Lubricants Market - Driven by the Demand for Enhanced Efficiency and Operational Convenience in Aviation

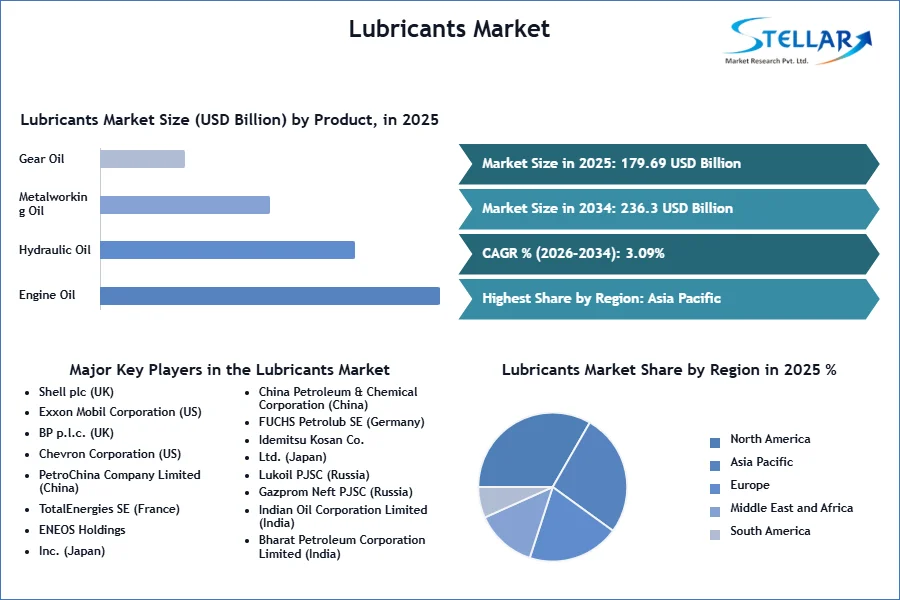

The Lubricants Market size was valued at USD 179.69 Billion in 2025 and the total Global Lubricants revenue is expected to grow at a CAGR of 3.1% from 2026 to 2034, reaching nearly USD 236.3 Billion by 2034.

Lubricants Market Overview

In the chemical and material industry, lubricants are specialized substances designed to control and reduce friction, wear, and heat generation between surfaces in relative motion. They play a crucial role in enhancing operational efficiency, preventing mechanical failures, and extending the durability of components. Lubricants are widely used across automotive, aerospace, industrial machinery, and manufacturing industries, ensuring seamless operation, enhanced energy efficiency, and reduced maintenance costs.

- In March 2025, Saudi Arabian Oil Group (Saudi Aramco) acquired Valvoline Inc.'s Global Products Business for USD 2.65 billion, marking a strategic move to strengthen its position in the global lubricants market. This acquisition enhances Aramco’s downstream portfolio, enabling it to diversify its high-value finished lubricants offerings across automotive, industrial, and commercial sectors. By leveraging Valvoline’s strong brand equity, extensive manufacturing and distribution network, and advanced R&D capabilities, Aramco aims to expand its market presence, improve supply chain efficiencies, and tap into the growing demand for premium lubricants, particularly in emerging markets. The acquisition aligns with Aramco’s broader vision of downstream business expansion, integrating Valvoline’s well-established customer base and product innovation to create a competitive edge in the integrated, branded lubricants industry.

- Valvoline Inc., a U.S.-based automotive services company, is known for manufacturing and distributing high-performance lubricants and automotive chemicals. With this divestiture, Valvoline shifts its focus towards its retail and service businesses, aligning with its long-term growth strategy. Meanwhile, Aramco benefits from acquiring an industry-leading lubricants business with a well-recognized brand, positioning itself as a dominant player in the global lubricants sector. This acquisition not only reinforces Aramco’s commitment to premium lubricants production and distribution but also enhances its ability to cater to a wider customer base, ensuring long-term growth and competitive advantage in the industry.

