Organic Wine Market - Global Industry Analysis and Forecast 2026-2034

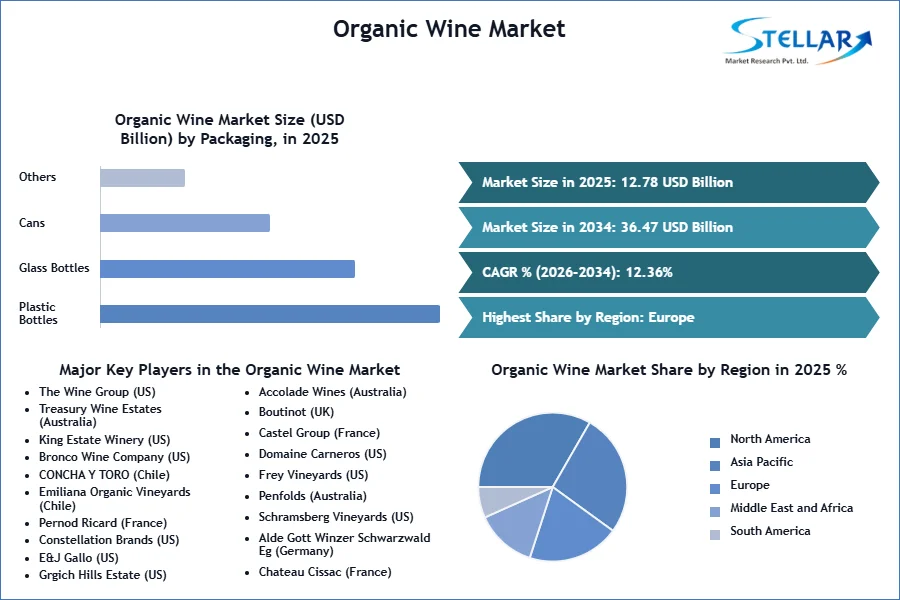

The Organic Wine Market size was valued at USD 12.78 billion in 2025 and the total Organic Wine Market size is expected to grow at a CAGR of 12.36% from 2026 To 2034, reaching nearly USD 36.47 billion by 2034.

Organic Wine Market Overview

Organic wine is a wine produced from grapes that are grown according to organic farming by using synthetic pesticides, herbicides, and fertilizers. As consumers become more health conscious, they increasingly focus on natural products including wine. This shift is driven by way of growing awareness of the potential health risks of artificial chemical substances and flavors in conventional wines. Thus, the increasing customer focus on health and wellness drives the growth of the organic wine market. In 2025, approximately 66% of consumers are willing to pay more for sustainable products. Thus, the growing consumer demand for sustainable products offers a significant opportunity for the organic wine market.

The organic wine market faces significant challenges associated with certification and compliance costs that wine producers require for detailed documentation and regular inspections to ensure adherence to organic farming practices. The market is segmented into type, packaging, distribution channel, and geographic elements. Europe was the dominant region in the organic wine market this is due to the European Union (EU) has played an important role in promoting organic agriculture through complete guidelines and support programs this EU provides financial guidance and incentives for organic farming through applications like the Common Agriculture Policy (CAP). Consumer demand for organic products also helps to boost the growth of organic wine farming in that region. The Wine Group, Treasury Wine Estates, King Estate Winery, Bronco Wine Company, CONCHA Y TORO, and Emiliana Organic Vineyards are most of the leading players in the Organic Wine market.

To get more Insights: Request Free Sample Report

Organic Wine Market Dynamics:

The Increasing Consumer Focus on Health and Wellness Drives the Growth of the Organic Wine Market

The increasing customer focus on health and wellness drives the growth of the organic wine market. As consumers become more health conscious, they increasingly focus on natural products including wine. This shift is driven by way of growing awareness of the potential health risks of artificial chemical substances and flavors in conventional wines. Organic wines are produced without artificial chemical compounds or pesticides. They offer a perceived healthier opportunity, attractive to those who prioritize natural and clean-label products. Organic wine offers these priorities to enhance the growth of the organic wine market. A broader trend towards sustainable living fuels the demand for organic wine. Consumers are not only worried about their health but also about the environmental effects of their purchases. Organic wine manufacturing usually focuses on eco-friendly practices which reverberate with the ones looking to make more responsible choices. This alignment with private and environmental health needs drives the growth of the organic wine market.

