Dairy Foods Market Industry Overview, Size, Share, Growth Trends, Research Insights and Forecast 2026–2034

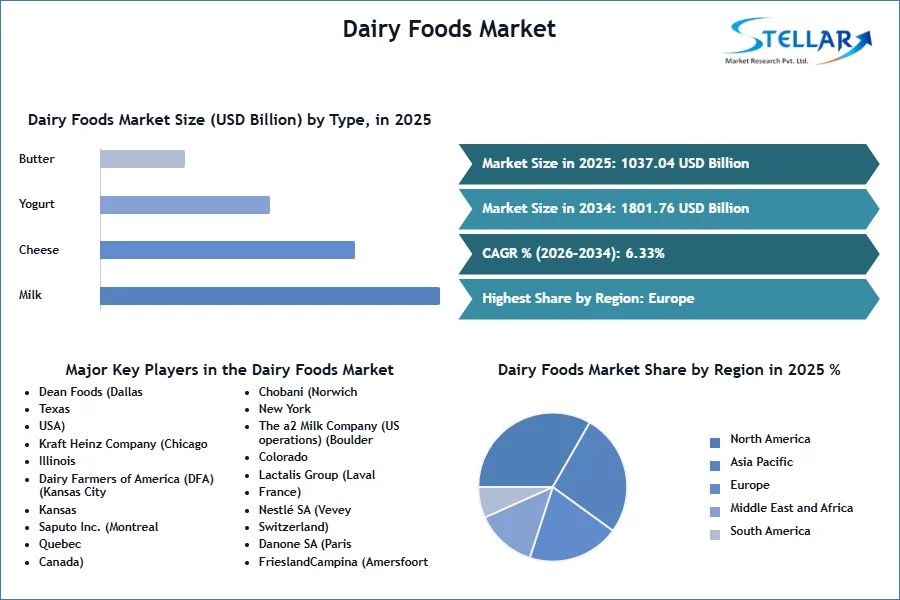

Dairy Foods Market was valued at USD 1037.04 Bn in 2025. Its total industry revenue is expected to grow by 6.33% from 2026 to 2034, reaching nearly USD 1801.76 Bn in 2034.

Dairy Foods Market Overview

Dairy foods include a number of products obtained from the milk, including fluid milk, cheese, yogurt, butter, ice cream, and other processed dairy items. Products are rich in an essential nutrient such as calcium, protein, and vitamins, making them a dietary staple worldwide. The category also includes lactose-free and plant-based dairy products, catering to developing the consumer preferences.

The market for dairy products is expanding since most consumers prefer diets high in protein and wellness. For people who are unable to consume normal milk, the companies are producing plant-based and lactose-free dairy products, such almond milk. The America and Europe are concentrating on the biological and premium dairy products, the China and India are increasing their milk consumption as a result of growing disposable incomes. Obstacles like the high cost of milk and the growing popularity of vegetarianism enhanced progress.

A big firms are creating the new flavours, healthier alternatives, and eco-friendly packaging to remain in the competition. Rapid growth of A2 milk products, which are simpler to digest than regular milk, is a remarkable trend in the dairy industry. Large firms are investing in the A2 milk production to enhance a consumer concern regarding the heath.

In 2025, New Zealand, the EU, and the U.S. dominate global dairy exports, supplying milk powder, cheese, and whey to top importers like China, Southeast Asia, and Africa. New Zealand leads in bulk exports (especially to China), while the EU excels in premium products like infant formula. The U.S. focuses on Mexico and Canada under USMCA. Trade faces hurdles like tariffs, regulations, and sustainability demands, but demand in emerging markets keeps dairy trade strong.

To get more Insights: Request Free Sample Report

Dairy Foods Market Dynamics

Health & Wellness to Drive Demand for Functional Dairy Products

Dairy Foods Market is going through a significant change towards health and welfare as consumers seek fast, protein-rich, probiotic, and functional dairy products. In addition, Greek yogurt, which is known for its high protein content and gut-friendly cultures, has become a necessity in a health-conscious diet. While being coupled with vitamins and minerals, it provides fortified nutritional value. Probiotic-rich products such as kefir and fermented beverages are receiving traction for their digestive and immune health benefits. Also, the lactose-free and lower-sugar dairy options are addressing dietary restrictions without compromising on nutrition. Sports nutrition and high-protein dairy snacks reflect the increasing demand for convenient, performance foods. The brands are also innovating to appeal to beauty and welfare trends with collagen-infused and omega-rich dairy. Since consumer preventive healthcare is preferred, functional dairy products combine traditional nutrition with modern health sciences. This trend underscores the focus of the industry on distributing the value-added products that align with developing wellness preferences.