To get more Insights: Request Free Sample Report

Lubricants Market Dynamics

Automotive and Industrial Growth: A Key Driver for the Lubricants Market

The expansion of the automotive and industrial sectors is one of the most influential forces driving the global lubricants market. Increasing vehicle ownership and industrial activities worldwide have significantly boosted the demand for lubricants required for smooth machinery operations and vehicle maintenance. As global economies continue to expand, industries such as manufacturing, construction, transportation, and mining are scaling up operations, leading to a surge in lubricant consumption. The automotive sector alone accounted for nearly 55% of the total lubricant demand, with increasing vehicle ownership in countries like China, India, and Brazil driving this growth. The global vehicle population surpassed 1.5 billion in 2025, with China and India leading new vehicle sales. This rise has escalated the demand for engine oils, transmission fluids, and greases for passenger cars, commercial fleets, and two-wheelers.

Also, the industrial sector contributes over 30% of lubricant consumption, with the manufacturing and construction industries being the largest consumers. The global industrial lubricant market was valued at USD 174.30 billion in 2025 and is projected to witness steady growth due to increasing investments in heavy machinery, automation, and infrastructure projects. Moreover, the rise of the electric vehicle (EV) market is reshaping lubricant demand patterns. While EVs require fewer traditional lubricants, they create new opportunities for specialized EV fluids such as battery coolants, dielectric fluids, and gear lubricants. Automakers are heavily investing in thermal management lubricants, ensuring battery efficiency and longevity. This transition is forcing lubricant manufacturers to innovate and develop low-viscosity, energy-efficient, and high-performance solutions tailored to electric drivetrains. With automotive electrification and industrial expansion on the rise, the lubricant industry is poised for sustained growth, adapting to both traditional and emerging market needs.

Fluctuating Lubricant Production and Trade: A Major Challenge for the UK Lubricant Market

The lubricant market in the United Kingdom faces significant challenges due to declining domestic production, increasing reliance on imports, and volatile trade activities. Over the past decade, the UK has experienced fluctuating lubricant production levels, influenced by rising raw material costs, stringent environmental regulations, and shifting industrial demand. The decline in local manufacturing capacity has raised concerns about supply chain resilience, forcing businesses to depend more on international suppliers to meet growing domestic requirements. Additionally, the increasing demand for synthetic and environmentally acceptable lubricants has placed pressure on UK manufacturers to innovate while maintaining cost efficiency, making it difficult to compete with large-scale producers from regions with lower production costs. The economic impact of Brexit, supply chain disruptions, and global market uncertainties have further compounded these challenges, leading to an unstable market environment where businesses must navigate higher operational costs and evolving compliance standards.

The above graph highlights the ongoing struggles in the UK lubricant market, particularly the steep decline in domestic production and the growing dependence on imports. In 2025, lubricant production fell to 232 thousand metric tons, marking a 21% decline from the previous year clear indication of the sector’s shrinking manufacturing base. At the same time, imports surged to 322 thousand metric tons, underscoring the country’s increasing reliance on foreign suppliers to meet industrial demand. This dependency on imports presents a critical challenge, as global trade disruptions, geopolitical tensions, and fluctuating transportation costs could jeopardize supply stability and inflate procurement expenses. Moreover, while exports have remained relatively stable, the UK’s ability to compete in the global lubricant market is being tested by stronger international players with more cost-effective production capabilities. These factors collectively pose a significant restraint on the UK's lubricant industry, necessitating urgent investment in domestic production capabilities, technological innovation, and sustainable manufacturing practices to regain market stability and reduce external dependencies.

Lubricants Market Regional Analysis

Asia-Pacific Holds A Dominant Force in the Global Lubricants Market

The Asia-Pacific region holds the largest share of the global lubricants market, driven by a unique combination of economic expansion, industrial growth, and increasing consumer demand. As the fastest-growing market, the region benefits from rapid urbanization, accelerating industrialization, and a surge in vehicle ownership, all of which contribute to the rising demand for high-performance lubrication solutions across various sectors. The region is home to some of the world's fastest-growing economies, including China, India, Indonesia, and Vietnam, where large-scale infrastructure projects, expanding manufacturing activities, and rising disposable incomes have fueled market growth. China alone accounts for nearly 45% of the region’s lubricant consumption, driven by its vast automotive and industrial sectors. Meanwhile, India’s lubricant market is witnessing significant growth, fueled by rising demand in the automotive, heavy machinery, and power generation industries. As the world's largest importer of lube oil, India received 37.2 thousand barrels per day in 2025, representing 18.8% of global lubricant shipments. This surge in imports underscores India's expanding industrial activities and increasing reliance on high-performance lubricants to support its growing infrastructure and transportation sectors. The increasing preference for synthetic and semi-synthetic lubricants in these economies is further reshaping market trends, as industries shift toward higher efficiency and environmentally friendly lubrication technologies.

