Shortening Market Size, Share, Growth Trends, Industry Analysis, Key Players, Investment Opportunities and Forecast (2026-2032)

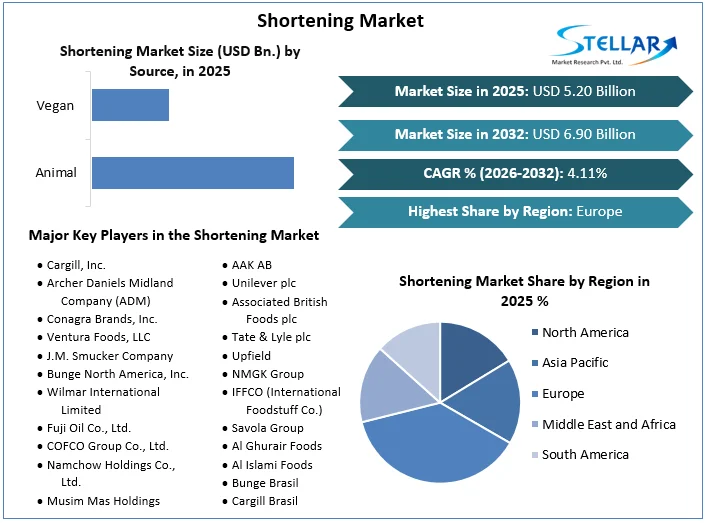

Shortening Market was valued at USD 5.20 Bn in 2025, and the total revenue is expected to grow at a CAGR of 4.11% from 2026 to 2032, reaching nearly 6.90 Bn by 2032.

Shortening Market overview:

The idea of shortening dates back to at least the 18th century, well before the invention of modern, shelf-stable vegetable shortening. These are ingredients that help in adding texture and crispiness to the various bakery and confectionery items. Also, some of the common shortening products are vegetable oils or hydrogenated vegetable oils such as palm or coconut oils. Shortening has an interesting processing method that allows it to be made from either animal-based sources or vegan sources. Lard, on the other hand, is completely obtained from the fatty tissue of a pig, while tallow, another shortening product, is obtained from cattle or sheep. Shortening products, just like starch, are an important baking ingredient as they elongate the feeling of crispiness and flakiness in longer solid fat confectioneries.

Bakers and Confectioners add monoglycerides to reduce the water-oil interfacial tension, thereby helping in making various bread and buns. The governing application, Bakery, has been growing at a rapid pace thereby supplementing the growth along with the uprising of a robust working-class supplemented by growing urbanization across the globe and acting as key drivers for the Shortening Industry in the projected period of 2026-2032.

The Shortening Market is driven by fast technological advancements and changing consumer preferences. The influence of social media and intense global competition gives the result. Companies are forced to innovate quickly and adapt the market changes frequently, and manage shorter product lifecycles. Also, businesses must adopt agile marketing and flexible production responses to the strategic environment of the company.

Key industry leaders in the market for shortening are Cargill, ADM, Bunge, Wilmar International, and AAK AB. All of these are working to promote sustainable sourcing, clean-label formulations, and tailored product formats to satisfy changing consumer demand and regulatory requirements

To get more Insights: Request Free Sample Report

Shortening Market Dynamics:

Rising Demand for Processed Foods to Drive Shortening Market

From the Need fullfilment to Want Fullfillment there has been increase the demand for processed food coupled with a rise of urbanisation and a shift in consumer lifestyle. One of the predominant reasons for the same is the availability of the internet across the world, especially the rising data consumption patterns from low-and middle-income countries that have aided the overall demand. As per the latest report from TRAI, the internet users are bound to touch 0.9 billion by 2025, from earlier 0.622 billion in 2022 to 2024 The following results in an increase of 45% for the next 5 years. Retail giants have noted a surge in bakery-related items from the tier-2 and 3 cities, particularly about bakery items owing to their availability of the internet and mobile payments. Owing to such reasons, the overall market is positioned favourably.

