Semiconductor in Telecommunication Market Size, Share & Forecast 2026-2032: 5G & AI Powering Growth

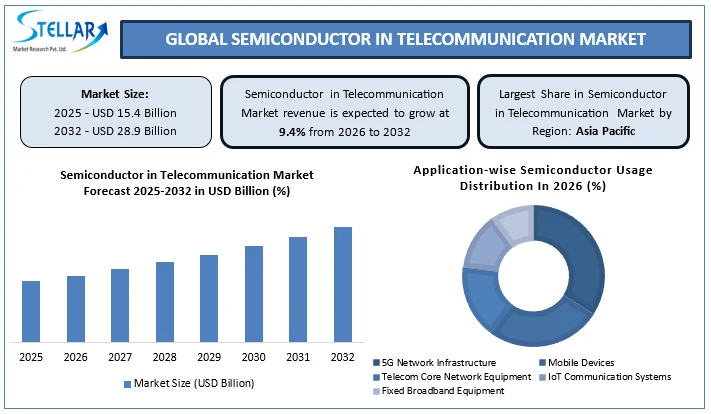

Global Semiconductor in Telecommunication Market is projected to grow at a CAGR of 9.4%, reaching USD 15.4 billion in 2025 and 28.9 billion by 2032, driven by 5G rollout, high-speed data demand, and AI/ML integration.

Global Semiconductor in Telecommunication Market Overview:

Semiconductor In Telecommunication refers to electronic chips used to process signals, manage data transmission, and enable connectivity in telecom networks and devices, supporting technologies such as 4G, 5G, broadband, and IoT communication systems. Semiconductor in Telecommunication Market is evolving rapidly as accelerating 5G deployment, rising demand for high-speed data transmission, and growing integration of AI and machine learning reshape global telecom infrastructure.

Global Semiconductor in Telecommunication Market is projected to grow at a CAGR of 9.4%, reaching USD 15.4 billion in 2025 and 28.9 billion by 2032. Advanced semiconductors such as RF ICs, baseband processors, and network chipsets are becoming critical to enable low latency, higher throughput, and intelligent network operations. Despite high production costs acting as a restraint, strong investments and technological innovation continue to support market size expansion, competitive share dynamics, and a positive long-term forecast across regions, led by Asia Pacific.

Key Highlights

- Global 5G Deployment: China Semiconductor in Telecommunication Market deployed 4.2–4.7 million 5G base stations by late 2025, supporting over 1 billion 5G-enabled mobile subscriptions worldwide.

- Mobile Data Growth: OECD countries’ average mobile data usage increased from nearly 8 GB/month (2022) to 17 GB/month (2024) per subscription, reflecting surging high-speed data demand.

- Global Mobile Traffic: Worldwide mobile broadband traffic rose from Nearly 1 ZB in 2023 to Nearly 1.3 ZB in 2024, with 1.9 billion broadband subscriptions by mid-2024.

- Asia Pacific Investment: USD 220 billion was invested in telecom infrastructure during 2019–2024, including 39 commercial 5G networks launched across nine countries.

- Semiconductor Manufacturing Scale: TSMC produces 11,800+ semiconductor products with annual capacity exceeding 16 million 12-inch equivalent wafers, enabling advanced telecom semiconductor supply globally.

To get more Insights: Request Free Sample Report

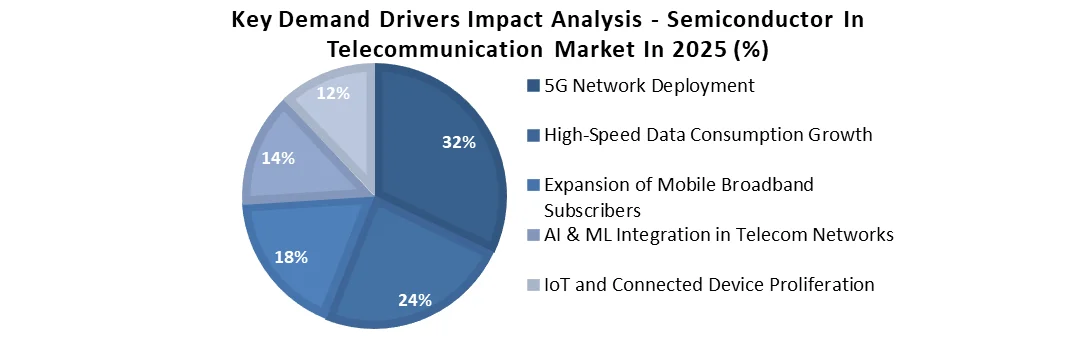

5G Expansion Driving High-Performance Demand in Semiconductor in Telecommunication Market

- In Semiconductor in Telecommunication Market rapid 5G rollout is a key structural trend driving demand for advanced telecom semiconductors.

