Smart Grid & Infrastructure Digitization Market: Renewable Integration, Grid Automation & Digital Utility Transformation (2026–2032)

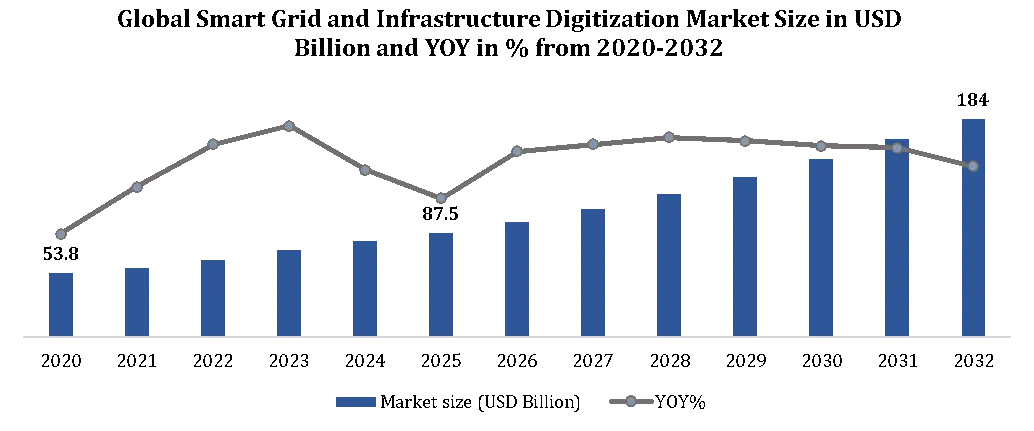

The Smart Grid and Infrastructure Digitization Market was estimated at USD 87.5 billion in 2025 and is estimated to be valued at USD 184.0 billion by 2032, developing at an 11.2% CAGR. The biggest contributor is the absolute need to manage solar and wind variability, DERs, storage, EV charging, and two-way power flows via digital grid systems.

Global Smart Grid and Infrastructure Digitization Market Overview

The Global Smart Grid and Infrastructure Digitization Market refers to the deployment of advanced digital technologies such as smart meters, AI-powered grid analytics, IoT sensors, digital substations, cloud-based energy management systems, and automated transmission infrastructure to modernize conventional electricity networks. These intelligent grid ecosystems enable utilities and infrastructure operators to improve energy efficiency, real-time monitoring, predictive maintenance, renewable energy integration, and grid reliability across industrial, commercial, and residential sectors.

The market is witnessing strong growth due to rising investments in renewable energy infrastructure, increasing electricity demand, rapid EV charging network expansion, and government-led smart city initiatives. Utilities are increasingly adopting intelligent grid automation systems to reduce transmission losses, optimize power distribution, strengthen energy resilience, and support decentralized energy ecosystems.

North America currently leads the market because of advanced grid modernization programs, large-scale deployment of smart meters, strong regulatory support, and high investments in digital energy infrastructure across the United States and Canada. The U.S. remains the leading country due to significant investments in smart transmission systems, AI-enabled utility management, and renewable grid integration projects.

By component, software and grid automation platforms dominate the market due to increasing adoption of AI-driven energy analytics and cloud-based grid management solutions. By application, smart transmission and distribution infrastructure holds the largest share. Key players operating in the market include Siemens, Schneider Electric, ABB, General Electric, Hitachi Energy, Cisco Systems, Honeywell, Eaton, IBM, and Itron.

To get more Insights: Request Free Sample Report

Global Smart Grid and Infrastructure Digitization Market Dynamics

Heavy renewable power systems are forcing utilities to operate the grid with more precision than ever before. Recurrent output, over-roof supply, storage dispatch, and charging loads changing electricity flows throughout the day, so utilities must move on from regular reviews to real-time analytics. This is forcing investors toward digital/smart meters, feeder automation, smart substations, control-room software, secure data networks, and grid-edge analytics that help operators detect stress, balance supply, manage voltage, and respond instantly to defects.

