Paper Straw Market Global Industry Analysis and Forecast (2026-2032)

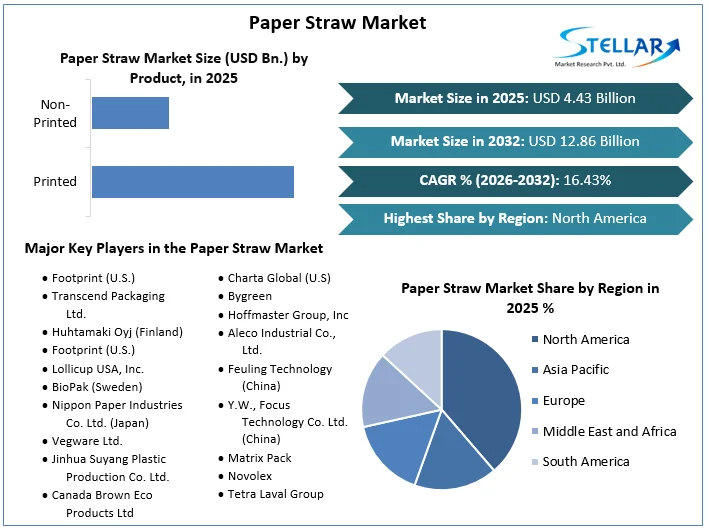

The Paper Straw Market size was valued at USD 4.43 Billion in 2025 and the total Global Paper Straw revenue is expected to grow at a CAGR of 16.43% from 2026 to 2032, reaching nearly USD 12.86 Billion by 2032.

Paper Straw Market Overview

The paper straw market has witnessed substantial growth in recent years, driven by escalating environmental concerns and regulatory shifts away from single-use plastics. With governments, businesses, and consumers alike prioritizing sustainability, paper straws have emerged as a viable alternative to traditional plastic ones. Companies across various sectors, from food and beverage to hospitality and retail, are adopting paper straws as part of their sustainability initiatives. This shift not only addresses consumer demand for eco-friendly paper straws but also aligns with regulatory measures aimed at reducing plastic waste. The major paper straw market leaders such as Transcend Packaging Ltd. have positioned themselves prominently in this space, specializing in sustainable paper-based packaging solutions including paper straws. Their initiatives reflect broader industry trends where sustainability is becoming a central focus. This strategic approach not only reflects broader market movements but also helps companies boost profitability in the paper straw market. Despite these driving factors, the adoption of paper straws faces challenges such as higher production costs and durability compared to plastic alternatives.

Innovations in paper straw material technology and manufacturing processes are expected to address these hurdles, potentially improving durability and reducing costs, thus fostering wider adoption of paper straws. The paper straw market expands in new geographic regions where regulatory pressures are increasing such as France and the UK, legislative measures have been enacted to restrict or ban the use of plastic straws, encouraging widespread adoption of paper alternatives by restaurants, cafes, and retailers. Strategic partnerships between packaging manufacturers and food service industries are also playing a crucial role in driving paper straw market penetration, facilitating their adoption across diverse markets, and enhancing sustainability efforts on a global scale.

The report provides a comprehensive analysis of the global paper straw market, which includes the current market size, overall segmentation analysis (By Product, Material, Application, and Regions), market trends, drivers, restraints, opportunities, scope, and key players. The market value is considered in USD Billion and volume is in Billion Units.

