Network as a Service Market Size, Dynamics, Regional Insights, and Market Segment Analysis

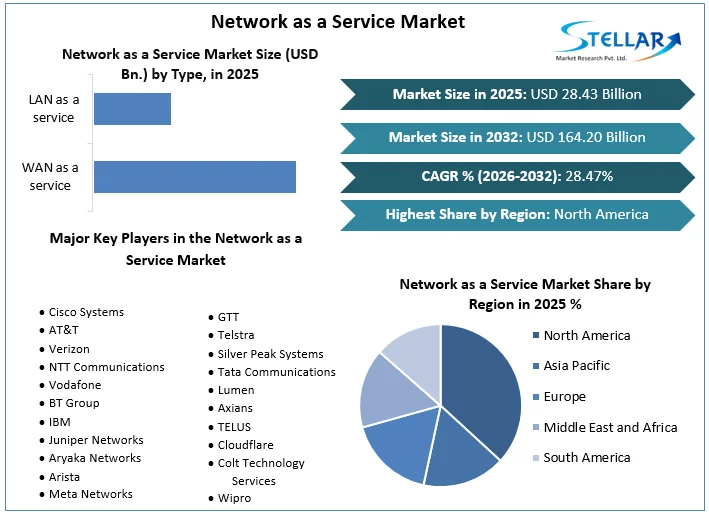

Network as a Service Market size was valued at USD 28.43 Bn. in 2025 and is expected to reach USD 164.20 Bn. by 2032, at CAGR of 28.47%.

Network as a Service Market Overview

Network as a Service (NaaS) is a cloud computing model that allows organizations to lease network services from a third-party provider rather than developing and maintaining their network infrastructure. This model works similarly to other cloud services such as Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS).

The significant shift towards cloud computing has been a major driver for the network as a service market expansion. As of 2023, 94% of U.S. enterprises utilize cloud services, with 67% of their infrastructure being cloud-based and 92% adopting multi-cloud strategies. This trend underscores the growing reliance on cloud technologies, which is expected to fuel the demand for NaaS.

The launch of 5G networks is creating new opportunities for the Network as a service market. 5G technology brings enhancements such as higher speeds, reduced latency, and improved connectivity, which are critical for supporting advanced applications and accommodating a growing number of connected devices. The market faces challenges related to dependency on Wide Area Networks (WANs). WAN reliance can lead to service disruptions and performance issues, such as congestion and latency, which affect the reliability and efficiency of network services.

The Network as a Service market is segmented based on type, application, organization size, and end-user industries. The market is divided into WAN as a Service and LAN as a Service, with WAN as a Service holding the largest market share due to its ability to support cloud-based applications and distributed networks. Regionally, North America dominates the Network as a service market, driven by its advanced technology infrastructure and the presence of leading NaaS providers. The United States and Canada lead this trend, with significant contributions from tech giants and cloud service providers. In contrast, the Asia-Pacific region is anticipated to experience the highest growth rate due to rapid digitalization, increasing internet penetration, and government support for technological advancements.

To get more Insights: Request Free Sample Report

Network as a Service Market Dynamics

Network as a Service Market Driver

The increased adoption of cloud services among enterprises is significantly driving the growth of the Network as a Service market, by boosting the demand for flexible and scalable network solutions. As organizations migrate their operations to cloud platforms such as AWS, Azure, and Google Cloud, they require robust network infrastructure to support seamless connectivity between various cloud environments and applications. Network as a Service (NaaS) addresses this demand by offering network solutions over the cloud and offers a solution by providing on-demand, scalable network infrastructure that integrates seamlessly with cloud services.

This integration ensures that organizations can efficiently manage their network resources without investing heavily in physical hardware or dealing with complex network configurations. As more companies move their operations to the cloud, they require a network that can easily adapt to their changing needs. Network as a Service (NaaS) provides this kind of network by offering it as a service over the cloud, which aligns well with the demands of modern cloud-based environments. As cloud services continue to grow, the need for reliable, secure, and adaptable network solutions like NaaS becomes increasingly critical, further propelling the market's expansion.

- The global cloud computing market, valued at USD 700.41 billion in 2023, is projected to grow to $2342.58 billion by 2032, with CAGR of 16.29%.

- In 2020, 61% of businesses migrated their workloads to the cloud, driven by the need for remote work solutions due to the COVID-19 pandemic. The shift to cloud services was crucial for enabling remote work and maintaining business operations during the crisis.

- As of 2023 94% of US enterprises use cloud services, with 67% of enterprise infrastructure is now cloud-based and 92% adopting a multi-cloud strategy.