Demand and implementations are the primary constraints. Large-scale deployment was challenging because utilities primarily use outdated technology, have slow clearance periods, minimal digital competency, and stringent cybersecurity regulations. As the use of renewable energy increases, vendors who link new platforms with current grid systems, lower integration risk, and facilitate DER coordination, EV load management, predictive maintenance, and resilience planning will have more opportunities.

Global Smart Grid and Infrastructure Digitization Market Drivers

Requirements for real-time grid visibility are being created by renewable energy. As solar and wind output fluctuate throughout the day, utilities require quicker visibility into voltage, congestion, power quality, and load behaviour.

Digitization is being pushed further into distribution networks by distributed energy resources (DERs). AMI, DERMS, feeder sensors, and local control systems are necessary for rooftop solar, batteries, EV chargers, and prosumers.

As the use of renewable energy sources increases, grid automation is becoming more and more valuable. Utilities may manage variable generation without sacrificing dependability with the aid of automated switching, fault detection, outage response, and voltage control.

Software-led control is replacing hardware-only enhancements in smart grid spending thanks to renewable integration. Utilities can coordinate renewable-heavy networks in real time with the aid of ADMS, DERMS, forecasting tools, and AI-based analytics.

Global Smart Grid and Infrastructure Digitization Market Restraints

Adoption is slowed by high upfront costs. Before benefits completely materialize, utilities must finance smart meters, sensors, communication networks, software platforms, cybersecurity systems, and field integration.

Digital preparedness is constrained by legacy grid infrastructure. Before modern automation can function well, older feeders, substations, protection systems, and control rooms frequently need to be redesigned.

With connected grid assets, cybersecurity susceptibility rises. The utility attack surface is increased by smart meters, sensors, controllers, DER platforms, and communication networks.

Deployment is delayed by governmental approvals and utility procurement processes. Before recovering digital-grid investments through tariffs, regulated utilities frequently require lengthy approval periods.

Global Smart Grid and Infrastructure Digitization Market Opportunities

DERMS generates a high-value software opportunity. In order to monitor and manage distributed solar, batteries, EVs, flexible loads, and virtual power plants (VPPs), utilities require DERMS platforms.

Mission-critical grid communication can be supported via private wireless networks. For automation, sensors, substations, and field equipment, utilities require low-latency, secure networks.

AI-based asset monitoring can lower the risk of maintenance failures and outages. Before service breakdowns are caused by grid fluctuation from renewable energy, predictive analytics can identify equipment stress.

A new control layer is made possible by EV-grid integration. Fleet electrification, charging load management, and bidirectional charging require smart coordination between utilities, charging operators, and grid software platforms.

Global Smart Grid and Infrastructure Digitization Market Challenges

Most power systems were originally designed around centralized generation and one-way electricity flow, which creates a major execution gap for utilities moving toward cleaner and more flexible grids. To support renewable energy integration, utilities need faster grid control, stronger forecasting, better system interoperability, and deeper distribution-level visibility. However, many existing substations, feeders, and control systems are not ready for this shift without major infrastructure upgrades. The market also faces barriers such as procurement delays, cybersecurity risks, data integration challenges, vendor lock-in, regulatory approval delays, and a shortage of engineers skilled in both digital platforms and power systems. Even though the value of renewable integration and smart grid digitization is clear, these challenges continue to slow wider market adoption.

Global Smart Grid and Infrastructure Market Segmentation:

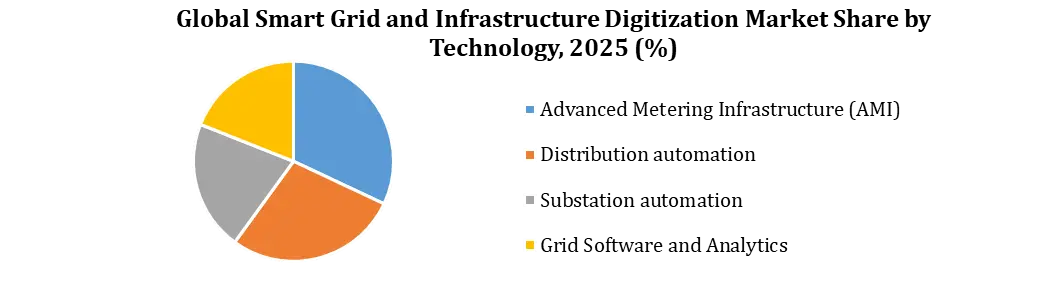

Global Smart Grid and Infrastructure Digitization Market Size and Share by Technology

