Semiconductor in Wireless Communication Market- Navigating the Future Innovations and Growth in Industry

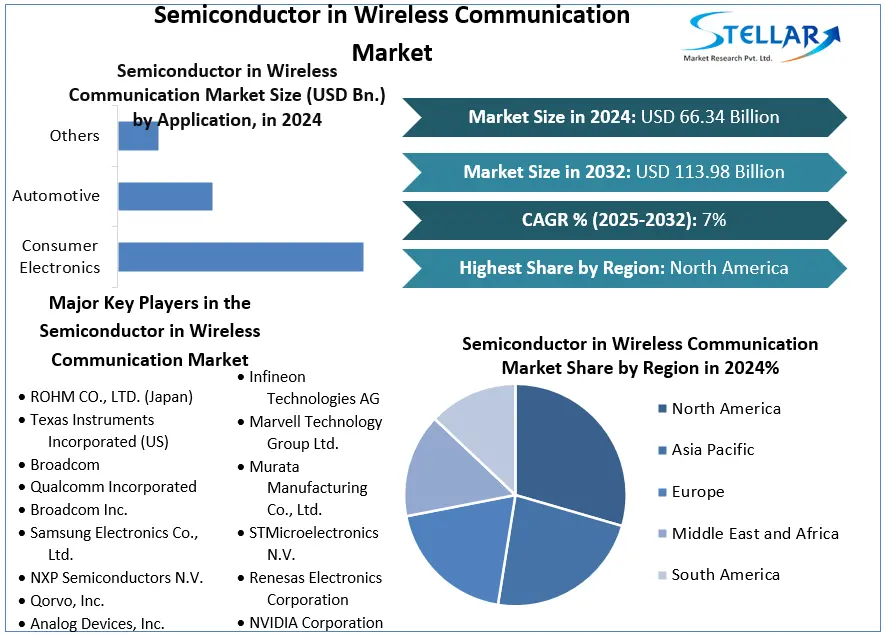

The Semiconductor in Wireless Communication Market size was valued at USD 66.34 Bn. in 2024 and the total Semiconductor in Wireless Communication Market revenue is expected to grow at a CAGR of 7% from 2025 to 2032, reaching nearly USD 113.98 Bn. by 2032.

Semiconductor in Wireless Communication Market Overview

Semiconductors are essential in wireless communication devices such as smartphones, wireless routers, etc. The semiconductor market for wireless communication includes semiconductor components and systems used in wireless communication technologies, such as cellular networks, Wi-Fi, Bluetooth, satellite communication, and more. These components include chips and ICs (integrated circuits) that are crucial for signal processing, data transmission, and connectivity.

These devices enable the transmission and reception of signals by converting electrical signals into radio waves and vice versa. Increasing use of smartphones, IoT devices, and connected devices boosts the demand for advanced wireless communication solutions. Innovations in semiconductor technology, such as smaller node processes and advanced packaging, drive Semiconductor in Wireless Communication market growth.

To get more Insights: Request Free Sample Report

Semiconductor in Wireless Communication Market Dynamics

Technological advancements and increasing demand for connectivity to boost the Semiconductor in Wireless Communication Market growth

The transition to 5G and the development of 6G are significant milestones that require sophisticated semiconductor solutions. This growth is largely fueled by the increasing need for faster and more reliable wireless communication, which in turn drives the demand for advanced semiconductors, which is expected to boost the Semiconductor in Wireless Communication Market growth. With the proliferation of smartphones, tablets, and other wireless devices, there is an ever-increasing need for high-performance semiconductors. According to SMR, the number of smartphone users worldwide is expected to reach 6.8 Bn by 2023, up from 6.3 Bn in 2021. This surge in smartphone usage directly correlates with the need for more efficient and powerful semiconductor chips to support high-speed data transmission and improved battery life.

The integration of artificial intelligence (AI) and machine learning (ML) into wireless communication is another key driver. These technologies require advanced semiconductors capable of performing complex computations at high speeds. For example, AI-powered network management systems optimize wireless networks in real time, enhancing performance and reliability.

