Medical Sensors Market Global Industry Analysis and Forecast (2026-2032) By Type, Technology, end user and Application

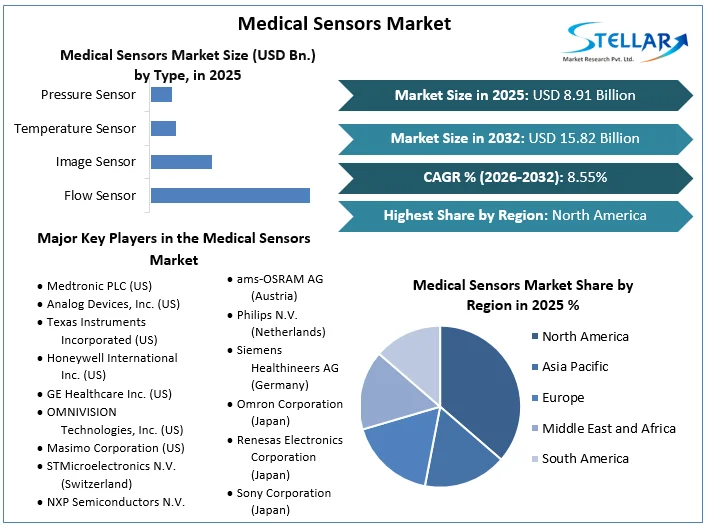

Global Medical Sensors Market size was valued at USD 8.91 Bn. in 2025 and is expected to reach USD 15.82 Bn. by 2032, at a CAGR of 8.55%.

Medical Sensors Market Overview

The medical sensors market involves the development and deployment of devices that measure, monitor, and analyze physiological signals and health conditions. These sensors, including temperature, pressure, flow, and image sensors, are crucial for diagnostics, patient monitoring, and therapeutic applications. The market supports a range of applications, from chronic disease management to real-time health monitoring, enhancing patient outcomes and healthcare efficiency. The growing demand for remote and personalized healthcare solutions is the primary driver of the medical sensors market. Wearable and networked sensor technologies have advanced to allow for real-time health monitoring, improved chronic illness management, and early disease identification. Furthermore, the rise of telemedicine and the elderly population are driving the market's growth.

In 2021, the medical sensors market saw the dominance of temperature sensors, crucial for monitoring body temperature in various medical contexts, including RF hyperthermia treatments and critical care, as well as during the COVID-19 pandemic. Hospitals led the end-user segment due to their financial resources, high patient volumes, and extensive care capabilities.

North America held the largest medical sensors market share in 2025, driven by favourable reimbursement policies, advanced technology integration, and a growing aging population, with key players like Medtronic, Honeywell, and Abbott spearheading innovation. Conversely, the Asia-Pacific medical sensors market is projected to have the highest growth, fuelled by increasing demand for diagnostic imaging and patient monitoring, particularly in China and India. China's large elderly population and governmental support, combined with India's rising need for advanced monitoring solutions, are significant growth drivers.

- Medtronic reported that FY23 revenue of USD 2.262 billion increased by 2.4%.Q4 revenue of USD 595 million increased by 3.0%.

- In 2025, Medtronic Diabetes received U.S. FDA approval for the world's first approval for the MiniMed 780G System with Simplera Sync, a disposable, all-in-one sensor.

- Double-digit growth in Western Europe in Q4 was based on strong continued adoption of the MiniMed 780G system and an associated increase in CGM attachment rates based on the strength of the GuardianTM 4 sensor.

To get more Insights: Request Free Sample Report

Medical Sensors Market Trend

The Evolution of Wearable Sensors through Emerging Materials and Nano Architecture Is Set To Transform the Medical Sensors Market

Wearable sensors built for telehealth, which use novel materials and nanoarchitecture, are expected to significantly boost the medical sensor market. These new sensors, which are frequently manufactured from cutting-edge materials like graphene and flexible polymers, offer increased sensitivity, durability, and comfort. The entire concept of nanoarchitecture, which implies detailed molecular design, enables the development of ultra-compact, high-performance sensors capable of monitoring numerous health metrics in real time.