Innovations And Advanced Technology in the Food Industry to Boost Shortening Market

The advancement of food technology is driving the Shortening Market Industry forward, enabling producers to develop innovative formulations with enhanced performance characteristics. These innovations include the creation of shorter shelf-life products. Consumers purchase bakery or confectionary items, snacks, and savoury products to satisfy the long ordeal of mouthfeel or eye feel. The role of shortening in such products allows the end-users to feel “happy” “content” or “satisfied” post-consumption. Shortbread cookies for example, easily melt in one’s mouth or would crumble if pressed between the fingers too tightly. The role of shortening is to separate pie dough from water, thereby creating air pockets that make these products extremely flaky and tasty as well. The growing urbanisation trends have led to extensive stress and sedentary lifestyles. Hence, consumers are looking to satisfy their food cravings from such products, to reduce anxiety-depression and various other reasons.

As for urbanisation, around 10% of the population lived in cities by 1900, which grew to 58% in 2016 to reach more than 75% by 2050. The trends dictate that human stress would only grow and supplement the market.

Awareness of the Harmful Effects of Fat to Restrain The Shortening Market

Consumers have become increasingly concerned about the ingredients, particularly if they contain high amounts. Moreover, the predominant ingredients which are used for shortening are high in various fats, which can negatively impact one’s health. Even consumers who are looking for vegan options, such as Coconut oil, have to be wary of the various ill effects such alternatives might present. Coconut oil is 90% saturated fat, which is even higher than butter (64%) or lard (40%). The said factors can lead to an increase in LDL or bad cholesterol levels. The population is soaring with high LDLS as nearly 94 million US adults have cholesterol above 200mg/dl while 0.028 billion adults have it above 240mg/dl. Owing to such health ailments, the market’s growth has been impeded.

Shortening Market Segmentations:

The Shortening market, based on source, is segmented into animal and vegan. Vegan segment dominates the market share in the year 2025 and is expected to grow during the forecast period. Various vegetable oils are included within the vegan segment, and the rise of veganism as a trend has rightly helped the market gain an edge. Consumers have become extremely aware of the ingredients they are consuming, plus aspects such as non-GMO, organic, and other aspects have aided the market growth. Further, giants such as Cargill had introduced new product lines especially for supplementing the vegan demand within the bakery items.

The Shortening market based on the application, segmented into bakery, confectioneries, snacks, savoury and others. The bakery and Confectioneries segment dominates the market share in the year 2025 and is expected to grow during the forecast period. It is owing to the inclusion of various types of bakery items that require shortening products. Shortening brings a gap between water and dough, thereby allowing the flakiness and crispness in the entire offerings. Bakery items boomed during the pandemic owing to offline channels and household sales. Consumers purchased baking soda-cocoa powder various other ancillaries to bake cakes, as manufacturers such as Tata and Cadbury reported a 70-80% increment in sales. Additionally, pre-mixes sales boomed, which include all the necessary oils and shortening products. Home baking as a trend helped the bakery and confectionery hold a lion’s share.