- Increased deployment requires RF semiconductors, 5G ICs, network chipsets, and baseband processors for modern telecom infrastructure and devices.

- China deployed approximately 4.2–4.7 million 5G base stations by late 2025, supported by over 1 billion 5G-enabled mobile subscriptions.

- India operationalized 518,800+ 5G base transceiver stations and served 400+ million 5G subscribers by end-2025.

- Expanding 5G coverage increases demand for high-performance, power-efficient semiconductors to enable higher throughput and lower latency.

- 5G deployment acceleration is shaping technology priorities, infrastructure investment, and strategic planning across the global semiconductor and telecommunication ecosystem.

Surging High-Speed Data Drives Advanced Semiconductor Demand in Telecom

High-speed data transmission has become a fundamental requirement in modern telecommunications, driven by the rapid adoption of data-intensive applications and expanding mobile connectivity worldwide. This shift is compelling telecom networks to upgrade capacity and efficiency, directly increasing the need for advanced semiconductor solutions capable of handling escalating data volumes and performance expectations.

- In OECD countries, average mobile data usage rose from Nearly 8 GB per month (2022) to Nearly 17 GB per month (2024) per subscription.

- Global mobile broadband subscriptions reached 1.9 billion by mid-2024, while total traffic increased from Nearly 1 ZB (2023) to Nearly 1.3 ZB (2024).

AI & ML Integration Unlocks Next-Gen Semiconductor Opportunities in Telecom

The integration of artificial intelligence and machine learning is emerging as a strategic opportunity in telecommunications, enabling more intelligent, adaptive, and efficient network operations. Standardized approaches to AI/ML adoption are creating a structured pathway for semiconductor innovation and accelerating the transformation of telecom infrastructure toward automated and data-driven performance management.

- ITU-T recommendations, including Y.3142, formally define AI/ML roles in network design, routing, and capacity optimization.

- Semiconductor development is expanding toward AI-capable baseband processors, hardware accelerators, and intelligent RF front ends.

High Production Costs Challenge Semiconductor in Telecommunication Market Expansion

High production costs remain a significant structural restraint in semiconductor manufacturing, particularly for telecom-grade chips that require advanced process technologies. The capital-intensive nature of fabrication and equipment investment creates sustained cost pressures, affecting the scalability, affordability, and supply stability of semiconductors used in high-performance telecommunication networks.

- Advanced wafer fabrication facilities increased in cost from Nearly USD 3 billion (2016) to Nearly USD 5 billion (2020).

- U.S. semiconductor and electronic component manufacturing capital expenditure exceeded USD 16.9 billion in 2022.

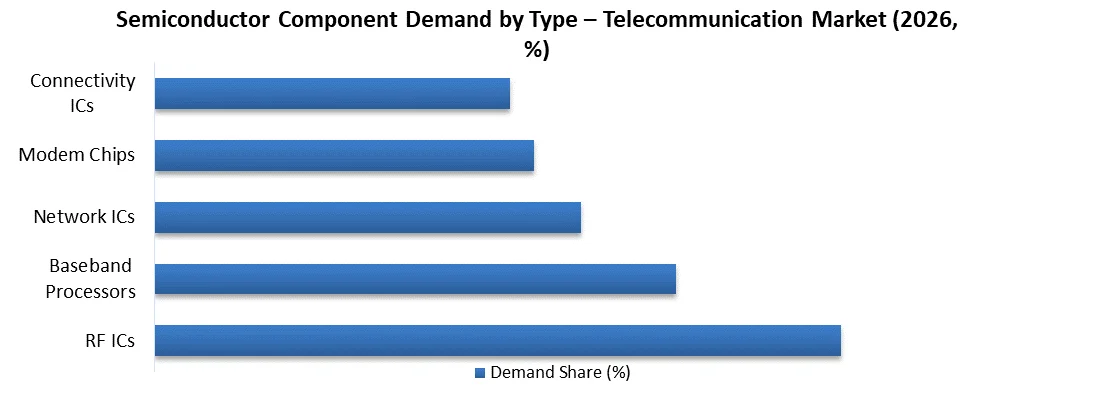

Global Semiconductor in Telecommunication Market Segmentation Analysis

Demand in Semiconductor telecommunication Market is structured by component functionality and deployment use cases. Product-based segmentation reflects the technological building blocks enabling connectivity, while application-based segmentation captures how these semiconductors are embedded across networks, devices, and digital ecosystems as global communication intensity continues to rise.

