Electronic Toll Collection Market - Global Industry analysis and forecast 2026-2032

Electronic Toll Collection Market Size was valued at USD 14.19 Billion in 2025. The market is expected to grow at a CAGR of 7.8% during the forecasting period of 2026-2034, reaching nearly USD 27.89 Billion by 2034.

Electronic Toll Collection Market Overview

Electronic toll collection (ETC) is a wireless technology used to automatically collect the usage fee or toll charged to vehicles using toll roads, HOV lanes, toll bridges, and toll tunnels. Toll booths, where vehicles must stop and the driver physically pays the toll with cash or a card, are being replaced by this alternative. The payment of toll is done through cashless transactions which reduce traffic congestion that caused from paying with cash or credit cards at a toll site.

The Electronic Toll Collation market is expected to grow during the forecast period of 2026-2034, driven by advancements in technology, increasing number of vehicle, and government initiatives to update road infrastructure. In the future, emerging technologies like AI and IoT are probably play a crucial role in shaping the future of ETC systems. Poor road conditions and increased traffic congestion have attracted demand for automatic toll collection.

Electronic toll collection market is divided into the various regions like North America, Europe, Asia-Pacific, Middle east and Africa and South America. North America is dominating region in the electronic toll collection market due to the well-established infrastructure. The need for efficient traffic management, and technological advancements drive the demand for ETC systems in this region. India is also experiencing growth in the ETC market, with significant investments in tolling infrastructure to improve efficiency on national highways.

Major Key player of the Electronic Toll Collection Market are the Kapsch TrafficCom AG, Conduent, Inc., Thales, Cubic Corporation, TRMI Systems Integration, Transcore Holdings, Inc., Honeywell International, Inc., Mitsubishi Heavy Industries, Ltd., and others. These companies offer a range of solutions, including dedicated short-range communication (DSRC) systems, radio-frequency identification (RFID) technology, and automated license plate recognition (ALPR) systems.

Despite its growth, the ETC market faces challenges such as the high initial cost of system implementation, interoperability issues among different toll systems, and privacy concerns related to vehicle tracking. However, ongoing technological advancements and increasing government investments in smart infrastructure are expected to drive further growth and innovation in the ETC market.

To get more Insights: Request Free Sample Report

Electronic Toll Collection Market Dynamics

Drivers

Government initiatives like addressing urban traffic congestion and improving infrastructure efficiency.

Government initiatives like addressing traffic restrictions and improving infrastructure efficiency, play an important role in driving the electronic toll collection (ETC) market. Numerous governments are investing, in the installation and growth of ETC systems in recognizing the growing challenges associated with urban traffic congestion and the demand for efficient transportation networks. These initiatives are component of larger efforts to modernize road infrastructure, improve traffic management, and reducing operating inefficiencies. ETC systems are increasingly incorporated by governments into their infrastructure development plans to minimize delays at toll points, which reduced traffic jams and increased travel times. ETC systems significantly improve traffic flow and reduce congestion, contributing to smoother and more efficient travel by enabling vehicles to pass through toll locations without stopping. This improvement ensure that freight and logistics operations are less disturbed by traffic delays, which benefits individual drivers as well as supports economic activities.

Government-led ETC initiatives frequently concentrate on integrating advanced technologies that support with environmental and sustainability goals in addition to reducing traffic. ETC systems help reduce fuel usage and emissions, contributing to cleaner air and supporting national and international environmental standards by reducing vehicle idling and accelerating traffic movement. Governments facilitate the growth of the ETC market by offering financial incentives, regulatory frameworks, and support for technological innovation. ETC systems being used by governments to gather valuable data on traffic patterns and vehicle behaviour, which will be useful for policy-making and future infrastructure planning. This data used for more informed decision-making and the development of intelligent and flexible traffic management strategies. Overall, government initiatives by addressing traffic congestion, enhancing infrastructure efficiency, supporting environmental goals are driving the ETC market.