To get more Insights: Request Free Sample Report

Paper Straw Market Dynamics

Shift towards eco-friendly alternatives and stringent environmental regulation for sustainability drives Paper Straw Market growth:

Increasing awareness about the environmental impact of plastic pollution has led to a shift Growing awareness and concern regarding the environmental impact of plastic pollution has led to a shift towards sustainable and environmentally friendly alternatives such as paper straws. The shift is driven by governments, businesses, and consumers, each playing crucial roles in promoting and adopting sustainable packaging solutions to reduce plastic waste. Stringent regulatory practices and bans on single-use plastics in various regions have influenced the paper straws demand. For instance, in Jun 2022 Canada's Ministers of Environment and Health finalized regulations to ban several single-use plastics and straws. The manufacturing and import of these plastics were prohibited by Dec 2022 and sales were banned from December 2023. Canada also going to cease the export of these plastics by the end of 2025, making Canada the first among peer jurisdictions to do so internationally. This increased paper straw demand and regulatory support which raise the investment and innovation in the paper straw sector, expanding the market presence and contributing to broader efforts to reduce plastic waste and promote sustainable packaging solutions.

Technological advancements and innovations in manufacturing processes have revolutionized the production of paper straws, making them increasingly competitive with plastic alternative products. These advancements have addressed critical challenges such as durability, functionality, and performance which increases the adoption of paper straws as a sustainable alternative. For instance, Aardvark Straws one of the leading paper straw manufacturers, has invested in advanced technology to enhance the durability and performance of its paper straws. Their straws are designed to withstand liquid for extended periods without becoming soggy. Collaborations between packaging companies, food and beverage manufacturers, and retailers that align with sustainable practices are fostering the adoption of paper straws. McDonald's UK partnered with Transcend Packaging to trial paper straws in its restaurants as part of a broader commitment to reduce plastic waste. This collaboration helped scale up production and distribution of paper straws across McDonald's locations in the UK. These driving factors collectively contribute to expanding the paper straw market size.

High manufacturing costs and available substituents in the market affect the paper straw market growth:

The rapidly growing paper straw market faces significant challenges that impact its overall expansion and adoption. High manufacturing costs are the primary restraining factor for the adoption of paper straws in the market. Paper straws generally have a higher production cost compared to plastic alternatives due to the specialized materials and manufacturing processes required to enhance their durability and quality. This deters businesses, especially smaller startups or those operating on thin profit margins. The concerns regarding the supply chain such as sourcing sustainable raw materials and ensuring consistent paper straw quality pose ongoing challenges. Paper straw manufacturers must navigate complex supply chains to obtain paper from responsibly managed forests or recycled sources, while also meeting the stringent environmental and regulatory standards. The disruptions in the supply chain impact the production processes and lead to inconsistencies in product availability.

Bioplastics as a competitive substitute pose another restraining factor for paper straws due to their comparable eco-friendly credentials and superior durability and heat resistance. Manufacturers as well as consumers navigating between these alternatives are influenced by the perceived quality and cost-effectiveness of bioplastics. This substitute potentially slows the widespread adoption of paper straws in the market despite their sustainable advantages. Addressing these challenges requires continued innovation in materials and manufacturing processes. By overcoming these challenges, the paper straw market establishes itself as a viable and preferred alternative to plastic, contributing to global efforts to reduce plastic waste and promote sustainable consumption practices.

Potential Opportunities for Paper Straw Market:

Ongoing innovations in manufacturing processes and materials for paper straws enhance product quality and durability, making them more competitive in international markets. For instance, advancements in water-resistant coatings and biodegradable materials improve the durability and functionality of paper straws, appealing to global consumers and businesses seeking eco-friendly alternatives. Increasing global regulations banning single-use plastic products presents a significant opportunity for paper straw manufacturers. The European Union's Single-Use Plastics Directive and Canada's ban on certain single-use plastics create a conducive regulatory environment for paper straws. This allows paper straw manufacturers to benefit from these regulations by exporting their products to these markets or partnering with local distributors to meet growing demand. Collaborations and partnerships with international retailers, food service chains, and beverage companies facilitate market entry and expansion. Establishing robust international supply chains allows paper straw manufacturers to leverage economies of scale, reduce manufacturing costs, and reach new markets efficiently. The growing awareness of plastic pollution globally increases the paper straw demand in various regions. Effective marketing strategies and consumer engagement initiatives, such as social media campaigns and sustainability certifications, differentiate sustainable paper straw products in a competitive international paper straw market.