Plant-Based Disruption to Reshape the Dairy Market Landscape

The dairy foods industry has faced growing competition from plant-based options such as almonds, oats, and soy milk, which has gained mainstream popularity among health-conscious and environmentally conscious consumers. These dairy-free options are no longer niche products; innovation with global brands and startups with Barista-grade oat milk and protein-species almond varieties. Retail shelves now dedicate similar places to plant-based options, reflecting their 15–20% annual growth. Many markets describe traditional dairy. Environmental concerns drive this change, as consumers look at more sustainable plant-based options than traditional dairy production. However, the industry is responding with hybrid products and lactose-free innovations to maintain market share, their premium pricing and Gen Z/Millennial Appeals keep them in position for continuous expansion, forcing dairy players to adapt or cooperate in this developed landscape.

Precision Fermentation and Lab-Grown Dairy to Redefine Sustainable Food Technology

The dairy foods industry is undergoing a high-technological revolution because accurate fermentation and cellular agriculture enable actual dairy proteins without animals. Startups such as Perfect Day and Remillk use microbial fermentation to create similar whey and casein proteins, providing lactose-free, low-carbon dairy options with similar functionality to traditional products. Meanwhile, lab-grown dairy promotes real milk without the environmental footprint of industrial farming, manufactured by the enhancement of breast cells. These technologies address significant stability challenges, reducing greenhouse gas emissions by 90% compared to traditional dairy production. While regulatory barriers and scaling costs remain obstructions, the major Food Corporations are investing heavily, expecting the FDA/EFSA approval, the global princely fermentation dairy market can reach $ 40 billion by 2032, indicating a fundamental change that we produce dairy-blending aware consumers, increase food science with stability to meet demand.

Dairy Foods Market Segment Analysis

Based on type, the Dairy Foods Market is divided into Milk, Cheese, Yogurt, Butter, and Others. Milk dominates the dairy market as the most consumed product globally, serving as a dietary staple in all age groups. Its leadership stems from universal availability, nutritional value (rich in calcium and protein), and versatility in both liquid and processed forms. Emerging markets increase in volume through rising income and government nutritional programs, while the developed markets focus on the valuable variants such as lactose-free, organic, and stronghold milk. Although cheese and yogurt show rapid price increases due to their premium, milk maintains its top position through essential daily consumption and inexpensive pricing. There is a demand to pursue innovations like A2 milk and functional formulations. Intensive integration of segments in food culture and the economies of scale in production are dominated by cement. Even with plant-based competition, traditional milk is irreplaceable in most homes worldwide.

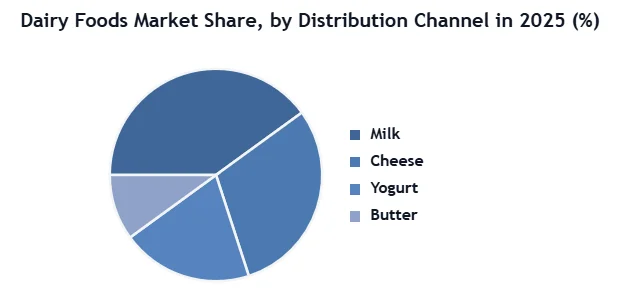

Based on distribution channel, Supermarkets/hypermarkets dominate dairy distribution and capture the largest market share due to their ability to offer a one-stop purchasing experience with diverse dairy products under one roof. This retail format thrives on bulk purchases, frequent publicity, and reliable cold chain management, important for bad goods such as milk and yogurt. Their scale allows competitive pricing and personally labeled expansion, which appeals to cost-conscious consumers. While e-commerce achieves traction with doorstep delivery, supermarkets maintain an edge through immediate access and in-store quality checks, especially in emerging markets. Specialty stores serve premium products such as organic or artisanal dairy but lack mainstream access. B2B channels (restaurants, manufacturers) drive volume but work on a low margin. The trust, convenience, and impulsive appeal of the supermarket/hypermarket cement their leadership, although the online grocery is continuously shaping the dairy foods landscape.