Furthermore, the rapid industrialization of developing economies in the region has significantly heightened the demand for premium-grade lubricants essential for ensuring the longevity and efficiency of machinery used in construction, mining, energy production, and manufacturing. Governments across Asia-Pacific are investing heavily in infrastructure development, including smart cities, industrial corridors, and transportation networks, which in turn amplifies the need for industrial lubricants such as hydraulic fluids, gear oils, and metalworking fluids. Additionally, the region’s automotive sector is experiencing unprecedented growth, with India and China leading global vehicle production and sales, further driving the need for engine oils, transmission fluids, and greases. As Asia-Pacific remains a key manufacturing hub for automobiles, electronics, and heavy machinery, lubricant manufacturers are increasingly focusing on product innovation, sustainability, and supply chain efficiency to meet the evolving needs of industries. With ongoing technological advancements and a rising regulatory focus on energy-efficient lubricants, the Asia-Pacific lubricants market is poised to continue its dominance, shaping global trends in industrial and automotive lubrication solutions.

Lubricants Market Segment Analysis

By Base Oil

The lubricants market is segmented by base oil into mineral oil lubricants, synthetic lubricants, and bio-based lubricants, each catering to different industrial and automotive needs. Mineral oil lubricants dominate the market, accounting for over 60% of the global demand, largely due to their low cost and widespread applications in industries such as automotive, industrial machinery, and marine. However, the shift toward high-performance lubrication solutions is fuelling the growth of synthetic lubricants, which are expected to add nearly 2 million metric tons of demand by 2034. The adoption of bio-based lubricants is also accelerating, particularly in Europe and North America, where regulatory policies and sustainability initiatives are driving the market. These environmentally friendly lubricants currently represent around 5-8% of the total market but are gaining momentum, with leading manufacturers investing in research and production capacity expansions to meet the rising demand.

By Product Type

The lubricant market is classified into engine oil, hydraulic oil, metalworking oil, gear oil, compressor oil, grease, turbine oil, and others, each serving essential functions in transportation, industrial, and manufacturing applications. Engine oil holds the largest market share, with global consumption exceeding 20 million metric tons annually, driven by the rising vehicle parc, increasing maintenance activities, and growing sales of commercial vehicles. Hydraulic oil demand is expanding due to its widespread use in construction, mining, and manufacturing equipment, with annual consumption surpassing 10 million metric tons. Metalworking fluids are growing steadily, with demand expected to increase by 1.5 million metric tons over the next five years, primarily due to rising automotive and aerospace manufacturing activities. Greases, although a relatively smaller segment, account for approximately 5% of the total lubricant market, with their demand increasing particularly in heavy industrial applications and off-highway vehicles.

Lubricants Market Scope

|

Lubricants Market Scope |

|

|

Market Size in 2025 |

USD 179.69 Bn. |

|

Market Size in 2034 |

USD 236.3 Bn. |

|

CAGR (2026-2034) |

3.1% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Base Oil Mineral Oil Lubricants Synthetic Lubricants Bio-based Lubricants |

|

By Product Type Engine Oil Hydraulic Oil Metalworking Oil Gear Oil Compressor Oil Grease Turbine Oil Others |

|

|

By End Use Industry Transportation Industrial Automotive Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Players in the Lubricants Market

- Shell plc (UK)

- Exxon Mobil Corporation (US)

- BP p.l.c. (UK)

- Chevron Corporation (US)

- PetroChina Company Limited (China)

- TotalEnergies SE (France)

- ENEOS Holdings, Inc. (Japan)

- China Petroleum & Chemical Corporation (China)

