Global Satellite Propulsion Market: Electric Propulsion, Sustainable Space Operations & Maneuverable Satellite Platforms Driving Market Growth (2025–2032)

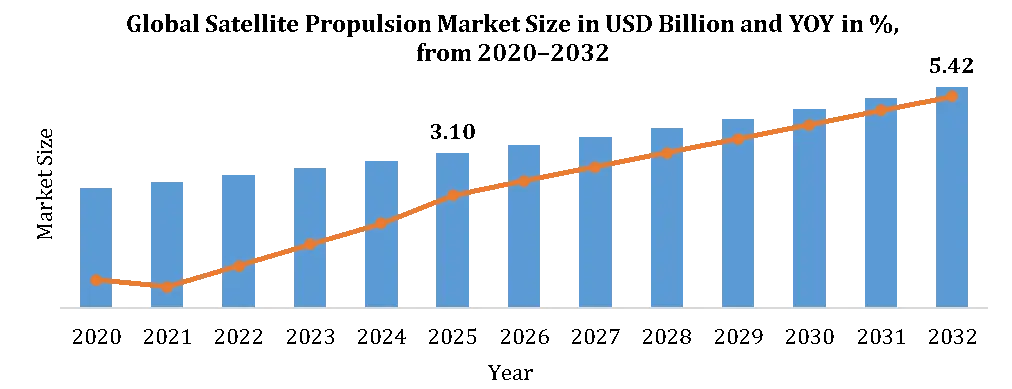

The Global Satellite Propulsion Market is valued at USD 3.10 billion in 2025 and is projected to reach USD 5.42 billion by 2032, growing at a CAGR of 8.3%. Market growth is supported by rising satellite launches, increasing spacecraft mobility requirements, stronger debris-management rules, and growing demand for mission-life extension across commercial, defence, and government satellite programs.

Global Satellite Propulsion Market Overview

Satellite propulsion has evolved into a fundamental feature of current-generation spacecraft design because satellites need to maneuver, change orbits, and remain operational throughout the mission. Propulsion systems help satellites improve orbital precision, maintain mission stability, manage space traffic risks, and carry out safe deorbiting maneuvers, making propulsion a value-protecting system rather than just a support component.

The satellite propulsion market includes much more than thrusters. It covers key hardware such as propellant tanks, valves, feed systems, control electronics, power processing units, and integration hardware that enable reliable spacecraft movement. Electric propulsion is increasingly used in missions that require fuel efficiency, lower spacecraft mass, and longer operating life, while chemical propulsion remains important for missions needing high thrust, fast response, and proven reliability.

To get more Insights: Request Free Sample Report

Global Satellite Propulsion Market Dynamics

Operators use satellite propulsion systems for much more than just orbit control. They depend on propulsion to properly position satellites, provide orbital maintenance, avoid collision threats, prolong mission life, and enable deorbiting at end of life. Satellite propulsion has become an essential mission system for today's satellites.

The same old factors – price pressures, long qualification processes, low on-board power, and strict propellant handling requirements – still play a role in supplier selections. Providers with smaller, more reliable, safer, and easier-to-integrate solutions should see increasing demand from small-satellite producers, military applications, and commercial constellations.

Drivers behind the Growth of Global Satellite Propulsion Market

Strict rules for debris management are helping propulsion systems gain traction for satellite disposal needs. The FCC five-year post-mission disposal requirement for many low earth orbit satellites provides a significant boost to end-of-life propulsion systems.

The need to replace constellations periodically means more ongoing sales of propulsion modules, propellant tanks, valves, and fuel delivery systems. Once customers move beyond initial deployment, the sales cycle becomes less sporadic.

Military and government missions push up the average contract size. National security applications, scientific missions, and other strategic spacecraft’s have higher qualification and redundancy requirements for propulsion architecture.

Global Satellite Propulsion Market Restraints

Long qualification times stand as a barrier to market expansion for satellite propulsion suppliers. In addition to thorough testing of the hardware in different temperatures, vibrations, environments, and endurance tests, each new model requires operator approval to fly.

