SATCOM Equipment Market Size, Share, Growth Opportunities and Forecast Analysis 2032

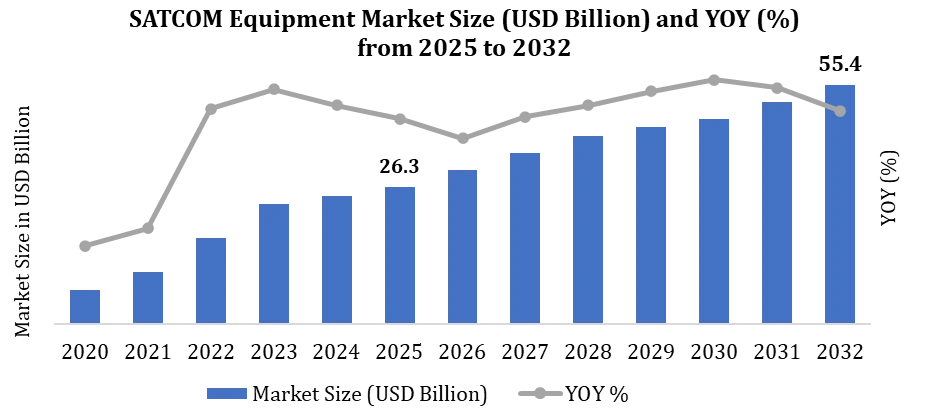

The Global SATCOM Equipment Market is valued at USD 26.3 billion in 2025 and is expected to reach USD 55.4 billion by 2032, growing at 11.2% CAGR, driven by rising demand for secure, compact, certified, and multi-network satellite communication hardware across defence, aviation, maritime, telecom backhaul, enterprise, emergency response, and remote connectivity applications.

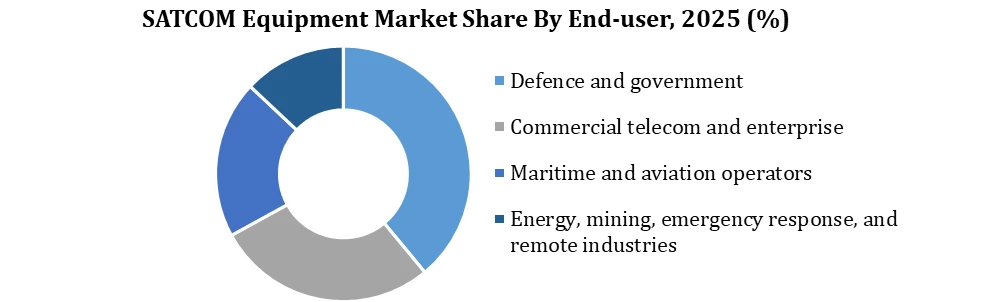

The market remains equipment-specific because customers invest directly in terminals, antennas, RF chains, modems, routers, hubs, gateways, and ground systems before they consume satellite capacity or managed connectivity. In 2025, defence and government users account for 39% of demand, followed by commercial telecom and enterprise, maritime and aviation operators, and remote industries and emergency-response users showing that hardware value comes from certified, platform-ready, and mission-specific communication systems rather than bandwidth subscriptions.

To get more Insights: Request Free Sample Report

SATCOM Equipment Market Definition and Scope

The market includes hardware used to transmit, receive, amplify, process, route, secure, and manage communication through satellite networks. It covers SATCOM terminals, VSAT terminals, flat-panel antennas, parabolic antennas, electronically steered antennas, RF systems, BUCs, LNBs, transceivers, modems, routers, network equipment, gateway hardware, ground station equipment, tactical terminals, airborne systems, maritime systems, and defence-grade communication hardware.

The market excludes satellite manufacturing, launch services, satellite bandwidth revenue, connectivity subscription revenue, managed communication services, consumer internet plans, general telecom hardware not used for SATCOM, software-only platforms, and cloud services not directly bundled with ground station equipment. This boundary keeps the SATCOM Equipment Market Size focused on hardware revenue and avoids mixing it with service-based satellite communication revenue.