Growing Consumer Demand for Sustainable Products is a Significant Opportunity for the Organic Wine Market

The growing consumer demand for sustainable products offers a significant opportunity for the organic wine market. As environmental and health concerns become more prominent, purchasers are increasingly seeking out products that reflect their values together with those that are produced through the use of eco-friendly and ethical practices. Organic wines that are made without artificial pesticides or fertilizers and frequently contain sustainable vineyard management, fit this evolving consumer preference perfectly. This shift in consumer attitudes creates a favorable environment for organic wine manufacturers to capture a dedicated and expanding market. By emphasizing their dedication to sustainability producers can appeal to consumers who are ready to pay a premium for products that align with their environmental values. This trend boosts income ability as well as improves brand loyalty amongst eco-conscious consumers. Furthermore, the growing demand for sustainable products encourages innovation within the organic wine sector. Producers are stimulated to adopt and develop new environment-friendly practices and technologies, additionally improving the quality and attraction of their wines. This innovation results in higher product services and increased market growth in the organic wine market.

Certification and Compliance Costs are Major Challenges of the Organic Wine Market

Certification and compliance costs are the major challenges of the organic wine market. This is due to the inflexible standards required for organic labeling. Producers undergo certification processes that involve detailed documentation and regular inspections to ensure adherence to organic farming practices. These requirements experience high costs as well as demand considerable time and resources from wine producers. Furthermore, wine producers face an increased financial and administrative burden due to the complexity of complying with many worldwide organic rules. Because of these increased expenses, customers find organic wines to be more expensive which reduces their ability to compete in the market as well as affects the growth of the organic wine market. Additionally, to comply with organic requirements the certification procedure frequently requires a significant investment in infrastructure and training which can be difficult for growers switching from conventional to organic techniques. These costs put a strain on the budgets of current producers or discourage new players from obtaining organic certification. As a result, the high expenses of certification affect the overall competitiveness and growth of the organic wine market.

Organic Wine Market Segment Analysis:

By Type, the market is classified into Red Organic Wine and White Organic Wine. The red organic wine held the largest shares in the organic wine market. This is due to the growing demand for red wines which are often related to health benefits and rich flavors. Consumers are increasingly drawn to red organic wines due to the fact they provide a full-bodied flavor profile and are perceived as having extra complex flavors that enchant casual drinkers and wine connoisseurs. This segment consists of an excessive amount of resveratrol, a powerful antioxidant that allows fight free radicals and toxins that may damage cells and organs. The resveratrol in red wines promotes health and longevity. These features of red wine boost the market growth of Organic Wine. The white organic wine segment is expected to hold the largest shares in the forecast year. This is due to the changing consumer alternatives and growing awareness of the specific features of white organic wines. White wines have a lighter profile and are frequently perceived as extra fresh and approachable than red. This makes them popular amongst an extensive range of customers including those who are not ordinary wine drinkers. This popularity of the white organic wine segment helped to maintain its dominance in the forecast year.

By Packaging, the market is classified into Plastic Bottles, Glass bottles, Cans, and Others. The glass bottles held the largest shares in the Organic Wine market. This is due to the awareness of glass as a premium and environment-friendly packaging option. Glass bottles are favored for their ability to maintain the flavor and quantity of wine which is important for organic wines that often bring natural and high-quality production processes. Glass bottles are widely used for their recyclability and sustainability which lead to boosts the growth of the organic wine market. The plastic bottles segment is expected to hold the largest shares in the forecast year. This is due to several factors such as cost-effectiveness, lightweight properties, and advancements in plastic technology that improve the preservation of wine. As the organic wine market continues to grow and evolve the need for more economical and convenient packaging solutions can result in the increasing use of plastic bottles regardless of their less traditional image as compared to glass. The innovations in plastic recycling and biodegradable options ease environmental concerns and make plastic a greater sustainable desire for both producers and consumers.