- A practical example of these drivers in action is Qualcomm's Snapdragon processors, which are widely used in smartphones, tablets, and other wireless devices. Qualcomm's advancements in 5G technology and AI integration have positioned it as a leader in the semiconductor market. Similarly, companies like Samsung and TSMC are investing in advanced manufacturing processes, such as extreme ultraviolet (EUV) lithography, to produce smaller, more efficient semiconductors that cater to the growing needs of the Semiconductor in Wireless Communication market.

Technologies Driving Connectivity

Types of wireless communication include infrared, satellite, broadcast radio, microwave, mobile communications systems, Wi-Fi, and technologies such as Bluetooth and Zigbee. In addition, radio frequency (RF) power devices are also key components in a broad range of wireless communications. Here are just a few examples:

- Small devices that are capable of delivering several watts of RF power from a battery power source of a few volts are used in handheld applications such as cellphones.

- High-power RF devices, which can deliver up to hundreds of watts, are used in infrastructure applications such as cellphone base stations.

- System-on-chip (SoC) and field-programmable gate array (FPGA) devices are being used in the development of wireless communications systems such as 5G.

- Low-energy microcontrollers (MCUs) are enabling Bluetooth capabilities.

- Wireless sensor networks are used for applications such as environmental monitoring, structural monitoring of bridges and buildings, and asset tracking.

Challenges in Semiconductor in Wireless Communication Market

Rapid technological Evolution to present significant challenge in Semiconductor in Wireless Communication Market

The semiconductor industry, in the wireless communication market, faces challenges that influence its growth and sustainability. Industry disruptors, demand and supply dynamics, and economic indicators contribute to the Semiconductor in Wireless Communication market complexity. Recent years have seen a 38.8% decline in the memory market in 2023 due to oversupply, reflecting the volatility in demand and supply dynamics. In 2024, R&D spending projections indicate a slight decrease in R&D spending, which significantly impact the semiconductor in Wireless Communication industry growth.

The continuous innovation in wireless communication technologies like 5G and the expected 6G requires ongoing advancements in semiconductor design and manufacturing. Keeping up with this Semiconductor in Wireless Communication market evolution demands substantial investment in R&D and the ability to swiftly adapt to new standards and protocols. This constant evolution strain resources and lead to increased costs. Additionally, wireless communication devices, particularly mobile and IoT devices, demand semiconductors that are power-efficient while maintaining high performance.

Balancing these requirements is challenging, as increased functionality often results in higher power consumption. Developing power-efficient semiconductors requires innovative materials and design techniques, adding to the R&D burden. Environmentally, semiconductor manufacturing is resource-intensive, consuming large amounts of water, energy, and raw materials. Addressing the environmental impact of semiconductor component production processes is crucial for sustainability, necessitating substantial investment in new technologies and processes.

Semiconductor in Wireless Communication Market Segment Analysis

Based on Application, the market is segmented into Consumer Electronics, Automotive, and Others. Consumer Electronics segment dominated the market in 2024 and is expected to hold the largest Semiconductor in Wireless Communication Market share over the forecast period. The consumer electronics segment within the semiconductor market for wireless communication is a dynamic and rapidly evolving area driven by the increasing demand for connectivity, miniaturization, and enhanced functionality. This segment includes a wide range of devices such as smartphones, tablets, laptops, wearables, smart home devices, and entertainment systems. The growth in this segment is fueled by several factors, including technological advancements, consumer demand for smarter and more connected devices, and the proliferation of the Internet of Things (IoT).

Smartphones and tablets are the primary drivers of the consumer electronics segment. According to SMR, global smartphone shipments reached over 1.5 billion units in 2022. The demand for faster processors, better graphics, improved battery life, and advanced connectivity features like 5G drives the need for sophisticated semiconductors. Companies like Qualcomm, Apple, and Samsung are continuously innovating to provide more powerful and energy-efficient chipsets for these devices.

Semiconductor in Wireless Communication Market Regional Insight

North America dominated the market in 2024 and is expected to hold the largest Semiconductor in Wireless Communication Market share over the forecast period. The rapid progression of wireless communication technologies is a significant driver for the semiconductor market in North America. The deployment and expansion of 5G networks are at the forefront of this technological evolution.