- FUCHS Petrolub SE (Germany)

- Idemitsu Kosan Co., Ltd. (Japan)

- Lukoil PJSC (Russia)

- Gazprom Neft PJSC (Russia)

- Indian Oil Corporation Limited (India)

- Bharat Petroleum Corporation Limited (India)

- Hindustan Petroleum Corporation Limited (India)

- Motul S.A. (France)

- Phillips 66 (US)

- Valvoline Inc. (US)

- Petronas Lubricants International (Malaysia)

- Gulf Oil International Ltd. (UK)

- Repsol S.A. (Spain)

- SK Lubricants Co., Ltd. (South Korea)

- Quaker Houghton (US)

- Morris Lubricants (UK)

- Caltex Australia Limited (Australia)

- Sinopec Lubricant Co., Ltd. (China)

- Amalie Oil Company (US)

- Liqui Moly GmbH (Germany)

- Pertamina Lubricants (Indonesia)

- Royal Manufacturing Co. (US)

Frequently Asked Questions

Ans: The Asia-Pacific region leads in consumption, with China and India being major contributors due to rapid industrialization and vehicle ownership growth.

Ans: Mineral oil, synthetic, and bio-based lubricants, catering to industries like automotive, aerospace, and manufacturing

Ans: EVs require specialized lubricants, including battery coolants and gear oils, driving new product innovations.

Ans: Shell, ExxonMobil, BP, Chevron, and TotalEnergies, among others, dominate the industry with strong market presence and innovation.

