Brake System Market: Global analysis and forecast for the period 2026-2034

The Brake System Market was valued at USD 36.31 Bn. in the year 2025 and is expected to reach USD 53.08 Bn. by 2034 with a growing CAGR of 4.31% over the forecast period of 2026-2034.

Brake System Market Overview:

The brake system in an automobile serves as a fundamental pillar of both safety and control. Its intricate mechanisms and components are designed to effectively slow down or halt a vehicle, translating kinetic energy into heat through friction. Brakes are essential for navigating traffic, negotiating corners, and responding to sudden obstacles on the road. With advancements in technology, various types of braking systems have emerged, each tailored to cater to different vehicle models and driving conditions. From traditional drum and disc brakes to more sophisticated anti-lock braking systems (ABS), the evolution of braking systems highlights their pivotal role in ensuring safety and optimal performance on the road.

The brake system market is undergoing significant transformations driven by advancements in electrification and technology. The rise of electric, hybrid, and plug-in-hybrid vehicles necessitates sophisticated braking systems, with regenerative braking being a key development. This technology recovers energy during braking, improving energy efficiency and extending driving range. Additionally, the integration of Advanced Driver Assistance Systems (ADAS) demands advanced braking solutions that offer precise and timely responses to various driving conditions. The expansion of automotive aftermarket services is another crucial driver, with increased vehicle maintenance awareness and the growth of service centres enhancing demand for brake system components.

Brake-by-wire systems represent a significant market opportunity, offering benefits such as reduced weight and improved performance through electronic controls. However, cost pressures and supply chain disruptions present challenges. Manufacturers must balance high-performance systems with affordability while navigating global supply chain issues. The brake system market is divided in segments such as type, vehicle type, component, actuation, technology. Asia Pacific leads with its low-cost production advantages and growing automotive demand, while North America is expected to grow at the highest CAGR.

.webp)

To get more Insights: Request Free Sample Report

Brake System Market Trend:

Electrification and Advanced Technologies

The rise of electric, hybrid, plug-in-hybrid vehicles is significantly influencing the brake system market, as these vehicles require advanced braking technologies to enhance performance and efficiency. Regenerative braking systems are a key development, allowing electric and hybrid vehicles to recover energy during braking and convert it back to electrical power. This not only improves energy efficiency but also extends the driving range of these vehicles.

Moreover, the integration of Advanced Driver Assistance Systems (ADAS) in modern vehicles is pushing the evolution of braking technologies. Features like automatic emergency braking and adaptive cruise control necessitate sophisticated brake systems that can respond accurately and promptly to various driving conditions.

- Volvo’s City Safety system uses ADAS to automatically apply brakes if a collision risk is detected, enhancing safety and driver confidence.

- Tesla’s Model S uses regenerative braking to increase range and enhance overall driving dynamics. These advancements are driving market growth as automakers and suppliers invest in research and development to meet the increasing demand for high-performance, reliable, and efficient brake systems. As a result, the market is experiencing a shift towards more advanced and integrated braking solutions, reflecting broader trends in automotive technology.

Brake System Market Dynamics:

Brake System Market Driver:

Expansion of Automotive Aftermarket

The expansion of automotive repair and service centers, coupled with heightened vehicle maintenance awareness, significantly impacts the brake system market. As the number of service centers grows, particularly in emerging markets, more consumers have access to regular maintenance and repair services, which include brake system upkeep. This expansion leads to increased demand for brake system components, as these service centers require a steady supply of parts for replacement and repairs. Furthermore, rising awareness among vehicle owners about the importance of regular maintenance for vehicle safety and performance encourages proactive replacement of brake components. Consumers are more likely to invest in high-quality brake parts to ensure optimal performance and safety, boosting the market for advanced braking technologies.

- Firestone Complete Auto Care: With a broad network of service centers across North America, Firestone facilitates widespread access to brake system services, contributing to increased demand for brake parts and maintenance services.