- By Type: Covers RF ICs, baseband processors, network ICs, modem chips, and connectivity ICs supporting signal processing and data transmission.

- By Application: Includes 5G networks, telecom infrastructure, mobile devices, IoT communication, and network equipment driving

Global Semiconductor in Telecommunication Market Regional Insights: Asia Pacific

Asia Pacific dominates the Semiconductor in Telecommunication Market in 2025, driven by rapid digital adoption, strong government support, and large-scale telecom infrastructure expansion. Extensive mobile penetration and accelerated rollout of next-generation networks have strengthened demand for advanced telecom semiconductors across both developed and emerging economies in the region.

- 5G population coverage surged from nearly 3% in 2020 to about 62% in 2024

- 4G and 3G coverage reached nearly 96% and 98% respectively

- Around USD 220 billion invested in telecom infrastructure during 2019–2024

- 39 commercial 5G networks launched across nine Asia Pacific countries

Global Semiconductor in Telecommunication Market Competitive Landscape

Qualcomm Incorporated

- Fabless semiconductor leader in wireless communication technologies.

- Core strengths: SoCs, multi-mode modems, RF front-end modules, and connectivity ICs.

- Strategic role:

- Enables global adoption of 3G, 4G LTE, and 5G standards.

- Relies on third-party foundries; assembly and testing largely based in Asia Pacific.

Taiwan Semiconductor Manufacturing Company (TSMC)

- World’s largest pure-play semiconductor foundry.

- Operational scale:

- Serves 500+ customers.

- Manufactures 11,800+ semiconductor products.

- Annual capacity exceeds 16 million 12-inch equivalent wafers.

- Strategic importance:

- Core manufacturing enabler for advanced telecom semiconductors globally.

Global Semiconductor in Telecommunication Market Scope:

|

Global Semiconductor in Telecommunication Market |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2032 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 15.4 Billion |

|

Forecast Period 2026 to 2032 CAGR: |

9.4% |

Market Size in 2032: |

USD 28.9 Billion |

|

Global Semiconductor in Telecommunication Market Segment Analysis |

By Type |

RF ICs Baseband Processors Network ICs Modem Chips Connectivity ICs |

|

|

By Application |

5G Networks Telecom Infrastructure Mobile Devices IoT Communication Network Equipment |

||

|

By Technology |

5G Technology Semiconductors 4G / LTE Semiconductors IoT & M2M Semiconductors Network Infrastructure Semiconductors |

||

|

By End Use |

Telecommunications Consumer Electronics Automotive (connected and communication systems) Industrial Applications Defense & Aerospace |

||

Global Semiconductor in Telecommunication Market Key Players

- Qualcomm Incorporated

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Intel Corporation

- Broadcom Inc.

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- NVIDIA Corporation

- Texas Instruments Incorporated

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Marvell Technology Group Ltd.

- Renesas Electronics Corporation

- Microchip Technology Inc.

- ON Semiconductor Corporation

- STMicroelectronics N.V.

- Skyworks Solutions, Inc.

- Qorvo, Inc.

- UNISOC (Shanghai) Technologies Co., Ltd.

- Nordic Semiconductor ASA

- OmniVision Integrated Circuits Group, Inc.

- Sequans Communications

- DB HiTek Co., Ltd.

- Tsinghua Unigroup Co., Ltd.

- Huatian Technology Co., Ltd.

- Rebellions Inc.

- SK Hynix Inc.

- Semiconductor Manufacturing International Corporation (SMIC)

- United Microelectronics Corporation (UMC)

- Murata Manufacturing Co., Ltd.

- Huawei Technologies Co., Ltd.

- Others

Frequently Asked Questions

Asia Pacific dominates due to rapid digital adoption, large-scale 5G rollout, and USD 220 billion investment in telecom infrastructure between 2019–2024.

AI and ML integration enables intelligent, adaptive network operations and drives the development of AI-capable baseband processors, hardware accelerators, and smart RF front ends.

Rapid 5G rollout in China and India drives demand for RF ICs, baseband processors, network chipsets, and power-efficient semiconductors.

High production costs, with wafer fabs costing up to USD 5 billion and U.S. CapEx exceeding USD 16.9 billion, limit semiconductor scalability and affordability.