SATCOM Equipment Market Dynamics

|

SATCOM Equipment Market Drivers |

SATCOM Equipment Market Restraints |

|

Rising demand for secure government and defence communication systems is driving deployment of tactical terminals, RF systems, and mobile SATCOM hardware. FCC modernization reforms and earth-station infrastructure upgrades are accelerating investments in gateways, hub systems, and RF infrastructure. |

Certification delays across aviation, maritime, and defence platforms slow commercialization and deployment timelines. High installation and integration costs for terminals, antennas, cybersecurity layers, and mounting systems limit faster adoption. |

|

SATCOM Equipment Market Opportunities |

SATCOM Equipment Market Challenges |

|

Growing adoption of compact tactical terminals and software-defined modems creates strong opportunities across defence and enterprise SATCOM networks. Europe’s IRIS² initiative and global secure-connectivity programs are increasing long-term demand for gateways, terminals, and ground infrastructure. |

Export controls, spectrum coordination issues, and cybersecurity compliance requirements increase product launch complexity. Suppliers must manage thermal performance, ruggedization, RF interference, interoperability, and power efficiency across multiple platforms. |

SATCOM Equipment Market Segmentation

SATCOM Equipment Market by Equipment Type:

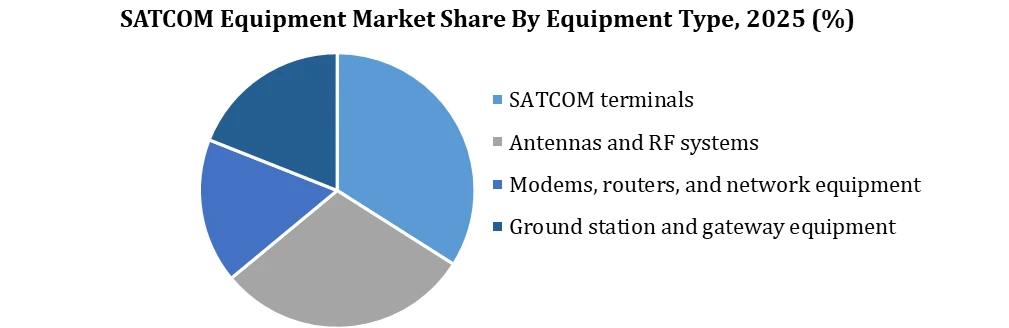

The SATCOM terminals segment leads the market with a 34% share because terminals serve as the main endpoint hardware across fixed, mobile, maritime, airborne, enterprise, and defence networks. Antennas and RF systems hold 30% as they directly control signal strength, transmission quality, and network performance through antennas, BUCs, LNBs, amplifiers, and RF chains. Ground station and gateway equipment accounts for 19% due to the high-value infrastructure needed for hubs, teleports, gateways, and ground network operations. Modems, routers, and network equipment represent 17% because they support link efficiency, data routing, traffic control, and secure SATCOM network access.

SATCOM Equipment Market by Platform

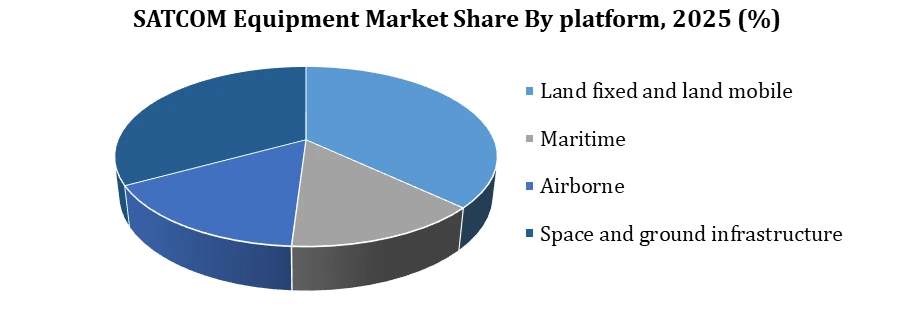

The land fixed and land mobile segment leads the Global SATCOM Equipment Market with a 37% share because fixed sites, vehicles, emergency response units, and remote operations create the widest deployment base. Space and ground infrastructure holds xx% as gateways, hubs, teleports, and mission ground systems involve high-value project equipment and network backbone investments. Airborne SATCOM accounts for xx% because aircraft systems require certified, lightweight, low-drag, and safety-compliant hardware, which increases average selling prices. Maritime represents xx% due to demand for stabilized, rugged, weather-resistant systems designed for ships, offshore assets, and marine connectivity environments.