1. Lubricants Market Introduction

1.1. Study Assumption and Market Definition

1.2. Scope of the Study

1.3. Executive Summary

2. Global Lubricants Market: Competitive Landscape

2.1. Ecosystem Analysis

2.2. SMR Competition Matrix

2.3. Competitive Landscape

2.4. Key Players Benchmarking

2.4.1. Company Name

2.4.2. Business Segment

2.4.3. End-user Segment

2.4.4. Revenue (2024)

2.4.5. Company Locations

2.5. Market Structure

2.5.1. Market Leaders

2.5.2. Market Followers

2.5.3. Emerging Players

2.6. Mergers and Acquisitions Details

3. Lubricants Market: Dynamics

3.1. Lubricants Market Trends by Region

3.1.1. North America Lubricants Market Trends

3.1.2. Europe Lubricants Market Trends

3.1.3. Asia Pacific Lubricants Market Trends

3.1.4. Middle East and Africa Lubricants Market Trends

3.1.5. South America Lubricants Market Trends

3.2. Lubricants Market Dynamics

3.2.1. Global Lubricants Market Drivers

3.2.2. Global Lubricants Market Restraints

3.2.3. Global Lubricants Market Opportunities

3.2.4. Global Lubricants Market Challenges

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

3.5. Trade Analysis

3.5.1. Top 10 Importing Countries

3.5.2. Top 10 Exporting Countries

3.6. Technology Analysis

3.6.1. Re-refining technology

3.6.2. SO2 scrubbing system technology

3.6.3. Nanotechnology in lubricants

3.7. Pricing Analysis

3.7.1. Average Selling Price Trend of key players, by Base Oil

3.7.2. Average Selling Price Trend, by Region

3.8. Regulatory Landscape by Region

3.8.1. North America

3.8.2. Europe

3.8.3. Asia Pacific

3.8.4. Middle East and Africa

3.8.5. South America

3.9. Key Opinion Leader Analysis for Lubricants Industry

4. Lubricants Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2024-2032)

4.1. Lubricants Market Size and Forecast, By Base Oil (2024-2032)

4.1.1. Mineral Oil Lubricants

4.1.2. Synthetic Lubricants

4.1.3. Bio-based Lubricants

4.2. Lubricants Market Size and Forecast, By Product Type (2024-2032)

4.2.1. Engine Oil

4.2.2. Hydraulic Oil

4.2.3. Metalworking Oil

4.2.4. Gear Oil

4.2.5. Compressor Oil

4.2.6. Grease

4.2.7. Turbine Oil

4.2.8. Others

4.3. Lubricants Market Size and Forecast, By End User Industry (2024-2032)

4.3.1. Transportation

4.3.2. Industrial

4.3.3. Automotive

4.3.4. Aerospace

4.3.5. Others

4.4. Lubricants Market Size and Forecast, by Region (2024-2032)

4.4.1. North America

4.4.2. Europe

4.4.3. Asia Pacific

4.4.4. Middle East and Africa

4.4.5. South America

5. North America Lubricants Market Size and Forecast by Segmentation (by Value in USD Million) (2024-2032)

5.1. North America Lubricants Market Size and Forecast, By Base Oil (2024-2032)

5.1.1. Mineral Oil Lubricants

5.1.2. Synthetic Lubricants

5.1.3. Bio-based Lubricants

5.2. North America Lubricants Market Size and Forecast, By Product Type (2024-2032)

5.2.1. Engine Oil

5.2.2. Hydraulic Oil

5.2.3. Metalworking Oil

5.2.4. Gear Oil

5.2.5. Compressor Oil

5.2.6. Grease

5.2.7. Turbine Oil

5.2.8. Others

5.3. North America Lubricants Market Size and Forecast, By End User Industry (2024-2032)

5.3.1. Transportation

5.3.2. Industrial

5.3.3. Automotive

5.3.4. Aerospace

5.3.5. Others

5.4. North America Lubricants Market Size and Forecast, by Country (2024-2032)

5.4.1. United States

5.4.1.1. United States Lubricants Market Size and Forecast, By Base Oil (2024-2032)

5.4.1.1.1. Mineral Oil Lubricants

5.4.1.1.2. Synthetic Lubricants

5.4.1.1.3. Bio-based Lubricants

5.4.1.2. United States Lubricants Market Size and Forecast, By Product Type (2024-2032)

5.4.1.2.1. Engine Oil

5.4.1.2.2. Hydraulic Oil

5.4.1.2.3. Metalworking Oil

5.4.1.2.4. Gear Oil

5.4.1.2.5. Compressor Oil

5.4.1.2.6. Grease

5.4.1.2.7. Turbine Oil

5.4.1.2.8. Others

5.4.1.3. United States Lubricants Market Size and Forecast, By End User Industry (2024-2032)