Advanced Metering Infrastructure (AMI) leads the Smart Grid and Infrastructure Digitization market with a 32% share, supported by its growing role in prosumer billing, demand response, and stronger grid visibility. Distribution automation driven by the rising need for voltage control, fault response, and remote switching in networks with higher levels of renewable energy. Substation automation, as digital substations improve protection, monitoring, and control across both transmission and distribution systems. Grid software and analytics, including EMS, ADMS, and DERMS, which help utilities manage renewable integration and distributed energy assets in real time.

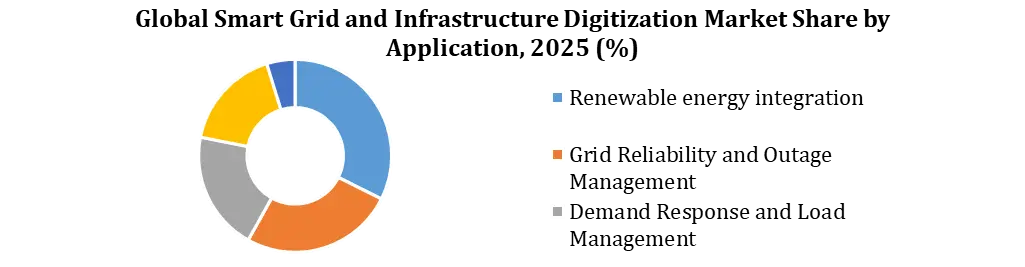

Global Smart Grid and Infrastructure Digitization Market Size and Share by Application:

Renewable energy integration leads the market with a 34% share in 2025, driven by the growing use of solar power, wind power, storage systems, DERs, and electric vehicles. These technologies are increasing the need for stronger grid visibility and control.

Grid reliability and outage management follows as utilities work to improve automation and outage response while managing rising risks from weather disruptions and power variability. Demand response and load management is supported by advanced metering infrastructure and software solutions that help utilities manage peak demand and encourage more flexible energy use. Asset monitoring and predictive maintenance also hold a significant share, where utilities use sensors, data analytics, and performance insights to improve the reliability of ageing grid infrastructure.

Global Smart Grid and Infrastructure Digitization Market Size and Share By End-Use

Distribution utilities hold the highest share of the market at 48%, owing to the increasing use of rooftop solar PV, EV charging, smart metering, and feeder automation technologies. Transmission utilities supported by growing investments in digital substations, grid monitoring systems, and wide-area network visibility.

Renewable energy firms driven by the increasing need for renewable forecasting, battery management systems, and distributed energy coordination solutions. Industrial and commercial power user’s Large users deploy demand response, energy management, and grid-interactive systems.

Smart Grid and Infrastructure Digitization Market Regional Analysis

The Global Smart Grid and Infrastructure Digitisation Market is witnessing strong growth across major regions, driven by renewable energy integration, rising electricity demand, EV adoption, and the need for reliable and flexible power grids.

Asia Pacific Smart Grid and Infrastructure Digitisation Market holds the largest market share in 2025, supported by rapid renewable energy expansion, rising electricity consumption, EV adoption, and network growth. China, India, Japan, Australia, and Southeast Asian countries are investing heavily in smart meters, distribution automation, grid communication, and renewable integration technologies. North America Smart Grid and Infrastructure Digitisation Market is growing rapidly as utilities in the U.S. and Canada invest in DERMS, advanced metering, cybersecurity, automation platforms, digital substations, grid software, and communication infrastructure to improve reliability and manage renewables, EV charging, and distributed energy resources.