Urbanization, traffic congestion and technologies like RFID and DSRC enhancing efficiency

Growth of the electronic toll collection (ETC) market is driven by the factors like urbanization and traffic congestion. The significant traffic congestion, particularly in urban areas are rise due to the expansion of cities and increase in population with the rise in number of vehicles on the road. Traditional toll collection methods are making these traffic issues worse, which frequently require vehicles to stop or slow down in order to pay manually, causes long queues and delays. The need for effective traffic management solutions becomes critical in such situations. Using technologies like RFID, DSRC, and video analytics, ETC systems enables vehicles to pass through toll points without stopping. These solutions improve overall travel efficiency, reduce congestion and streamline traffic flow. Moreover, the environmental benefits of reduced idling times, which lower vehicle emissions, contribute to cleaner urban environments. The push for smart city initiatives and the integration of advanced technologies in urban infrastructure further boost the demand for ETC systems, making them an essential component of modern traffic management strategies.

Opportunities

Emerging technologies like AI and IoT, offering innovation and efficiency

Electronic toll collection (ETC) market is about to undergo a transformation because of Emerging technologies like artificial intelligence (AI) and the Internet of Things (IoT), which offering significant opportunities for innovation and efficiency. Through advanced data analytics, predictive modeling, and real-time decision-making artificial intelligence (AI) can improve the accuracy and speed of toll processing. To ensure the seamless and secure toll transactions, AI-powered image and video recognition can also enhance vehicle identification and fraud detection. These benefits are increased when the integration of IoT devices further amplifies by enabling real-time connectivity and data exchange between vehicles, tolling infrastructure, and central systems. Vast amounts of data on traffic patterns, vehicle speeds, and environmental conditions can be monitored and collected by IoT sensors and connected devices. This data can be leveraged to support predictive maintenance of tolling equipment, provide real-time updates to drivers, and enhance traffic management strategies. AI and IoT work together to build a smart, interconnected ecosystem that improves the efficiency and reliability of ETC systems also enhances the overall user experience. These advancements open up opportunities in the ETC market, like development of smart tolling solutions, data-driven services, and advanced traffic management systems. Companies specializing in AI and IoT technologies can work with traditional toll system suppliers to create new products and services. ETC market stands to benefit significantly from these technological advancements as the demand for intelligent transportation systems, driving future growth and development.

Challenges

High initial costs of electronic toll collection systems hinder widespread adoption

High initial costs cause a significant challenge for the widespread adoption of electronic toll collection (ETC) systems. Advanced technologies such as RFID, DSRC, GPS, and video analytics, as well as the physical components like gantries, sensors, cameras, and communication networks demand a substantial investment for implementation of ETC infrastructure. IT is complex and costly to install and integrate these technologies into existing road and highway networks. The long-term costs further increased by the maintenance and regular updates to keep the systems up to date with advancements in technology and regulatory changes. Financing these projects frequently need substantial government funding or public-private partnerships (PPPs), which can be difficult to obtain. The high upfront costs can discourage regions or countries with limited budgets, slowing the adoption rate of ETC systems. Despite these challenges, governments and private sectors are increasingly recognizing the value of these systems in building efficient, sustainable transportation networks. This has resulted in innovative financing solutions and strategic partnerships to overcome the high initial cost barrier.

Electronic Toll Collection Market Segment Analysis

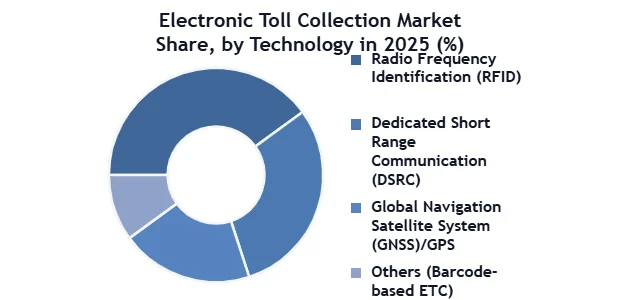

By Technology

The RFID segment accounted for the largest market share in 2025, due to the increase in usage of radio-frequency electromagnetic fields to identify objects that carry RFID tags. This technology is used for electronic identification, tracking, and storing information on a tag. Interrogators or readers, which are also two-way radio transmitters/receivers, send a signal to the tag and receive its response. After scanning the tag with an RFID reader, the data is sent to a database for a storage. RFID low operational cost makes it prominent electronic toll collection technology.