- As of 2023, 60% of all corporate data is stored in the cloud, with 48% of businesses opting to keep their most critical data there. This reflects widespread trust in cloud storage for both every day and essential data due to its security and reliability.

- Amazon dominates the cloud computing market. Amazon Web Services holds a 32% share of the market compared to its competitors. The next four leading companies are Azure (20%), Google Cloud (9%), and Alibaba Cloud (6%). Together, just these four companies make up 67% of the entire market share.

Network as a service Market Opportunities

The launch of 5G networks significantly impacts the Network as a Service market by creating opportunities for providers to offer advanced and enhanced network capabilities. 5G technology brings higher speeds, reduced latency, and improved connectivity, which can be integrated into NaaS solutions to deliver superior network performance and functionality.

5G networks enable faster data transmission rates compared to previous generations of mobile networks. This increased speed allows NaaS providers to offer high-bandwidth services that support demanding applications such as high-definition video streaming, large data transfers, and real-time communications. By incorporating 5G technology into their service offerings, NaaS providers can cater to enterprises with high data throughput requirements, enhancing their overall network experience and supporting advanced applications that require rapid data processing.

5G reduces latency, or the delay between sending and receiving data, to unprecedented levels. This low latency is crucial for applications that rely on real-time interactions, such as virtual reality (VR), augmented reality (AR), and autonomous vehicles. NaaS providers can take advantage of 5G's low latency to deliver solutions that enable these applications to run smoothly, offering businesses the opportunity to adopt cutting-edge technology and improve operational efficiency.

5G networks offer improved connectivity and reliability, which is essential for supporting the increasing number of connected devices and the growing Internet of Things (IoT) ecosystem. NaaS providers can utilize 5G's enhanced connectivity to offer scalable and reliable network solutions that accommodate a vast array of IoT devices and applications. This capability is particularly valuable for industries such as manufacturing, healthcare, and smart cities, where reliable and consistent network performance is critical.

- The number of 5G connections worldwide will exceed 1.5 billion by the end of 2023, making it the fastest-growing mobile technology to date. It took 10 years for 3G to reach the same milestone and more than five years for 4G.

Network as a Service Market Challenge

Dependency on WAN Connectivity

Relying on WANs in a network as a service market presents significant challenge that can affect the reliability and performance of services. Wide area networks (WANs) are essential for connecting distributed business locations and facilitating cloud access, but their reliance can lead to several challenges. One major challenge is service disruptions. Since WANs plays an important role in transmitting data across various geographic locations, any disruption in the WAN whether due to hardware failure, network congestion, or outages from service providers can severely affect business operations.

Another major challenge is performance issues related to WAN congestion and latency. As businesses increasingly adopt cloud-based applications and services, they generate significant amounts of data that must travel across the WAN. High volumes of traffic can cause congestion that causes delays in data transmission and degrades application performance. Latency, or delay in data transmission, can still affect the user experience, especially in real-time applications such as video conferencing and online events.

For example, in the early months of the COVID-19 pandemic, many organizations experienced performance degradation of their cloud-based tools due to unprecedented spikes in WAN traffic. The increased demand for remote work and network services has strained the existing WAN infrastructure, resulting in noticeable delays and disruptions in application responsiveness. These performance issues emphasize the need for robust WAN management and optimization of NaaS solutions to ensure reliable and efficient network performance.

Network as a service Market Segmentation

Based On Type, Network as a service market is segmented into WAN as a service and LAN as a service. WAN as service segment held the largest market share of Xx% in 2025 and expected to grow at a CAGR of Xx% during forecasted period (2026-2032). This is due to increasing adoption of cloud-based applications and the need for efficient, secure connectivity across distributed networks. WAN solutions are widely used by companies in various industries, as it provides scalable, on-demand solution for managing wide area networks and allow them to connect multiple branch offices, data centers and cloud environments smoothly.

SD-WAN has quickly become one of the fastest adopting technologies in the industry due to its ability to meet the requirements of modern tech with a robust network focused on scalability, agility, flexibility, security, and compliance. In addition, it provides a high-quality customer experience through a range of branch services at affordable prices. Major companies are launching SD-WAN services to increase growth in specific segments.

According to SMR’s Analysis

- The adoption rates for SD-WAN as a security solution show a mix, with 7% currently using it and 14% in the testing phase. It is anticipated that by 2025, more than 60% of SD-WAN users will embrace the SASE (Secure Access Service Edge) framework for cloud applications.