Europe Smart Grid and Infrastructure Digitisation Market is expected to generate significant revenue due to its focus on renewables, grid flexibility, interconnection, and digital network planning. Utilities and transmission system operators are expanding smart meters, automation systems, digital substations, and flexibility platforms to support wind and solar integration.

The Middle East and Africa are still at an early stage but show strong potential through smart city projects, solar parks, renewable energy investments, and utility modernization, creating demand for digital monitoring, automation, smart metering, and control technologies. South America is growing gradually, supported by renewable generation, hydropower balancing, outage reduction, and distribution efficiency needs. Brazil and Chile are driving demand for grid automation, smart metering, asset monitoring, and software-based network management, though adoption remains slower than in Asia Pacific and North America.

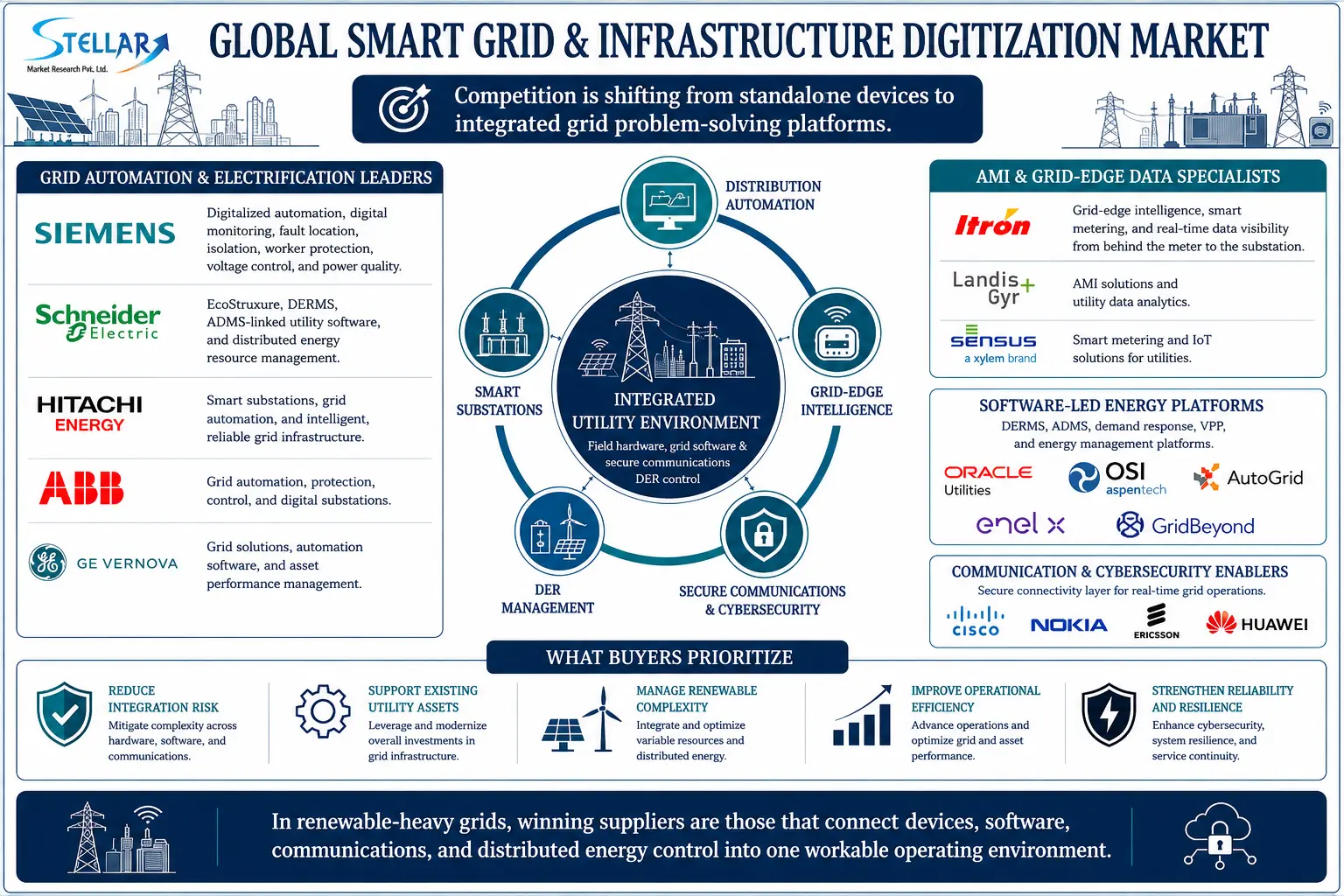

Global Smart Grid and Infrastructure Digitization Market Competitive Landscape

Competition in the market is shifting toward companies that can provide integrated grid solutions instead of standalone hardware. Siemens, Schneider Electric, ABB, GE Vernova, and Hitachi Energy are strengthening their positions through grid automation, smart substations, and renewable integration technologies.

Companies such as Itron, Landis+Gyr, and Sensus focus on smart metering and grid-edge visibility, while software providers including Oracle Utilities, AspenTech, AutoGrid, and Enel X compete through DERMS, ADMS, and virtual power plant solutions.

Communication and cybersecurity providers such as Cisco, Nokia, Ericsson, and Huawei support the connectivity layer required for real-time grid operations. Vendors that reduce integration complexity and improve renewable energy management are expected to gain a stronger competitive advantage.

Global Smart Grid and Infrastructure Digitization Market Ecosystem

Global Smart Grid and Infrastructure Digitization Market Recent Developments

|

Company |

Year |

Recent Development |

Strategic Impact |

|

Oracle Utilities |

2025 |

Expanded ADMS capabilities to support DER integration, renewable forecasting, and grid flexibility management. |

Strengthened utility demand for AI-enabled grid visibility and real-time network optimization. |

|

Siemens |

2025 |