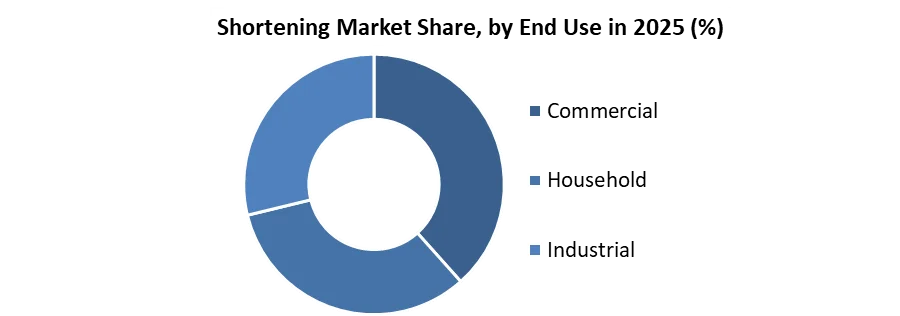

Based on End use, the Shortening Market is segmented into Commercial, Household and Industrial. the Commercial segment dominates the market share in 2025 and is expected to grow during the forecast period. A result of an expanding demand that is fuelled by diversified applications across numerous end-use categories. Within the market, the Commercial segment is a significant driver, with the rising number of bakeries and food service establishments. The Household segment also plays a key role in the market, with consumers looking for easy cooking solutions, which drives the demand for shortening in home kitchens. The Industrial segment is also active in sizeable proportions, supplying bulk supplies to food processing businesses. These segments are of importance given changes in consumer eating habits towards cooking and baking at home, combined with constant improvements in foodstuffs. As the Shortening Market keeps developing, data points towards a steady growth trend based on health trends and consumer movement towards plant-based alternatives, which poses challenges and opportunities to the industry players. Generally, the Shortening Market data shows a multi-layered ecosystem marked by changing consumer needs and industry adaptation.

Shortening Market Regional Analysis:

Europe

By region, the Shortening Market is segmented into North America, Europe, Asia-Pacific, South America, and Rest of the World. Europe is the dominant market in 2025 and is expected to have the largest market share during the forecast period. It is owing to the strong presence of various manufacturing or processing bakeries & confectionery industries within the region. Moreover, the number of bakers pre-COVID was on the increase, especially the artisanal bakers’ numbers increased by around 36% within a span of 10 years. Owing to such reasons, the region held a dominant size.

Asia Pacific

However, the Asia Pacific is expected to provide Beneficial growth opportunities to marketers owing to the growing strength in the food packaging and processing industries, especially in China and India. Various ready-to-eat baked goods and savouries are manufactured in China owing to the presence of cheap labour and other overhead costs. Moreover, governmental support would readily aid the market.

Shortening Market Competitive Landscape:

The Shortening Market is dominated by a competitive marketplace with diverse players struggling for a substantial market portion through pioneering products and value-added facilities. The industry has seen a rise in demand as the intake of baked goods, dessert items, and handled foods has been mounting, leading makers to reinforce their product offerings and improve their supply chain capabilities.

Contenders in this business exist crosswise around regional players, each one with particular qualities to bring to the table. Some regional players focus primarily on local distribution and personalised customer service, providing customised solutions to meet specific regional needs. Larger competitors struggle to achieve economies of scale through standardised mass production and global logistics networks, aiming to produce consistent, high-quality products at low costs to access broader international markets.

|

Shortening Market Scope Table |

|

|

Market Size in 2025 |

USD 5.20 Bn. |

|

Market Size in 2032 |

USD 6.90 Bn. |

|

CAGR (2026-2032) |

4.11% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Source Animal Vegan |

|

By Application Bakery Confectionary Snacks Savoury Others |

|

|

By End Use Commercial Household Industrial |

|

|

By Regional North America Asia Pacific Europe Middle East America South America |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, South Korea, Japan, India, Australia, Indonesia, Philippines, Malaysia, Vietnam, Thailand Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Players in Shortening Market:

North America

- Cargill, Inc.

- Archer Daniels Midland Company (ADM)

- Conagra Brands, Inc.

- Ventura Foods, LLC

- J.M. Smucker Company

- Bunge North America, Inc.

Asia Pacific

7. Wilmar International Limited

8. Fuji Oil Co., Ltd.

9. COFCO Group Co., Ltd.

10. Namchow Holdings Co., Ltd.

11. Musim Mas Holdings

12. Sime Darby Plantation Berhad

13. Premium Vegetable Oils Sdn Bhd

14. Uni-President Enterprises Corp.

Europe

15. AAK AB

16. Unilever plc

17. Associated British Foods plc

18. Tate & Lyle plc

19. Upfield

20. NMGK Group

Middle East

21. IFFCO (International Foodstuff Co.)

22. Savola Group

23. Al Ghurair Foods

24. Al Islami Foods

South America

25. Bunge Brasil

26. Cargill Brasil

27. BRF S.A.

28. Seara Alimentos S.A.

29. Solvay Group (Latin America operations)

30. Palmas Del Cesar S.A.

Frequently Asked Questions

The expected CAGR for the shortening Market from 2026 to 2032 is 4.11%.