Propellant handling increases costs and operational challenges. Old-school propellants such as hydrazine require extensive safety protocols, training of ground teams, unique storage techniques, and special handling at launch sites.

Low on-board power availability limits the implementation of electric propulsion. Some smaller satellites lack sufficient power margins to operate electric propulsion efficiently without impacting performance of other mission systems.

Export controls could affect suppliers' ability to sell products abroad. Military-related propulsion technology typically falls under certain regulations limiting transfer and customer access.

Global Satellite Propulsion Market Opportunities

Green propulsion could make launches simpler and safer. New non-toxic or less hazardous propellant options may attract interest where suppliers can demonstrate reliable qualification status and mission-readiness.

Standardized small-satellite propulsion systems could accelerate market development. Small plug-and-play propulsion modules could ease integration challenges for satellite producers while making it easier for providers to scale across CubeSats, nanosats, and microsatellite segments.

In-space servicing requires a reliable mobility solution. Propulsion serves as the enabling component for maneuvering, docking, and positioning servicing spacecraft and satellites.

Collision avoidance features could increase demand for propulsion systems. Autonomous satellites relying on internal decision-making might lead to increased demands for maneuverable propulsion systems.

Global Satellite Propulsion Market Challenges

Satellite propulsion is inherently difficult to scale since the system must be highly reliable once deployed into orbit, where repairs aren't possible. High development costs, testing procedures, thermal limitations, power constraints, and reliability risks slow down production from prototype phase to mass manufacturing.

Another serious challenge for suppliers lies with small satellite platforms. Small satellites need propulsion technology that works within constrained mass, volume, power capacity, and budget.

Global Satellite Propulsion Market Trends

Electric satellite propulsion technology keeps improving efficiency and compactness. Electric propulsion systems such as hall effect thrusters, ion engines, FEEP technology, and RF propulsion allow satellites to cut weight and enhance mission lifetimes.

Green propulsion systems based on water could be gaining momentum. Providers increasingly focus on reduced hazards and simplified logistics without compromising mission performance.

Small satellite propulsion systems get more modular and easy-to-use. Suppliers are working towards producing propulsion modules with integrated thrusters, propellant tanks, valves, electronics, and software for small satellite applications.

Deorbiting, satellite servicing, and collision avoidance technologies drive changes in satellite design. Increasing threat of space debris and collisions results in greater prevention and mitigation measures for satellite operators.

Global Satellite Propulsion Market Segmentation Analysis

Global Satellite Propulsion Market by Propulsion Type:

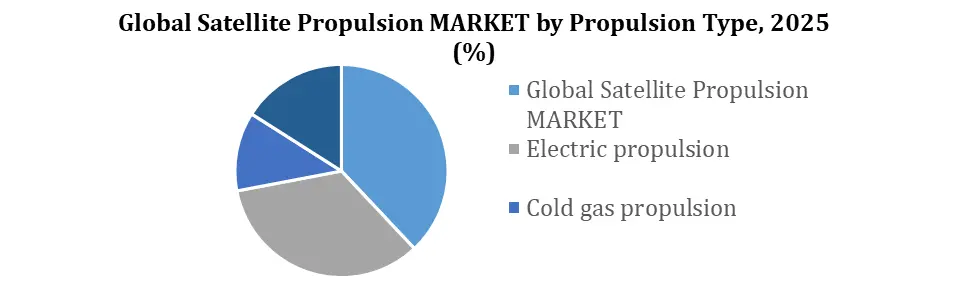

Chemical propulsion leads the Global Satellite Propulsion Market with a 38% share because it supports GEO satellites, defence missions, orbit insertion, and high-thrust maneuvers. Electric propulsion follows with a 34% share, driven by its high efficiency, mass-saving benefits, and growing use in station keeping and orbit raising. Green and hybrid propulsion holds a xx% share as operators look for safer handling and sustainable propellant options, while cold gas propulsion accounts for xx%, mainly due to its use in CubeSats, nanosatellites, attitude control, and low-complexity maneuvers.