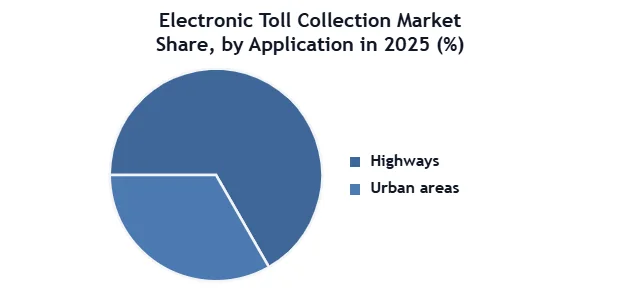

By Application

The urban areas segment dominated the market share and is expected to grow during the forecast period of 2026-2034, driven by the unmatched advantages of electronic toll collection (ETC) systems. By eliminating the need to stop, ETC transforms the transportation landscape and improve traffic flow while reducing congestion especially during the rush hours. For urban areas dealing with increasing traffic volumes, this is an attractive offer. Additionally, this segment is expected to increase at the greatest CAGR throughout the forecast period due to the rise in global urbanization.

The highway segment is anticipated to show the fastest growth during the forecasting period of 2026-2034, due to rising global investment in road and highway construction projects. On the toll plaza, highway vehicles can pay their toll using automatic collecting system without stopping at toll plazas, which is fueling the global market.

Electronic Toll Collection Market Import-Export Analysis

Countries in Asia-Pacific, particularly China, India, and Southeast Asian nations, are the leaders in the electronic toll collection market. The importation of Electronic Toll Collection technology into these regions is often facilitated through government contracts and public-private partnerships aimed at improving national highway networks and urban mobility. The influx of imported electronic toll collection systems is also driven by the need to meet international standards and the preference for proven technologies from established players in the market.

Key exporting countries, such as the United States, Germany, and Japan, dominate the supply of advanced electronic toll Collection technologies, including RFID tags, transponders, and sophisticated tolling software. These countries benefit from their strong industrial bases, technological expertise, and well-established manufacturing sectors, allowing them to produce and export high-quality electronic toll collection systems. As demand for smart transportation solutions rises globally, these exporters are well-positioned to capitalize on the growing needs of developing nations that are rapidly urbanizing and investing in smart city projects.

Electronic Toll Collection Market Regional Analysis

North America dominated the electronic toll collection market in 2025 and expected to grow during the forecasting period due to the due to its vast highway networks and early adoption of advanced tolling system. The United States has led the market by implementing ETC systems, with numerous states integrating this system into their tolling infrastructure to address traffic congestion, improve efficiency, and enhance revenue collection. Strong governmental support and policies have also contributed to early adoption. The region's strong emphasis on using technology to enhance infrastructural efficiency, which has created easier environment for the growth of the ETC market. Because of early adoption of technology, extensive and well-maintained highway networks, strong governmental support and environmental initiatives North America led the electronic toll collection market.

Asia Pacific is expected to hold the largest share of the electronic toll collection market in forecasting period of 2026-2034, due to the strong government support for infrastructure development and rapid urbanization and industrialization in this region. Asia Pacific is one of the most important high-potential markets for electronic toll collection systems as it is segmented into the countries like China, Japan, India and Rest of Asia Pacific countries. The increasing urban population has risen the more traffic congestion led to worse environment and increased in accidents. By reducing air pollution, the use of Electronic toll collection systems enhances the environment and prevents accidents.

Electronic Toll Collection Market Competitive Landscape

Major Key player of the Electronic Toll Collection Market are the Kapsch TrafficCom AG, Conduent, Inc., Thales, Cubic Corporation, TRMI Systems Integration, Transcore Holdings, Inc., Honeywell International, Inc., Mitsubishi Heavy Industries, Ltd. And others.