The Europe region is the dominant market in 2025 and is expected to hold the highest market share during the forecast period.

Cargill, Incorporated, Archer Daniels Midland Company (ADM),Bunge Limited,Wilmar International Limited,AAK AB are the key players in Shotening Market.

Rising Demand for Processed Foods and Technological advancements are driving the Shortening Market in the upcoming years.

1. Shortening Market Introduction

1.1. Study Assumption and Market Definition

1.2. Scope of the Study

1.3. Executive Summary

2. Shortening Market: Competitive Landscape

2.1. Ecosystem Analysis

2.2. SMR Competition Matrix

2.3. Competitive Landscape

2.4. Key Players Benchmarking

2.4.1. Company Name

2.4.2. Business Segment

2.4.3. End-user Segment

2.4.4. Revenue (2025)

2.4.5. Company Locations

2.5. Market Structure

2.5.1. Market Leaders

2.5.2. Market Followers

2.5.3. Emerging Players

2.6. Mergers and Acquisitions Details

3. Shortening Market: Dynamics

3.1. Shortening Market Trends by Region

3.1.1. North America Shortening Market Trends

3.1.2. Europe Shortening Market Trends

3.1.3. Asia Pacific Shortening Market Trends

3.1.4. Middle East and Africa Shortening Market Trends

3.1.5. South America Shortening Market Trends

3.2. Shortening Market Dynamics

3.2.1. Global Shortening Market Drivers

3.2.2. Global Shortening Market Restraints

3.2.3. Global Shortening Market Opportunities

3.2.4. Global Shortening Market Challenges

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

3.5. Trade Analysis

3.6. Regulatory Landscape by Region

3.6.1. North America

3.6.2. Europe

3.6.3. Asia Pacific

3.6.4. Middle East and Africa

3.6.5. South America

3.7. Key Opinion Leader Analysis

4. Shortening Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

4.1. Shortening Market Size and Forecast, By Source (2025-2032)

4.1.1. Animal

4.1.2. Vegan

4.2. Shortening Market Size and Forecast, By Application (2025-2032)

4.2.1. Bakery

4.2.2. Confectionary

4.2.3. Snacks

4.2.4. Savoury

4.2.5. Others

4.3. Shortening Market Size and Forecast, End Use (2025-2032)

4.3.1. Commercial

4.3.2. Household

4.3.3. Industrial

4.4. Shortening Market Size and Forecast, by Region (2025-2032)

4.4.1. North America

4.4.2. Europe

4.4.3. Asia Pacific

4.4.4. Middle East and Africa

4.4.5. South America

5. North America Shortening Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

5.1. North America Shortening Market Size and Forecast, By Source (2025-2032)

5.1.1. Animal

5.1.2. Vegan

5.2. North America Shortening Market Size and Forecast, By Application (2025-2032)

5.2.1. Bakery

5.2.2. Confectionary

5.2.3. Snacks

5.2.4. Savoury

5.2.5. Others

5.3. North America Shortening Market Size and Forecast, End Use (2025-2032)

5.3.1. Commercial

5.3.2. Household

5.3.3. Industrial

5.4. North America Shortening Market Size and Forecast, by Country (2025-2032)

5.4.1. United States

5.4.1.1. United States Shortening Market Size and Forecast, By Source (2025-2032)

5.4.1.1.1. Animal

5.4.1.1.2. Vegan

5.4.1.2. United States Shortening Market Size and Forecast, By Application (2025-2032)

5.4.1.2.1. Bakery

5.4.1.2.2. Confectionary

5.4.1.2.3. Snacks

5.4.1.2.4. Savoury

5.4.1.2.5. Others

5.4.1.3. United States Shortening Market Size and Forecast, End Use (2025-2032)

5.4.1.3.1. Commercial

5.4.1.3.2. Household

5.4.1.3.3. Industrial

5.4.1.4. Canada Shortening Market Size and Forecast, By Source (2025-2032)