Expanded digital substation and grid automation offerings integrated with AI-enabled monitoring systems. |

Strengthened position in renewable integration and intelligent utility infrastructure. |

|

Schneider Electric |

2025 |

Enhanced EcoStruxure Grid platform for utility digitization and DER management. |

Improved distributed energy visibility and grid resilience capabilities. |

|

ABB |

2025 |

Increased investments in digital substations, grid-edge intelligence, and EV-grid integration technologies. |

Supported renewable-heavy grid management and utility modernization. |

|

Hitachi Energy |

2026 |

Expanded grid automation and renewable integration technologies including HVDC systems. |

Strengthened renewable power transmission and smart grid digitization capabilities. |

|

Cisco |

2026 |

Expanded utility-focused cybersecurity and grid communication infrastructure solutions. |

Enhanced secure real-time grid operations and OT cybersecurity capabilities. |

|

GE Vernova |

2026 |

Expanded grid modernization portfolio focused on renewable integration and transmission digitization. |

Strengthened utility operational optimization and renewable grid management. |

|

Mitsubishi Electric |

2026 |

Expanded investments in smart substations and digital transmission systems in Asia Pacific. |

Accelerated regional grid modernization and renewable integration development. |

|

Global Smart Grid and Infrastructure Digitization Market |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2032 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 87.5 Bn. |

|

Forecast Period 2025 to 2032 CAGR: |

11.2% |

Market Size in 2032: |

USD 184 Bn. |

|

Segments

|

By Component |

Hardware Software Services |

|

|

By Grid Type |

Smart Transmission Systems Smart Distribution Systems Microgrids Virtual Power Plants (VPP) |

||

|

By Technology

|

Advanced Metering Infrastructure Distribution Automation Substation Automation Grid Software and Analytics |

||

|

By Application |

Renewable Energy Integration Grid Reliability and Outage Management Demand Response and Load Management Asset Monitoring and Predictive Maintenance Others |

||

|

By Deployment Mode |

On-Premise Cloud-Based |

||

|

By End User |

Transmission Utilities Distribution Utilities Renewable Energy Operators Industrial and Commercial Power Users Others |

||

Smart Grid and Infrastructure Digitisation Market Key Players Covered in the Report

