance applications. These collaborative UAV ecosystems are expected to significantly expand the operational capabilities of future autonomous aviation systems.

Global Fixed-Wing VTOL UAV Market Challenges

Fixed-wing VTOL UAV systems remain difficult to scale because platforms must operate reliably in remote, mission-critical, and dynamic operational environments where system failure can significantly impact safety and operational continuity.

High R&D costs, autonomous flight validation requirements, AI reliability testing, propulsion optimization challenges, and complex aerospace certification procedures continue slowing commercialization timelines for next-generation UAV technologies.

Small UAV platforms face operational constraints related to:

- Payload limitations

- Power availability

- Edge AI processing capability

- Flight endurance

- Real-time data transmission

Cross-border regulatory inconsistency remains a challenge for global UAV fleet expansion and commercial BVLOS deployment.

Global Fixed-Wing VTOL UAV Market Trends

AI-enabled autonomous UAV systems continue transforming the fixed-wing VTOL UAV industry by improving real-time intelligence generation, autonomous navigation, predictive mission analytics, and operational efficiency. Enterprises and defence agencies are increasingly investing in intelligent aerial systems capable of supporting scalable autonomous operations across mission-critical environments.

Hybrid-electric UAV propulsion technologies are gaining strong market traction because of their ability to improve flight endurance, reduce fuel consumption, lower operational emissions, and optimize payload performance. These technologies are becoming increasingly important as organizations prioritize sustainable aviation infrastructure and long-duration autonomous flight capability.

Drone fleet automation platforms are rapidly evolving through the integration of edge AI processing, cloud-based mission systems, real-time telemetry infrastructure, autonomous analytics engines, and predictive maintenance capabilities. Organizations are increasingly adopting centralized UAV ecosystem management platforms to improve fleet scalability, mission coordination, and operational visibility.

The integration of UAV-generated aerial intelligence with GIS systems, industrial IoT infrastructure, enterprise asset management platforms, and digital twin ecosystems is further expanding the commercial value proposition of fixed-wing VTOL UAV systems. Enterprises are increasingly leveraging drone-generated operational intelligence to support predictive decision-making and infrastructure optimization strategies.

In addition, drone logistics and autonomous cargo delivery applications are gaining commercial momentum across healthcare, industrial supply chains, remote infrastructure operations, and emergency response ecosystems. The growing maturity of autonomous aerial logistics networks is expected to create significant long-term growth opportunities for fixed-wing VTOL UAV platforms.

Global Fixed-Wing VTOL UAV Market Segmentation Analysis

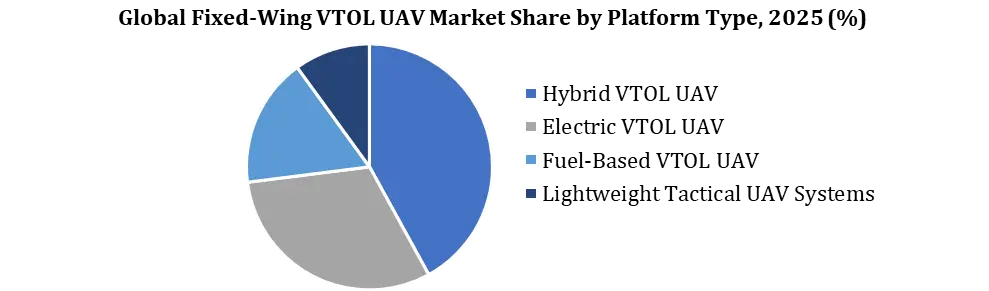

Global Fixed-Wing VTOL UAV Market by Platform Type

Hybrid VTOL UAVs lead the Global Fixed-Wing VTOL UAV Market with a 42% share because they provide superior endurance, operational flexibility, payload optimization, and long-range mission capability. Electric VTOL UAVs follow with a 31% share, driven by growing adoption in smart agriculture, infrastructure inspection, mapping, and commercial analytics applications. Fuel-based VTOL UAVs hold a xx% share due to their deployment in defence and long-duration tactical missions, while lightweight tactical UAV systems account for xx%, mainly because of border surveillance, ISR operations, and industrial monitoring applications.