5.4.1.4.1. Animal

5.4.1.4.2. Vegan

5.4.1.5. Canada Shortening Market Size and Forecast, By Application (2025-2032)

5.4.1.5.1. Bakery

5.4.1.5.2. Confectionary

5.4.1.5.3. Snacks

5.4.1.5.4. Savoury

5.4.1.5.5. Others

5.4.2. Canada Shortening Market Size and Forecast, End Use (2025-2032)

5.4.2.1.1. Commercial

5.4.2.1.2. Household

5.4.2.1.3. Industrial

5.4.3. Mexico

5.4.3.1. Mexico Shortening Market Size and Forecast, By Source (2025-2032)

5.4.3.1.1. Animal

5.4.3.1.2. Vegan

5.4.3.2. Mexico Shortening Market Size and Forecast, By Application (2025-2032)

5.4.3.2.1. Bakery

5.4.3.2.2. Confectionary

5.4.3.2.3. Snacks

5.4.3.2.4. Savoury

5.4.3.2.5. Others

5.4.3.3. Mexico Shortening Market Size and Forecast, End Use (2025-2032)

5.4.3.3.1. Commercial

5.4.3.3.2. Household

5.4.3.3.3. Industrial

6. Europe Shortening Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

6.1. Europe Shortening Market Size and Forecast, By Source (2025-2032)

6.2. Europe Shortening Market Size and Forecast, By Application (2025-2032)

6.3. Europe Shortening Market Size and Forecast, End Use (2025-2032)

6.4. Europe Shortening Market Size and Forecast, by Country (2025-2032)

6.4.1. United Kingdom

6.4.1.1. United Kingdom Shortening Market Size and Forecast, By Source (2025-2032)

6.4.1.2. United Kingdom Shortening Market Size and Forecast, By Application (2025-2032)

6.4.1.3. United Kingdom Shortening Market Size and Forecast, End Use (2025-2032)

6.4.2. France

6.4.2.1. France Shortening Market Size and Forecast, By Source (2025-2032)

6.4.2.2. France Shortening Market Size and Forecast, By Application (2025-2032)

6.4.2.3. France Shortening Market Size and Forecast, End Use (2025-2032)

6.4.3. Germany

6.4.3.1. Germany Shortening Market Size and Forecast, By Source (2025-2032)

6.4.3.2. Germany Shortening Market Size and Forecast, By Application (2025-2032)

6.4.3.3. Germany Shortening Market Size and Forecast, End Use (2025-2032)

6.4.4. Italy

6.4.4.1. Italy Shortening Market Size and Forecast, By Source (2025-2032)

6.4.4.2. Italy Shortening Market Size and Forecast, By Application (2025-2032)

6.4.4.3. Italy Shortening Market Size and Forecast, End Use (2025-2032)

6.4.5. Spain

6.4.5.1. Spain Shortening Market Size and Forecast, By Source (2025-2032)

6.4.5.2. Spain Shortening Market Size and Forecast, By Application (2025-2032)

6.4.5.3. Spain Shortening Market Size and Forecast, End Use (2025-2032)

6.4.6. Sweden

6.4.6.1. Sweden Shortening Market Size and Forecast, By Source (2025-2032)

6.4.6.2. Sweden Shortening Market Size and Forecast, By Application (2025-2032)

6.4.6.3. Sweden Shortening Market Size and Forecast, End Use (2025-2032)

6.4.7. Austria

6.4.7.1. Austria Shortening Market Size and Forecast, By Source (2025-2032)

6.4.7.2. Austria Shortening Market Size and Forecast, By Application (2025-2032)

6.4.7.3. Austria Shortening Market Size and Forecast, End Use (2025-2032)

6.4.8. Rest of Europe

6.4.8.1. Rest of Europe Shortening Market Size and Forecast, By Source (2025-2032)

6.4.8.2. Rest of Europe Shortening Market Size and Forecast, By Application (2025-2032)

6.4.8.3. Rest of Europe Shortening Market Size and Forecast, End Use (2025-2032)

7. Asia Pacific Shortening Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

7.1. Asia Pacific Shortening Market Size and Forecast, By Source (2025-2032)