SATCOM Equipment Market by End User

The defense and government segment leads the Global SATCOM Equipment Market with a 39% share because secure tactical, naval, airborne, and fixed government communication systems require rugged, certified, and mission-critical SATCOM equipment. Commercial telecom and enterprise accounts for xx%, supported by telecom backhaul, VSAT networks, private enterprise connectivity, and remote branch communication needs. Maritime and aviation operators hold xx% as ships and aircraft depend on higher-value, platform-specific SATCOM hardware with strict integration, safety, and retrofit requirements. Energy, mining, emergency response, and remote industries represent xx% because these users rely on satellite equipment where terrestrial networks remain weak, unavailable, or operationally unreliable.

SATCOM Equipment Market Competitive Analysis

The Global SATCOM Equipment Market remains moderately fragmented but technically specialized, with competition spread across terminals, antennas, RF systems, modems, hubs, gateways, airborne systems, maritime systems, and defence-grade communication hardware. Viasat, Hughes/EchoStar, Gilat, ST Engineering iDirect, and Comtech hold strong positions in core SATCOM networking and ground equipment, supported by terminals, VSAT platforms, modems, routers, amplifiers, RF chains, and gateway infrastructure. These companies compete on network reliability, link efficiency, installed base strength, defence compatibility, enterprise connectivity, and the ability to support GEO, LEO, MEO, and multi-orbit communication environments.

Platform-focused players such as Thales, L3Harris, RTX/Collins Aerospace, Honeywell Aerospace, Cobham Satcom, Intellian, Kymeta, ThinKom, Get SAT, CPI Satcom, AvL Technologies, and Kratos strengthen the market through specialized hardware portfolios. Their advantage lies in certified airborne systems, rugged maritime antennas, tactical terminals, mobile flat-panel solutions, transportable ground stations, and defence communication infrastructure. Competition is shifting toward compact, secure, low-profile, multi-network, and mission-ready SATCOM equipment, as customers prioritize mobility, resilience, faster deployment, and platform-specific integration over conventional single-network hardware.

Recent Developments Impacting the Global SATCOM Market.

|

Date |

Company/Organisation |

Recent Development |

Market Impact |

|

Jun-25 |

FCC (U.S.) |

Advanced earth-station licensing reforms and proposed broader blanket licensing for satellite infrastructure deployment. |

Accelerated deployment of gateways, earth stations, RF systems, and network-control equipment with lower regulatory barriers. |

|

2025 |

U.S. Space Force / DoD |

Expanded focus on interoperable SATCOM architectures capable of supporting integrated commercial and military communication systems. |

Increased demand for multi-path terminals, flexible modems, tactical SATCOM equipment, and resilient network infrastructure. |

|

Jul-25 |

Starlink, Jio-SES & Eutelsat OneWeb |

Received final approvals for commercial satellite communication service rollout in India. |

Strengthened demand for user terminals, gateways, satellite backhaul hardware, and rural connectivity infrastructure across Asia Pacific. |

|

Jun-25 |

French Government & Eutelsat |

France increased investment support for Eutelsat to strengthen Europe’s sovereign satellite communication capabilities and IRIS² participation. |

Accelerated investments in secure communication systems, sovereign satellite infrastructure, and defence-grade SATCOM networks. |

|

2025 |

Kratos Defense |

Expanded deployment of software-defined and virtualized SATCOM ground systems through OpenSpace architecture. |

Improved flexibility, interoperability, and scalability of next-generation SATCOM ground infrastructure. |

SATCOM Equipment Market Regional Analysis

North America leads the SATCOM Equipment Market with an estimated 39% regional share in 2025. The region’s development is equipment-led because the United States has a large defence SATCOM base, mature aerospace suppliers, commercial satellite operators, aviation connectivity programs, maritime communication systems, and extensive gateway infrastructure. Demand is strongest for secure terminals, airborne SATCOM hardware, tactical communication systems, gateways, RF systems, modems, and earth-station equipment.

Recent regulatory activity is strengthening the region’s equipment outlook. In 2025, the FCC proposed modernization of space and earth-station licensing, including extending most space-station and earth-station license terms to 20 years and expanding the list of modifications applicants can make without prior approval. This supports long-term investment in gateway equipment, earth-station hardware, hub systems, RF infrastructure, and network-control platforms.