Based on end-user, Residential users are the primary consumers of dairy, holding the largest market share, as households frequently buy milk, cheese, and yogurt for their daily meals and nutrition. Families sustain steady demand through regular grocery shopping, focusing on essentials like liquid milk and breakfast dairy products. While commercial sectors (restaurants, manufacturers) buy in bulk, residential buyers fuel higher retail margins through branded and premium dairy foods products. The segment benefits from dairy’s essential role in home cooking, children’s diets, and snacking. Rising health awareness further boosts the demand for fortified, organic, and functional dairy in households. Unlike commercial demand, which fluctuates with food service trends, residential consumption remains stable, reinforcing its market leadership. Emerging markets, in particular, show strong household-driven growth due to expanding middle-class populations and dietary shifts.

Dairy Foods Market Regional Analysis

Europe Dominates Dairy Foods Market Through Premium Products And Health Trends

Europe dominates in the Global Dairy Foods Market, mainly due to its strong tradition of dairy consumption and high demand for advanced processing technologies of functional and premium dairy products. The region consumes probiotic dairy, which contains yogurt and kefir staple foods that are supported by extensive awareness about health benefits. Additionally, innovation in Europe's strict quality standards and organic, lactose-free, and stronghold dairy products further strengthens its market status. Countries such as Germany, France, and the Netherlands are major contributors, with a growing preference for well-established dairy industries and permanent on health-centered dairy options. This combination of cultural preference, regulatory support, and consumer trends strengthens Europe's dominance in the global dairy market.

Dairy Foods Market Competitive Landscape

Dairy Foods Market is highly competitive, leading to global giants such as Nestle, Danone, and Lactalis through strong brand recognition and diverse product portfolios. These players compete with regional leaders such as Amul (India) and Mengniu (China), which dominate the local markets. Oatly and accurate fermentation startups (eg, Perfect Day) are disrupting the sector-based innovator sector, pushing traditional brands to expand dairy options. Competition intensifies because companies invest in functional dairy (probiotic yogurt, protein-rich milk) and stability initiatives (carbon-plate production, eco-packing). Privately labeled products are receiving traction in cost-sensitive markets, putting pressure on branded players. Missing, acquisitions, and partnerships remain an important strategy for development and market expansion. The rise of e-commerce and D2C models is reshaping competitive mobility in favor of agile and digitally loving brands.

|

Dairy Foods Market Scope |

|

|

Market Size in 2025 |

USD 1037.04 Bn. |

|

Market Size in 2034 |

USD 1801.76 Bn. |

|

CAGR (2026-2034) |

6.33 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Type Milk Cheese Yogurt Butter Others |

|

By Distribution Channel Supermarkets/Hypermarkets Specialty Stores B2B E-Commerce |

|

|

By End User Commercial Residential |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, Malaysia, Indonesia, Philippines, Vietnam, Thailand, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Players in the Dairy Foods Market

North America

- Dean Foods (Dallas, Texas, USA)

- Kraft Heinz Company (Chicago, Illinois, USA)

- Dairy Farmers of America (DFA) (Kansas City, Kansas, USA)

- Saputo Inc. (Montreal, Quebec, Canada)

- Chobani (Norwich, New York, USA)

- The a2 Milk Company (US operations) (Boulder, Colorado, USA)

Europe

- Lactalis Group (Laval, France)

- Nestlé SA (Vevey, Switzerland)

- Danone SA (Paris, France)

- FrieslandCampina (Amersfoort, Netherlands)

- Hochland SE (Heimenkirch, Germany)

- Arla Foods (Viby, Denmark)

- Granarolo S.p.A. (Bologna, Italy)

- Emmi Group (Lucerne, Switzerland)

Asia-Pacific

- Amul (GCMMF) (Anand, Gujarat, India)

- Yili Group (Hohhot, Inner Mongolia, China)

- Mengniu Dairy (Hohhot, Inner Mongolia, China)

- Meiji Holdings (Tokyo, Japan)