Organic Wine Market Regional Insight:

Europe was the dominant region in the organic wine market in 2025. The European Union (EU) has played an important role in promoting organic agriculture through complete guidelines and support programs. The EU provides financial guidance and incentives for organic farming through applications like the Common Agriculture Policy (CAP). These applications assist farmers in transitioning to organic practices and maintaining their certification by way of supporting the growth of the organic wine sector. The development in viticulture techniques which include using cover crops and biodynamic practices has advanced soil fitness and grape high-quality. Consumer demand for organic products has been regularly growing in Europe which has led to a boosting growth of the organic wine market in that region. Countries like France and Italy are main with support incorporating sustainable practices into their vineyards consisting of the use of natural pest control techniques to improve biodiversity. In 2025, Europe accounted for over 70% of worldwide organic wine production. France remains the maximum crucial manufacturer with approximately 40% of Europe’s organic wine production. Italy and Spain contribute approximately 25% and 15% respectively. Thus, these contributions and the increasing popularity of organic wine in diverse countries of Europe drive the growth of the Organic Wine Market.

Organic Wine Market Competitive Landscape:

The market is a highly competitive global sector with many participants striving to be leaders. The prominent players operating in the Organic Wine market are constantly adopting various growth strategies to survive in the market. Innovations, product launches, adoption of new technologies, collaboration, and partnership are some of the growth strategies that are adopted by these key players.

The Wine Group and Emiliana Organic Vineyards are the major leading players in the Organic Wine market. The wine group is a prominent player in this market. The Wine Group has been proactive in incorporating sustainable practices into its operations. This includes organic winery management where they avoid synthetic pesticides and fertilizers using instead natural methods to enhance soil health and plant productivity. The company has multiplied its organic wine manufacturing and gives an extensive range of varieties that provide to different consumer preferences. The company focuses on organic wines by the use of natural farming techniques that avoid artificial chemical compounds which demand health-conscious and environmentally aware consumers. Thus, the wine group’s advancements in organic wine manufacturing and commitment to sustainability maintain leadership within the Organic Wine market. Emiliana Organic Vineyards is another leading player in the Organic Wine market. The company is focusing on natural methods that enhance soil health and reduce chemical use. Their commitment extends beyond just organic certification. They also practice biodynamic farming which incorporates holistic methods to winery management that respect natural rhythms and promote biodiversity. The company has also invested in advanced technologies to support sustainable practices. The development in technology and sustainability practices assist Emiliana Organic Vineyards in maintaining its leadership in the Organic Wine Production market.

|

Organic Wine Market Scope |

|

|

Market Size in 2025 |

USD 12.78 Bn. |

|

Market Size in 2034 |

USD 36.47 Bn. |

|

CAGR (2026-2034) |

12.36% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Type

|

|

By Packaging

|

|

|

By Distribution Channel

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Organic Wine Market

- The Wine Group (US)

- Treasury Wine Estates (Australia)

- King Estate Winery (US)

- Bronco Wine Company (US)

- CONCHA Y TORO (Chile)

- Emiliana Organic Vineyards (Chile)

- Pernod Ricard (France)

- Constellation Brands (US)

- E&J Gallo (US)

- Grgich Hills Estate (US)

- Accolade Wines (Australia)

- Boutinot (UK)

- Castel Group (France)

- Domaine Carneros (US)

- Frey Vineyards (US)

- Penfolds (Australia)

- Schramsberg Vineyards (US)

- Alde Gott Winzer Schwarzwald Eg (Germany)

- Chateau Cissac (France)

- Other

Frequently Asked Questions

Ans. North America is expected to lead the Organic Wine Market during the forecast period.

Ans. An analysis of profit trends and projections for companies in the Organic Wine Market is included, offering insights into factors driving profitability, cost management strategies, and financial performance metrics.

Ans. The Organic Wine Market size was valued at USD 12.78 billion in 2025 and the total Organic Wine Market size is expected to grow at a CAGR of 12.36% from 2026 to 2034, reaching nearly USD 36.47 billion by 2034.