Europe’s SATCOM equipment market is evolving around secure connectivity, sovereign communication infrastructure, defence modernization, and encrypted government communication systems. The region is witnessing rising demand for secure terminals, gateway systems, antennas, ground infrastructure, and network-control hardware. The EU’s IRIS² programme is becoming a major growth driver by accelerating investments in multi-orbit satellite communication systems for defence, maritime surveillance, border security, and critical infrastructure applications.

Asia Pacific is emerging as a major SATCOM growth hub due to rising rural connectivity requirements, telecom backhaul demand, maritime traffic, aviation expansion, and national satellite initiatives. India is playing a key role following satellite internet licensing approvals for Starlink, OneWeb India, and Jio Satellite Communication, increasing demand for user terminals, gateways, ground stations, and satellite backhaul equipment.

Middle East & Africa is strengthening demand for ruggedized SATCOM systems across oil & gas, defence, maritime, and remote industrial applications. South America, particularly Brazil, is witnessing growing satellite communication deployment for rural broadband, mining operations, remote-area connectivity, and emergency communication infrastructure.

|

SATCOM Equipment Market Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2025 -2032 |

|

Historical Data: |

2020 to 2024 |

Market Size in 2025: |

USD 26.3 Bn |

|

Forecast Period 2025 to 2032 CAGR: |

11.2% |

Market Size in 2032: |

USD 55.4 Bn. |

|

Segments |

By Equipment Type |

SATCOM terminals Antennas and RF systems Modems, routers, and network equipment Ground station and gateway equipment |

|

|

By End-use

|

Defence and government Commercial telecom and enterprise Maritime and aviation operators Energy, mining, emergency response, and remote industries |

||

|

By Orbit Compatibility |

GEO-only equipment LEO-compatible equipment MEO-compatible equipmen Multi-orbit equipment |

||

|

By Platform |

Land fixed and land mobile Maritime Airborne Space and ground infrastructure |

||

SATCOM Equipment Market Global Key Players:

North America

- Viasat

- Hughes Network Systems / EchoStar

- Comtech Telecommunications

- L3Harris Technologies

- Kratos Defence & Security Solutions

Europe

- Thales

- Cobham Satcom

- ND SatCom

- WORK Microwave

- SpacePath Communications

Asia-Pacific

- ST Engineering iDirect

- Intellian Technologies

- Mitsubishi Electric

- Furuno Electric

- NEC Corporation

Middle East & Africa

- Gilat Satellite Networks

- Orbit Communication Systems

- Get SAT

- ASELSAN

- CTech

Frequently Asked Questions

The SATCOM Equipment Market size is estimated at USD 26.3 billion in 2025 under a hardware-only scope. This excludes satellite bandwidth, managed services, launch services, satellite manufacturing, and consumer internet subscription revenue.

The Global SATCOM Equipment Market is forecast to reach USD 55.4 billion by 2032, growing at a CAGR of 11.2% from 2025 to 2032

The key growth drivers are defence SATCOM modernization, ground station upgrades, aviation and maritime connectivity equipment, enterprise VSAT deployment, telecom backhaul, remote-site communication, and demand for multi-orbit terminals. These drivers increase demand for antennas, terminals, modems, routers, RF equipment, and gateway systems.

SATCOM terminals hold the largest share because every satellite communication network requires endpoint hardware for user access. Antennas and RF systems also hold a major share because link quality depends on signal acquisition, amplification, frequency handling, and platform compatibility.