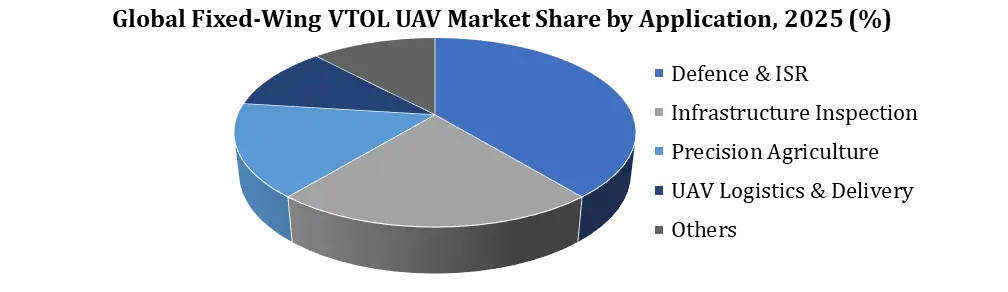

Global Fixed-Wing VTOL UAV Market by Application

Defence & ISR operations lead the Global Fixed-Wing VTOL UAV Market with a 39% share, driven by increasing military modernization programs, border surveillance requirements, and AI-enabled tactical intelligence operations. Infrastructure inspection holds a xx% share due to rising deployment across energy, utilities, transportation, and industrial monitoring sectors. Precision agriculture accounts for xx%, supported by crop intelligence, precision spraying, and smart farming automation. UAV logistics & delivery hold a xx% share as autonomous delivery networks and drone logistics ecosystems continue expanding globally.

Global Fixed-Wing VTOL UAV Market by Technology

AI-enabled autonomous UAV systems dominate the market with a 46% share because organizations increasingly require autonomous navigation, real-time analytics, predictive flight intelligence, and scalable drone fleet automation. Semi-autonomous flight systems follow with a xx% share due to enterprise transition strategies toward autonomous operations. Remotely operated UAV systems account for xx%, primarily across regulated defence, industrial, and government-controlled operations.

Global Fixed-Wing VTOL UAV Market Competitive Landscape

The Global Fixed-Wing VTOL UAV Market demonstrates an increasingly competitive environment. Large aerospace and defence companies dominate high-value defence surveillance, ISR, and long-endurance tactical missions due to their strong aerospace infrastructure, autonomous technology capability, and established government contracts.

At the same time, emerging UAV technology providers are rapidly gaining traction across commercial, industrial, agriculture, mapping, and logistics applications where enterprises require modular, scalable, AI-enabled, and cost-efficient UAV systems.

Competition is increasingly shifting toward:

- AI-powered autonomous capability

- Hybrid-electric propulsion efficiency

- BVLOS operational readiness

- Real-time aerial intelligence

- Drone fleet scalability

- Cloud-based mission ecosystems

Suppliers offering strong flight endurance, easier payload integration, scalable fleet automation, and lower operational complexity are expected to gain stronger market positioning.

|

Company Type |

Competitive Strength |

Market Position |

|

Global aerospace & defence companies |

Strong ISR capability, aerospace infrastructure, defence contracts |

Lead in military and tactical UAV operations |

|

Commercial UAV platform providers |

Scalable industrial drone ecosystems and analytics capability |

Strong in enterprise UAV deployment |

|

AI-powered autonomous UAV companies |

Autonomous navigation and edge AI intelligence |

Growing in smart aerial analytics |

|

Hybrid-electric UAV innovators |

Long-endurance and sustainable propulsion systems |

Expanding in industrial and logistics applications |

|

Drone mapping & analytics providers |

Geospatial intelligence and digital twin integration |

Growing in infrastructure and surveying operations |

Global Fixed-Wing VTOL UAV Recent Market Movements

AI-enabled autonomous UAV systems are moving into mainstream aerospace operations as enterprises increasingly require real-time mission intelligence, autonomous navigation, and scalable aerial analytics.