- Midas: As a global leader in automotive repair services, Midas offers comprehensive brake system services. Their expansion into new markets and commitment to quality service drives both the demand for brake system parts and the adoption of advanced braking technologies.

Brake System Market Opportunity:

Brake-by-wire systems represent a significant innovation in brake system market replacing traditional mechanical linkages with electronic controls. This shift offers multiple advantages, including reduced weight, which can enhance vehicle fuel efficiency, and improved performance through precise control and faster response times. By eliminating physical components like hydraulic lines and mechanical linkages, brake-by-wire systems also allow for more flexible vehicle design and integration with advanced driver assistance systems (ADAS).

The adoption of brake-by-wire systems is set to grow as advancements in electronics and increasing consumer demand for more efficient, responsive braking solutions drive Brake System Market expansion. The ability to integrate these systems with sophisticated safety features, such as automatic emergency braking and adaptive cruise control, enhances overall vehicle safety and performance.

- Bosch's iBooster is a notable example of a brake-by-wire system that combines electronic control with regenerative braking technology. This system improves braking efficiency and contributes to overall vehicle performance while reducing weight.

- Tesla’s Model S utilizes an advanced brake-by-wire system that integrates with its Autopilot suite, offering precise control and enhanced safety features. The system not only improves the vehicle’s performance but also supports Tesla’s push toward greater automation and efficiency.

Brake System Market Challenge:

Cost Pressures and Supply Chain Issues

Balancing high-performance brake systems with affordability is a significant challenge in the brake system emarket. Manufacturers must ensure that advanced braking technologies, such as ABS and regenerative braking systems, remain cost-effective without compromising quality. This balancing act often involves investing in R&D to innovate cost-efficient manufacturing processes and materials. The impact on the market includes potential price increases for consumers, reduced profit margins for manufacturers, and a constant push for cost optimization.

- Bosch has heavily invested in R&D to develop cost-effective, high-quality brake components, maintaining its competitive edge. Similarly, Brembo focuses on optimizing production processes to offer high-performance brakes at competitive prices, ensuring market sustainability.

The global supply chain's vulnerability to disruptions, such as geopolitical tensions or pandemics, poses significant risks to the brake system market. Supply chain disruptions can lead to delays in the availability of raw materials, increased costs, and production halts. These challenges can result in higher prices for end consumers and strained relationships with OEMs.

- Continental faced challenges in maintaining its supply chain during the pandemic, prompting the company to reassess its supply chain strategies. Similarly, Aptiv experienced disruptions that led to increased costs and delays, necessitating a strategic focus on supply chain resilience and diversification.

Brake System Market Segment Analysis:

By Type: The brake systems market is divided into drum brakes and disc brakes based on type. In 2025, the disc brake sector dominated with a market share of XX.X%. Recently, there has been a substantial increase in the use of disc brakes. Disc brakes have become popular due to their ability to function effectively in challenging weather conditions without overheating or losing performance. Furthermore, the disc brake segment's expansion is being driven even more by its ability to work with other sophisticated systems.

The gas extractors in the drum brake section will likely show a notable compound annual growth rate of 4.1% during the expected time frame. Drum brakes use a closed design and circular brake shoes to create the needed friction for reducing speed. On the flip side, disc brakes utilize a slender rotor and caliper to halt wheel rotation. Therefore, performance is negatively impacted. Even though discs have greater braking power than drums, car manufacturers opt for drums due to their cost efficiency.