Kapsch is one of Austria's leading global technology companies, comprising various subsidiaries including the flagship company Kapsch TrafficCom. Renowned for its extensive Intelligent Transportation Systems (ITS) portfolio, Kapsch is actively addressing both current and future mobility challenges through innovative solutions. Kapsch TrafficCom delivers advanced technologies for transport and traffic, offering expertise in tolling, traffic management, smart urban mobility, road safety, and connected vehicles. Different parts of the Kapsch TrafficCom tolling portfolio are flexible, modular, and scalable, ensuring seamless integration across various systems and supporting sustainable mobility initiatives.

Cubic Corporation, a prominent player in the transportation and defense sectors, has a significant presence in the electronic toll collection (ETC) market through its subsidiary, Cubic Transportation Systems (CTS). The company’s ETC solutions are part of its broader portfolio of intelligent transportation systems (ITS), which cater to the needs of urban mobility and smart cities. Cubic's offerings in this space are primarily focused on providing end-to-end solutions that include both hardware and software components, such as automated fare collection systems, real-time traffic management, and integrated payment solutions. The company’s solutions are known for their reliability, scalability, and interoperability, which are crucial in managing high-volume traffic environments

|

Electronic Toll Collection Market Scope |

|

|

Market Size in 2025 |

USD 14.19 Billion |

|

Market Size in 2034 |

USD 27.89 Billion |

|

CAGR (2026-2034) |

7.8 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Type

|

|

By Technology

|

|

|

By Offerings

|

|

|

By Application

|

|

Key Regions

- North America (United States, Canada, Mexico)

- Eurospe (UK, France, Germany, Italy, Spain, Sweden, Austria, Rest of Europe)

- Asia Pacific (China, S Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, Rest of Asia Pacific)

- Middle East and Africa (South Africa, GCC, Egypt, Nigeria, Rest of MEA)

- South America (Brazil, Mexico, Rest of South America)

Key Players

- Kapsch TrafficCom AG

- Conduent, Inc.

- Thales

- Cubic Corporation

- TRMI Systems Integration

- Transcore Holdings, Inc.

- EFKON

- Honeywell International, Inc.

- Mitsubishi Heavy Industries, Ltd.

- Perceptics.

- Q-Free.

- IRD

- Toshiba Infrastructure Systems and Solutions Corp

- Magnetic Autocontrol GmbH

- The Revenue Markets Inc

- Sociedad Iberica de Construcciones Electricas SA

- P Square Solutions LLC

- Verra Mobility Corp

Frequently Asked Questions

The Kapsch Traffic Com AG, Conduent, Inc., Thales, Cubic Corporation, TRMI Systems Integration, Transcore Holdings, Inc., Honeywell International, Inc., Mitsubishi Heavy Industries, Ltd. And others, are the Major Key player of the Electronic Toll Collection Market.

Ans) The market size of the electronic toll collection market is USD 14.19 Billion in 2025.

Ans) The growth of the toll collection market is driven by the advancements in technology, increasing number of vehicle, and government initiatives to update road infrastructure.