The growing demand for WAN solutions can be linked to the increasing reliance on cloud services, remote work, and the need for efficient global connectivity. As businesses continue to expand their digital infrastructure and integrate cloud-based applications, WAN as a Service is expected to maintain its dominance in the network as a service market through 2032.

Global revenue for SD-WAN infrastructure is forecast to exceed $17.37 billion in 2023, showing a compound annual growth rate (CAGR) of 33.66% between 2025 and 2032.

Based on Application, Network as a service market is segmented into Cloud and SaaS Connectivity, Bandwidth of demand (BOD), Integrated network security as a service, virtual private network and others.

In 2025, the Cloud and SaaS Connectivity segment led the Network as a Service market with Xx% share. This segment focuses on providing network services specifically for cloud-based applications and Software as a Service (SaaS) platforms. Cloud based service segment dominance is driven by the increasing use of cloud computing and SaaS apps, which require reliable and high-performance network connections. The flexibility and scalability of cloud services make this segment crucial as more businesses use SaaS for tasks like CRM, ERP, and collaboration.

Additionally, with growing concerns over data security and compliance, NaaS providers in Cloud and SaaS Connectivity offer strong security features, including encryption and secure access controls, which are vital for industries with strict regulations. With a projected CAGR of Xx%, the Cloud and SaaS Connectivity segment is expected to remain dominant as more companies moving towards cloud.

Network as a service Market Regional Insights

In 2025, North America dominated the Network as a service Market with a market share of more than Xx %, due to its advanced technology infrastructure and presence of leading NaaS providers. The need for cloud services and digital transformation led businesses in North America to quickly adopt NaaS to improve network efficiency, security, and scalability. Businesses in different sectors have rapidly adopted NaaS to simplify their processes, facilitate remote work, and oversee intricate multi-cloud setups. The strong IT infrastructure in the area enables the widespread adoption of NaaS by providing the essential support for these developments. Moreover, companies in North America are enthusiastic about embracing the latest technologies and frequently utilize NaaS to enhance competitiveness and streamline network management procedures.

The United States and Canada are the leading countries in this trend. In the US, for example, major tech hubs like Silicon Valley and tech giants like Cisco and IBM have been at the forefront of NaaS adoption, offering end-to-end solutions that improve network efficiency, security and scalability. Additionally, the strong presence of cloud service providers such as Amazon Web Services (AWS) and Microsoft Azure has strengthened the Network as a Service market by integrating their services with advanced network solutions.

However, Asia Pacific region is expected to grow at the highest CAGR of Xx% during the forecast period. This is due to rapid digitalization in countries such as China, India and other Southeast Asian countries. Key drivers include increasing internet penetration levels among businesses that are going digital and government efforts in supporting technological advancements. The rising demand for flexible and scalable networking solutions among many SMEs and a move towards cloud services emphasize on growing requirement for NaaS within this area.

Network as a Service Market Competitive Landscape:

The Network as a Service market is highly competitive and fragmented, with well-established and emerging players vying for market share. Major players such as Cisco Systems, AT&T, Verizon, IBM, and Oracle dominate the market, leveraging their extensive technological expertise and robust infrastructure to deliver comprehensive NaaS offerings. These leading companies provide a wide range of services, including virtualized network functions, cloud-based connectivity, and advanced security features, catering to diverse business needs.

In addition to these giants, a number of emerging companies are making progress by introducing innovative solutions that meet specific niche requirements and offer competitive pricing. The market dynamics are further influenced by ongoing advancements in cloud computing, increased adoption of multi-cloud strategies, and the growing need for agile and cost-effective network management solutions.

Cisco Systems, a global leader in networking technology, offers a wide range of NaaS solutions that include advanced network virtualization, security, and integrated cloud services. With a strong financial performance and large market share, Cisco leverages its extensive resources and established customer base to maintain a leading position. On the other hand, Aryaka Networks, an emerging player, specializes in providing a managed NaaS platform with a focus on global connectivity and performance optimization for cloud applications.

Despite being smaller than Cisco, Aryaka has shown promising growth potential by offering innovative solutions that appeal to businesses seeking cost-effective and highly optimized network services. Aryaka’s financial performance, while not as extensive as Cisco's, reflects significant investment and expansion efforts aimed at capturing a niche market. Both companies exemplify different approaches within the NaaS landscape, with Cisco offering broad, established solutions and Aryaka focusing on specialized, agile offerings.