The integration of these sensors into wearable devices allows for continuous health monitoring, which provides crucial data for telehealth applications in the medical sensor market. This technology not only improves remote diagnoses but also enables proactive disease management and personalized treatment strategies in the medical sensor market. As telehealth use grows, driven by the desire for convenient and affordable healthcare, the demand for these sophisticated wearable sensors will skyrocket. Their ability to provide precise, real-time health insights combines with the increased emphasis on preventive care and patient engagement, propelling the medical sensor market forward.

For instance,

- In 2022, NanoScent developed a wearable sensor using nano technology for early detection of respiratory conditions and disease, highlighting advances in nano architectonics.

- In 2023, Johnson & Johnson merged with Auris Health, boosting its capabilities in medical sensors for minimally invasive surgeries.

- In 2024, Siemens Healthineers acquired Epigenomics AG, enhancing its portfolio with innovative sensor technology for genetic and molecular diagnostics.

Medical Sensors Market Dynamics

Sensor Miniaturization and Digitization to Meet the Growing Demand in Medical Sensors Market

Miniaturization is essential for enhancing the functionality and portability of medical devices in the medical sensors market. It enables the integration of compact, lightweight sensors into smaller devices that can seamlessly connect to mobile apps, providing patients with detailed personal health data. This advancement not only improves the safety of medical pumps by detecting even the smallest air bubbles but also benefits respiratory care with the development of portable CPAP machines and oxygen concentrators.

In the medical sensors market, miniaturization plays a crucial role in minimally invasive surgery, where smaller sensors allow for precise monitoring during procedures while enabling smaller incisions. This leads to better patient outcomes and reduced hospital stays. One example is the integration of advanced sensors in cataract surgery that monitor eye pressure during tiny incisions. Sensor fusion, which combines multiple digital sensor outputs, creates highly accurate, integrated signals that enhance diagnostics and provide deeper insights in the medical sensors market.

The medical sensors market has witnessed significant advancements due to the impact of miniaturization. It has improved device functionality, safety, and sustainability while expanding applications across various medical fields. As the demand for portable, connected, and precise medical devices continues to grow, the medical sensors market will likely see further innovations in miniaturization to meet the evolving needs of healthcare professionals and patients.

For instance,

- In 2021, Medtronic launched the Guardian Connect system, utilizing small, accurate sensors for continuous glucose monitoring, enhancing diabetes management through digital connectivity.

- In 2022, Apple released the Apple Watch Series 7, incorporating advanced miniaturized sensors for improved health monitoring, including blood oxygen and ECG measurements.

- In 2023, Medtronic partnered with AstraZeneca to integrate miniaturized sensors into remote monitoring solutions for chronic disease management.

Guarding Patient Data Overcoming Cyber Security Challenges in the Medical Sensors Market

Data breaches in connected medical devices present a significant challenge to the growth of the medical sensors market. As these devices gather and transmit sensitive health information, any security breaches can compromise patient privacy, diminish trust, and result in costly legal consequences for manufacturers. Concerns regarding data security may discourage healthcare providers and patients from embracing new technologies, thereby hindering medical sensors market expansion. Furthermore, stringent regulatory requirements and compliance costs aimed at mitigating these risks can escalate operational expenses for companies within the market.

To address these challenges, it is essential for the medical sensors market to invest in robust cyber security measures, secure data transmission protocols, and regular system audits. Implementing effective data security solutions will be critical to sustaining growth in the medical sensors market, fostering innovation, and ensuring the widespread acceptance of advanced medical sensors.

Medical Sensors Market Segment Analysis

Based on Type, the temperature sensor dominated the medical sensors market in 2025 and is expected to continue its dominance during the forecast period. Temperature sensors are widely used in various medical applications in the medical sensors market, such as monitoring body temperature during RF hyperthermia treatments, measuring patient surface temperature during MRI or fMRI procedures, and in research and development for NMR/MRI systems. These medical sensors are crucial for monitoring patient body temperature, especially in critical care units and during the COVID-19 pandemic for fever detection.

For instance,

- In May 2020, GOQii, a healthcare firm, released Vital 3.0, which includes temperature sensors capable of measuring heart rate, body temperature, and blood pressure, reducing the need for frequent contact between COVID-19 patients and caregivers.

- In February 2020, Texas Instruments increased their temperature sensor portfolio with the introduction of linear thermistors, which provide about 50% more accuracy than negative temperature coefficient sensors, even in harsh settings.