1. Executive Summary

1.1 Global SATCOM Equipment Market Snapshot

1.2 Market Size, Forecast, and CAGR

1.3 Key Market Findings

1.4 Demand Outlook by Equipment Type

1.5 Demand Outlook by Platform

1.6 Demand Outlook by Region

1.7 Strategic Implications for SATCOM Equipment Suppliers

2. Research Scope and Market Definition

2.1 SATCOM Equipment Market Definition

2.2 Inclusions and Exclusions

2.3 Hardware Scope: Terminals, Antennas, RF Systems, Modems, Routers, Gateways, and Ground Stations

2.4 Difference Between SATCOM Equipment and SATCOM Services

2.5 Difference Between Satellite Communication Equipment and Satellite Bandwidth Revenue

2.6 Base Year, Historical Period, and Forecast Period

2.7 Currency, Units, and Assumption Framework

3. Research Methodology

3.1 Primary Research Framework

3.2 Secondary Research Validation

3.3 Bottom-Up Market Sizing Approach

3.4 Top-Down Triangulation Approach

3.5 Demand Block Identification

3.6 Installed Base Estimation

3.7 New Deployment Estimation

3.8 Equipment ASP Modelling

3.9 Replacement and Upgrade Factor Calculation

3.10 Company Revenue Triangulation

3.11 Regional Share Validation

3.12 Segment Share Validation

3.13 CAGR and Forecast Audit

3.14 Data Reliability and Confidence Scoring

4. Market Engineering and Size Estimation

4.1 Global SATCOM Equipment Market Size, 2025

4.2 Global SATCOM Equipment Market Forecast, 2032

4.3 SATCOM Equipment Market CAGR, 2025–2032

4.4 Market Size by Demand Block

4.5 Defence and Government SATCOM Equipment Market Size

4.6 Commercial VSAT and Enterprise SATCOM Hardware Market Size

4.7 Maritime SATCOM Equipment Market Size

4.8 Airborne SATCOM Equipment Market Size

4.9 Land-Mobile and Remote-Site SATCOM Equipment Market Size

4.10 Ground Station and Gateway Equipment Market Size

4.11 Telecom Backhaul SATCOM Equipment Market Size

4.12 Tactical and Secure SATCOM Equipment Market Size

4.13 Replacement and Modernization Demand Analysis

4.14 Market Size Audit and Sensitivity Check

5. Historical Market Analysis, 2020–2024

5.1 Global SATCOM Equipment Market Historical Size

5.2 Year-on-Year Growth Analysis

5.3 COVID-19 and Supply Chain Impact

5.4 Aviation SATCOM Equipment Recovery

5.5 Maritime SATCOM Hardware Adoption

5.6 Defence SATCOM Procurement Movement

5.7 Enterprise VSAT Hardware Demand

5.8 Ground Station and Gateway Expansion

5.9 Historical Company Revenue Indicators

5.10 Historical Market Movement Summary

6. Forecast Analysis, 2025–2032

6.1 Global SATCOM Equipment Market Forecast

6.2 Year-on-Year Forecast Movement

6.3 Forecast Assumption Framework

6.4 Multi-Orbit SATCOM Equipment Outlook

6.5 Flat-Panel Antenna Adoption Outlook

6.6 Electronically Steered Antenna Outlook

6.7 Software-Defined Modem Outlook

6.8 Ground Infrastructure Modernization Outlook

6.9 Defence and Tactical SATCOM Forecast

6.10 Aviation and Maritime SATCOM Equipment Forecast

6.11 Forecast Risk and Scenario Review

6.12 CAGR Calculation and Verification

7. Market Overview

7.1 Role of SATCOM Equipment in Satellite Communication Networks

7.2 Hardware Revenue vs. Service Revenue

7.3 SATCOM Terminals Market Overview

7.4 SATCOM Antenna Market Overview

7.5 SATCOM RF Systems Market Overview

7.6 SATCOM Modems and Routers Market Overview

7.7 Gateway and Ground Station Equipment Overview

7.8 Application Role Across Defence, Aviation, Maritime, Telecom, Enterprise, and Remote Industries

8. Market Dynamics

8.1 Market Growth Drivers

8.1.1 Defence SATCOM Equipment Modernization

8.1.2 Ground Station and Gateway Infrastructure Upgrades

8.1.3 Maritime and Airborne SATCOM Equipment Demand

8.1.4 Enterprise VSAT and Telecom Backhaul Deployment

8.1.5 Multi-Orbit Terminal Readiness

8.2 Market Restraints

8.2.1 High Equipment and Integration Cost

8.2.2 Certification and Platform Approval Delays

8.2.3 Spectrum Coordination Constraints

8.2.4 Export Control and Security Compliance Burden

8.2.5 Procurement Cycle Volatility

8.3 Market Opportunities

8.3.1 Compact Tactical SATCOM Terminals