1. Electronic Toll Collection: Research Methodology

2. Electronic Toll Collection: Competitive Landscape

2.1. Stellar Competition Matrix

2.2. Competitive Landscape

2.3. Key Players Benchmarking

2.4. Market Structure

2.4.1. Market Leaders

2.4.2. Market Followers

2.4.3. Emerging Players

2.5. Consolidation of the Market

3. Electronic Toll Collection: Executive Summary

4. Electronic Toll Collection: Dynamics

4.1. Market Drivers

4.2. Market Restraints

4.3. Market Opportunities

4.4. Market Challenges

4.5. Regulatory Landscape by Region

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Middle East and Africa

4.5.5. South America

5. Electronic Toll Collection Market Size and Forecast by Segments (by Value USD Billion)

5.1. Electronic Toll Collection Market Size and Forecast, by Product Type (2026-2034)

5.1.1. Automatic Vehicle Classification (AVC)

5.1.2. Violation Enforcement System (VES)

5.1.3. Automatic Vehicle Identification System (AVIS)

5.1.4. Others (Transaction Processing/Back Office)

5.2. Electronic Toll Collection Market Size and Forecast, by Technology (2026-2034)

5.2.1. Radio Frequency Identification (RFID)

5.2.2. Dedicated Short Range Communication (DSRC)

5.2.3. Global Navigation Satellite System (GNSS)/GPS

5.2.4. Others (Barcode-based ETC)

5.3. North America Electronic Toll Collection Market Size and Forecast, by Application (2026-2034)

5.3.1. Highways

5.3.2. Urban areas

5.4. Electronic Toll Collection Market Size and Forecast, by Offerings (2026-2034)

5.4.1. Hardware

5.4.2. Back Office

5.4.3. Other services

5.5. Electronic Toll Collection Market Size and Forecast, by Region (2026-2034)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Electronic Toll Collection Market Size and Forecast (by Value USD Billion)

6.1. North America Electronic Toll Collection Market Size and Forecast, by Product Type (2026-2034)

6.1.1. Automatic Vehicle Classification (AVC)

6.1.2. Violation Enforcement System (VES)

6.1.3. Automatic Vehicle Identification System (AVIS)

6.1.4. Others (Transaction Processing/Back Office)

6.2. North America Electronic Toll Collection Market Size and Forecast, by Technology (2026-2034)

6.2.1. Radio Frequency Identification (RFID)

6.2.2. Dedicated Short Range Communication (DSRC)

6.2.3. Global Navigation Satellite System (GNSS)/GPS

6.2.4. Others (Barcode-based ETC)

6.3. North America Electronic Toll Collection Market Size and Forecast, by Application (2026-2034)

6.3.1. Highways

6.3.2. Urban areas

6.4. North America Electronic Toll Collection Market Size and Forecast, by Offerings (2026-2034)

6.4.1. Hardware

6.4.2. Back Office

6.4.3. Other services

6.5. North America Electronic Toll Collection Market Size and Forecast, by Country (2026-2034)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Electronic Toll Collection Market Size and Forecast (by Value USD Billion)

7.1. Europe Electronic Toll Collection Market Size and Forecast, by Product Type (2026-2034)

7.1.1. Automatic Vehicle Classification (AVC)

7.1.2. Violation Enforcement System (VES)

7.1.3. Automatic Vehicle Identification System (AVIS)

7.1.4. Others (Transaction Processing/Back Office)

7.2. Europe Electronic Toll Collection Market Size and Forecast, by Technology (2026-2034)

7.2.1. Radio Frequency Identification (RFID)

7.2.2. Dedicated Short Range Communication (DSRC)

7.2.3. Global Navigation Satellite System (GNSS)/GPS

7.2.4. Others (Barcode-based ETC)

7.3. Europe Electronic Toll Collection Market Size and Forecast, by Application (2026-2034)

7.3.1. Highways

7.3.2. Urban areas

7.4. Europe Electronic Toll Collection Market Size and Forecast, by Offerings (2026-2034)

7.4.1. Hardware

7.4.2. Back Office

7.4.3. Other services

7.5. Europe Electronic Toll Collection Market Size and Forecast, by Country (2026-2034)

7.5.1. UK

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Austria

7.5.8. Rest of Europe

8. Asia Pacific Electronic Toll Collection Market Size and Forecast (by Value USD Billion)

8.1. Asia Pacific Electronic Toll Collection Market Size and Forecast, by Product Type (2026-2034)

8.1.1. Automatic Vehicle Classification (AVC)

8.1.2. Violation Enforcement System (VES)

8.1.3. Automatic Vehicle Identification System (AVIS)

8.1.4. Others (Transaction Processing/Back Office)

8.2. Asia Pacific Electronic Toll Collection Market Size and Forecast, by Technology (2026-2034)

8.2.1. Radio Frequency Identification (RFID)

8.2.2. Dedicated Short Range Communication (DSRC)

8.2.3. Global Navigation Satellite System (GNSS)/GPS

8.2.4. Others (Barcode-based ETC)

8.3. Asia Pacific Electronic Toll Collection Market Size and Forecast, by Application (2026-2034)

8.3.1. Highways

8.3.2. Urban areas

8.4. Asia Pacific Electronic Toll Collection Market Size and Forecast, by Offerings (2026-2034)

8.4.1. Hardware

8.4.2. Back Office

8.4.3. Other services

8.5. Asia Pacific Electronic Toll Collection Market Size and Forecast, by Country (2026-2034)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. Indonesia