The pressure sensor segment also held a significant market share in the medical sensors market in 2025, driven by its use in monitoring blood pressure and respiratory functions. Pressure sensors are integral to devices such as blood pressure monitors and ventilators, offering precise measurements crucial for patient management. Both temperature and pressure sensors are expected to remain dominant in the medical sensor market due to their critical roles in patient monitoring and diagnostic accuracy.

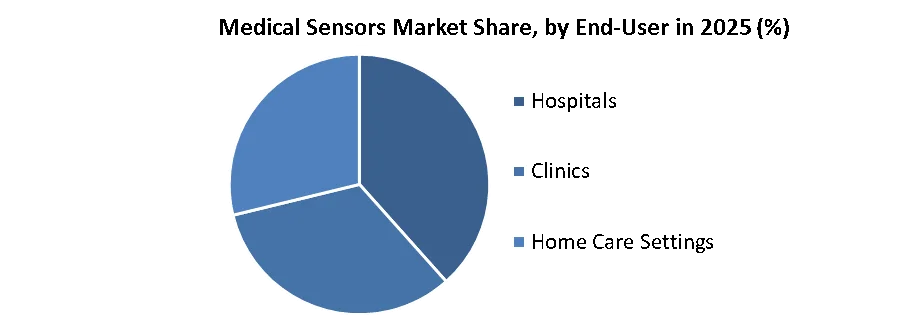

Based on End-User, in 2025, the hospitals sub segment continued to dominate the medical sensors market, owing to their stronger financial resources, high patient numbers, and availability of skilled employees. Hospitals can treat a huge number of patients while producing significant money and keeping a strong client base, which is essential in the medical sensors market. High patient churn is frequently the outcome of providing high-quality care and a wide choice of services in the medical sensors market.

The clinics sub-segment was the second-largest end-user group in the medical sensors market in 2025. Clinics profit from increased patient demand for outpatient services and preventative treatment, which encourages the use of medical sensors for diagnosis and monitoring. The use of medical sensors in clinics improves patient care by allowing for faster interventions and better health outcomes. As the healthcare landscape advances, hospitals and clinics are projected to continue to use advanced medical sensors to improve patient monitoring and treatment efficacy over the forecast period.

For instance,

- In 2024, GE Healthcare partnered with Samsung BioLogics to develop advanced wearable sensors for real-time patient monitoring in clinics, enhancing outpatient care and data integration.

- In 2023. Stryker acquired OrthoSpace, integrating its sensor technology into hospital surgical tools for improved precision in orthopaedic procedures.

- In 2022. Boston Scientific launched the VisiScope system, providing hospitals with high-precision sensors for endoscopic procedures, improving surgical outcomes and patient monitoring.

Medical Sensors Market Regional Insights

In 2025, the North American medical sensors market dominated the market with the largest market share of the medical sensors market and is expected to maintain this position throughout the forecast period. The United States, in particular, benefits from favourable reimbursement policies and a growing aging population, which increases the demand for chronic disease management solutions. Additionally, the integration of advanced technologies into medical sensors enhances the functionality and reliability of medical devices.

This combination of factors positions North America as a key player in the medical sensors market, ensuring continued growth and development in the coming years. The region's supremacy can be attributed to the presence of leading companies such as Medtronic, Honeywell, and Abbott. These companies are pivotal in driving innovation and developing cutting-edge medical sensor technologies.

The medical sensors market in Asia Pacific is projected to register the highest growth during the forecast period. The Asia Pacific medical sensors market is driven by the increasing demand for diagnostic imaging and patient monitoring devices. The China medical sensors market accounted for the largest share of the market in 2025, and a similar trend is expected to continue during the forecast period. Important factors driving market growth in China include the growing elderly population and support from the government for healthcare services. India is projected to register the highest growth during the forecast period owing to an increase in demand for advanced and connected devices, especially for patient monitoring purposes. Due to expensive treatment in hospitals, there has been an increase in the adoption of remote monitoring systems, leading to a rise in demand for medical sensors market.

For instance,

- In 2021, Siemens Healthineers launched the SOMATOM X.cite CT scanner in China, featuring advanced imaging sensors for improved diagnostic capabilities.

- In 2021, Philips partnered with China’s National Health Commission to integrate advanced diagnostic sensors into local healthcare systems, enhancing diagnostic imaging and patient monitoring.

