Food Intolerance Products Market Global Industry Analysis and Forecast (2026-2032)

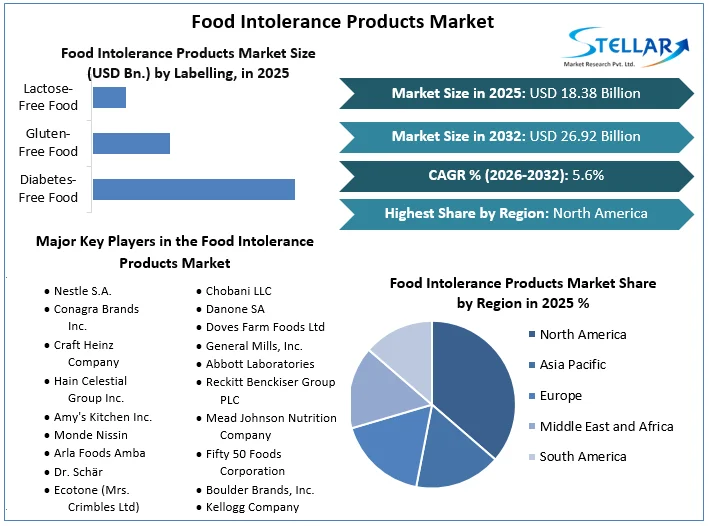

The global Food Intolerance Products Market size was valued at USD 18.38 Bn in 2025. The market is expected to grow at a CAGR of 5.6 % during the forecast period from 2026-2032, reaching nearly USD 26.92 Bn by 2032

Food Intolerance Products Market Overview

Food Intolerance, also known as food sensitivity, can cause various digestive symptoms like bloating and nausea. Although food intolerance may cause symptoms similar to those caused by a food allergy, the two are different. The food intolerance products market focuses on products meant for individuals who have sensitivities or intolerances to some foods. This market includes products that are free from allergens like lactose, gluten and nuts.

The food intolerance products market is expected to grow during the forecast period 2026-2032, due to the increasing awareness of food intolerances and allergies. The market is driven by the factors like increase in number of people who have celiac disease and those who are choose gluten-free products like bread, pasta, cereals, and bakery products.

North America dominated the Food Intolerance Product Market in 2025, driven by high awareness, a strong presence of key players, and a large consumer base with food intolerances. Europe is expected to grow in forecast period of 2026-2032, due to strict regulations on food labeling and a high incidence of food allergies and intolerances.

Key players in the food industry include Nestlé SA, General Mills, Abbott Laboratories, Kraft Heinz Company, Dr. Schär AG/SPA, Mead Johnson Nutritionals, Inc., Danone SA, Fifty 50 Foods, Inc., Bol Brands, Inc., and Kellogg Company, among others. Nestlé Offers a variety of gluten-free and allergen-free products tailored for babies and young children with mild to severe cow’s milk protein allergy and other complex multiple food allergies. Developing products that meet with individual nutritional needs and preferences, driven by advancements in nutrition science and technology. Promoting food intolerance products with a healthy lifestyle aligns with the general health and wellness trend.

To get more Insights: Request Free Sample Report

Food Intolerance Products Market Dynamics

Drivers

Increasing consumer awareness and prevalence of food intolerance drive the market

Food intolerance products are highly demanded worldwide due to the increasing gluten allergies, indigestion cases, lactose intolerance people, celiac disease, and high gluten sensitivity. Improved medical testing and increased disease awareness have enabled individuals to understand their unique nutritional needs. Empowering individuals to take charge of their health by making healthier choices in their diet, rises the need for food items and encourages companies to create new products and extend their ranges. According to the Ministry of Health (Ministero della salute), 15,569 cases in 2016 and 8,134 cases in 2017 diagnosed in Italy with the celiac disease are increasing demand for gluten-free products. According to the Ministry's data, the Bolzano Autonomous Province in Italy spent a EUR 1,630.15 per person on gluten-free products in 2017. There has been a significant increase in the demand for natural and organic products among consumers in recent period as they are becoming more aware of the health effects associated with the consumption of various food elements and gluten-containing foods, such as wheat and barley.

According to a study published by the International Food Information Council Foundation, in 2019, about 59% of Americans claimed to always read labels on packaged food before buying it for the first time, with about 24% of them specifically looking for certain claims. Thus, due to the increasing consumer awareness, the demand for food intolerance products is rising around the globe.