Export and Import Analysis

The global trade of paper straws involves both export and import activities driven by environmental concerns and regulatory shifts worldwide. In Jun 2022 Canada's Ministers of Environment and Health finalized regulations to ban single-use plastics and straws. The manufacturing and import of these plastics were prohibited by Dec 2022 and sales were banned from December 2023. Canada also going to cease the export of these plastics by the end of 2025, making Canada the first among peer jurisdictions to do so internationally. This drives the import and export of plastic-free products such as paper straws worldwide.

In recent years, there has been a significant increase in the export of paper straws from manufacturing hubs in countries like China, Vietnam, and India. These nations have maximized their production to meet the growing demand primarily from Western markets, where stringent regulations and consumer preferences for eco-friendly alternatives to plastic have fueled the adoption of paper straws. According to the report, in 2023 the total volume of paper straws exported globally amounted to 77,400 units by 4,770 world exporters to 5,704 buyers. China (27,151 shipments), Vietnam (9,961 shipments), and Indonesia (3,867 shipments) are the top paper straw exporters in the world. The total imported volume of 49100 units was imported by 7,178 world importers from 6,051 paper straw suppliers. United States (21,361 shipments), Vietnam (5,350 shipments), and India (3,810 shipments), are the top paper straw importers in the world.

Paper Straw Market Segment Analysis

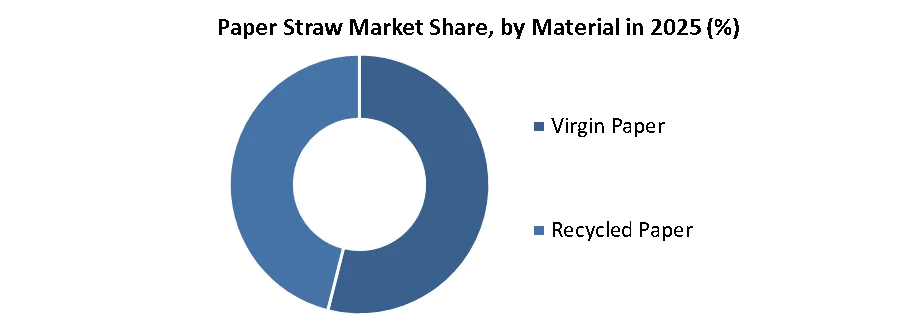

Based on Material, the global paper straw market is segmented into virgin paper and recycled paper. The virgin paper segment dominated the paper straw market in 2025. Virgin paper, sourced directly from wood pulp, maintains superior strength and integrity compared to recycled paper, making it particularly suitable for applications like paper straws that require durability to withstand liquids over extended periods. Concerning direct contact with food, virgin paper straw offers consistent quality and purity which influence the consumer demand to meet stringent hygiene standards crucial in the food and beverage industries. Manufacturers often prefer virgin paper for its reliable performance in production processes, ensuring uniformity and minimizing production defects. Additionally, advancements in sustainable forestry practices and certifications such as Forest Stewardship Council (FSC) ensure responsible sourcing of virgin paper, aligning with growing corporate sustainability goals and regulatory requirements.

By Application, the global paper straw market is segmented into food service, institutional, and household applications.

In 2025, the global paper straw market segmented by application revealed significant dominance in the food service sector, which held the largest market share. The segment's robust growth is driven by increasing adoption in restaurants, cafes, fast food chains, and other food service establishments globally. The shift towards sustainable packaging solutions, prompted by stringent regulations and growing consumer preference for eco-friendly options, has accelerated the paper straws demand. For instance, Starbucks announced plans to eliminate plastic straws from its stores globally by transitioning to paper and compostable straws. Similarly, McDonald's has implemented paper straws in various markets as part of its sustainability strategy to reduce plastic waste. This shift reflects a broader trend where food service giants are embracing eco-friendly solutions to meet consumer demand for greener practices while adhering to regulatory mandates aimed at reducing single-use plastics.