- Fonterra Co-operative Group (Auckland, New Zealand)

- Bega Cheese (Bega, New South Wales, Australia)

- Seoul Dairy Cooperative (Seoul, South Korea)

Middle East & Africa

- Almarai Company (Riyadh, Saudi Arabia)

- National Food Products Company (NFPC) (Abu Dhabi, UAE)

- Clover Industries (Pretoria, South Africa)

South America

- BRF S.A. (São Paulo, Brazil)

- SanCor Cooperatives (Sunchales, Argentina)

- Soprole (Santiago, Chile)

Frequently Asked Questions

A2 milk, probiotic yogurt, and functional dairy (protein-collagen blends) cater to health trends.

Environmental concerns and perceived health benefits propel demand for almond, oat, and soy milk, especially among Gen Z and millennials.

Consumers increasingly seek protein-rich, probiotic, and fortified dairy for gut health, immunity, and overall wellness, driving demand for Greek yogurt, kefir, and lactose-free options.

Due to established consumption patterns, strong dairy traditions, and advanced processing technologies.

1. Dairy Foods Market Introduction

1.1. Study Assumption and Market Definition

1.2. Scope of the Study

1.3. Executive Summary

2. Global Dairy Foods Market: Competitive Landscape

2.1. SMR Competition Matrix

2.2. Key Players Benchmarking

2.2.1. Company Name

2.2.2. Service Segment

2.2.3. End-User Segment

2.2.4. Revenue (2025)

2.2.5. Geographical Presence

2.3. Market Structure

2.3.1. Market Leaders

2.3.2. Market Followers

2.3.3. Emerging Players

2.4. Mergers and Acquisitions Details

3. Dairy Foods Market: Dynamics

3.1. Dairy Foods Market Trends

3.2. Dairy Foods Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

3.2.4. Challenges

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

3.5. Regulatory Landscape by Region

3.6. Key Opinion Leader Analysis For the Global Industry

3.7. Analysis of Government Schemes and Initiatives for Industry

4. Dairy Foods Market: Global Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

4.1. Dairy Foods Market Size and Forecast, By Type (2026-2034)

4.1.1. Milk

4.1.2. Cheese

4.1.3. Yogurt

4.1.4. Butter

4.1.5. Others

4.2. Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

4.2.1. Supermarkets/Hypermarkets

4.2.2. Specialty Stores

4.2.3. B2B

4.2.4. E-Commerce

4.3. Dairy Foods Market Size and Forecast, By End-User (2026-2034)

4.3.1. Commercial

4.3.2. Residential

4.4. Dairy Foods Market Size and Forecast, By Region (2026-2034)

4.4.1. North America

4.4.2. Europe

4.4.3. Asia Pacific

4.4.4. Middle East and Africa

4.4.5. South America

5. North America Dairy Foods Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

5.1. North America Dairy Foods Market Size and Forecast, By Type (2026-2034)

5.1.1. Milk

5.1.2. Cheese

5.1.3. Yogurt

5.1.4. Butter

5.1.5. Others

5.2. North America Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

5.2.1. Supermarkets/Hypermarkets

5.2.2. Specialty Stores

5.2.3. B2B

5.2.4. E-Commerce

5.3. North America Dairy Foods Market Size and Forecast, By End-User (2026-2034)

5.3.1. Commercial

5.3.2. Residential

5.4. North America Dairy Foods Market Size and Forecast, by Country (2026-2034)

5.4.1. United States

5.4.1.1. United States Dairy Foods Market Size and Forecast, By Type (2026-2034)

5.4.1.1.1. Milk

5.4.1.1.2. Cheese

5.4.1.1.3. Yogurt

5.4.1.1.4. Butter

5.4.1.1.5. Others

5.4.1.2. United States Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

5.4.1.2.1. Supermarkets/Hypermarkets

5.4.1.2.2. Specialty Stores

5.4.1.2.3. B2B

5.4.1.2.4. E-Commerce

5.4.1.3. United States Dairy Foods Market Size and Forecast, By End-User (2026-2034)

5.4.1.3.1. Commercial

5.4.1.3.2. Residential

5.4.2. Canada

5.4.2.1. Canada Dairy Foods Market Size and Forecast, By Type (2026-2034)

5.4.2.1.1. Milk

5.4.2.1.2. Cheese

5.4.2.1.3. Yogurt