Growing health awareness boosts demand for gluten-free, lactose-free and glucose-free products

Rising consumer awareness regarding the health and wellness, especially healthy eating, and increasing use of food intolerance products. Consumers are choosing gluten-free, lactose-free, and sugar-free products as part of their lifestyle to improve health, control weight, and avoid health problems. The movement is supported by health experts, influencers, and media promoting the benefits of reducing the consumption of specific allergens and irritants in diets. Food companies are developing products that cater food to individuals with specific sensitivities while also targeting to health-conscious consumers at large. In February 2023, Nestlé presented more than 35 new items at Natural Products Expo West 2023 in Anaheim, California. Key food products included plant-based natural bliss oat milk and California Pizza Kitchen's BBQ chicken frozen pizza with gluten-free cauliflower crust, catering to a variety of nutritional needs and health-conscious people.

Food Intolerance Market Opportunities

Rising demand for healthy lifestyle drives innovations, strategic investments and collaboration

The food intolerance products market examines a significant rise in customers opting for healthy lifestyles and food products free from food claims without compromising taste. This provide an opportunity for the manufacture around the globe to develop products that serve to consumer needs and achieve a competitive edge over other companies. The strategic initiates like continuous investment in research and development to innovate food, acquiring smaller companies to enhance technology and providing training and resources to help customer effectively use food intolerance products tools are gaining the food intolerance products market. The market has witnessed significant demand for organic baby food, including lactose-free infant formula, gaining popularity among parents due to growing concern over children's health.

Therefore, major players start to invest in developing innovative products with organic claims to capture the growing demand and achieve significant market shares, anticipated to drive the market demand during the forecasting period 2024-2030. Additionally, the strategic partnerships and the collaborations are also gaining popularity in the food intolerance products market. The companies are partnering with other market player to develop new products and enhance the supply of products to the market.

Food Intolerance Market Challenges

High costs, labelling risks, and cross-contamination issues stop growth in the food intolerance market

The high price of gluten-free food products and risk of labelling and transparency are the challenges stopping the food intolerance products market growth. This challenge restricts market growth despite the increasing demand for non-dairy milk alternatives, low FODMAP products, and plant-based alternatives. Consumers seek affordable paleo-friendly foods, organic food options, and vegan products beside allergy-friendly snacks. The high cost of developing corn-free products and sulphite-free products further inhibit market expansion, necessitating innovation to address pricing barriers. The Increasing Risk of Labelling and Transparency are also being the obstacles for the Food intolerance product market growth around the globe.

Also, there has been a gross regional dissimilarity in the remaining gluten levels in gluten-free (GF) food, as there are no manufacturing process for manufacturers making such gluten-free food claims. The supply chain of gluten-free products is not strictly monitored in underdeveloped regions like Asia-Pacific thus, there is a greater risk of cross-contamination, providing the unnecessary GF claims. Food contamination with gluten can occur at many critical points, such as milling centres, grocery stores, processing, production facilities, and even at home are inhibit the market growth.

Food Intolerance Products Market Segment Analysis

By Product Type

The bakery products segment dominated the food intolerance products market in 2025 and the growth is driven by the rising demand for gluten-free bakery products. Bakery products include gluten-free breads, cakes, cookies, and pastries are widely use in the treatment of the celiac disease or gluten intolerance. Evaluation in baking technology and replacing elements, like almond flour and coconut flour are leading to advancements in the gluten-free bakery sector, increasing the attractiveness and availability of these products. This segment is expanding quickly because of the rising need for gluten-free products that maintain both flavour and consistency.

Dairy and dairy alternatives segment is expected to grow fast during the forecasting period 2026-2032 due to choice of eating plant-based foods and the increasing number of people with lactose intolerance food. This segment included the lactose-free dairy products like milk, cheese, yogurt, and non-dairy alternatives, including almond milk, soy milk, and oat milk and the advancements in taste and consistency are enhancing the popularity of non-dairy options. The segment is beneficial due to increasing consumer demand for sustainable and legally sourced food items.

By Labelling

The gluten-free segment dominated the market, with a largest market share in 2025 and expected to grow during the forecast period 2026-2032, due to the growing prevalence of celiac disease across the world. The main treatment for the celiac disease is a strictly follow a gluten-free diet, which increasing the demand for the gluten-free products. The raising awareness about the gluten-free food among the population through government awareness programs and initiatives drive the gluten-free market growth.