8.3.2 Software-Defined SATCOM Modems

8.3.3 Electronically Steered Antenna Systems

8.3.4 Cloud-Connected Ground Infrastructure

8.3.5 Satellite-Cellular Convergence Hardware

8.4 Market Challenges

8.4.1 Thermal Management and Power Consumption

8.4.2 Interoperability Across Satellite Networks

8.4.3 Cybersecurity Requirements

8.4.4 Hardware Miniaturization Pressure

8.4.5 Field Reliability in Harsh Environments

9. Market Trends

9.1 Multi-Orbit SATCOM Equipment

9.2 LEO-Compatible SATCOM Terminals

9.3 Flat-Panel SATCOM Antennas

9.4 Electronically Steered Antennas

9.5 Software-Defined Modems

9.6 AI-Enabled Network Management Equipment

9.7 Cloud-Connected Ground Stations

9.8 Tactical Portable SATCOM Systems

9.9 Satellite-Cellular Convergence Hardware

9.10 Interoperable Terminals Across GEO, MEO, and LEO Networks

10. Market Segmentation

10.1 Global SATCOM Equipment Market by Equipment Type

10.1.1 SATCOM Terminals

10.1.2 Antennas and RF Systems

10.1.3 Modems, Routers, and Network Equipment

10.1.4 Ground Station and Gateway Equipment

10.2 Global SATCOM Equipment Market by Platform

10.2.1 Land Fixed and Land Mobile

10.2.2 Maritime

10.2.3 Airborne

10.2.4 Space and Ground Infrastructure

10.3 Global SATCOM Equipment Market by End User

10.3.1 Defence and Government

10.3.2 Commercial Telecom and Enterprise

10.3.3 Maritime and Aviation Operators

10.3.4 Energy, Mining, Emergency Response, and Remote Industries

10.4 Global SATCOM Equipment Market by Orbit Compatibility

10.4.1 GEO-Only Equipment

10.4.2 LEO-Compatible Equipment

10.4.3 MEO-Compatible Equipment

10.4.4 Multi-Orbit Equipment

10.5 Segment Share Comparison

10.6 Segment Growth Attractiveness Matrix

10.7 Segment-Level Investment Opportunity

11. Regional Analysis

11.1 Global Regional Snapshot

11.2 North America SATCOM Equipment Market

11.2.1 United States

11.2.2 Canada

11.2.3 Mexico

11.2.4 Defence SATCOM Equipment Demand

11.2.5 Aviation and Ground Infrastructure Demand

11.3 Europe SATCOM Equipment Market

11.3.1 Germany

11.3.2 France

11.3.3 United Kingdom

11.3.4 Italy

11.3.5 Spain

11.3.6 Secure Connectivity and Sovereign SATCOM Programs

11.4 Asia Pacific SATCOM Equipment Market

11.4.1 China

11.4.2 India

11.4.3 Japan

11.4.4 South Korea

11.4.5 Australia

11.4.6 Southeast Asia

11.4.7 Telecom Backhaul and Remote Connectivity Demand

11.5 Middle East and Africa SATCOM Equipment Market

11.5.1 GCC Countries

11.5.2 Israel

11.5.3 Turkey

11.5.4 South Africa

11.5.5 Rest of Middle East and Africa

11.5.6 Defence, Oil and Gas, Maritime, and Remote-Site Demand

11.6 South America SATCOM Equipment Market

11.6.1 Brazil

11.6.2 Argentina

11.6.3 Chile

11.6.4 Colombia

11.6.5 Rest of South America

11.6.6 Mining, Remote Connectivity, and Telecom Backhaul Demand

11.7 Regional Share Analysis

11.8 Regional Growth Opportunity Ranking

11.9 Regional Risk Assessment

12. Competitive Landscape

12.1 Competitive Overview

12.2 Market Concentration Analysis

12.3 Global Top SATCOM Equipment Companies

12.4 Regional SATCOM Equipment Companies

12.5 Company Positioning by Equipment Type

12.6 Company Positioning by Platform

12.7 Company Positioning by End User

12.8 Competitive Benchmarking Matrix

12.9 Product Portfolio Comparison

12.10 Recent Company Developments

12.11 Strategic Partnerships and Contracts

12.12 Mergers, Acquisitions, and Investments

12.13 Competitive Gaps and White Space

13. Company Profiles

13.1 Viasat

13.2 Hughes Network Systems / EchoStar

13.3 ST Engineering iDirect

13.4 Comtech Telecommunications

13.5 Thales

13.6 L3Harris Technologies

13.7 RTX / Collins Aerospace

13.8 Honeywell Aerospace

13.9 Cobham Satcom

13.10 Intellian Technologies

13.11 Gilat Satellite Networks

13.12 Kymeta

13.13 ThinKom Solutions

13.14 CPI Satcom & Antenna Technologies

13.15 Kratos Defence & Security Solutions

Each company profile should include: Company Overview, SATCOM Equipment Portfolio, Target Platforms, End-User Focus, Geographic Presence, Recent Developments, Strategic Positioning, and Analyst View.