- In 2023, Philips collaborated with Indian Institute of Technology (IIT) Delhi to advance sensor technology for remote monitoring systems in India.

- In 2024, Toshiba Medical Systems unveiled the Aquilion One Prism Edition CT scanner in China, featuring cutting-edge sensors for enhanced diagnostic imaging.

Medical Sensors Market Competitive Landscape

The medical sensors market is highly competitive, with major competitors including Medtronic, Abbott, Philips, and Siemens Healthcare. These companies dominate the market with cutting-edge technologies for a wide range of sensor types, including glucose monitoring, temperature sensors, and imaging sensors. Medtronic and Abbott are particularly strong in diabetes management and implantable sensors, whereas Philips and Siemens Healthineers specialize in advanced diagnostic and imaging sensors. As demand for precision medicine and remote monitoring rises, these top players are projected to maintain their competitive advantage through continued innovation and strategic alliances, accelerating growth in the medical sensors market.

Medical Sensors Market Scope

|

Medical Sensors Market |

|

|

Market Size in 2025 |

USD 8.91 Bn. |

|

Market Size in 2032 |

USD 15.82 Bn. |

|

CAGR (2026-2032) |

8.55% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Medical Sensors Market Segments |

By Type Flow Sensor Image Sensor Temperature Sensor Pressure Sensor Other Types |

|

By Technology Wearable Sensors Implantable Sensors Wireless Others |

|

|

|

By Application Diagnostic Therapeutic Monitoring Wellness and Fitness Others |

|

|

By End-User Hospitals Clinics Home Care Settings Others |

|

Regional Scope |

North America – United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa – South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Medical Sensors Market Key players

North America

- Medtronic PLC (US)

- Analog Devices, Inc. (US)

- Texas Instruments Incorporated (US)

- Honeywell International Inc. (US)

- GE Healthcare Inc. (US)

- OMNIVISION Technologies, Inc. (US)

- Masimo Corporation (US)

Europe

- STMicroelectronics N.V. (Switzerland)

- NXP Semiconductors N.V. (Netherlands)

- Sensirion AG (Switzerland)

- ams-OSRAM AG (Austria)

- Philips N.V. (Netherlands)

- Siemens Healthineers AG (Germany)

Asia Pacific

- Omron Corporation (Japan)

- Renesas Electronics Corporation (Japan)

- Sony Corporation (Japan)

- Samsung Electronics Co., Ltd. (South Korea)

- Toshiba Corporation (Japan)

- Fujifilm Holdings Corporation (Japan)

Middle East and Africa (MEA)

- Biovac (South Africa)

Frequently Asked Questions

North America is expected to dominate the Medical Sensors Market during the forecast period.

The Medical Sensors Market size is expected to reach USD 8.91 Billion by 2025.

The major top players in the Global Medical Sensors Market are Medtronic PLC (US), Analog Devices, Inc. (US), Honeywell International Inc. (US), Siemens Healthineers AG (Germany), Samsung Electronics Co., Ltd. (South Korea) and others.

The Global Medical Sensors Market growth is driven by technological advancements, increasing chronic disease prevalence, rising healthcare demand, growing aging population, and the push for remote patient monitoring and personalized medicine.