1. Semiconductor in Telecommunication Market Introduction

1.1. Study Assumptions and Market Definition

1.2. Scope of the Study

1.3. Global Semiconductor in Telecommunication Market Executive Summary

1.4. Market Size (2025) & Forecast (2026-2032)

1.5. Market Size (USD) and Market Share (%) - By Segments, Regions and Country

2. Global Semiconductor in Telecommunication Market: Competitive Landscape

2.1. MMR Competition Matrix

2.2. Competitive Landscape

2.3. Key Players Benchmarking

2.3.1. Company Name

2.3.2. Headquarter

2.3.3. Product Portfolio

2.3.4. Verticals

2.3.5. Total Company Revenue (2025)

2.3.6. Certifications

2.3.7. Global Presence

2.4. Market Structure

2.4.1. Market Leaders

2.4.2. Market Followers

2.4.3. Emerging Players

2.5. Mergers and Acquisitions Details

2.6. Recent Developments

2.7. Market Positioning & Share Analysis

2.7.1. Company Revenue, Semiconductor in Telecommunication Revenue, and Market Share (%)

2.7.2. MMR Competitive Positioning

2.8. Strategic Developments & Partnerships

2.8.1. Mergers, acquisitions, and joint ventures

2.8.2. Expansion into emerging markets

2.8.3. Strategic alliances with OEMs or system integrators

2.8.4. Investments in new production facilities

2.8.5. Sustainability initiatives and green product launches

3. Semiconductor in Telecommunication Market: Dynamics

3.1. Semiconductor in Telecommunication Market Trends

3.2. Semiconductor in Telecommunication Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

3.2.4. Challenges

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

4. Technological Advancements & Product Innovation in the Semiconductor in Telecommunication Market

4.1. Innovations in RF ICs, Baseband Processors, Network Chipsets, and Connectivity ICs

4.2. Advanced Semiconductor Designs for 5G, IoT, and Broadband Networks

4.3. Power-Efficient Semiconductor Solutions for Low-Latency, High-Throughput Telecom Applications

4.4. AI & ML-Enabled Semiconductor Products for Intelligent Network Operations

4.5. Automation and Industry 4.0 Applications in Telecom Semiconductor Manufacturing

5. Global Semiconductor in Telecommunication Market Pricing Analysis (2020–2025)

5.1. Price Trends of Key Semiconductor Components (RF ICs, Baseband, Network ICs)

5.2. Raw Material Cost Structures: Silicon, Rare Earth Materials, and Specialty Chemicals

5.3. Regional Price Variations and Impact on Telecom Equipment Production

5.4. Pricing Dynamics for Advanced, Certified, and AI-Integrated Semiconductor Solutions

6. Semiconductor in Telecommunication Market Supply Chain & Manufacturing Insights

6.1. Key Raw Material Sources and Component Suppliers

6.2. Major Semiconductor Manufacturing Clusters and Industrial Corridors

6.3. Fabrication Processes, Yield Optimization, and Quality Control Practices

6.4. Import Dependency, Global Trade Flows, and Supply Chain Risk Assessment

6.5. Logistics, Distribution Channels, and E-Procurement Trends in Telecom Semiconductors

7. Policy & Regulatory Environment for Semiconductor Production

7.1. Global Manufacturing Standards, Certifications, and Compliance Requirements

7.2. Environmental Regulations Governing Energy, Emissions, and Waste in Semiconductor Production

7.3. Trade Policies, Tariffs, and Non-Tariff Barriers Affecting Semiconductor Supply

7.4. Government Incentives Supporting Advanced Telecom Semiconductor Manufacturing

8. Circular Economy & Sustainability in Semiconductor Production

8.1. Adoption of Circular Economy Principles in Semiconductor Manufacturing

8.2. Integration of Recycled Materials and Resource-Efficient Processes

8.3. Environmental and Economic Benefits of Sustainable Semiconductor Systems

8.4. Industry and Government Initiatives Promoting Sustainable Semiconductor Practices

9. Digitalization & Semiconductor in Telecommunication Market Demand Insights

9.1. Impact of Telecom Digital Transformation on Semiconductor Demand

9.2. Growth of 5G, IoT, and Broadband Networks Driving High-Performance Chip Needs

9.3. Adoption Trends in AI/ML-Integrated Network Infrastructure

9.4. Strategic Role of Semiconductor Solutions in a Digital & Sustainable Telecom Ecosystem