Paper Straw Market Regional Analysis

North America held the largest paper straw market share in 2025 and is expected to grow substantially during the forecast period. This is attributed to stringent environmental regulations, eighteen consumer awareness regarding sustainability, and proactive corporate responsibility initiatives. The countries such as the United States (U.S.) and Canada particular, have played pivotal roles in shaping this market trend. The U.S. has implemented bans or restrictions on single-use plastics, including plastic straws, prompting widespread adoption of paper alternatives. For example, California enacted a statewide ban on plastic straws for dine-in restaurants unless requested by customers, leading many establishments to switch to eco-friendly options like paper straws. Major restaurant chains such as Starbucks and McDonald's have responded to these regulatory changes and consumer preferences by phasing out plastic straws and introducing paper alternatives nationwide. Canada has seen significant growth in the use of paper straws due to similar regulatory measures and consumer demand for sustainable products. Provinces like British Columbia and cities such as Vancouver have implemented bans or restrictions on plastic straws, encouraging businesses to adopt more environmentally friendly options. Canadian companies like Canada Brown Eco Products Ltd. have expanded their paper straw production to meet the increasing demand from restaurants, cafes, and food service providers striving to comply with these regulations and consumer preferences.

Asia-Pacific region represented the fastest-growing paper straw market in 2025, owing to increasing environmental consciousness, regulatory initiatives, and expanding consumer awareness. Countries like Japan and Australia have been at the forefront of this trend. In Japan, stringent regulations and public awareness campaigns against plastic pollution have led to the widespread paper straws adoption. Companies such as Nippon Paper Industries Co. Ltd. have capitalized on this opportunity by producing and supplying sustainable paper straw solutions to meet the market demand.

Paper Straw Market Competitive Landscape

The competitive landscape of the paper straw market is characterized by several key players who differentiate themselves through various strategies, including product innovation, sustainability initiatives, market presence, and customer relationships. Footprint, Transcend Packaging Ltd., Huhtamaki Oyj, Footprint, Lollicup USA, Inc., BioPak, Nippon Paper Industries Co. Ltd., etc. are the leading paper straw companies in the global market. Transcend Packaging Ltd. and Tipi Straws differentiate themselves through continuous product innovation. They focus on developing paper straws that not only meet regulatory standards but also offer enhanced durability and functionality compared to traditional plastic alternatives. For instance, innovations in paper straw design that improve strength and water resistance are key factors in attracting and retaining customers. Vegware Ltd., positions itself as a leader in compostable foodservice packaging, including paper straws, which aligns closely with consumer and regulatory expectations for eco-friendly solutions. Huhtamaki Oyj and Tetra Laval Group leverage their global reach and extensive distribution networks to effectively penetrate new markets and cater to diverse customer demands for sustainable packaging solutions, including paper straws. Companies such as Duni Group (BioPak) focus on understanding customer needs in specific sectors like food service and institutional markets, offering tailored packaging solutions including paper straws that address unique operational and sustainability challenges.

|

Paper Straw Market Scope |

|

|

Market Size in 2025 |

USD 4.43 Billion |

|

Market Size in 2032 |

USD 12.86 Billion |

|

CAGR (2026-2032) |

16.43% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Product Printed Non-Printed |

|

By Material Virgin Paper Recycled Paper |

|

|

By Application Foodservice Institutional Household |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Paper Straw Market

- Footprint (U.S.)

- Transcend Packaging Ltd.

- Huhtamaki Oyj (Finland)

- Footprint (U.S.)

- Lollicup USA, Inc.

- BioPak (Sweden)

- Nippon Paper Industries Co. Ltd. (Japan)

- Vegware Ltd.

- Jinhua Suyang Plastic Production Co. Ltd.

- Canada Brown Eco Products Ltd

- Charta Global (U.S)

- Bygreen

- Hoffmaster Group, Inc

- Aleco Industrial Co., Ltd.