Hybrid-electric propulsion technologies are becoming commercially viable as manufacturers focus on longer endurance, fuel optimization, lower emissions, and sustainable aerial mobility.

BVLOS drone operations are gaining stronger regulatory support, increasing deployment opportunities across:

- Infrastructure inspection

- Logistics delivery

- Industrial monitoring

- Agriculture analytics

- Remote surveillance

Drone fleet automation platforms are gaining buyer interest because enterprises increasingly prefer centralized UAV management systems with:

- Real-time telemetry

- Predictive analytics

- AI-based mission optimization

- Cloud-native command capability

Edge AI integration is becoming a critical purchasing factor as operators seek low-latency aerial intelligence and autonomous decision-making capability. Defence modernization programs are increasing UAV value per platform as governments prioritize tactical intelligence, border security, autonomous surveillance, and ISR modernization initiatives. Supplier competition is increasingly shifting toward production scalability, autonomous capability, and integrated UAV intelligence ecosystems rather than standalone drone hardware.

Global Fixed-Wing VTOL UAV Market Regional Analysis

North America currently dominates the global fixed-wing VTOL UAV market because of its advanced aerospace manufacturing ecosystem, strong defence procurement budgets, rapid AI-enabled aviation innovation, and supportive BVLOS regulatory evolution. The region continues accelerating the deployment of autonomous tactical UAV systems, industrial aerial intelligence platforms, and next-generation drone ecosystem infrastructure across both commercial and military applications.

Europe maintains a strong market position due to increasing investments in sustainable aviation technologies, defence modernization programs, smart mobility initiatives, and industrial automation ecosystems. The region is also emphasizing green UAV propulsion technologies, intelligent aerospace digitization strategies, and advanced airspace integration frameworks to support future autonomous aviation infrastructure.

Asia Pacific demonstrates the highest growth potential as governments and enterprises across China, India, Japan, South Korea, and Southeast Asia continue aggressively investing in defence UAV modernization, smart agriculture technologies, infrastructure digitization, autonomous aerial analytics, and industrial automation initiatives. Rapid technological adoption and expanding UAV manufacturing capability are expected to accelerate regional market growth throughout the forecast period.

The Middle East & Africa region is witnessing steady market expansion through growing investments in border surveillance systems, oil & gas inspection infrastructure, smart city development initiatives, tactical ISR modernization programs, and critical asset monitoring applications. Governments across the region are increasingly prioritizing UAV deployment for security and infrastructure optimization purposes.

South America remains an emerging growth market supported by increasing adoption of agricultural intelligence applications, environmental monitoring solutions, mining analytics platforms, infrastructure inspection technologies, and government surveillance initiatives. Expanding industrial digitization and resource management requirements are expected to support long-term UAV deployment opportunities across the region.

|

Global Fixed-Wing VTOL UAV Market Scope |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026 -2032 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 3.94 Bn |

|

Forecast Period 2026 to 2032 CAGR: |

23.11% |

Market Size in 2032: |

USD 16.83 Bn. |

|

Segments |

By Platform Type |

Hybrid VTOL UAV Electric VTOL UAV Fuel-Based VTOL UAV Tactical Lightweight UAV Systems |

|

|

By Technology

|

AI-Enabled Autonomous UAVs Semi-Autonomous Flight Systems Remotely Operated UAVs |

||

|

By Endurance |

Short-Endurance UAVs Medium-Endurance UAVs Long-Endurance UAVs |

||

|

By Application |

Defence & ISR Operations Infrastructure Inspection Precision Agriculture UAV Logistics & Delivery Mapping & Surveying Environmental Monitoring Disaster Management Border Surveillance |