5.4.1.3.1. Transportation

5.4.1.3.2. Industrial

5.4.1.3.3. Automotive

5.4.1.3.4. Aerospace

5.4.1.3.5. Others

5.4.1.4. Canada Lubricants Market Size and Forecast, By Base Oil (2024-2032)

5.4.1.4.1. Mineral Oil Lubricants

5.4.1.4.2. Synthetic Lubricants

5.4.1.4.3. Bio-based Lubricants

5.4.1.5. Canada Lubricants Market Size and Forecast, By Product Type(2024-2032)

5.4.1.5.1. Engine Oil

5.4.1.5.2. Hydraulic Oil

5.4.1.5.3. Metalworking Oil

5.4.1.5.4. Gear Oil

5.4.1.5.5. Compressor Oil

5.4.1.5.6. Grease

5.4.1.5.7. Turbine Oil

5.4.1.5.8. Others

5.4.2. Canada Lubricants Market Size and Forecast, By End User Industry(2024-2032)

5.4.2.1.1. Transportation

5.4.2.1.2. Industrial

5.4.2.1.3. Automotive

5.4.2.1.4. Aerospace

5.4.2.1.5. Others

5.4.3. Mexico

5.4.3.1. Mexico Lubricants Market Size and Forecast, By Base Oil (2024-2032)

5.4.3.1.1. Mineral Oil Lubricants

5.4.3.1.2. Synthetic Lubricants

5.4.3.1.3. Bio-based Lubricants

5.4.3.2. Mexico Lubricants Market Size and Forecast, By Product Type (2024-2032)

5.4.3.2.1. Engine Oil

5.4.3.2.2. Hydraulic Oil

5.4.3.2.3. Metalworking Oil

5.4.3.2.4. Gear Oil

5.4.3.2.5. Compressor Oil

5.4.3.2.6. Grease

5.4.3.2.7. Turbine Oil

5.4.3.2.8. Others

5.4.3.3. Mexico Lubricants Market Size and Forecast, By End User Industry (2024-2032)

5.4.3.3.1. Transportation

5.4.3.3.2. Industrial

5.4.3.3.3. Automotive

5.4.3.3.4. Aerospace

5.4.3.3.5. Others

6. Europe Lubricants Market Size and Forecast by Segmentation (by Value in USD Million) (2024-2032)

6.1. Europe Lubricants Market Size and Forecast, By Base Oil (2024-2032)

6.2. Europe Lubricants Market Size and Forecast, By Product Type (2024-2032)

6.3. Europe Lubricants Market Size and Forecast, By End User Industry (2024-2032)

6.4. Europe Lubricants Market Size and Forecast, by Country (2024-2032)

6.4.1. United Kingdom

6.4.1.1. United Kingdom Lubricants Market Size and Forecast, By Base Oil (2024-2032)

6.4.1.2. United Kingdom Lubricants Market Size and Forecast, By Product Type (2024-2032)

6.4.1.3. United Kingdom Lubricants Market Size and Forecast, By End User Industry (2024-2032)

6.4.2. France

6.4.2.1. France Lubricants Market Size and Forecast, By Base Oil (2024-2032)

6.4.2.2. France Lubricants Market Size and Forecast, By Product Type (2024-2032)

6.4.2.3. France Lubricants Market Size and Forecast, By End User Industry (2024-2032)

6.4.3. Germany

6.4.3.1. Germany Lubricants Market Size and Forecast, By Base Oil (2024-2032)

6.4.3.2. Germany Lubricants Market Size and Forecast, By Product Type (2024-2032)

6.4.3.3. Germany Lubricants Market Size and Forecast, By End User Industry (2024-2032)

6.4.4. Italy

6.4.4.1. Italy Lubricants Market Size and Forecast, By Base Oil (2024-2032)

6.4.4.2. Italy Lubricants Market Size and Forecast, By Product Type (2024-2032)

6.4.4.3. Italy Lubricants Market Size and Forecast, By End User Industry (2024-2032)

6.4.5. Spain

6.4.5.1. Spain Lubricants Market Size and Forecast, By Base Oil (2024-2032)

6.4.5.2. Spain Lubricants Market Size and Forecast, By Product Type (2024-2032)

6.4.5.3. Spain Lubricants Market Size and Forecast, By End User Industry (2024-2032)

6.4.6. Sweden

6.4.6.1. Sweden Lubricants Market Size and Forecast, By Base Oil (2024-2032)

6.4.6.2. Sweden Lubricants Market Size and Forecast, By Product Type (2024-2032)

6.4.6.3. Sweden Lubricants Market Size and Forecast, By End User Industry (2024-2032)

6.4.7. Austria

6.4.7.1. Austria Lubricants Market Size and Forecast, By Base Oil (2024-2032)

6.4.7.2. Austria Lubricants Market Size and Forecast, By Product Type (2024-2032)

6.4.7.3. Austria Lubricants Market Size and Forecast, By End User Industry (2024-2032)

6.4.8. Rest of Europe

6.4.8.1. Rest of Europe Lubricants Market Size and Forecast, By Base Oil (2024-2032)