8.5.7. Malaysia

8.5.8. Vietnam

8.5.9. Taiwan

8.5.10. Bangladesh

8.5.11. Pakistan

8.5.12. Rest of Asia Pacific

9. Middle East and Africa Electronic Toll Collection Market Size and Forecast (by Value USD Billion)

9.1. Middle East and Africa Electronic Toll Collection Market Size and Forecast, by Product Type (2026-2034)

9.1.1. Automatic Vehicle Classification (AVC)

9.1.2. Violation Enforcement System (VES)

9.1.3. Automatic Vehicle Identification System (AVIS)

9.1.4. Others (Transaction Processing/Back Office)

9.2. Middle East and Africa Electronic Toll Collection Market Size and Forecast, by Technology (2026-2034)

9.2.1. Radio Frequency Identification (RFID)

9.2.2. Dedicated Short Range Communication (DSRC)

9.2.3. Global Navigation Satellite System (GNSS)/GPS

9.2.4. Others (Barcode-based ETC)

9.3. Middle East and Africa Electronic Toll Collection Market Size and Forecast, by Application (2026-2034)

9.3.1. Highways

9.3.2. Urban areas

9.4. Middle East and Africa Electronic Toll Collection Market Size and Forecast, by Offerings (2026-2034)

9.4.1. Hardware

9.4.2. Back Office

9.4.3. Other services

9.5. Middle East and Africa Electronic Toll Collection Market Size and Forecast, by Country (2026-2034)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Egypt

9.5.4. Nigeria

9.5.5. Rest of MEA

10. South America Electronic Toll Collection Market Size and Forecast (by Value USD Billion)

10.1. South America Electronic Toll Collection Market Size and Forecast, by Product Type (2026-2034)

10.1.1. Automatic Vehicle Classification (AVC)

10.1.2. Violation Enforcement System (VES)

10.1.3. Automatic Vehicle Identification System (AVIS)

10.1.4. Others (Transaction Processing/Back Office)

10.2. South America Electronic Toll Collection Market Size and Forecast, by Technology (2026-2034)

10.2.1. Radio Frequency Identification (RFID)

10.2.2. Dedicated Short Range Communication (DSRC)

10.2.3. Global Navigation Satellite System (GNSS)/GPS

10.2.4. Others (Barcode-based ETC)

10.3. South America Electronic Toll Collection Market Size and Forecast, by Application (2026-2034)

10.3.1. Highways

10.3.2. Urban areas

10.4. South America Electronic Toll Collection Market Size and Forecast, by Offerings (2026-2034)

10.4.1. Hardware

10.4.2. Back Office

10.4.3. Other services

10.5. South America Electronic Toll Collection Market Size and Forecast, by Country (2026-2034)

10.5.1. Brazil

10.5.2. Mexico

10.5.3. Rest of South America

11. Company Profile: Key players

11.1. Kapsch TrafficCom AG

11.1.1. Company Overview

11.1.2. Financial Overview

11.1.3. Business Portfolio

11.1.4. SWOT Analysis

11.1.5. Business Strategy

11.1.6. Recent Developments

11.2. Conduent, Inc.

11.3. Transcore Holdings, Inc.

11.4. Thales

11.5. Cubic Corporation

11.6. TRMI Systems Integration

11.7. EFKON (Austria)

11.8. Honeywell International, Inc.

11.9. Mitsubishi Heavy Industries, Ltd.

11.10. Perceptics (U.S.)

11.11. Q-Free (Norway)

11.12. IRD (Canada)

11.13. Toshiba Infrastructure Systems and Solutions Corp

11.14. Magnetic Autocontrol GmbH

11.15. The Revenue Markets Inc

11.16. Sociedad Iberica de Construcciones Electricas SA

11.17. P Square Solutions LLC

11.18. Verra Mobility Corp

11.19. Others

12. Key Findings

13. Industry Recommendations