||

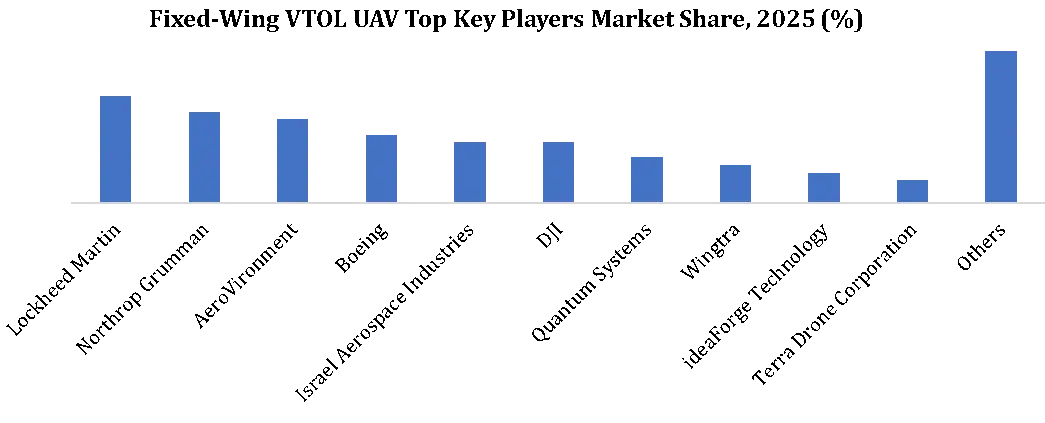

Global Key Players List Covered in the Global Fixed-Wing VTOL UAV Market

- AeroVironment

- Lockheed Martin

- Northrop Grumman

- Boeing

- Israel Aerospace Industries

- Quantum Systems

- Wingtra

- Delair

- DJI

- Parrot SA

- Terra Drone Corporation

- ideaForge Technology

- Garuda Aerospace

- Asteria Aerospace

- Flytrex

- Aironment

- Skydio

- UAVIA

- EDGE Group

- South America Key Players

- XMobots

- Stella Tecnologia

- Others

Frequently Asked Questions

Fixed-wing VTOL UAVs support defence surveillance, infrastructure inspection, precision agriculture, mapping, logistics delivery, disaster response, border monitoring, and industrial aerial intelligence operations.

The Global Fixed-Wing VTOL UAV Market size is estimated at USD 3.94 billion in 2025.

The Fixed-Wing VTOL UAV Market is projected to reach USD 16.87 billion by 2032, supported by autonomous aviation expansion, AI-powered UAV ecosystems, and increasing BVLOS drone deployment.

Hybrid VTOL UAVs hold the largest market share because of their long-endurance capability, operational flexibility, payload efficiency, and suitability for defence and industrial missions.

AI-powered UAV systems improve mission automation, route optimization, aerial analytics, obstacle avoidance, fleet scalability, and real-time operational intelligence.