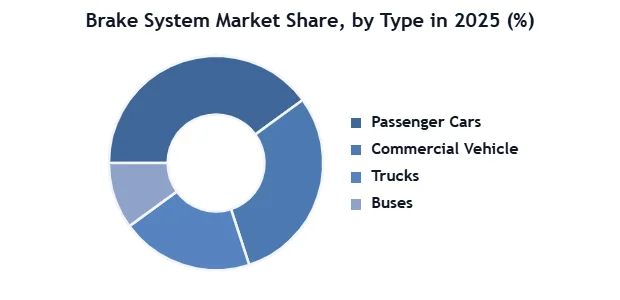

By Vehicle Type: The brake system market based on vehicle is divided into commercial vehicles and passenger cars. In 2025, passenger cars held the largest market share at XX.X% in terms of revenue. The number of passenger cars is on the rise because of the growth in population, disposable income, and urbanization. Manufacturers focus on improving braking systems to enhance safety features. The primary brake system market share and growth of passenger cars are mostly influenced by the ADAS system. Moreover, the rise in spending on ADAS is projected to impact the brake systems industry by driving up demand for electromagnetic induction braking systems in various vehicles like automobiles and motorcycles in the upcoming period.

However, the commercial vehicles sector is projected to experience substantial growth with a 5.3% CAGR during the predicted timeframe. The global need for commercial vehicles like trucks, buses, and vans has consistently risen. The increase is a result of the growth of online retail, increasing demand for shipping and transportation services, and expansion in sectors such as construction and mining. With the growth of the commercial vehicle fleet, the need for dependable and effective braking systems is also increasing.

Based on technology Brake system market is divided into antilock brake systems (ABS), traction control systems, electronic stability control, and electronic brake-force distribution. In 2024, Electronic Stability Control (ESC) had the largest market share of revenue at XX.XX%. The perception of benefits in regaining vehicle control in an emergency is leading to increased adoption of electronic stability control technology. Hence, it is anticipated to stimulate market growth in the forecast period. During the forecast period, the ABS sector experienced a notable compound annual growth rate of 32.3%. The increase in ABS technology is a result of the determined actions of a number of car manufacturers pushing for the required installation of ABS in important areas.

It is anticipated that the Traction Control System (TCS) sector will experience substantial growth with a CAGR of 6.6%. The TCS technology enhances safety by maintaining traction in challenging driving conditions. TCS is commonly utilized alongside anti-lock braking systems to enhance effectiveness. Traction control prevents the wheels from spinning by using ABS to apply brake pressure and managing the throttle.

Brake System Market Regional Insights:

Asia Pacific held the majority share of revenue in 2025 with XX.X% dominance in the brake system market. Because of the presence of inexpensive labor and materials, local businesses provide substantial cost reductions. Moreover, China and India, along with other countries, serve as important centers for automotive manufacturing. Market growth is anticipated to be propelled by the increasing demand for automotive brake systems and the higher sales of luxury and premium vehicles. Furthermore, the rise in the number of accidents and the increase in sales of cars also play a role in the overall market expansion.

It is anticipated that North America will experience the highest Compound Annual Growth Rate (CAGR) of 5.7% throughout the forecast period. The brake system market in this region has expanded due to the increasing demand for improved vehicle performance in bad weather, major car manufacturers being present, and a rise in the supply of light commercial vehicles and passenger cars. In addition, the regional market growth has been propelled by the requirement for ESC technology to be installed in all light cars since 2020.

Brake System Market Competitive Landscape:

Bosch and Hitachi Astemo are leaders in brake system market, each with distinct strategies and innovations. Bosch prioritizes advanced electronic and integrated braking systems, emphasizing safety, efficiency, and digital integration. Their sustainability efforts focus on eco-friendly products and manufacturing processes, particularly for electric vehicles. Financially, Bosch's automotive segment significantly contributes to their €87 billion revenue in 2024, with substantial R&D investments in automotive technology. Innovations like the eCall system and ADAS integration highlight their commitment to safety and performance.

In contrast, Hitachi Astemo concentrates on cutting-edge active safety systems and electric brake actuators, with a strong global expansion strategy targeting emerging markets. As part of the Hitachi Group, their automotive segment is a key revenue driver within the ¥10 trillion reported in 2024. Heavy R&D investments help maintain their competitive edge. Hitachi Astemo’s innovations in next-gen active brake systems and electric brakes cater to modern vehicle demands, including autonomous driving.