Global Satellite Propulsion Market by Satellite Size:

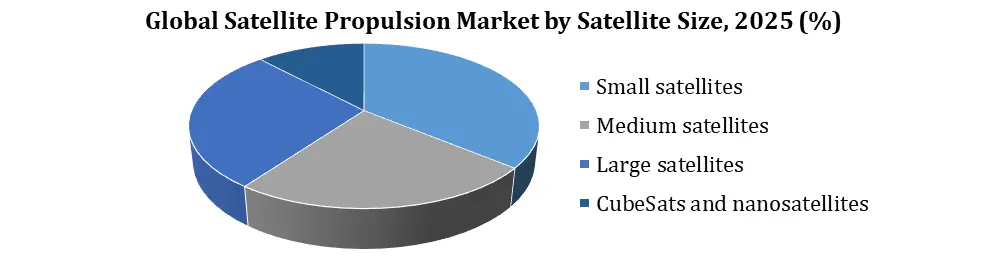

Small satellites lead the Global Satellite Propulsion Market with a 36% share, driven by rising LEO deployment, stronger manoeuvrability requirements, and high unit volumes. Large satellites hold a xx% share, supported by high-value GEO, MEO, and government spacecraft propulsion systems. Medium satellites account for xx%, driven by earth observation, communication, and defence platforms that require integrated propulsion. CubeSats and nanosatellites hold a xx% share as adoption grows, but their lower average selling price keeps their total market value smaller.

Global Satellite Propulsion Market Competitive Landscape

In the Global Satellite Propulsion Market, there exists an interesting competition environment. Traditional aerospace suppliers dominate high-margin GEO, defence missions, and deep space applications due to their ability to provide flight heritage, test facilities, mission reliability, and qualification. In contrast, new entrants have been successful with LEO, CubeSat, nanosatellite, and small satellite applications that require modular, smaller, and more easily integrated propulsion systems.

Competition is now focusing on mission readiness rather than just supply of products. Satellite companies favor propulsion providers that provide orbital heritage, lower integration risk, qualification capabilities, and consistent supply volumes. Thrust consistency, safer fuel, efficient electronics, and consistent manufacturing are going to be the main drivers of success for future players in the market.

|

Global Satellite Propulsion Recent Market Movements

High-power electric propulsion is moving into mainstream spacecraft architecture as mission’s demand better efficiency, stronger thrust control, and longer operating life. This shift increases demand for power processing units, thermal control systems, and precision thrust management.

End-of-life mobility is becoming a more stringent design requirement for satellites. Operators now need propulsion hardware that supports controlled disposal, orbit lowering, and safe mission closure.

Compact propulsion modules are gaining buyer interest because satellite builders want faster integration and lower platform complexity. Systems that combine thrusters, tanks, valves, feed hardware, and electronics help manufacturers reduce assembly effort.

Alternative propellants are moving closer to commercial adoption as manufacturers focus on safer handling, easier storage, and better launch-site logistics. Iodine, water-based systems, and green propellants can gain wider use if they prove strong in-orbit reliability.

Servicing and debris-removal spacecraft are creating demand beyond traditional satellite programs. These missions need rendezvous movement, approach control, docking support, and repeatable thrust performance.

Flight-proven hardware is becoming a stronger purchase filter. Satellite manufacturers prefer suppliers with orbital heritage, qualified systems, and documented mission performance.

Defence and sovereign space programs are increasing propulsion value per spacecraft. These missions often require redundancy, secure supply chains, and high-reliability propulsion architecture.

Supplier competition is shifting toward production readiness. Companies that offer standardized propulsion units, shorter qualification timelines, and stable manufacturing capacity will gain stronger market traction.

Global Satellite Propulsion Market Regional Analysis

North America is currently the biggest market, since it translates high-cost space technologies into actual thrust orders. NASA's Gateway Power and Propulsion Element is employing state-of-the-art electric propulsion thrusters, indicating that North America is trending toward adopting high-power electric propulsion for prolonged duration space missions. This bodes well for higher demand for thrusters, power processing units, control electronics, and other verified propulsion hardware.