1. Fixed-Wing VTOL UAV Market: Research Methodology

2. Fixed-Wing VTOL UAV Market Introduction

2.1. Study Assumption and Market Definition

2.2. Scope of the Study

2.3. Executive Summary

1. Global Fixed-Wing VTOL UAV Market: Competitive Landscape

3.1. MMR Competition Matrix

3.2. Competitive Positioning of Key Players

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Headquarter

3.3.3. Business Segment

3.3.4. End User Segment

3.3.5. Total Company Revenue (2026)

3.3.6. Profit Margin (%)

3.3.7. Growth Rate (%)

3.3.8. R&D Expenditure (%)

3.3.9. Certifications

3.3.10. Geographical Presence

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

3.6. Recent Developments

4. Global Fixed-Wing VTOL UAV Market: Dynamics

4.1. Global Fixed-Wing VTOL UAV Market Trends

4.2. Global Fixed-Wing VTOL UAV Market Dynamics

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.2.4. Challenges

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

4.5. Key Opinion Leader Analysis for the Global Fixed-Wing VTOL UAV Market

5. Emerging Trends Shaping the Fixed-Wing VTOL UAV Industry

5.1. AI-powered autonomous flight systems and intelligent mission planning adoption

5.2. BVLOS (Beyond Visual Line of Sight) operations expansion in commercial UAV applications

5.3. Hybrid-electric propulsion technologies improving endurance and operational efficiency

5.4. Advanced ISR (Intelligence, Surveillance & Reconnaissance) capabilities in defense UAV platforms

5.5. Integration of LiDAR, thermal imaging, and hyperspectral sensors in VTOL UAV systems

5.6. Growing deployment in smart agriculture, infrastructure inspection, and geospatial analytics

5.7. Disaster response, border surveillance, and emergency logistics applications using VTOL UAVs

6. Technology Disruption & Digital Transformation Strategy

6.1. AI-enabled autonomous navigation and predictive flight analytics platforms

6.2. Cloud-connected UAV fleet management and mission control systems

6.3. 5G-enabled fixed-wing VTOL UAV communication and real-time data transmission