Ans. The segments covered in the market report are by Type, Packaging, and Distribution Channel.

1. Organic Wine Market: Research Methodology

2. Organic Wine Market: Executive Summary

3. Organic Wine Market: Competitive Landscape

4. Potential Areas for Investment

4.1. Stellar Competition Matrix

4.2. Competitive Landscape

4.3. Key Players Benchmarking

4.4. Market Structure

4.4.1. Market Leaders

4.4.2. Market Followers

4.4.3. Emerging Players

4.5. Consolidation of the Market

4.6. Import and export of Organic Wine Market

5. Organic Wine Market: Dynamics

5.1. Market Driver

5.1.1. Increasing Consumer Awareness

5.1.2. Innovation in Product Offerings

5.2. Market Trends by Region

5.2.1. North America

5.2.2. Europe

5.2.3. Asia Pacific

5.2.4. Middle East and Africa

5.2.5. South America

5.3. Market Drivers by Region

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

5.4. Market Restraints

5.5. Market Opportunities

5.6. Market Challenges

5.7. PORTER’s Five Forces Analysis

5.8. PESTLE Analysis

5.9. Strategies for New Entrants to Penetrate the Market

5.10. Regulatory Landscape by Region

5.10.1. North America

5.10.2. Europe

5.10.3. Asia Pacific

5.10.4. Middle East and Africa

5.10.5. South America

6. Organic Wine Market Size and Forecast by Segments (by Value and Volume Units)

6.1. Organic Wine Market Size and Forecast, by Type (2026-2034)

6.1.1. Red Organic Wine

6.1.2. White Organic Wine

6.2. Organic Wine Market Size and Forecast, by Packaging (2026-2034)

6.2.1. Plastic Bottles

6.2.2. Glass bottles

6.2.3. Cans

6.2.4. Others

6.3. Organic Wine Market Size and Forecast, by Distribution Channel (2026-2034)

6.3.1. Hypermarkets/Supermarkets

6.3.2. Liquor Stores

6.3.3. Convenience Stores

6.3.4. Online Channels

6.3.5. Others

6.4. Organic Wine Market Size and Forecast, by Region (2026-2034)

6.4.1. North America

6.4.2. Europe

6.4.3. Asia Pacific

6.4.4. Middle East and Africa

6.4.5. South America

7. North America Organic Wine Market Size and Forecast (by Value and Volume Units)

7.1. North America Organic Wine Market Size and Forecast, by Type (2026-2034)

7.1.1. Red Organic Wine

7.1.2. White Organic Wine

7.2. North America Organic Wine Market Size and Forecast, by Packaging (2026-2034)

7.2.1. Plastic Bottles

7.2.2. Glass bottles

7.2.3. Cans

7.2.4. Others

7.3. North America Organic Wine Market Size and Forecast, by Distribution Channel (2026-2034)

7.3.1. Hypermarkets/Supermarkets

7.3.2. Liquor Stores

7.3.3. Convenience Stores

7.3.4. Online Channels

7.3.5. Others

7.4. North America Organic Wine Market Size and Forecast, by Country (2026-2034)

7.4.1. United States

7.4.2. Canada

7.4.3. Mexico

8. Europe Organic Wine Market Size and Forecast (by Value and Volume Units)

8.1. Europe Organic Wine Market Size and Forecast, by Type (2026-2034)

8.1.1. Red Organic Wine

8.1.2. White Organic Wine

8.2. Europe Organic Wine Market Size and Forecast, by Packaging (2026-2034)

8.2.1. Plastic Bottles

8.2.2. Glass bottles

8.2.3. Cans

8.2.4. Others

8.3. Europe Organic Wine Market Size and Forecast, by Distribution Channel (2026-2034)

8.3.1. Hypermarkets/Supermarkets

8.3.2. Liquor Stores

8.3.3. Convenience Stores

8.3.4. Online Channels

8.3.5. Others