1. Medical Sensors Market: Research Methodology

2. Medical Sensors Market Introduction

2.1. Study Assumption and Market Definition

2.2. Scope of the Study

2.3. Executive Summary

3. Global Medical Sensors Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Product Segment

3.3.3. End-user Segment

3.3.4. Revenue (2025)

3.3.5. Company Headquarter

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

4. Medical Sensors Market: Dynamics

4.1. Medical Sensors Market Trends

4.2. Medical Sensors Market Dynamics

4.2.1.1. Drivers

4.2.1.2. Restraints

4.2.1.3. Opportunities

4.2.1.4. Challenges

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

4.5. Technological Roadmap

4.6. Regulatory Landscape by Region

4.6.1. North America

4.6.2. Europe

4.6.3. Asia Pacific

4.6.4. Middle East and Africa

4.6.5. South America

5. Medical Sensors Market: Global Market Size and Forecast (Value in USD Million) (2025-2032)

5.1. Medical Sensors Market Size and Forecast, By Type 2025-2032)

5.1.1. Flow Sensor

5.1.2. Image Sensor

5.1.3. Temperature Sensor

5.1.4. Pressure Sensor

5.1.5. Other Types

5.2. Medical Sensors Market Size and Forecast, By Technology (2025-2032)

5.2.1. Wearable Sensors

5.2.2. Implantable Sensors

5.2.3. Wireless

5.2.4. Others

5.3. Medical Sensors Market Size and Forecast, By Application (2025-2032)

5.3.1. Diagnostic

5.3.2. Therapeutic

5.3.3. Monitoring

5.3.4. Wellness and Fitness

5.3.5. Others

5.4. Medical Sensors Market Size and Forecast, By End-User (2025-2032)

5.4.1. Hospitals

5.4.2. Clinics

5.4.3. Home Care Settings

5.4.4. Others

5.5. Medical Sensors Market Size and Forecast, by Region (2025-2032)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Medical Sensors Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

6.1. North America Medical Sensors Market Size and Forecast, By Type (2025-2032)

6.1.1. Flow Sensor

6.1.2. Image Sensor

6.1.3. Temperature Sensor

6.1.4. Pressure Sensor

6.1.5. Other Types

6.2. North America Medical Sensors Market Size and Forecast, By Technology (2025-2032)

6.2.1. Wearable Sensors

6.2.2. Implantable Sensors

6.2.3. Wireless

6.2.4. Others

6.3. North America Medical Sensors Market Size and Forecast, By Application (2025-2032)

6.3.1. Diagnostic

6.3.2. Therapeutic

6.3.3. Monitoring

6.3.4. Wellness and Fitness

6.3.5. Others

6.4. North America Medical Sensors Market Size and Forecast, By End-User (2025-2032)

6.4.1. Hospitals

6.4.2. Clinics

6.4.3. Home Care Settings

6.4.4. Others

6.5. North America Medical Sensors Market Size and Forecast, by Country (2025-2032)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Medical Sensors Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

7.1. Europe Medical Sensors Market Size and Forecast, By Type (2025-2032)

7.2. Europe Medical Sensors Market Size and Forecast, By Technology (2025-2032)

7.3. Europe Medical Sensors Market Size and Forecast, by Country (2025-2032)

7.3.1. United Kingdom

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Russia

7.3.8. Rest of Europe

8. Asia Pacific Medical Sensors Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

8.1. Asia Pacific Medical Sensors Market Size and Forecast, By Type (2025-2032)

8.2. Asia Pacific Medical Sensors Market Size and Forecast, By Technology (2025-2032)

8.3. Asia Pacific Medical Sensors Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. ASEAN

8.3.7. Rest of Asia Pacific

9. Middle East and Africa Medical Sensors Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

9.1. Middle East and Africa Medical Sensors Market Size and Forecast, By Type (2025-2032)

9.2. Middle East and Africa Medical Sensors Market Size and Forecast, By Technology (2025-2032)

9.3. Middle East and Africa Medical Sensors Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Nigeria

9.3.4. Rest of ME&A

10. South America Medical Sensors Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

10.1. South America Medical Sensors Market Size and Forecast, By Type (2025-2032)

10.2. South America Medical Sensors Market Size and Forecast, By Technology (2025-2032)

10.3. South America Medical Sensors Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest Of South America

11. Company Profile: Key Players

11.1. Medtronic PLC (US)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Analog Devices, Inc. (US)

11.3. Texas Instruments Incorporated (US)

11.4. Honeywell International Inc. (US)

11.5. GE Healthcare Inc. (US)

11.6. OMNIVISION Technologies, Inc. (US)

11.7. Masimo Corporation (US)

11.8. STMicroelectronics N.V. (Switzerland)

11.9. NXP Semiconductors N.V. (Netherlands)

11.10. Sensirion AG (Switzerland)

11.11. ams-OSRAM AG (Austria)

11.12. Philips N.V. (Netherlands)

11.13. Siemens Healthineers AG (Germany)

11.14. Omron Corporation (Japan)

11.15. Renesas Electronics Corporation (Japan)

11.16. Sony Corporation (Japan)

11.17. Samsung Electronics Co., Ltd. (South Korea)

11.18. Toshiba Corporation (Japan)

11.19. Fujifilm Holdings Corporation (Japan)

11.20. Biovac (South Africa)

12. Key Findings

13. Industry Recommendations