5.4.2.1.4. Butter

5.4.2.1.5. Others

5.4.2.2. Canada Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

5.4.2.2.1. Supermarkets/Hypermarkets

5.4.2.2.2. Specialty Stores

5.4.2.2.3. B2B

5.4.2.2.4. E-Commerce

5.4.2.3. Canada Dairy Foods Market Size and Forecast, By End-User (2026-2034)

5.4.2.3.1. Commercial

5.4.2.3.2. Residential

5.4.3. Mexico

5.4.3.1. Mexico Dairy Foods Market Size and Forecast, By Type (2026-2034)

5.4.3.1.1. Milk

5.4.3.1.2. Cheese

5.4.3.1.3. Yogurt

5.4.3.1.4. Butter

5.4.3.1.5. Others

5.4.3.2. Mexico Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

5.4.3.2.1. Supermarkets/Hypermarkets

5.4.3.2.2. Specialty Stores

5.4.3.2.3. B2B

5.4.3.2.4. E-Commerce

5.4.3.3. Mexico Dairy Foods Market Size and Forecast, By End-User (2026-2034)

5.4.3.3.1. Commercial

5.4.3.3.2. Residential

6. Europe Dairy Foods Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

6.1. Europe Dairy Foods Market Size and Forecast, By Type (2026-2034)

6.2. Europe Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

6.3. Europe Dairy Foods Market Size and Forecast, By End-User (2026-2034)

6.4. Europe Dairy Foods Market Size and Forecast, by Country (2026-2034)

6.4.1. United Kingdom

6.4.1.1. United Kingdom Dairy Foods Market Size and Forecast, By Type (2026-2034)

6.4.1.2. United Kingdom Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

6.4.1.3. United Kingdom Dairy Foods Market Size and Forecast, By End-User (2026-2034)

6.4.2. France

6.4.2.1. France Dairy Foods Market Size and Forecast, By Type (2026-2034)

6.4.2.2. France Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

6.4.2.3. France Dairy Foods Market Size and Forecast, By End-User (2026-2034)

6.4.3. Germany

6.4.3.1. Germany Dairy Foods Market Size and Forecast, By Type (2026-2034)

6.4.3.2. Germany Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

6.4.3.3. Germany Dairy Foods Market Size and Forecast, By End-User (2026-2034)

6.4.4. Italy

6.4.4.1. Italy Dairy Foods Market Size and Forecast, By Type (2026-2034)

6.4.4.2. Italy Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

6.4.4.3. Italy Dairy Foods Market Size and Forecast, By End-User (2026-2034)

6.4.5. Spain

6.4.5.1. Spain Dairy Foods Market Size and Forecast, By Type (2026-2034)

6.4.5.2. Spain Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

6.4.5.3. Spain Dairy Foods Market Size and Forecast, By End-User (2026-2034)

6.4.6. Sweden

6.4.6.1. Sweden Dairy Foods Market Size and Forecast, By Type (2026-2034)

6.4.6.2. Sweden Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

6.4.6.3. Sweden Dairy Foods Market Size and Forecast, By End-User (2026-2034)

6.4.7. Russia

6.4.7.1. Russia Dairy Foods Market Size and Forecast, By Type (2026-2034)

6.4.7.2. Russia Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

6.4.7.3. Russia Dairy Foods Market Size and Forecast, By End-User (2026-2034)

6.4.8. Rest of Europe

6.4.8.1. Rest of Europe Dairy Foods Market Size and Forecast, By Type (2026-2034)

6.4.8.2. Rest of Europe Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

6.4.8.3. Rest of Europe Dairy Foods Market Size and Forecast, By End-User (2026-2034)

7. Asia Pacific Dairy Foods Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

7.1. Asia Pacific Dairy Foods Market Size and Forecast, By Type (2026-2034)

7.2. Asia Pacific Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

7.3. Asia Pacific Dairy Foods Market Size and Forecast, By End-User (2026-2034)

7.4. Asia Pacific Dairy Foods Market Size and Forecast, by Country (2026-2034)

7.4.1. China

7.4.1.1. China Dairy Foods Market Size and Forecast, By Type (2026-2034)

7.4.1.2. China Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.1.3. China Dairy Foods Market Size and Forecast, By End-User (2026-2034)