According to the Global System for Mobile Communications (GSMA), North America is expected to have 5G connections making up 51% of total mobile connections by 2025. This shift necessitates advanced semiconductor solutions to support higher data speeds, lower latency, and increased connectivity. Companies like Qualcomm and Intel are leading the charge with cutting-edge chipsets designed specifically for 5G applications, underscoring the importance of technological innovation in the region.

Governmental support plays a crucial role in driving the semiconductor market in North America. Initiatives like the U.S. CHIPS Act, which allocates USD 52 billion for semiconductor research, development, manufacturing, and workforce development, are designed to bolster domestic semiconductor production and innovation. This legislative support aims to reduce dependency on foreign semiconductor imports and strengthen the domestic semiconductor industry, providing a significant boost to the Semiconductor in Wireless Communication Market. The United States, as the largest market in North America, is characterized by a high concentration of semiconductor companies and a strong focus on innovation and technology. Silicon Valley, for example, is a global hub for semiconductor research and development, housing some of the world's leading semiconductor firms and start-ups.

Canada is also emerging as a significant player, particularly in areas like AI and advanced wireless communication research. Canadian universities and research institutions are collaborating with industry leaders to drive innovation in semiconductor technologies. Additionally, the Canadian government is investing in initiatives to support the growth of the semiconductor industry, further contributing to the regional Semiconductor in Wireless Communication Market development.

Semiconductor in Wireless Communication Market Competitive Landscape

NXP Semiconductors NV operates as a global semiconductor company, designing products for various industries such as mobile communications, consumer electronics, security applications, and networking. With a focus on automotive, identification, wireless infrastructure, lighting, mobile, and computing applications, Nxp Semiconductors Nv has a diverse portfolio of products. The company’s high scores in Dividend, Growth, and Momentum indicate a strong performance in these areas, positioning Nxp Semiconductors Nv for success in the competitive semiconductor market.

Samsung Research, a leading research and development organization at Samsung Electronics, is collaborating with semiconductor and software design company Arm on the research of parallel packet processing technology (SIMD, Single Instruction Multiple Data) — one of the key software technologies in next-generation communications. As part of the collaboration, Samsung Research plans to launch an open-source project with Arm to jointly develop and refine parallel packet processing technology.

Samsung Research’s emphasis on next-generation communication technologies through collaborative R&D gives it a competitive edge in developing future-ready solutions. NXP’s established product portfolio and strong market performance show its capability in delivering high-performance semiconductors across various applications.

Semiconductor in Wireless Communication Market Scope

|

Semiconductor in Wireless Communication Market |

|

|

Market Size in 2024 |

USD 66.34 Bn. |

|

Market Size in 2032 |

USD 113.98 Bn. |

|

CAGR (2025-2032) |

7% |

|

Historic Data |

2019-2024 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2032 |

|

Semiconductor in Wireless Communication Market Segments |

By Type

|

|

By Application

|

|

|

Regional Scope |

North America – United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa – South Africa, GCC, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Semiconductor in Wireless Communication Market Key players includes:

- ROHM CO., LTD. (Japan)

- Texas Instruments Incorporated (US)

- Broadcom

- Qualcomm Incorporated

- Broadcom Inc.

- Samsung Electronics Co., Ltd.

- NXP Semiconductors N.V.

- Qorvo, Inc.

- Analog Devices, Inc.

- Infineon Technologies AG

- Marvell Technology Group Ltd.

- Murata Manufacturing Co., Ltd.

- STMicroelectronics N.V.

- Renesas Electronics Corporation

- NVIDIA Corporation

- Microchip Technology Incorporated

- Maxim Integrated Products, Inc.

- Realtek Semiconductor Corp.

- Vishay Intertechnology, Inc.

Frequently Asked Questions

The demand is driven by the increasing use of smartphones, IoT devices, and the need for faster and more reliable communication. Innovations like 5G and future 6G technologies also drive the need for advanced semiconductor solutions.

5G requires sophisticated semiconductor solutions for high-speed data transmission and low latency. This has led to increased investment in R&D and advanced semiconductor technologies to support the deployment of 5G networks.