10. Regional Semiconductor in Telecommunication Market Insights

10.1. Asia Pacific: Rapid 5G Rollout and Infrastructure Investments

10.2. North America: Advanced Semiconductor Manufacturing and Innovation Hubs

10.3. Europe: Sustainability-Focused Production and Regulatory Compliance

10.4. Emerging Economies: Growing Telecom Penetration and Infrastructure Development

11. Resource & Environmental Management in Semiconductor Manufacturing

11.1. Water Consumption, Recycling, and Wastewater Treatment Practices

11.2. Energy Efficiency and Carbon Emission Reduction Initiatives

11.3. Material Scarcity, Recycling, and Supply Chain Sustainability

11.4. Cost Implications and Operational Benefits of Resource Management

12. Long-Term Market Outlook & Demand Forecast

12.1. Demand Forecast by Component Type, Application, and Region

12.2. Impact of 5G, High-Speed Data, and AI/ML Integration on Market Size

12.3. Socioeconomic Contributions: Employment, Regional Development, and CSR Activities

12.4. Challenges in Scaling Production: Technology Costs, Raw Material Availability, and Workforce Skills

13. Global Semiconductor in Telecommunication Market Trade & Export Dynamics

13.1. Semiconductor Trade Flows and Key Import/Export Regions

13.2. Supply-Demand Trends Across North America, Europe, and Asia Pacific

13.3. Competitive Positioning of Major Semiconductor Producing Countries

13.4. Trade Barriers, Logistics Constraints, and Export Opportunities

14. Semiconductor in Telecommunication Market: Global Market Size and Forecast by Segmentation (by Value USD Billion) (2025-2032)

14.1. Semiconductor in Telecommunication Market Size and Forecast, by Type (2025-2032)

14.1.1. RF ICs

14.1.2. Baseband Processors

14.1.3. Network ICs

14.1.4. Modem Chips

14.1.5. Connectivity ICs

14.2. Semiconductor in Telecommunication Market Size and Forecast, by Application (2025-2032)

14.2.1. 5G Networks

14.2.2. Telecom Infrastructure

14.2.3. Mobile Devices

14.2.4. IoT Communication

14.2.5. Network Equipment

14.3. Semiconductor in Telecommunication Market Size and Forecast, by Technology (2025-2032)

14.3.1. 5G Technology Semiconductors

14.3.2. 4G / LTE Semiconductors

14.3.3. IoT & M2M Semiconductors

14.3.4. Network Infrastructure Semiconductors

14.4. Semiconductor in Telecommunication Market Size and Forecast, by End Use (2025-2032)

14.4.1. Telecommunications

14.4.2. Consumer Electronics

14.4.3. Automotive (connected and communication systems)

14.4.4. Industrial Applications

14.4.5. Defense & Aerospace

14.5. Semiconductor in Telecommunication Market Size and Forecast, by Region (2025-2032)

14.5.1. North America

14.5.2. Europe

14.5.3. Asia Pacific

14.5.4. Middle East and Africa

14.5.5. South America

15. North America Semiconductor in Telecommunication Market Size and Forecast by Segmentation (by Value USD Billion) (2025-2032)

15.1. North America Semiconductor in Telecommunication Market Size and Forecast, by Type (2025-2032)

15.1.1. RF ICs

15.1.2. Baseband Processors

15.1.3. Network ICs

15.1.4. Modem Chips

15.1.5. Connectivity ICs

15.2. North America Semiconductor in Telecommunication Market Size and Forecast, by Application (2025-2032)

15.2.1. 5G Networks

15.2.2. Telecom Infrastructure

15.2.3. Mobile Devices

15.2.4. IoT Communication

15.2.5. Network Equipment

15.3. North America Semiconductor in Telecommunication Market Size and Forecast, by Technology (2025-2032)

15.3.1. 5G Technology Semiconductors

15.3.2. 4G / LTE Semiconductors

15.3.3. IoT & M2M Semiconductors

15.3.4. Network Infrastructure Semiconductors

15.4. North America Semiconductor in Telecommunication Market Size and Forecast, by End Use (2025-2032)

15.4.1. Telecommunications

15.4.2. Consumer Electronics

15.4.3. Automotive (connected and communication systems)

15.4.4. Industrial Applications

15.4.5. Defense & Aerospace

15.5. North America Semiconductor in Telecommunication Market Size and Forecast, by Country (2025-2032)

15.5.1. United States

15.5.2. Canada

15.5.3. Mexico

16. Europe Semiconductor in Telecommunication Market Size and Forecast by Segmentation (by Value USD Billion) (2025-2032)