|

Network as a Service Market Scope |

|

|

Market Size in 2025 |

USD 28.43 Bn. |

|

Market Size in 2032 |

USD 164.20 Bn. |

|

CAGR (2026-2032) |

28.47 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Type WAN as a service LAN as a service |

|

By Application Cloud and SaaS Connectivity Bandwidth of demand (BOD) Integrated network security as a service virtual private network Others |

|

|

Based On Organization Type, Large Enterprises SMEs |

|

|

By End-User IT &Telecom Banking, Financial Services and Insurance (BFSI) Manufacturing Healthcare Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Network as a Service Market Key players

- Cisco Systems

- AT&T

- Verizon

- NTT Communications

- Vodafone

- BT Group

- IBM

- Juniper Networks

- Aryaka Networks

- Arista

- Meta Networks

- GTT

- Telstra

- Silver Peak Systems

- Tata Communications

- Lumen

- Axians

- TELUS

- Cloudflare

- Colt Technology Services

- Wipro

Frequently Asked Questions

North America is expected to hold the highest share of the Network as a Service Market.

The Network as a Service Market size was valued at USD 28.43 Billion in 2025 reaching nearly USD 164.20 Billion in 2032.

Launch of 5G Network creates an opportunity for providers to offer advanced and enhanced network capabilities.

The segments covered in the Network as a Service Market report are based on Type, Application, Organization Size and End – User.

1. Network as a Service Market: Research Methodology

2. Network as a Service Market: Executive Summary

2.1. Study Assumption and Market Definition

2.2. Scope of the Study

2.3. Executive Summar

3. Network as a Service Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

4. Network as a Service Market: Dynamics

4.1. Network as a Service Market Trends

4.2. Network as a Service Market Dynamics

4.2.1. Market Driver

4.2.2. Market Restraints

4.2.3. Market Opportunities

4.2.4. Market Challenges

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

4.5. Regulatory Landscape by Region

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Middle East and Africa

4.5.5. South America

5. Network as a Service Market Size and Forecast by Segments (by Value in USD Million)

5.1. Network as a Service Market Size and Forecast, by Type (2025-2032)

5.1.1. WAN as a service

5.1.2. LAN as a service

5.2. Network as a Service Market Size and Forecast, by Application (2025-2032)

5.2.1. Cloud and SaaS Connectivity

5.2.2. Bandwidth of demand (BOD)

5.2.3. Integrated network security as a service

5.2.4. virtual private network

5.2.5. Others

5.3. Network as a Service Market Size and Forecast, by Organisation Type (2025-2032)

5.3.1. Large Enterprises

5.3.2. SMEs

5.4. Network as a Service Market Size and Forecast, by End-User (2025-2032)

5.4.1. IT &Telecom

5.4.2. Banking, Financial Services and Insurance (BFSI)

5.4.3. Manufacturing

5.4.4. Healthcare

5.4.5. Others

5.5. Network as a Service Market Size and Forecast, by region (2025-2032)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Network as a Service Market Size and Forecast (by Value in USD Million)

6.1. North America Network as a Service Market Size and Forecast, by Type (2025-2032)

6.1.1. WAN as a service

6.1.2. LAN as a service

6.2. North America Network as a Service Market Size and Forecast, by Application (2025-2032)

6.2.1. Cloud and SaaS Connectivity

6.2.2. Bandwidth of demand (BOD)

6.2.3. Integrated network security as a service

6.2.4. virtual private network

6.2.5. Others

6.3. North America Network as a Service Market Size and Forecast, by Organisation Type (2025-2032)

6.3.1. Large Enterprises

6.3.2. SMEs

6.4. North America Network as a Service Market Size and Forecast, by End-User (2025-2032)

6.4.1. IT &Telecom

6.4.2. Banking, Financial Services and Insurance (BFSI)

6.4.3. Manufacturing

6.4.4. Healthcare

6.4.5. Others

6.5. North America Network as a Service Market Size and Forecast, by Country (2025-2032)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Network as a Service Market Size and Forecast (by Value in USD Million)