8.4. Europe Organic Wine Market Size and Forecast, by Country (2026-2034)

8.4.1. UK

8.4.2. France

8.4.3. Germany

8.4.4. Italy

8.4.5. Spain

8.4.6. Sweden

8.4.7. AustriaValue

8.4.8. Rest of Europe

9. Asia Pacific Organic Wine Market Size and Forecast (by Value and Volume Units)

9.1. Asia Pacific Organic Wine Market Size and Forecast, by Type (2026-2034)

9.1.1. Red Organic Wine

9.1.2. White Organic Wine

9.2. Asia Pacific Organic Wine Market Size and Forecast, by Packaging (2026-2034)

9.2.1. Plastic Bottles

9.2.2. Glass bottles

9.2.3. Cans

9.2.4. Others

9.3. Asia Pacific Organic Wine Market Size and Forecast, by Distribution Channel (2026-2034)

9.3.1. Hypermarkets/Supermarkets

9.3.2. Liquor Stores

9.3.3. Convenience Stores

9.3.4. Online Channels

9.3.5. Others

9.4. Asia Pacific Organic Wine Market Size and Forecast, by Country (2026-2034)

9.4.1. China

9.4.2. S Korea

9.4.3. Japan

9.4.4. India

9.4.5. Australia

9.4.6. Rest of Asia Pacific

10. Middle East and Africa Organic Wine Market Size and Forecast (by Value and Volume Units)

10.1. Middle East and Africa Organic Wine Market Size and Forecast, by Type (2026-2034)

10.1.1. Red Organic Wine

10.1.2. White Organic Wine

10.2. Middle East and Africa Organic Wine Market Size and Forecast, by Packaging (2026-2034)

10.2.1. Plastic Bottles

10.2.2. Glass bottles

10.2.3. Cans

10.2.4. Others

10.3. Middle East and Africa Organic Wine Market Size and Forecast, by Distribution Channel (2026-2034)

10.3.1. Hypermarkets/Supermarkets

10.3.2. Liquor Stores

10.3.3. Convenience Stores

10.3.4. Online Channels

10.3.5. Others

10.4. Middle East and Africa Organic Wine Market Size and Forecast, by Country (2026-2034)

10.4.1. South Africa

10.4.2. GCC

10.4.3. Rest of ME&A

11. South America Organic Wine Market Size and Forecast (by Value and Volume Units)

11.1. South America Organic Wine Market Size and Forecast, by Type (2026-2034)

11.1.1. Red Organic Wine

11.1.2. White Organic Wine

11.2. South America Organic Wine Market Size and Forecast, by Packaging (2026-2034)

11.2.1. Plastic Bottles

11.2.2. Glass bottles

11.2.3. Cans

11.2.4. Others

11.3. South America Organic Wine Market Size and Forecast, by Distribution Channel (2026-2034)

11.3.1. Hypermarkets/Supermarkets

11.3.2. Liquor Stores

11.3.3. Convenience Stores

11.3.4. Online Channels

11.3.5. Others

11.4. South America Organic Wine Market Size and Forecast, by Country (2026-2034)

11.4.1. Brazil

11.4.2. Argentina

11.4.3. Rest of South America

12. Company Profile: Key players

12.1. The Wine Group

12.1.1. Company Overview

12.1.2. Financial Overview

12.1.3. Business Portfolio

12.1.4. SWOT Analysis

12.1.5. Business Strategy

12.1.6. Recent Developments

12.2. Treasury Wine Estates

12.3. King Estate Winery

12.4. Bronco Wine Company

12.5. CONCHA Y TORO

12.6. Emiliana Organic Vineyards

12.7. Pernod Ricard

12.8. Constellation Brands

12.9. E&J Gallo

12.10. Grgich Hills Estate

12.11. Accolade Wines

12.12. Boutinot

12.13. Castel Group

12.14. Domaine Carneros

12.15. Frey Vineyards

12.16. Penfolds

12.17. Schramsberg Vineyards

12.18. Alde Gott Winzer Schwarzwald Eg

12.19. Chateau Cissac

12.20. XX Inc.

13. Key Findings

14. Industry Recommendation