16.1. Europe Semiconductor in Telecommunication Market Size and Forecast, by Type (2025-2032)

16.2. Europe Semiconductor in Telecommunication Market Size and Forecast, by Application (2025-2032)

16.3. Europe Semiconductor in Telecommunication Market Size and Forecast, by Technology (2025-2032)

16.4. Europe Semiconductor in Telecommunication Market Size and Forecast, by End Use (2025-2032)

16.5. Europe Semiconductor in Telecommunication Market Size and Forecast, by Country (2025-2032)

16.5.1. United Kingdom

16.5.2. France

16.5.3. Germany

16.5.4. Italy

16.5.5. Spain

16.5.6. Sweden

16.5.7. Austria

16.5.8. Rest of Europe

17. Asia Pacific Semiconductor in Telecommunication Market Size and Forecast by Segmentation (by Value USD Billion) (2025-2032)

17.1. Asia Pacific Semiconductor in Telecommunication Market Size and Forecast, by Type (2025-2032)

17.2. Asia Pacific Semiconductor in Telecommunication Market Size and Forecast, by Application (2025-2032)

17.3. Asia Pacific Semiconductor in Telecommunication Market Size and Forecast, by Technology (2025-2032)

17.4. Asia Pacific Semiconductor in Telecommunication Market Size and Forecast, by End Use (2025-2032)

17.5. Asia Pacific Semiconductor in Telecommunication Market Size and Forecast, by Country (2025-2032)

17.5.1. China

17.5.2. S Korea

17.5.3. Japan

17.5.4. India

17.5.5. Australia

17.5.6. Indonesia

17.5.7. Malaysia

17.5.8. Vietnam

17.5.9. Taiwan

17.5.10. Rest of Asia Pacific

18. Middle East and Africa Semiconductor in Telecommunication Market Size and Forecast by Segmentation (by Value USD Billion) (2025-2032)

18.1. Middle East and Africa Semiconductor in Telecommunication Market Size and Forecast, by Type (2025-2032)

18.2. Middle East and Africa Semiconductor in Telecommunication Market Size and Forecast, by Application (2025-2032)

18.3. Middle East and Africa Semiconductor in Telecommunication Market Size and Forecast, by Technology (2025-2032)

18.4. Middle East and Africa Semiconductor in Telecommunication Market Size and Forecast, by End Use (2025-2032)

18.5. Middle East and Africa Semiconductor in Telecommunication Market Size and Forecast, by Country (2025-2032)

18.5.1. South Africa

18.5.2. GCC

18.5.3. Egypt

18.5.4. Nigeria

18.5.5. Rest of ME&A

19. South America Semiconductor in Telecommunication Market Size and Forecast by Segmentation (by Value USD Billion) (2025-2032)

19.1. South America Semiconductor in Telecommunication Market Size and Forecast, by Type (2025-2032)

19.2. South America Semiconductor in Telecommunication Market Size and Forecast, by Application (2025-2032)

19.3. South America Semiconductor in Telecommunication Market Size and Forecast, by Technology (2025-2032)

19.4. South America Semiconductor in Telecommunication Market Size and Forecast, by End Use (2025-2032)

19.5. South America Semiconductor in Telecommunication Market Size and Forecast, by Country (2025-2032)

19.5.1. Brazil

19.5.2. Argentina

19.5.3. Chile

19.5.4. Colombia

19.5.5. Rest Of South America

20. Company Profile: Key Players

20.1. Cisco Systems, Inc

20.1.1. Company Overview

20.1.2. Business Portfolio

20.1.3. Financial Overview

20.1.4. SWOT Analysis

20.1.5. Strategic Analysis

20.1.6. Recent Developments

20.2. AWS

20.3. Google

20.4. Dell

20.5. HPE

20.6. IBM

20.7. OpenStack

20.8. Microsoft

20.9. VMware

20.10. Databricks

20.11. HashiCorp

20.12. ServiceTitan

20.13. Oracle cloud

20.14. Rackspace

20.15. Alibaba Cloud

20.16. Hewlett Packard Enterprise (HPE)

20.17. Citrix Systems

20.18. Adobe Cloud

20.19. ServiceNow

20.20. Workday

20.21. Fujitsu Cloud

20.22. Tata Communications

20.23. OVHcloud

20.24. Red Hat (IBM subsidiary)

20.25. Nutanix

20.26. SAP Cloud Infrastructure

20.27. Others

21. Key Findings

22. Industry Recommendations

23. Semiconductor in Telecommunication Market: Research Methodology