European region enjoys a favourable position due to the closer relationship between satellite production, space safety regulations, and orbital environmental conditions. The latest ESA research emphasizes orbital congestion and orbital debris problems, putting increasing demand on satellite operators to implement effective maneuvering, collision avoidance, and deorbit procedures. This practical necessity drives regional demand for deorbiting hardware as well as satellite propulsion systems.

The Asia-Pacific region demonstrates promising growth prospects thanks to domestic development programs in the region. ISRO recently announced 1,000 hours of successful testing of their stationary plasma thruster, indicating that regional space organizations have started developing their propulsion systems domestically, not only purchasing ready-made satellite assemblies. This means that there is higher demand for local propulsion subsystems, including applications in communication, navigation, Earth observation, and defence missions.

Middle East & Africa region is experiencing steady development through selective satellite procurement and regional space programs. There is no wide-spread manufacturing-driven demand in this region yet – it focuses primarily on secured communications, connectivity in rural areas, remote sensing, and regional infrastructure monitoring. With the evolution of such applications, future satellites will require mission life extension, better orbit control, and propulsion dependability.

Despite promising prospects and regional growth, South America is currently a niche regional demand center, not an expansive production base. Here regional demand arises through public satellite programs, space-based communications projects, resource observation, and Earth observation services related to agriculture, climate, and other national missions.

|

Satellite Propulsion Market Scope |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2025 -2032 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 3.1 Bn |

|

Forecast Period 2025 to 2032 CAGR: |

8.3% |

Market Size in 2032: |

USD 5.42 Bn. |

|

Segments |

By Propulsion Type |

Chemical propulsion Electric propulsion Cold gas propulsion Green and hybrid propulsion |

|

|

By Satellite Size

|

Small satellites Medium satellites Large satellites CubeSats and nanosatellites |

||

|

By Orbit |

LEO MEO GEO Deep-space and interplanetary missions |

||

|

By Application |

Station keeping and orbit control Orbit raising and transfer Attitude control and maneuvering Deorbiting, collision avoidance, and mission extension |

||

Global Key Players List covered in the Global Satellite Propulsion Market

North America

- Moog Inc.

- Northrop Grumman

- L3Harris / Aerojet Rocketdyne

- Busek Co.

- Benchmark Space Systems

Europe

- ArianeGroup

- Safran Spacecraft Propulsion

- ThrustMe

- Exotrail

- Sitael

Asia Pacific

- IHI Aerospace

- Bellatrix Aerospace

- Pale Blue

- China Aerospace Science and Technology Corporation

- Mitsubishi Electric

Middle East & Africa

- Rafael Advanced Defence Systems

- Israel Aerospace Industries

South America

- INVAP

- Visiona Tecnologia Espacial

Frequently Asked Questions

Satellite propulsion supports orbit raising, station keeping, attitude control, collision avoidance, deorbiting, maneuvering, and mission-extension operations.

The Global Satellite Propulsion Market size is estimated at USD 3.10 billion in 2025.

The Satellite Propulsion Market forecast reaches USD 5.42 billion by 2032, supported by maneuverable satellites, advanced propulsion systems, and sustainability requirements.

Chemical propulsion holds the largest 2025 share at 38%, mainly because of its flight heritage, high-thrust capability, and continued use in GEO, defence, and mission-critical satellites.