6.4.8.2. Rest of Europe Lubricants Market Size and Forecast, By Product Type (2024-2032)

6.4.8.3. Rest of Europe Lubricants Market Size and Forecast, By End User Industry (2024-2032)

7. Asia Pacific Lubricants Market Size and Forecast by Segmentation (by Value in USD Million) (2024-2032)

7.1. Asia Pacific Lubricants Market Size and Forecast, By Base Oil (2024-2032)

7.2. Asia Pacific Lubricants Market Size and Forecast, By Product Type (2024-2032)

7.3. Asia Pacific Lubricants Market Size and Forecast, By End User Industry (2024-2032)

7.4. Asia Pacific Lubricants Market Size and Forecast, by Country (2024-2032)

7.4.1. China

7.4.1.1. China Lubricants Market Size and Forecast, By Base Oil (2024-2032)

7.4.1.2. China Lubricants Market Size and Forecast, By Product Type (2024-2032)

7.4.1.3. China Lubricants Market Size and Forecast, By End User Industry (2024-2032)

7.4.2. S Korea

7.4.2.1. S Korea Lubricants Market Size and Forecast, By Base Oil (2024-2032)

7.4.2.2. S Korea Lubricants Market Size and Forecast, By Product Type (2024-2032)

7.4.2.3. S Korea Lubricants Market Size and Forecast, By End User Industry (2024-2032)

7.4.3. Japan

7.4.3.1. Japan Lubricants Market Size and Forecast, By Base Oil (2024-2032)

7.4.3.2. Japan Lubricants Market Size and Forecast, By Product Type (2024-2032)

7.4.3.3. Japan Lubricants Market Size and Forecast, By End User Industry (2024-2032)

7.4.4. India

7.4.4.1. India Lubricants Market Size and Forecast, By Base Oil (2024-2032)

7.4.4.2. India Lubricants Market Size and Forecast, By Product Type (2024-2032)

7.4.4.3. India Lubricants Market Size and Forecast, By End User Industry (2024-2032)

7.4.5. Australia

7.4.5.1. Australia Lubricants Market Size and Forecast, By Base Oil (2024-2032)

7.4.5.2. Australia Lubricants Market Size and Forecast, By Product Type (2024-2032)

7.4.5.3. Australia Lubricants Market Size and Forecast, By End User Industry (2024-2032)

7.4.6. Indonesia

7.4.6.1. Indonesia Lubricants Market Size and Forecast, By Base Oil (2024-2032)

7.4.6.2. Indonesia Lubricants Market Size and Forecast, By Product Type (2024-2032)

7.4.6.3. Indonesia Lubricants Market Size and Forecast, By End User Industry (2024-2032)

7.4.7. Malaysia

7.4.7.1. Malaysia Lubricants Market Size and Forecast, By Base Oil (2024-2032)

7.4.7.2. Malaysia Lubricants Market Size and Forecast, By Product Type (2024-2032)

7.4.7.3. Malaysia Lubricants Market Size and Forecast, By End User Industry (2024-2032)

7.4.8. Vietnam

7.4.8.1. Vietnam Lubricants Market Size and Forecast, By Base Oil (2024-2032)

7.4.8.2. Vietnam Lubricants Market Size and Forecast, By Product Type (2024-2032)

7.4.8.3. Vietnam Lubricants Market Size and Forecast, By End User Industry (2024-2032)

7.4.9. Taiwan

7.4.9.1. Taiwan Lubricants Market Size and Forecast, By Base Oil (2024-2032)

7.4.9.2. Taiwan Lubricants Market Size and Forecast, By Product Type (2024-2032)

7.4.9.3. Taiwan Lubricants Market Size and Forecast, By End User Industry (2024-2032)

7.4.10. Rest of Asia Pacific

7.4.10.1. Rest of Asia Pacific Lubricants Market Size and Forecast, By Base Oil (2024-2032)

7.4.10.2. Rest of Asia Pacific Lubricants Market Size and Forecast, By Product Type (2024-2032)

7.4.10.3. Rest of Asia Pacific Lubricants Market Size and Forecast, By End User Industry (2024-2032)

8. Middle East and Africa Lubricants Market Size and Forecast by Segmentation (by Value in USD Million) (2024-2032)

8.1. Middle East and Africa Lubricants Market Size and Forecast, By Base Oil (2024-2032)

8.2. Middle East and Africa Lubricants Market Size and Forecast, By Product Type (2024-2032)

8.3. Middle East and Africa Lubricants Market Size and Forecast, By End User Industry (2024-2032)

8.4. Middle East and Africa Lubricants Market Size and Forecast, by Country (2024-2032)