Challenges include rapid technological evolution, balancing power efficiency with high performance, environmental impacts of manufacturing, and the need for substantial R&D investments.

North America leads the market, driven by advancements in 5G technology and strong governmental support, such as the U.S. CHIPS Act, which supports semiconductor research and development.

1. Semiconductor in Wireless Communication Market: Research Methodology

2. Semiconductor in Wireless Communication Market: Executive Summary

3. Semiconductor in Wireless Communication Market: Competitive Landscape

4. Potential Areas for Investment

4.1. Stellar Competition Matrix

4.2. Competitive Landscape

4.3. Key Players Benchmarking

4.4. Market Structure

4.4.1. Market Leaders

4.4.2. Market Followers

4.4.3. Emerging Players

4.5. Consolidation of the Market

5. Semiconductor in Wireless Communication Market: Dynamics

5.1. Market Trends

5.2. Market Drivers

5.3. Market Restraints

5.4. Market Opportunities

5.5. Market Challenges

5.6. PORTER’s Five Forces Analysis

5.7. PESTLE Analysis

5.8. Technology Roadmap

5.9. Strategies for New Entrants to Penetrate the Market

5.10. Regulatory Landscape by Region

5.10.1. North America

5.10.2. Europe

5.10.3. Asia Pacific

5.10.4. Middle East and Africa

5.10.5. South America

6. Semiconductor in Wireless Communication Market Size and Forecast by Segments (by Value USD Billion)

6.1. Semiconductor in Wireless Communication Market Size and Forecast, by Type (2024-2032)

6.1.1. Cellular Baseband Processors

6.1.2. Mobile Wi-Fi Chips

6.1.3. Bluetooth Transceivers

6.1.4. Global Positioning System (GPS) Receivers

6.1.5. Near-Field Communication Chips

6.1.6. Others

6.2. Semiconductor in Wireless Communication Market Size and Forecast, by Application (2024-2032)

6.2.1. Consumer Electronics

6.2.2. Automotive

6.2.3. Others

6.3. Semiconductor in Wireless Communication Market Size and Forecast, by Region (2024-2032)

6.3.1. North America

6.3.2. Europe

6.3.3. Asia Pacific

6.3.4. Middle East and Africa

6.3.5. South America

7. North America Semiconductor in Wireless Communication Market Size and Forecast (by Value USD Billion)

7.1. North America Semiconductor in Wireless Communication Market Size and Forecast, by Type (2024-2032)

7.1.1. Cellular Baseband Processors

7.1.2. Mobile Wi-Fi Chips

7.1.3. Bluetooth Transceivers

7.1.4. Global Positioning System (GPS) Receivers

7.1.5. Near-Field Communication Chips

7.1.6. Others

7.2. North America Semiconductor in Wireless Communication Market Size and Forecast, by Application (2024-2032)

7.2.1. Consumer Electronics

7.2.2. Automotive

7.2.3. Others

7.3. North America Semiconductor in Wireless Communication Market Size and Forecast, by Country (2024-2032)

7.3.1. United States

7.3.2. Canada

7.3.3. Mexico

8. Europe Semiconductor in Wireless Communication Market Size and Forecast (by Value USD Billion)

8.1. Europe Semiconductor in Wireless Communication Market Size and Forecast, by Type (2024-2032)

8.1.1. Cellular Baseband Processors

8.1.2. Mobile Wi-Fi Chips

8.1.3. Bluetooth Transceivers

8.1.4. Global Positioning System (GPS) Receivers

8.1.5. Near-Field Communication Chips

8.1.6. Others

8.2. Europe Semiconductor in Wireless Communication Market Size and Forecast, by Application (2024-2032)

8.2.1. Consumer Electronics

8.2.2. Automotive

8.2.3. Others

8.3. Europe Semiconductor in Wireless Communication Market Size and Forecast, by Country (2024-2032)