14. Recent Developments and Market Movements

14.1 Defence SATCOM Equipment Contracts

14.2 Ground Station and Gateway Modernization

14.3 Multi-Orbit Terminal Launches

14.4 Flat-Panel Antenna Product Developments

14.5 Maritime SATCOM Equipment Upgrades

14.6 Airborne SATCOM Hardware Developments

14.7 Satellite Broadband Equipment Deployments

14.8 Regulatory Developments Affecting SATCOM Equipment

14.9 Government Connectivity Programs

14.10 Strategic Partnerships and Product Integrations

15. Technology Analysis

15.1 SATCOM Terminal Architecture

15.2 Antenna Technology Evolution

15.3 RF Chain and Amplifier Technology

15.4 Modem and Router Technology

15.5 Gateway and Ground Station Architecture

15.6 Software-Defined SATCOM Hardware

15.7 Cybersecure SATCOM Equipment

15.8 Low-Power and Compact SATCOM Systems

15.9 Ruggedized Defence SATCOM Equipment

15.10 Future Technology Roadmap

16. Value Chain Analysis

16.1 Component Suppliers

16.2 RF and Antenna Manufacturers

16.3 Terminal Manufacturers

16.4 Modem and Network Equipment Suppliers

16.5 Gateway and Ground Infrastructure Providers

16.6 System Integrators

16.7 Satellite Operators

16.8 Defence and Commercial End Users

16.9 Aftermarket, Replacement, and Upgrade Channels

17. Pricing and ASP Analysis

17.1 SATCOM Terminal ASP

17.2 Maritime SATCOM Equipment ASP

17.3 Airborne SATCOM Equipment ASP

17.4 Tactical SATCOM Terminal ASP

17.5 Ground Station Equipment ASP

17.6 Modem and Router ASP

17.7 Antenna and RF System ASP

17.8 ASP Movement by Technology Type

17.9 ASP Pressure and Margin Impact

18. Supply-Side Analysis

18.1 Manufacturing Footprint

18.2 Component Availability

18.3 Semiconductor and RF Component Dependency

18.4 Antenna Manufacturing Capacity

18.5 Defence-Grade Equipment Production Constraints

18.6 Certification and Testing Capacity

18.7 Supplier Risk Analysis

18.8 Supply Chain Resilience

19. Demand-Side Analysis

19.1 Defence and Government Demand

19.2 Commercial Telecom Demand

19.3 Enterprise VSAT Demand

19.4 Maritime Operator Demand

19.5 Aviation Operator Demand

19.6 Energy and Mining Demand

19.7 Emergency Response Demand

19.8 Remote Community Connectivity Demand

19.9 Replacement and Upgrade Demand

20. Investment Opportunity Analysis

20.1 High-Growth Equipment Categories

20.2 High-Margin SATCOM Hardware Segments

20.3 Regional Investment Attractiveness

20.4 Defence and Secure Communication Opportunity

20.5 Ground Infrastructure Investment Opportunity

20.6 Aviation and Maritime Retrofit Opportunity

20.7 Multi-Orbit Terminal Opportunity

20.8 Emerging Market Connectivity Opportunity

20.9 Strategic Recommendations for Investors and Suppliers

21. Risk Analysis

21.1 Technology Risk

21.2 Certification Risk

21.3 Regulatory Risk

21.4 Export Control Risk

21.5 Procurement Risk

21.6 Supply Chain Risk

21.7 Pricing Risk

21.8 Competition Risk

21.9 Forecast Risk

22. Analyst Recommendations

22.1 Recommendations for SATCOM Equipment Manufacturers

22.2 Recommendations for Antenna and RF Suppliers

22.3 Recommendations for Ground Infrastructure Providers

22.4 Recommendations for Defence SATCOM Suppliers

22.5 Recommendations for Investors

22.6 Recommendations for New Entrants

22.7 Strategic Priorities Through 2032

23. Conclusion

23.1 Final Market Outlook

23.2 Key Growth Areas

23.3 Long-Term Equipment Demand View

23.4 Final Analyst Perspective