6.4. Edge computing architectures for low-latency aerial intelligence processing

6.5. Transition from conventional UAVs to intelligent autonomous VTOL aviation systems

6.6. Predictive maintenance and digital twin integration in UAV fleet operations

6.7. Automated mission planning and AI-driven aerial analytics for enterprise workflows

6.8. Shift from manual drone operations to fully autonomous UAV ecosystem management

7. Advanced Autonomy & Edge Intelligence Evolution

7.1. Edge AI and autonomous decision-making revolution in Fixed-Wing VTOL UAV Market

7.2. Onboard data processing and real-time situational awareness capabilities

7.3. Reduced communication dependency and enhanced remote operational performance

7.4. Real-time applications in defense, industrial inspection, and disaster management

7.5. Next-generation autonomous swarm intelligence and UAV coordination systems

8. Enterprise Integration & Digital Ecosystem Expansion

8.1. Integration of Fixed-Wing VTOL UAV systems with ERP, GIS, and enterprise digital platforms

8.2. End-to-end workflow automation in construction, mining, and energy infrastructure projects

8.3. GIS-enabled UAV mapping and geospatial intelligence enhancement

8.4. Data-driven asset monitoring and predictive maintenance capabilities using UAV analytics

8.5. Role of Fixed-Wing VTOL UAVs in enterprise digital transformation strategies

9. Strategic Cost & ROI Analysis in the Fixed-Wing VTOL UAV Market

9.1. Return on Investment (ROI) benchmarking in Fixed-Wing VTOL UAV Market

9.2. Operational cost reduction potential (25–45% savings)

9.3. Faster mission execution and operational efficiency gains (up to 65%)

9.4. Labor cost optimization and enhanced workforce productivity

9.5. High-precision aerial intelligence accuracy levels (up to 96%)

9.6. ROI realization cycle (12–18 months implementation benchmark)

9.7. AI-driven UAV analytics enhancing operational efficiency and predictive capabilities

10. Fixed-Wing VTOL UAV Market: Global Market Size and Forecast by Segmentation by (by Value in USD Billion) (2026–2032)

10.1 By Platform Type

10.2 By Technology

10.3 By Endurance

10.4 By Application

10.5. Fixed-Wing VTOL UAV Market Size and Forecast, By Region (2026–2032)

10.4.1. North America

10.4.2. Europe

10.4.3. Asia Pacific

10.4.4. Middle East and Africa

10.4.5. South America

11. North America Fixed-Wing VTOL UAV Market Size and Forecast by Segmentation by (by Value in USD Billion) (2026–2032)

11.1 By Platform Type

11.2 By Technology

11.3 By Endurance

11.4 By Application

11.4. North America Fixed-Wing VTOL UAV Market Size and Forecast, by Country (2026–2032)

11.4.1. United States

11.4.2. Canada

11.4.3. Mexico

12. Europe Fixed-Wing VTOL UAV Market Size and Forecast by Segmentation (by Value in USD Billion) (2026–2032)

12.1. Europe Fixed-Wing VTOL UAV Market Size and Forecast, By Platform Type (2026–2032)

12.2. Europe Fixed-Wing VTOL UAV Market Size and Forecast, By Technology (2026–2032)

12.3. Europe Fixed-Wing VTOL UAV Market Size and Forecast, By Endurance (2026–2032)

12.4. Europe Fixed-Wing VTOL UAV Market Size and Forecast, By Application (2026–2032)

12.5 Europe Fixed-Wing VTOL UAV Market Size and Forecast, by Country (2026–2032)

12.4.1. United Kingdom

12.4.2. France

12.4.3. Germany

12.4.4. Italy

12.4.5. Spain

12.4.6. Rest of Europe

13. Asia Pacific Fixed-Wing VTOL UAV Market Size and Forecast by Segmentation by (by Value in USD Billion) (2026–2032)

13.1. Asia Pacific Fixed-Wing VTOL UAV Market Size and Forecast, By Platform Type (2026–2032)

13.2. Asia Pacific Fixed-Wing VTOL UAV Market Size and Forecast, By Technology (2026–2032)

13.3. Asia Pacific Fixed-Wing VTOL UAV Market Size and Forecast, By Endurance (2026–2032)

13.4. Asia Pacific Fixed-Wing VTOL UAV Market Size and Forecast, By Application (2026–2032)

13.5. Asia Pacific Fixed-Wing VTOL UAV Market Size and Forecast, by Country (2026–2032)

13.4.1. China

13.4.2. South Korea

13.4.3. Japan

13.4.4. India

13.4.5. Australia

13.4.6. Indonesia

13.4.7. Malaysia

13.4.8. Vietnam

13.4.9. Taiwan

13.4.10. Rest of Asia Pacific

14. Middle East and Africa Fixed-Wing VTOL UAV Market Size and Forecast by Segmentation by (by Value in USD Billion) (2026–2032)

14.1. Middle East and Africa Fixed-Wing VTOL UAV Market Size and Forecast, By Platform Type (2026–2032)

14.2. Middle East and Africa Fixed-Wing VTOL UAV Market Size and Forecast, By Technology (2026–2032)

14.3. Middle East and Africa Fixed-Wing VTOL UAV Market Size and Forecast, By Endurance (2026–2032)

14.4. Middle East and Africa Fixed-Wing VTOL UAV Market Size and Forecast, By Application (2026–2032)

14.5. Middle East and Africa Fixed-Wing VTOL UAV Market Size and Forecast, by Country (2026–2032)

14.4.1. South Africa

14.4.2. UAE

14.4.3. Saudi Arebia

14.4.4. Nigeria

14.4.5. Rest of ME&A

15. South America Fixed-Wing VTOL UAV Market Size and Forecast by Segmentation by Demand and Supply Side (by Value in USD Billion) (2026–2032)

15.1. South America Fixed-Wing VTOL UAV Market Size and Forecast, By Platform Type (2026–2032)

15.2. South America Fixed-Wing VTOL UAV Market Size and Forecast, By Technology (2026–2032)

15.3. South America Fixed-Wing VTOL UAV Market Size and Forecast, By Endurance (2026–2032)

15.4. South America Fixed-Wing VTOL UAV Market Size and Forecast, By Application (2026–2032)

15.5. South America Fixed-Wing VTOL UAV Market Size and Forecast, by Country (2026–2032)

15.4.1. Brazil

15.4.2. Argentina

15.4.3. Rest of South America

16. Company Profile: Key Players

16.1. AeroVironment

16.1.1. Company Overview

16.1.2. Business Portfolio

16.1.3. Financial Overview

16.1.4. Strategic Analysis

16.1.5. SWOT Analysis

16.2. Lockheed Martin

16.3. Northrop Grumman

16.4. Boeing

16.5. Israel Aerospace Industries

16.6. Quantum Systems

16.7. Wingtra

16.8. Delair

16.9. DJI

16.10. Parrot SA

16.11. Terra Drone Corporation

16.12. ideaForge Technology

16.13. Garuda Aerospace

16.14. Asteria Aerospace

16.15. Flytrex

16.16. Aironment

16.17. Skydio

16.18. UAVIA

16.19. EDGE Group

16.20. South America Key Players

16.21. XMobots

16.22. Stella Tecnologia

17. Key Findings

18. Strategic Recommendations