1. Global Satellite Propulsion Market Executive Summary

1.1 Market Snapshot

1.2 2025 Market Size and 2032 Forecast

1.3 CAGR and Key Growth Logic

1.4 Strategic Meaning for Suppliers, Satellite Manufacturers, and Investors

2. Global Satellite Propulsion Market Definition and Scope

2.1 Satellite Propulsion Market Definition

2.2 Propulsion Systems, Thrusters, and Component Coverage

2.3 Satellite Classes Covered

2.4 Mission Functions Covered

2.5 Orbit Coverage

3. Research Methodology and Data Validation

3.1 Bottom-Up Market Sizing Method

3.2 Primary Source Mapping

3.3 Satellite Count and Propulsion Penetration Logic

3.4 ASP and Mission Adjustment Factor

3.5 Top-Down Cross-Check

3.6 CAGR, Segment, and Regional Share Validation

4. Global Satellite Propulsion Market Size Estimation and Forecast

4.1 Global Satellite Propulsion Market Size, 2025

4.2 Global Satellite Propulsion Market Forecast, 2032

4.3 Year-Wise Forecast, 2025–2032

4.4 Demand-Layer Market Build-Up

4.5 CAGR Calculation and Recalculation Check

5. Historical Global Satellite Propulsion Market Analysis, 2020–2024

5.1 Historical Market Size by Year

5.2 Satellite Deployment and Launch Activity Impact

5.3 Government and Defence Mission Influence

5.4 Smallsat and Electric Propulsion Adoption

5.5 Supply-Chain and Qualification Impact

6. Global Satellite Propulsion Market Dynamics

6.1 Key Market Drivers

6.2 Market Restraints

6.3 Market Opportunities

6.4 Market Challenges

6.5 Market Trends

6.6 Demand Shifts Across Commercial, Government, and Defence Missions

7. Global Satellite Propulsion Market Segmentation Analysis

7.1 By Platform

7.2 By System

7.3 By Propulsion Technology

7.4 By End User

7.5 By Region

7.6 Segment Share and Growth Attractiveness

8. Global Satellite Propulsion Market Pricing and Value Chain Analysis

8.1 Satellite Propulsion Value Chain

8.2 Component-Level Value Contribution

8.3 Thruster and Propulsion Module Cost Structure

8.4 ASP by Satellite Size and Mission Type

8.5 Make-vs-Buy Logic for Satellite Manufacturers

9. Global Satellite Propulsion Market Demand-Side Analysis

9.1 Satellite Operator Propulsion Requirements

9.2 Demand by Mission Type in 2025

9.3 Demand from Constellation Operators

9.4 Demand from GEO, MEO, and LEO Satellites

9.5 Demand from Defence, Science, Lunar, and Deep-Space Missions

10. Global Satellite Propulsion Market Regional Analysis

10.1 North America Satellite Propulsion Market

10.2 Europe Satellite Propulsion Market

10.3 Asia Pacific Satellite Propulsion Market

10.4 Middle East & Africa Satellite Propulsion Market

10.5 South America Satellite Propulsion Market

10.6 Regional Share and Demand Logic

11. Global Satellite Propulsion Market Technology Landscape

11.1 Chemical Propulsion

11.2 Electric Propulsion

11.3 Hall-Effect and Ion Thrusters

11.4 Cold Gas Propulsion

11.5 Green, Water-Based, Iodine, and Hybrid Propulsion

11.6 Technology Readiness and Flight Heritage Comparison

12. Global Satellite Propulsion Market Competitive Landscape and Key Players

12.1 Competitive Structure

12.2 Key Players List

1. ArianeGroup

2. Safran Spacecraft Propulsion

3. Moog Inc.

4. Northrop Grumman

5. L3Harris / Aerojet Rocketdyne

6. Busek Co.

7. Benchmark Space Systems

8. ThrustMe

9. Exotrail

10. Sitael

11. Bradford Space

12. Enpulsion

13. IHI Aerospace

14. Bellatrix Aerospace

15. Airbus Defence and Space

16. Pale Blue

17. China Aerospace Science and Technology Corporation

18. Mitsubishi Electric

19. Rafael Advanced Defence Systems

20. Israel Aerospace Industries

21. INVAP

22. Visiona Tecnologia Espacial

12.4 Company Product Mapping

12.5 Flight Heritage and Technology Positioning

12.6 Barriers to Entry

13. Global Satellite Propulsion Market Recent Developments, Policy, and Investment Opportunity

13.1 Recent Market Movements

13.2 Space Sustainability and Deorbiting Policy Impact

13.3 Defence and Government Contract Activity

13.4 Supplier Partnerships and Product Launches

13.5 High-Growth Investment Areas

13.6 Strategic Recommendations

14. Global Satellite Propulsion Market Key Findings

15. Global Satellite Propulsion Market Analyst Recommendations