8.3.1. UK

8.3.2. France

8.3.3. Germany

8.3.4. Italy

8.3.5. Spain

8.3.6. Sweden

8.3.7. Austria

8.3.8. Rest of Europe

9. Asia Pacific Semiconductor in Wireless Communication Market Size and Forecast (by Value USD Billion)

9.1. Asia Pacific Semiconductor in Wireless Communication Market Size and Forecast, by Type (2024-2032)

9.1.1. Cellular Baseband Processors

9.1.2. Mobile Wi-Fi Chips

9.1.3. Bluetooth Transceivers

9.1.4. Global Positioning System (GPS) Receivers

9.1.5. Near-Field Communication Chips

9.1.6. Others

9.2. Asia Pacific Semiconductor in Wireless Communication Market Size and Forecast, by Application (2024-2032)

9.2.1. Consumer Electronics

9.2.2. Automotive

9.2.3. Others

9.3. Asia Pacific Semiconductor in Wireless Communication Market Size and Forecast, by Country (2024-2032)

9.3.1. China

9.3.2. S Korea

9.3.3. Japan

9.3.4. India

9.3.5. Australia

9.3.6. Indonesia

9.3.7. Malaysia

9.3.8. Vietnam

9.3.9. Taiwan

9.3.10. Bangladesh

9.3.11. Pakistan

9.3.12. Rest of Asia Pacific

10. Middle East and Africa Semiconductor in Wireless Communication Market Size and Forecast (by Value USD Billion)

10.1. Middle East and Africa Semiconductor in Wireless Communication Market Size and Forecast, by Type (2024-2032)

10.1.1. Cellular Baseband Processors

10.1.2. Mobile Wi-Fi Chips

10.1.3. Bluetooth Transceivers

10.1.4. Global Positioning System (GPS) Receivers

10.1.5. Near-Field Communication Chips

10.1.6. Others

10.2. Middle East and Africa Semiconductor in Wireless Communication Market Size and Forecast, by Application (2024-2032)

10.2.1. Consumer Electronics

10.2.2. Automotive

10.2.3. Others

10.3. Middle East and Africa Electric Vehicle Traction Motor Market Size and Forecast, by Country (2024-2032)

10.3.1. South Africa

10.3.2. GCC

10.3.3. Egypt

10.3.4. Nigeria

10.3.5. Rest of ME&A

11. South America Semiconductor in Wireless Communication Market Size and Forecast (by Value USD Billion)

11.1. South America Semiconductor in Wireless Communication Market Size and Forecast, by Type (2024-2032)

11.1.1. Cellular Baseband Processors

11.1.2. Mobile Wi-Fi Chips

11.1.3. Bluetooth Transceivers

11.1.4. Global Positioning System (GPS) Receivers

11.1.5. Near-Field Communication Chips

11.1.6. Others

11.2. South America Semiconductor in Wireless Communication Market Size and Forecast, by Application (2024-2032)

11.2.1. Consumer Electronics

11.2.2. Automotive

11.2.3. Others

11.3. South America Semiconductor in Wireless Communication Market Size and Forecast, by Country (2024-2032)

11.3.1. Brazil

11.3.2. Argentina

11.3.3. Rest of South America

12. Company Profile: Key players

12.1. ROHM CO., LTD. (Japan)

12.1.1. Company Overview

12.1.2. Financial Overview

12.1.3. Business Portfolio

12.1.4. SWOT Analysis

12.1.5. Business Strategy

12.1.6. Recent Developments

12.2. Texas Instruments Incorporated (US)

12.3. Broadcom

12.4. Qualcomm Incorporated

12.5. Broadcom Inc.

12.6. Samsung Electronics Co., Ltd.

12.7. NXP Semiconductors N.V.

12.8. Qorvo, Inc.

12.9. Analog Devices, Inc.

12.10. Infineon Technologies AG

12.11. Marvell Technology Group Ltd.

12.12. Murata Manufacturing Co., Ltd.

12.13. STMicroelectronics N.V.

12.14. Renesas Electronics Corporation

12.15. NVIDIA Corporation

12.16. Microchip Technology Incorporated

12.17. Maxim Integrated Products, Inc.

12.18. Realtek Semiconductor Corp.

12.19. Vishay Intertechnology, Inc.

13. Key Findings

14. Industry Recommendations