7.4.2. S Korea

7.4.2.1. S Korea Dairy Foods Market Size and Forecast, By Type (2026-2034)

7.4.2.2. S Korea Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.2.3. S Korea Dairy Foods Market Size and Forecast, By End-User (2026-2034)

7.4.3. Japan

7.4.3.1. Japan Dairy Foods Market Size and Forecast, By Type (2026-2034)

7.4.3.2. Japan Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.3.3. Japan Dairy Foods Market Size and Forecast, By End-User (2026-2034)

7.4.4. India

7.4.4.1. India Dairy Foods Market Size and Forecast, By Type (2026-2034)

7.4.4.2. India Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.4.3. India Dairy Foods Market Size and Forecast, By End-User (2026-2034)

7.4.5. Australia

7.4.5.1. Australia Dairy Foods Market Size and Forecast, By Type (2026-2034)

7.4.5.2. Australia Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.5.3. Australia Dairy Foods Market Size and Forecast, By End-User (2026-2034)

7.4.6. Indonesia

7.4.6.1. Indonesia Dairy Foods Market Size and Forecast, By Type (2026-2034)

7.4.6.2. Indonesia Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.6.3. Indonesia Dairy Foods Market Size and Forecast, By End-User (2026-2034)

7.4.7. Malaysia

7.4.7.1. Malaysia Dairy Foods Market Size and Forecast, By Type (2026-2034)

7.4.7.2. Malaysia Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.7.3. Malaysia Dairy Foods Market Size and Forecast, By End-User (2026-2034)

7.4.8. Philippines

7.4.8.1. Philippines Dairy Foods Market Size and Forecast, By Type (2026-2034)

7.4.8.2. Philippines Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.8.3. Philippines Dairy Foods Market Size and Forecast, By End-User (2026-2034)

7.4.9. Thailand

7.4.9.1. Thailand Dairy Foods Market Size and Forecast, By Type (2026-2034)

7.4.9.2. Thailand Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.9.3. Thailand Dairy Foods Market Size and Forecast, By End-User (2026-2034)

7.4.10. Vietnam

7.4.10.1. Vietnam Dairy Foods Market Size and Forecast, By Type (2026-2034)

7.4.10.2. Vietnam Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.10.3. Vietnam Dairy Foods Market Size and Forecast, By End-User (2026-2034)

7.4.11. Rest of Asia Pacific

7.4.11.1. Rest of Asia Pacific Dairy Foods Market Size and Forecast, By Type (2026-2034)

7.4.11.2. Rest of Asia Pacific Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.11.3. Rest of Asia Pacific Dairy Foods Market Size and Forecast, By End-User (2026-2034)