- Siemens

- Schneider Electric

- ABB

- GE Vernova

- Hitachi Energy

- Eaton

- Honeywell

- Itron

- Landis+Gyr

- Xylem (Sensus)

- Oracle Utilities

- Cisco Systems

- Nokia

- Ericsson

- Huawei

- Toshiba Energy Systems & Solutions

- Mitsubishi Electric

- Schweitzer Engineering Laboratories (SEL)

- AspenTech OSI

- Trilliant

- Kamstrup

- AutoGrid Systems

- Wipro

- Gridspertise

- Hexing Electrical

- Fuji Electric

- Toshiba Infrastructure Systems

- WEG

- Minsait (Indra Group)

- S&C Electric Company

Frequently Asked Questions

Renewable energy integration increases demand for smart grid technologies because solar power, wind energy, battery storage, EV charging, and distributed energy resources make electricity networks more variable and decentralized. Utilities require digital systems to improve grid visibility, balance supply and demand, manage voltage, and control renewable-heavy power flows.

The Global Smart Grid & Infrastructure Digitization Market Gains from Renewable Energy Integration is estimated at USD 87.5 billion in 2025, driven by growing investments in AMI, grid automation, digital substations, DERMS, utility communication systems, and cybersecurity.

The market is projected to reach USD 184.0 billion by 2032, growing at a CAGR of 11.2% from 2025 to 2032. Growth is supported by increasing adoption of distribution automation, ADMS, DERMS, digital substations, and renewable integration technologies.

Hardware holds the largest market share at 37%, supported by strong utility investments in smart meters, grid sensors, PMUs, automation systems, and field devices that form the foundation of digital grid infrastructure.