7.2. Asia Pacific Shortening Market Size and Forecast, By Application (2025-2032)

7.3. Asia Pacific Shortening Market Size and Forecast, End Use (2025-2032)

7.4. Asia Pacific Shortening Market Size and Forecast, by Country (2025-2032)

7.4.1. China

7.4.1.1. China Shortening Market Size and Forecast, By Source (2025-2032)

7.4.1.2. China Shortening Market Size and Forecast, By Application (2025-2032)

7.4.1.3. China Shortening Market Size and Forecast, End Use (2025-2032)

7.4.2. S Korea

7.4.2.1. S Korea Shortening Market Size and Forecast, By Source (2025-2032)

7.4.2.2. S Korea Shortening Market Size and Forecast, By Application (2025-2032)

7.4.2.3. S Korea Shortening Market Size and Forecast, End Use (2025-2032)

7.4.3. Japan

7.4.3.1. Japan Shortening Market Size and Forecast, By Source (2025-2032)

7.4.3.2. Japan Shortening Market Size and Forecast, By Application (2025-2032)

7.4.3.3. Japan Shortening Market Size and Forecast, End Use (2025-2032)

7.4.4. India

7.4.4.1. India Shortening Market Size and Forecast, By Source (2025-2032)

7.4.4.2. India Shortening Market Size and Forecast, By Application (2025-2032)

7.4.4.3. India Shortening Market Size and Forecast, End Use (2025-2032)

7.4.5. Australia

7.4.5.1. Australia Shortening Market Size and Forecast, By Source (2025-2032)

7.4.5.2. Australia Shortening Market Size and Forecast, By Application (2025-2032)

7.4.5.3. Australia Shortening Market Size and Forecast, End Use (2025-2032)

7.4.6. Indonesia

7.4.6.1. Indonesia Shortening Market Size and Forecast, By Source (2025-2032)

7.4.6.2. Indonesia Shortening Market Size and Forecast, By Application (2025-2032)

7.4.6.3. Indonesia Shortening Market Size and Forecast, End Use (2025-2032)

7.4.7. Philippines

7.4.7.1. Malaysia Shortening Market Size and Forecast, By Source (2025-2032)

7.4.7.2. Malaysia Shortening Market Size and Forecast, By Application (2025-2032)

7.4.7.3. Malaysia Shortening Market Size and Forecast, End Use (2025-2032)

7.4.8. Malaysia

7.4.8.1. Malaysia Shortening Market Size and Forecast, By Source (2025-2032)

7.4.8.2. Malaysia Shortening Market Size and Forecast, By Application (2025-2032)

7.4.8.3. Malaysia Shortening Market Size and Forecast, End Use (2025-2032)

7.4.9. Vietnam

7.4.9.1. Vietnam Shortening Market Size and Forecast, By Source (2025-2032)

7.4.9.2. Vietnam Shortening Market Size and Forecast, By Application (2025-2032)

7.4.9.3. Vietnam Shortening Market Size and Forecast, End Use (2025-2032)

7.4.10. Thailand

7.4.10.1. Thailand Shortening Market Size and Forecast, By Source (2025-2032)

7.4.10.2. Thailand Shortening Market Size and Forecast, By Application (2025-2032)

7.4.10.3. Thailand Shortening Market Size and Forecast, End Use (2025-2032)

7.4.11. Rest of Asia Pacific

7.4.11.1. Rest of Asia Pacific Shortening Market Size and Forecast, By Source (2025-2032)

7.4.11.2. Rest of Asia Pacific Shortening Market Size and Forecast, By Application (2025-2032)

7.4.11.3. Rest of Asia Pacific Shortening Market Size and Forecast, End Use (2025-2032)

8. Middle East and Africa Shortening Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

8.1. Middle East and Africa Shortening Market Size and Forecast, By Source (2025-2032)

8.2. Middle East and Africa Shortening Market Size and Forecast, By Application (2025-2032)

8.3. Middle East and Africa Shortening Market Size and Forecast, End Use (2025-2032)