8.4.1. South Africa

8.4.1.1. South Africa Lubricants Market Size and Forecast, By Base Oil (2024-2032)

8.4.1.2. South Africa Lubricants Market Size and Forecast, By Product Type (2024-2032)

8.4.1.3. South Africa Lubricants Market Size and Forecast, By End User Industry (2024-2032)

8.4.2. GCC

8.4.2.1. GCC Lubricants Market Size and Forecast, By Base Oil (2024-2032)

8.4.2.2. GCC Lubricants Market Size and Forecast, By Product Type (2024-2032)

8.4.2.3. GCC Lubricants Market Size and Forecast, By End User Industry (2024-2032)

8.4.3. Nigeria

8.4.3.1. Nigeria Lubricants Market Size and Forecast, By Base Oil (2024-2032)

8.4.3.2. Nigeria Lubricants Market Size and Forecast, By Product Type (2024-2032)

8.4.3.3. Nigeria Lubricants Market Size and Forecast, By End User Industry (2024-2032)

8.4.4. Rest of ME&A

8.4.4.1. Rest of ME&A Lubricants Market Size and Forecast, By Base Oil (2024-2032)

8.4.4.2. Rest of ME&A Lubricants Market Size and Forecast, By Product Type (2024-2032)

8.4.4.3. Rest of ME&A Lubricants Market Size and Forecast, By End User Industry (2024-2032)

9. South America Lubricants Market Size and Forecast by Segmentation (by Value in USD Million) (2024-2032)

9.1. South America Lubricants Market Size and Forecast, By Base Oil (2024-2032)

9.2. South America Lubricants Market Size and Forecast, By Product Type (2024-2032)

9.3. South America Lubricants Market Size and Forecast, By End User Industry (2024-2032)

9.4. South America Lubricants Market Size and Forecast, by Country (2024-2032)

9.4.1. Brazil

9.4.1.1. Brazil Lubricants Market Size and Forecast, By Base Oil (2024-2032)

9.4.1.2. Brazil Lubricants Market Size and Forecast, By Product Type (2024-2032)

9.4.1.3. Brazil Lubricants Market Size and Forecast, By End User Industry (2024-2032)

9.4.2. Argentina

9.4.2.1. Argentina Lubricants Market Size and Forecast, By Base Oil (2024-2032)

9.4.2.2. Argentina Lubricants Market Size and Forecast, By Product Type (2024-2032)

9.4.2.3. Argentina Lubricants Market Size and Forecast, By End User Industry (2024-2032)

9.4.3. Rest Of South America

9.4.3.1. Rest Of South America Lubricants Market Size and Forecast, By Base Oil (2024-2032)

9.4.3.2. Rest Of South America Lubricants Market Size and Forecast, By Product Type (2024-2032)

9.4.3.3. Rest Of South America Lubricants Market Size and Forecast, By End User Industry (2024-2032)

10. Company Profile: Key Players

10.1. Shell plc (UK)

10.1.1. Company Overview

10.1.2. Business Portfolio

10.1.3. Financial Overview

10.1.4. SWOT Analysis

10.1.5. Strategic Analysis

10.1.6. Recent Developments

10.2. Exxon Mobil Corporation (US)

10.3. BP p.l.c. (UK)

10.4. Chevron Corporation (US)

10.5. PetroChina Company Limited (China)

10.6. TotalEnergies SE (France)

10.7. ENEOS Holdings, Inc. (Japan)

10.8. China Petroleum & Chemical Corporation (China)

10.9. FUCHS Petrolub SE (Germany)

10.10. Idemitsu Kosan Co., Ltd. (Japan)

10.11. Lukoil PJSC (Russia)

10.12. Gazprom Neft PJSC (Russia)

10.13. Indian Oil Corporation Limited (India)

10.14. Bharat Petroleum Corporation Limited (India)

10.15. Hindustan Petroleum Corporation Limited (India)

10.16. Motul S.A. (France)

10.17. Phillips 66 (US)

10.18. Valvoline Inc. (US)

10.19. Petronas Lubricants International (Malaysia)

10.20. Gulf Oil International Ltd. (UK)

10.21. Repsol S.A. (Spain)

10.22. SK Lubricants Co., Ltd. (South Korea)

10.23. Quaker Houghton (US)

10.24. Morris Lubricants (UK)

10.25. Caltex Australia Limited (Australia)

10.26. Sinopec Lubricant Co., Ltd. (China)

10.27. Amalie Oil Company (US)

10.28. Liqui Moly GmbH (Germany)

10.29. Pertamina Lubricants (Indonesia)

10.30. Royal Manufacturing Co. (US)

11. Key Findings

12. Analyst Recommendations

13. Lubricants Market: Research Methodology