- Feuling Technology (China)

- Y.W., Focus Technology Co. Ltd. (China)

- Matrix Pack

- Novolex

- Tetra Laval Group

- Others

Frequently Asked Questions

The top companies in the Paper Straw Market are Footprint, Transcend Packaging Ltd., Huhtamaki Oyj, Footprint, Lollicup USA, Inc., BioPak, Nippon Paper Industries Co. Ltd., etc.

The growth of the Paper Straw market is driven by increasing environmental awareness and regulatory restrictions on single-use plastics worldwide. Consumers and businesses are embracing sustainable alternatives, propelling the paper straws demand.

Asia-Pacific is the fastest-growing region in the Paper Straw market during the forecast period.

The segments covered in the market report are Product, Material, Application, and Region.

1. Paper Straw Market: Research Methodology

2. Paper Straw Market: Executive Summary

3. Paper Straw Market: Competitive Landscape

4. Potential Areas for Investment

4.1. Stellar Competition Matrix

4.2. Competitive Landscape

4.3. Key Players Benchmarking

4.4. Market Structure

4.4.1. Market Leaders

4.4.2. Market Followers

4.4.3. Emerging Players

4.5. Consolidation of the Market

5. Paper Straw Market: Dynamics

5.1. Market Trends

5.2. Market Drivers

5.3. Market Restraints

5.4. Market Opportunities

5.5. Market Challenges

5.6. PORTER’s Five Forces Analysis

5.7. PESTLE Analysis

5.8. Technology Roadmap

5.9. Strategies for New Entrants to Penetrate the Market

5.10. Regulatory Landscape by Region

5.10.1. North America

5.10.2. Europe

5.10.3. Asia Pacific

5.10.4. Middle East and Africa

5.10.5. South America

6. Paper Straw Market Size and Forecast by Segments (by Value USD Billion and Volume Billion units)

6.1. Paper Straw Market Size and Forecast, by Product (2025-2032)

6.1.1. Printed

6.1.2. Non-Printed

6.2. Paper Straw Market Size and Forecast, by Material (2025-2032)

6.2.1. Virgin Paper

6.2.2. Recycled Paper

6.3. Paper Straw Market Size and Forecast, by Application (2025-2032)

6.3.1. Foodservice

6.3.2. Institutional

6.3.3. Household

6.4. Paper Straw Market Size and Forecast, by Region (2025-2032)

6.4.1. North America

6.4.2. Europe

6.4.3. Asia Pacific

6.4.4. Middle East and Africa

6.4.5. South America

7. North America Paper Straw Market Size and Forecast (by Value USD Billion)

7.1. North America Paper Straw Market Size and Forecast, by Product (2025-2032)

7.1.1. Printed

7.1.2. Non-Printed

7.2. North America Paper Straw Market Size and Forecast, by Material (2025-2032)

7.2.1. Virgin Paper

7.2.2. Recycled Paper

7.3. North America Paper Straw Market Size and Forecast, by Application (2025-2032)

7.3.1. Foodservice

7.3.2. Institutional

7.3.3. Household

7.4. North America Paper Straw Market Size and Forecast, by Country (2025-2032)

7.4.1. United States

7.4.2. Canada

7.4.3. Mexico

8. Europe Paper Straw Market Size and Forecast (by Value USD Billion)

8.1. Europe Paper Straw Market Size and Forecast, by Product (2025-2032)

8.1.1. Printed

8.1.2. Non-Printed

8.2. Europe Paper Straw Market Size and Forecast, by Material (2025-2032)

8.2.1. Virgin Paper

8.2.2. Recycled Paper

8.3. Europe Paper Straw Market Size and Forecast, by Application (2025-2032)