8.4. Middle East and Africa Shortening Market Size and Forecast, by Country (2025-2032)

8.4.1. South Africa

8.4.1.1. South Africa Shortening Market Size and Forecast, By Source (2025-2032)

8.4.1.2. South Africa Shortening Market Size and Forecast, By Application (2025-2032)

8.4.1.3. South Africa Shortening Market Size and Forecast, End Use (2025-2032)

8.4.2. GCC

8.4.2.1. GCC Shortening Market Size and Forecast, By Source (2025-2032)

8.4.2.2. GCC Shortening Market Size and Forecast, By Application (2025-2032)

8.4.2.3. GCC Shortening Market Size and Forecast, End Use (2025-2032)

8.4.3. Nigeria

8.4.3.1. Nigeria Shortening Market Size and Forecast, By Source (2025-2032)

8.4.3.2. Nigeria Shortening Market Size and Forecast, By Application (2025-2032)

8.4.3.3. Nigeria Shortening Market Size and Forecast, End Use (2025-2032)

8.4.4. Rest of ME&A

8.4.4.1. Rest of ME&A Shortening Market Size and Forecast, By Source (2025-2032)

8.4.4.2. Rest of ME&A Shortening Market Size and Forecast, By Application (2025-2032)

8.4.4.3. Rest of ME&A Shortening Market Size and Forecast, End Use (2025-2032)

9. South America Shortening Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

9.1. South America Shortening Market Size and Forecast, By Source (2025-2032)

9.2. South America Shortening Market Size and Forecast, By Application (2025-2032)

9.3. South America Shortening Market Size and Forecast, End Use (2025-2032)

9.4. South America Shortening Market Size and Forecast, by Country (2025-2032)

9.4.1. Brazil

9.4.1.1. Brazil Shortening Market Size and Forecast, By Source (2025-2032)

9.4.1.2. Brazil Shortening Market Size and Forecast, By Application (2025-2032)

9.4.1.3. Brazil Shortening Market Size and Forecast, End Use (2025-2032)

9.4.2. Argentina

9.4.2.1. Argentina Shortening Market Size and Forecast, By Source (2025-2032)

9.4.2.2. Argentina Shortening Market Size and Forecast, By Application (2025-2032)

9.4.2.3. Argentina Shortening Market Size and Forecast, End Use (2025-2032)

9.4.3. Rest of South America

9.4.3.1. Rest of South America Shortening Market Size and Forecast, By Source (2025-2032)

9.4.3.2. Rest of South America Shortening Market Size and Forecast, By Application (2025-2032)

9.4.3.3. Rest of South America Shortening Market Size and Forecast, End Use (2025-2032)

10. Company Profile: Key Players

10.1. Cargill, Inc.

10.1.1. Company Overview

10.1.2. Business Portfolio

10.1.3. Financial Overview

10.1.4. SWOT Analysis

10.1.5. Strategic Analysis

10.1.6. Recent Developments

10.2. Archer Daniels Midland Company (ADM)

10.3. Conagra Brands, Inc.

10.4. Ventura Foods, LLC

10.5. J.M. Smucker Company

10.6. Bunge North America, Inc.

10.7. Wilmar International Limited

10.8. Fuji Oil Co., Ltd.

10.9. COFCO Group Co., Ltd.

10.10. Namchow Holdings Co., Ltd.

10.11. Musim Mas Holdings

10.12. Sime Darby Plantation Berhad

10.13. Premium Vegetable Oils Sdn Bhd

10.14. Uni-President Enterprises Corp.

10.15. AAK AB

10.16. Unilever plc

10.17. Associated British Foods plc

10.18. Tate & Lyle plc

10.19. Upfield

10.20. NMGK Group

10.21. IFFCO (International Foodstuff Co.)

10.22. Savola Group

10.23. Al Ghurair Foods

10.24. Al Islami Foods

10.25. Bunge Brasil

10.26. Cargill Brasil

10.27. BRF S.A.

10.28. Seara Alimentos S.A.

10.29. Solvay Group (Latin America operations)

10.30. Palmas Del Cesar S.A.

11. Key Findings

12. Analyst Recommendations

13. Shortening Market: Research Methodology