7.1. Europe Network as a Service Market Size and Forecast, by Type (2025-2032)

7.1.1. WAN as a service

7.1.2. LAN as a service

7.2. Europe Network as a Service Market Size and Forecast, by Application (2025-2032)

7.2.1. Cloud and SaaS Connectivity

7.2.2. Bandwidth of demand (BOD)

7.2.3. Integrated network security as a service

7.2.4. virtual private network

7.2.5. Others

7.3. Europe Network as a Service Market Size and Forecast, by Organisation Type (2025-2032)

7.3.1. Large Enterprises

7.3.2. SMEs

7.4. Europe Network as a Service Market Size and Forecast, by End-User (2025-2032)

7.4.1. IT &Telecom

7.4.2. Banking, Financial Services and Insurance (BFSI)

7.4.3. Manufacturing

7.4.4. Healthcare

7.4.5. Others

7.5. Europe Network as a Service Market Size and Forecast, by Country (2025-2032)

7.5.1. UK

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Austria

7.5.8. Rest of Europe

8. Asia Pacific Network as a Service Market Size and Forecast (by Value in USD Million)

8.1. Asia Pacific Network as a Service Market Size and Forecast, by Type (2025-2032)

8.1.1. WAN as a service

8.1.2. LAN as a service

8.2. Asia Pacific Network as a Service Market Size and Forecast, by Application (2025-2032)

8.2.1. Cloud and SaaS Connectivity

8.2.2. Bandwidth of demand (BOD)

8.2.3. Integrated network security as a service

8.2.4. virtual private network

8.2.5. Others

8.3. Asia Pacific Network as a Service Market Size and Forecast, by Organisation Type (2025-2032)

8.3.1. Large Enterprises

8.3.2. SMEs

8.4. Asia Pacific Network as a Service Market Size and Forecast, by End-User (2025-2032)

8.4.1. IT &Telecom

8.4.2. Banking, Financial Services and Insurance (BFSI)

8.4.3. Manufacturing

8.4.4. Healthcare

8.4.5. Others

8.5. Asia Pacific Network as a Service Market Size and Forecast, by Country (2025-2032)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. Indonesia

8.5.7. Malaysia

8.5.8. Vietnam

8.5.9. Taiwan

8.5.10. Bangladesh

8.5.11. Pakistan

8.5.12. Rest of Asia Pacific

9. Middle East and Africa Network as a Service Market Size and Forecast (by Value in USD Million)

9.1. Middle East and Africa Network as a Service Market Size and Forecast, by Type (2025-2032)

9.1.1. WAN as a service

9.1.2. LAN as a service

9.2. Middle East and Africa Network as a Service Market Size and Forecast, by Application (2025-2032)

9.2.1. Cloud and SaaS Connectivity

9.2.2. Bandwidth of demand (BOD)

9.2.3. Integrated network security as a service

9.2.4. virtual private network

9.2.5. Others

9.3. Middle East and Africa Network as a Service Market Size and Forecast, by Organisation Type (2025-2032)

9.3.1. Large Enterprises

9.3.2. SMEs

9.4. Middle East and Africa Network as a Service Market Size and Forecast, by End-User (2025-2032)

9.4.1. IT &Telecom

9.4.2. Banking, Financial Services and Insurance (BFSI)

9.4.3. Manufacturing

9.4.4. Healthcare

9.4.5. Others

9.5. Middle East and Africa Network as a Service Market Size and Forecast, by Country (2025-2032)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Egypt

9.5.4. Nigeria

9.5.5. Rest of ME&A

10. South America Network as a Service Market Size and Forecast (by Value in USD Million)

10.1. South America Network as a Service Market Size and Forecast, by Type (2025-2032)

10.1.1. WAN as a service

10.1.2. LAN as a service

10.2. South America Network as a Service Market Size and Forecast, by Application (2025-2032)

10.2.1. Cloud and SaaS Connectivity

10.2.2. Bandwidth of demand (BOD)

10.2.3. Integrated network security as a service

10.2.4. virtual private network

10.2.5. Others

10.3. South America Network as a Service Market Size and Forecast, by Organisation Type (2025-2032)

10.3.1. Large Enterprises

10.3.2. SMEs

10.4. South America Network as a Service Market Size and Forecast, by End-User (2025-2032)

10.4.1. IT &Telecom

10.4.2. Banking, Financial Services and Insurance (BFSI)

10.4.3. Manufacturing

10.4.4. Healthcare

10.4.5. Others

10.5. South America Network as a Service Market Size and Forecast, by Country (2025-2032)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest of South America

11. Company Profile: Key players

11.1. Cisco Systems

11.1.1. Company Overview

11.1.2. Financial Overview

11.1.3. Business Portfolio

11.1.4. SWOT Analysis

11.1.5. Business Strategy

11.1.6. Recent Developments

11.2. AT&T

11.3. Verizon

11.4. NTT Communications

11.5. Vodafone

11.6. BT Group

11.7. IBM

11.8. Juniper Networks

11.9. Aryaka Networks

11.10. Arista

11.11. Meta Networks

11.12. GTT

11.13. Telstra

11.14. Silver Peak Systems

11.15. Tata Communications

11.16. Lumen

11.17. Axians

11.18. TELUS

11.19. Cloudflare

11.20. Colt Technology Services

11.21. Wipro

12. Key Findings

13. Industry Recommendations