Lactose-free food segment is exacted to grow fast during the forecasting period 2025-2032, due to the growing incidence of lactose intolerance among population coupled with the growing demand for plant- based dairy replacements. Lactose abstinence allows the gut to recover and eliminate nutritional deficiency as well as other corresponding symptoms. Treatment of strict lactose-free diet adherence lowers the likelihood of developing many of the major long-term consequences associated with untreated lactose intolerance.

Food Intolerance Market Regional Insights

North America region is dominating the Food Intolerance Products Market in 2025, and projected to hold largest share in the Food Intolerance Products Market with the highest CAGR during the forecast period 2026-2032, driven by the factors such as rising consumer interest in clean labelling, organic foods, and health and wellness. Customers increasingly choose nutritious foods like Plant based, dairy or meat as they become more health conscious. Lactose free product becoming more popular, due to their potential health advantages, such as the weight loss and improved immune system by enabling precise digestion through lactose-free food products. The region also has a growing market of supermarkets, convenience store, and online sites that provide a variety of products suitable for people with different nutritional foods.

Europe is the second largest region and expected to grow during the forecasting period 2026-2032, due to the health concerns and the increasing consumption of lactose-free milk in countries such as Spain and France. In 2016, German manufacturer CFP Brands launched a new range of rice crackers under the brand name Nature Addicts. It is made from 95% jasmine rice and is described as gluten-free and baked rather than fried and available in Sea Salt, Black Pepper, and Red Pepper and sold in 70g bags. A further study by the Environmental Medicine Commission of the Robert Koch Institute states that the prevalence of food allergies in adults was 4.7% in 2016, propelling the market.

In February 2025, Nestlé a german company launch of Better Whey, a whey protein powder free of lactose and animal products, made a significant entry into the precision fermentation dairy protein market. This product minimized its environmental impact in comparison to conventional dairy products, making it more sustainable for consumers who are lactose intolerant.

Import-Export Analysis of Food Intolerance product Market

Countries with advanced food technology and production capacity, such as the United States, Germany, and Australia, are major exporters of food intolerance products. These countries have developed a range of specialized products, including gluten-free, lactose-free, and allergen-free foods, driven by increasing consumer demand for dietary alternatives. The U.S., in particular, has a strong market for innovative food products and benefits from well-established food processing industries and international exports. Germany and Australia also export significant amount of these products, supported by their strong food safety regulations and technological advancements.

European Countries, such as the UK, France, and Italy experiencing rising awareness and diagnosis of food intolerances are major importers of food intolerance products to meet their consumers' dietary needs. Countries in Asia and the Middle East are expanding their import amount as awareness of food intolerances grows and dietary trends shift. Importing countries often source products from established markets to ensure product quality and compliance with dietary standards.

Food Intolerance Products Market Competitive Landscape

Key players in the food industry include Nestlé SA, General Mills, Abbott Laboratories, Kraft Heinz Company, Dr. Schär AG/SPA, Mead Johnson Nutritionals, Inc., Danone SA, Fifty 50 Foods, Inc., Bol Brands, Inc., and Kellogg Company, among others. Nestlé has a wide range of food products suitable for infants and children with mild to severe cow protein allergy and other allergies to various foods, and even environmental allergies such as cat allergy. The company manufactures products for newborns at risk for diseases such as atopic dermatitis, hay fever and allergic asthma for international customers. Beyond the food allergies, Nestlé also invests in the development of novel solutions to help with the management of pet allergies. By bringing together all of its global R&D resources, Nestlé provide high quality, safe food solutions like nutrition, health, wellness, taste, texture or convenience

The Kraft Heinz Company is the one of the largest food and Beverage Company in North America, which provide the high quality, great taste and nutrition for all eating occasions. Kraft Heinz is a worldwide recognized food and Beverage Company offers a wide range of products including condiments and sauces, cheese and dairy, meals, meats, refreshment beverages, coffee, infant and nutrition products, and other grocery items. The Kraft Heinz Company is primarily serve as the food and beverage industry and dedicated to making sustainable health of people and planet while helping people with food.

|

Food Intolerance Products Market Scope |

|

|

Market Size in 2025 |

USD 18.38 Bn |

|

Market Size in 2032 |

USD 26.92 Bn |

|

CAGR (2026-2032) |

5.6% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Product Type

|

|

By Labelling

|

|

|

By Distribution Channel

|

|

Key Regions

- North America (United States, Canada, Mexico)

- Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Rest of Europe)

- Asia Pacific (China, S Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, Rest of Asia Pacific)

- Middle East and Africa (South Africa, GCC, Egypt, Nigeria, Rest of MEA)

- South America (Brazil, Mexico, Rest of South America)

Food Intolerance Product Key Players

- Nestle S.A.