1. Global Smart Grid and Infrastructure Digitization Market: Introduction

1.1 Market Definition

1.2 Market Scope and Coverage

1.3 Smart Grid Ecosystem Overview

1.4 Industry Value Chain Analysis

1.5 Research Assumptions and Limitations

2. Global Smart Grid and Infrastructure Digitization Market: Executive Summary

2.1 Market Snapshot, 2025 and 2032

2.2 Global Market Size and Forecast (USD Billion)

2.3 Key Market Highlights

2.4 Market Segmentation Overview

2.5 Renewable Energy Integration as a Core Growth Driver

2.6 Strategic Outlook for Utilities, Grid Operators, and Technology Providers

3. Global Smart Grid and Infrastructure Digitization Market: Research Methodology

3.1 Data Mining

3.2 Secondary Research

3.3 Primary Research

3.4 Subject Matter Expert Advice

3.5 Quality Check

3.6 Final Review

3.7 Data Triangulation

3.8 Top-Down Approach

3.9 Bottom-Up Approach

3.10 Forecast Modeling

3.11 Data Sources

4. Global Smart Grid and Infrastructure Digitization Market: Market Attractiveness Mapping

4.1 Global Market Overview

4.2 Competitive Analysis: Tier 1, Tier 2, and Tier 3 Players

4.3 Absolute Market Opportunity Analysis

4.4 Market Attractiveness Analysis, By Component

4.5 Market Attractiveness Analysis, By Grid Type

4.6 Market Attractiveness Analysis, By Technology

4.7 Market Attractiveness Analysis, By Application

4.8 Market Attractiveness Analysis, By Deployment Mode

4.9 Market Attractiveness Analysis, By End User

4.10 Regional Market Attractiveness Analysis

4.11 Future Market Opportunities

5. Global Smart Grid and Infrastructure Digitization Market: Market Outlook

5.1 Market Evolution and Industry Transition

5.2 Market Outlook

5.3 Market Drivers

5.4 Market Restraints

5.5 Market Opportunities

5.6 Market Challenges

5.7 Market Trends

5.8 PORTER’s Five Forces Analysis

5.8.1 Threat of New Entrants

5.8.2 Bargaining Power of Suppliers

5.8.3 Bargaining Power of Buyers

5.8.4 Threat of Substitute Products

5.8.5 Competitive Rivalry

5.9 Value Chain Analysis

5.10 Pricing and Cost Structure Analysis

5.11 Smart Grid Infrastructure Investment Analysis

5.12 Renewable Energy Integration Impact Analysis

5.13 Grid Modernization and Utility Digitization Analysis

5.14 Regulatory Standards and Policy Landscape

5.15 Green Grid and Sustainability Analysis

5.16 Technology Analysis

6. Global Smart Grid and Infrastructure Digitization Market: By Component

7. Global Smart Grid and Infrastructure Digitization Market: By Grid Type

8. Global Smart Grid and Infrastructure Digitization Market: By Technology

9. Global Smart Grid and Infrastructure Digitization Market: By Application

10. Global Smart Grid and Infrastructure Digitization Market: By Deployment Mode

11. Global Smart Grid and Infrastructure Digitization Market: By End User

12. Global Smart Grid and Infrastructure Digitization Market: Geography

12.1 North America Smart Grid and Infrastructure Digitization Market Size by Segments and Country (US billion) from 2025-2032

12.2 Europe Smart Grid and Infrastructure Digitization Market by Segments and Country (US billion) from 2025-2032

12.3 Asia Pacific Smart Grid and Infrastructure Digitization Market by Segments and Country (US billion) from 2025-2032

12.4 South America Smart Grid and Infrastructure Digitization Market by Segments and Country (US billion) from 2025-2032

12.5 Middle East and Africa Smart Grid and Infrastructure Digitization Market by Segments and Country (US billion) from 2025-2032

13. Global Smart Grid and Infrastructure Digitization Market: Competitive Landscape

13.1 Company Positioning Matrix

13.2 Product Portfolio Comparison

13.3 Market Share and Revenue Analysis

13.4 Strategic Partnerships and Collaborations

13.5 Mergers & Acquisitions

13.6 Recent Developments and Product Launches

14. Key Companies Profiled in the Global Smart Grid and Infrastructure Digitization Market

1. Siemens

2. Schneider Electric

3. ABB

4. GE Vernova

5. Hitachi Energy

6. Eaton

7. Honeywell

8. Itron

9. Landis+Gyr

10. Xylem (Sensus)

11. Oracle Utilities

12. Cisco Systems

13. Nokia

14. Ericsson

15. Huawei

16. Toshiba Energy Systems & Solutions

17. Mitsubishi Electric

18. Schweitzer Engineering Laboratories (SEL)

19. AspenTech OSI

20. Trilliant

21. Kamstrup

22. AutoGrid Systems

23. Wipro

24. Gridspertise

25. Hexing Electrical

26. Fuji Electric

27. Toshiba Infrastructure Systems

28. WEG

29. Minsait (Indra Group)

30. S&C Electric Company

15. Global Smart Grid and Infrastructure Digitization Market: Recent Developments

15.1 Smart Grid Technology Developments

15.2 Renewable Integration and Grid Flexibility Developments

15.3 Government Grid Modernization Programs

15.4 Utility Smart Meter and AMI Contracts

15.5 DERMS and ADMS Platform Launches

15.6 Digital Substation and Distribution Automation Projects

15.7 Grid Cybersecurity and Private Utility Network Developments

15.8 EV-Grid Integration and Energy Storage Coordination Programs

16. Global Smart Grid and Infrastructure Digitization Market: Investment and Demand Outlook

16.1 Utility Capex Shift Toward Digital Grid Infrastructure

16.2 Renewable Integration as a Smart Grid Investment Multiplier

16.3 Software-Led Growth in DERMS, ADMS, and Grid Analytics

16.4 Long-Term Demand for AMI, Automation, Communication Networks, and Cybersecurity

16.5 Strategic Outlook, 2025–2032

17. Global Smart Grid and Infrastructure Digitization Market Key Findings