8.3.1. Metallurgical

8.3.2. Ceramic

8.3.3. Chemicals

8.3.4. Others

8.4. Europe Paper Straw Market Size and Forecast, by Country (2025-2032)

8.4.1. UK

8.4.2. France

8.4.3. Germany

8.4.4. Italy

8.4.5. Spain

8.4.6. Sweden

8.4.7. Austria

8.4.8. Rest of Europe

9. Asia Pacific Paper Straw Market Size and Forecast (by Value USD Billion)

9.1. Asia Pacific Paper Straw Market Size and Forecast, by Product (2025-2032)

9.1.1. Printed

9.1.2. Non-Printed

9.2. Asia Pacific Paper Straw Market Size and Forecast, by Material (2025-2032)

9.2.1. Virgin Paper

9.2.2. Recycled Paper

9.3. Asia Pacific Paper Straw Market Size and Forecast, by Application (2025-2032)

9.3.1. Foodservice

9.3.2. Institutional

9.3.3. Household

9.4. Asia Pacific Paper Straw Market Size and Forecast, by Country (2025-2032)

9.4.1. China

9.4.2. S Korea

9.4.3. Japan

9.4.4. India

9.4.5. Australia

9.4.6. Indonesia

9.4.7. Malaysia

9.4.8. Vietnam

9.4.9. Taiwan

9.4.10. Bangladesh

9.4.11. Pakistan

9.4.12. Rest of Asia Pacific

10. Middle East and Africa Paper Straw Market Size and Forecast (by Value USD Billion)

10.1. Middle East and Africa Paper Straw Market Size and Forecast, by Product (2025-2032)

10.1.1. Printed

10.1.2. Non-Printed

10.2. Middle East and Africa Paper Straw Market Size and Forecast, by Material (2025-2032)

10.2.1. Virgin Paper

10.2.2. Recycled Paper

10.3. Middle East and Africa Paper Straw Market Size and Forecast, by Application (2025-2032)

10.3.1. Foodservice

10.3.2. Institutional

10.3.3. Household

10.4. Middle East and Africa Electric Vehicle Traction Motor Market Size and Forecast, by Country (2025-2032)

10.4.1. South Africa

10.4.2. GCC

10.4.3. Egypt

10.4.4. Nigeria

10.4.5. Rest of MEA

11. South America Paper Straw Market Size and Forecast (by Value USD Billion)

11.1. South America Paper Straw Market Size and Forecast, by Product (2025-2032)

11.1.1. Printed

11.1.2. Non-Printed

11.2. South America Paper Straw Market Size and Forecast, by Material (2025-2032)

11.2.1. Virgin Paper

11.2.2. Recycled Paper

11.3. South America Paper Straw Market Size and Forecast, by Application (2025-2032)

11.3.1. Foodservice

11.3.2. Institutional

11.3.3. Household

11.4. South America Paper Straw Market Size and Forecast, by Country (2025-2032)

11.4.1. Brazil

11.4.2. Argentina

11.4.3. Rest of South America

12. Company Profile: Key players

12.1. Footprint (U.S.)

12.1.1. Company Overview

12.1.2. Financial Overview

12.1.3. Business Portfolio

12.1.4. SWOT Analysis

12.1.5. Business Strategy

12.1.6. Recent Developments

12.2. Transcend Packaging Ltd.

12.3. Huhtamaki Oyj (Finland)

12.4. Footprint (U.S.)

12.5. Lollicup USA, Inc.

12.6. BioPak (Sweden)

12.7. Nippon Paper Industries Co. Ltd. (Japan)

12.8. Vegware Ltd.

12.9. Jinhua Suyang Plastic Production Co. Ltd.

12.10. Canada Brown Eco Products Ltd

12.11. Charta Global (U.S)

12.12. Bygreen

12.13. Hoffmaster Group, Inc

12.14. Aleco Industrial Co., Ltd.

12.15. Feuling Technology (China)

12.16. Y.W., Focus Technology Co. Ltd. (China)

12.17. Matrix Pack

12.18. Novolex

12.19. Tetra Laval Group

12.20. Others

13. Key Findings

14. Industry Recommendation