- Conagra Brands Inc.

- Craft Heinz Company

- Hain Celestial Group Inc.

- Amy's Kitchen Inc.

- Monde Nissin

- Arla Foods Amba

- Dr. Schär

- Ecotone (Mrs. Crimbles Ltd)

- General Mills Inc.

- Chobani LLC

- Danone SA

- Doves Farm Foods Ltd

- General Mills, Inc.

- Abbott Laboratories

- Reckitt Benckiser Group PLC

- Mead Johnson Nutrition Company

- Fifty 50 Foods Corporation

- Boulder Brands, Inc.

- Kellogg Company

- Others

Frequently Asked Questions

Ans) In the Food Intolerance Products Market, North America held the majority share in 2025

Ans) Europe was the fastest growing region in the Food Intolerance Product market in 2025.

Ans) As per The SMR, the size of the food intolerance products market was valued at USD 18.38 Bn in 2025 to USD 26.92 by 2032.

1. Food Intolerance Products Market: Research Methodology

2. Food Intolerance Products Market: Competitive Landscape

2.1. Stellar Competition Matrix

2.2. Competitive Landscape

2.3. Key Players Benchmarking

2.4. Market Structure

2.4.1. Market Leaders

2.4.2. Market Followers

2.4.3. Emerging Players

2.5. Consolidation of the Market

3. Food Intolerance Products Market: Executive Summary

4. Food Intolerance Products Market: Dynamics

4.1. Market Drivers

4.2. Market Restraints

4.3. Market Opportunities

4.4. Market Challenges

4.5. Regulatory Landscape by Region

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Middle East and Africa

4.5.5. South America

5. Food Intolerance Products Market Size and Forecast by Segments (by Value USD Bn)

5.1. Food Intolerance Products Market Size and Forecast, by Product Type (2025-2032)

5.1.1. Bakery Products

5.1.2. Confectionery Product

5.1.3. Dairy and Dairy Alternatives

5.1.4. Meat and Seafood

5.1.5. Sauces, Condiments and Dressings

5.1.6. Other Product Types

5.2. Food Intolerance Products Market Size and Forecast, by Labelling (2025-2032)

5.2.1. Diabetes-Free Food

5.2.2. Gluten-Free Food

5.2.3. Lactose-Free Food

5.3. Food Intolerance Products Market Size and Forecast, by Distribution Channel (2025-2032)

5.3.1. Supermarkets and Hypermarkets

5.3.2. Convenience Stores

5.3.3. Online Stores

5.4. Food Intolerance Products Market Size and Forecast, by Region (2025-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Food Intolerance Products Market Size and Forecast (by Value USD Bn)

6.1. North America Food Intolerance Products Market Size and Forecast, by Product Type (2025-2032)

6.1.1. Bakery Products

6.1.2. Confectionery Product

6.1.3. Dairy and Dairy Alternatives

6.1.4. Meat and Seafood

6.1.5. Sauces, Condiments and Dressings

6.1.6. Other Product Types

6.2. North America Food Intolerance Products Market Size and Forecast, by Labelling (2025-2032)

6.2.1. Diabetes-Free Food

6.2.2. Gluten-Free Food

6.2.3. Lactose-Free Food

6.3. North America Food Intolerance Products Market Size and Forecast, by Distribution Channel (2025-2032)

6.3.1. Supermarkets and Hypermarkets

6.3.2. Convenience Stores

6.3.3. Online Stores

6.4. North America Food Intolerance Products Market Size and Forecast, by Country (2025-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Food Intolerance Products Market Size and Forecast (by Value USD Bn)

7.1. Europe Food Intolerance Products Market Size and Forecast, by Product Type (2025-2032)

7.1.1. Bakery Products

7.1.2. Confectionery Product

7.1.3. Dairy and Dairy Alternatives

7.1.4. Meat and Seafood

7.1.5. Sauces, Condiments and Dressings

7.1.6. Other Product Types

7.2. Europe Food Intolerance Products Market Size and Forecast, by Labelling (2025-2032)

7.2.1. Diabetes-Free Food

7.2.2. Gluten-Free Food

7.2.3. Lactose-Free Food

7.3. Europe Food Intolerance Products Market Size and Forecast, by Distribution Channel (2025-2032)

7.3.1. Supermarkets and Hypermarkets

7.3.2. Convenience Stores

7.3.3. Online Stores

7.4. Europe Food Intolerance Products Market Size and Forecast, by Country (2025-2032)

7.4.1. UK

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Food Intolerance Products Market Size and Forecast (by Value USD Bn)