8. Middle East and Africa Dairy Foods Market Size and Forecast (by Value in USD Billion) (2024-2032

8.1. Middle East and Africa Dairy Foods Market Size and Forecast, By Type (2026-2034)

8.2. Middle East and Africa Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

8.3. Middle East and Africa Dairy Foods Market Size and Forecast, By End-User (2026-2034)

8.4. Middle East and Africa Dairy Foods Market Size and Forecast, by Country (2026-2034)

8.4.1. South Africa

8.4.1.1. South Africa Dairy Foods Market Size and Forecast, By Type (2026-2034)

8.4.1.2. South Africa Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

8.4.1.3. South Africa Dairy Foods Market Size and Forecast, By End-User (2026-2034)

8.4.2. GCC

8.4.2.1. GCC Dairy Foods Market Size and Forecast, By Type (2026-2034)

8.4.2.2. GCC Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

8.4.2.3. GCC Dairy Foods Market Size and Forecast, By End-User (2026-2034)

8.4.3. Egypt

8.4.3.1. Egypt Dairy Foods Market Size and Forecast, By Type (2026-2034)

8.4.3.2. Egypt Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

8.4.3.3. Egypt Dairy Foods Market Size and Forecast, By End-User (2026-2034)

8.4.4. Nigeria

8.4.4.1. Nigeria Dairy Foods Market Size and Forecast, By Type (2026-2034)

8.4.4.2. Nigeria Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

8.4.4.3. Nigeria Dairy Foods Market Size and Forecast, By End-User (2026-2034)

8.4.5. Rest of ME&A

8.4.5.1. Rest of ME&A Dairy Foods Market Size and Forecast, By Type (2026-2034)

8.4.5.2. Rest of ME&A Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

8.4.5.3. Rest of ME&A Dairy Foods Market Size and Forecast, By End-User (2026-2034)

9. South America Dairy Foods Market Size and Forecast by Segmentation (by Value in USD Billion) (2024-2032

9.1. South America Dairy Foods Market Size and Forecast, By Type (2026-2034)

9.2. South America Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

9.3. South America Dairy Foods Market Size and Forecast, By End-User (2026-2034)

9.4. South America Dairy Foods Market Size and Forecast, by Country (2026-2034)

9.4.1. Brazil

9.4.1.1. Brazil Dairy Foods Market Size and Forecast, By Type (2026-2034)

9.4.1.2. Brazil Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

9.4.1.3. Brazil Dairy Foods Market Size and Forecast, By End-User (2026-2034)

9.4.2. Argentina

9.4.2.1. Argentina Dairy Foods Market Size and Forecast, By Type (2026-2034)

9.4.2.2. Argentina Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

9.4.2.3. Argentina Dairy Foods Market Size and Forecast, By End-User (2026-2034)

9.4.3. Colombia

9.4.3.1. Colombia Dairy Foods Market Size and Forecast, By Type (2026-2034)

9.4.3.2. Colombia Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

9.4.3.3. Colombia Dairy Foods Market Size and Forecast, By End-User (2026-2034)

9.4.4. Chile

9.4.4.1. Chile Dairy Foods Market Size and Forecast, By Type (2026-2034)

9.4.4.2. Chile Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

9.4.4.3. Chile Dairy Foods Market Size and Forecast, By End-User (2026-2034)

9.4.5. Rest Of South America

9.4.5.1. Rest Of South America Dairy Foods Market Size and Forecast, By Type (2026-2034)

9.4.5.2. Rest Of South America Dairy Foods Market Size and Forecast, By Distribution Channel (2026-2034)

9.4.5.3. Rest Of South America Dairy Foods Market Size and Forecast, By End-User (2026-2034)

10. Company Profile: Key Players

10.1. Dean Foods (Dallas, Texas, USA)

10.1.1. Company Overview

10.1.2. Business Portfolio

10.1.3. Financial Overview

10.1.4. SWOT Analysis

10.1.5. Strategic Analysis

10.1.6. Recent Developments

10.2. Kraft Heinz Company (Chicago, Illinois, USA)

10.3. Dairy Farmers of America (DFA) (Kansas City, Kansas, USA)

10.4. Saputo Inc. (Montreal, Quebec, Canada)

10.5. Chobani (Norwich, New York, USA)

10.6. The a2 Milk Company (US operations) (Boulder, Colorado, USA)

10.7. Lactalis Group (Laval, France)

10.8. Nestlé SA (Vevey, Switzerland)

10.9. Danone SA (Paris, France)

10.10. FrieslandCampina (Amersfoort, Netherlands)

10.11. Hochland SE (Heimenkirch, Germany)

10.12. Arla Foods (Viby, Denmark)

10.13. Granarolo S.p.A. (Bologna, Italy)

10.14. Emmi Group (Lucerne, Switzerland)

10.15. Amul (GCMMF) (Anand, Gujarat, India)

10.16. Yili Group (Hohhot, Inner Mongolia, China)

10.17. Mengniu Dairy (Hohhot, Inner Mongolia, China)

10.18. Meiji Holdings (Tokyo, Japan)

10.19. Fonterra Co-operative Group (Auckland, New Zealand)

10.20. Bega Cheese (Bega, New South Wales, Australia)

10.21. Seoul Dairy Cooperative (Seoul, South Korea)

10.22. Almarai Company (Riyadh, Saudi Arabia)

10.23. National Food Products Company (NFPC) (Abu Dhabi, UAE)

10.24. Clover Industries (Pretoria, South Africa)

10.25. BRF S.A. (São Paulo, Brazil)

10.26. SanCor Cooperatives (Sunchales, Argentina)

10.27. Soprole (Santiago, Chile)

11. Key Findings

12. Industry Recommendations

13. Dairy Foods Market: Research Methodology