8.1. Asia Pacific Food Intolerance Products Market Size and Forecast, by Product Type (2025-2032)

8.1.1. Bakery Products

8.1.2. Confectionery Product

8.1.3. Dairy and Dairy Alternatives

8.1.4. Meat and Seafood

8.1.5. Sauces, Condiments and Dressings

8.1.6. Other Product Types

8.2. Asia Pacific Food Intolerance Products Market Size and Forecast, by Labelling (2025-2032)

8.2.1. Diabetes-Free Food

8.2.2. Gluten-Free Food

8.2.3. Lactose-Free Food

8.3. Asia Pacific Food Intolerance Products Market Size and Forecast, by Distribution Channel (2025-2032)

8.3.1. Supermarkets and Hypermarkets

8.3.2. Convenience Stores

8.3.3. Online Stores

8.4. Asia Pacific Food Intolerance Products Market Size and Forecast, by Country (2025-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Bangladesh

8.4.11. Pakistan

8.4.12. Rest of Asia Pacific

9. Middle East and Africa Food Intolerance Products Market Size and Forecast (by Value USD Bn)

9.1. Middle East and Africa Food Intolerance Products Market Size and Forecast, by Product Type (2025-2032)

9.1.1. Bakery Products

9.1.2. Confectionery Product

9.1.3. Dairy and Dairy Alternatives

9.1.4. Meat and Seafood

9.1.5. Sauces, Condiments and Dressings

9.1.6. Other Product Types

9.2. Middle East and Africa Food Intolerance Products Market Size and Forecast, by Labelling (2025-2032)

9.2.1. Diabetes-Free Food

9.2.2. Gluten-Free Food

9.2.3. Lactose-Free Food

9.3. Middle East and Africa Food Intolerance Products Market Size and Forecast, by Distribution Channel (2025-2032)

9.3.1. Supermarkets and Hypermarkets

9.3.2. Convenience Stores

9.3.3. Online Stores

9.4. Middle East and Africa Food Intolerance Products Market Size and Forecast, by Country (2025-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Egypt

9.4.4. Nigeria

9.4.5. Rest of MEA

10. South America Food Intolerance Products Market Size and Forecast (by Value USD Bn)

10.1. South America Food Intolerance Products Market Size and Forecast, by Product Type (2025-2032)

10.1.1. Bakery Products

10.1.2. Confectionery Product

10.1.3. Dairy and Dairy Alternatives

10.1.4. Meat and Seafood

10.1.5. Sauces, Condiments and Dressings

10.1.6. Other Product Types

10.2. South America Food Intolerance Products Market Size and Forecast, by Labelling (2025-2032)

10.2.1. Diabetes-Free Food

10.2.2. Gluten-Free Food

10.2.3. Lactose-Free Food

10.3. South America Food Intolerance Products Market Size and Forecast, by Distribution Channel (2025-2032)

10.3.1. Supermarkets and Hypermarkets

10.3.2. Convenience Stores

10.3.3. Online Stores

10.4. South America Food Intolerance Products Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Mexico

10.4.3. Rest of South America

11. Company Profile: Key players

11.1. Nestle S.A.

11.1.1. Company Overview

11.1.2. Financial Overview

11.1.3. Business Portfolio

11.1.4. SWOT Analysis

11.1.5. Business Strategy

11.1.6. Recent Developments

11.2. Conagra Brands Inc.

11.3. Hain Celestial Group Inc.

11.4. Amy's Kitchen Inc.

11.5. Monde Nissin

11.6. Arla Foods Amba

11.7. Dr. Schär

11.8. Ecotone (Mrs. Crimbles Ltd)

11.9. General Mills Inc.

11.10. Chobani LLC

11.11. Danone SA

11.12. Doves Farm Foods Ltd

11.13. General Mills, Inc.

11.14. Abbott Laboratories

11.15. Reckitt Benckiser Group PLC

11.16. Craft Heinz Company

11.17. Mead Johnson Nutrition Company

11.18. Fifty 50 Foods Corporation

11.19. Boulder Brands, Inc.

11.20. Kellogg Company

11.21. Others

12. Key Findings

13. Industry Recommendations