Brake System Market Scope

|

Brake System Market |

|

|

Market Size in 2025 |

USD 36.31 billion |

|

Market Size in 2034 |

USD 53.08 billion |

|

CAGR (2026-2034) |

4.31 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Brake System Market Segments |

By Type Disc Brake Drum Brake |

|

By Technology Anti-lock braking system Electronic stability control Traction control system Electronic brakeforce distribution Automatic emergency braking |

|

|

By Component Master cylinders Brake pads Brake shoes Brake calipers Brake disc rotors |

|

|

By Actuation Hydraulics Pneumatic |

|

|

By Vehicle Type Passenger Cars Commercial Vehicle Trucks Buses |

|

|

Regional Scope |

North America - United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Brake System Market Key Players:

- Akebono Brake Industry

- Brembo

- Continental AG

- Robert Bosch GmbH

- Knorr-Bremse AG

- Mando Corporation

- Aisin Seiki

- Advics

- Hitachi Astemo, Ltd.

- Nissin Kogyo

- ZF Friedrichshafen

- Haldex

- Tenneco(Federal-mogul)

Frequently Asked Questions

Asia Pacific will continue to be the largest market for Brake System Market.

High maintenance cost of advanced braking technology, supply chain issues are the challenges of Brake System Market.

The segments covereem Market report ard in the Brake Syste based on type, vehicle type, component, actuation, technology.

The increasing focus on automotive safety, the growing adoption of advanced driver assistance systems (ADAS) and the expansion of automotive repair and service centers are driving the brake system market.

1. Brake System Market: Research Methodology

2. Brake System Market Introduction

2.1. Study Assumption and Market Definition

2.2. Scope of the Study

2.3. Executive Summary

3. Global Brake System Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Offering Segment

3.3.3. End-user Segment

3.3.4. Revenue (2025)

3.3.5. Company Headquarter

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

4. Brake System Market: Dynamics

4.1. Brake System Market Trends

4.2. Brake System Market Dynamics

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.2.4. Challenges

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

4.5. Value Chain Analysis

4.6. Regulatory Landscape by Region

4.6.1. North America

4.6.2. Europe

4.6.3. Asia Pacific

4.6.4. Middle East and Africa

4.6.5. South America

5. Brake System Market: Global Market Size and Forecast (Value in USD Billion) (2026-2034)

5.1. Brake System Market Size and Forecast, By type (2026-2034)

5.1.1. Disc Brake

5.1.2. Drum Brake

5.2. Brake System Market Size and Forecast, By Technology(2026-2034)

5.2.1. Anti-lock braking system

5.2.2. Electronic stability control

5.2.3. Traction control system

5.2.4. Electronic brakeforce distribution

5.2.5. Automatic emergency braking

5.3. Brake System Market Size and Forecast, By Component (2026-2034)

5.3.1. Master cylinders

5.3.2. Brake pads

5.3.3. Brake shoes

5.3.4. Brake calipers

5.3.5. Brake disc rotors

5.4. Brake System Market Size and Forecast, By Actuation (2026-2034)

5.4.1. Hydraulics

5.4.2. Pneumatic

5.5. Brake System Market Size and Forecast, By Vehicle Type (2026-2034)

5.5.1. Passenger Cars

5.5.2. Commercial Vehicle

5.5.3. Trucks

5.5.4. Buses

5.6. Brake System Market Size and Forecast, by Region (2026-2034)

5.6.1. North America

5.6.2. Europe

5.6.3. Asia Pacific

5.6.4. Middle East and Africa

5.6.5. South America

6. North America Brake System Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2034)

6.1. North America Brake System Market Size and Forecast, By type (2026-2034)

6.1.1. Disc Brake

6.1.2. Drum Brake

6.2. North America Brake System Market Size and Forecast, By Technology(2026-2034)

6.2.1. Anti-lock braking system

6.2.2. Electronic stability control

6.2.3. Traction control system

6.2.4. Electronic brakeforce distribution

6.2.5. Automatic emergency braking

6.3. North America Brake System Market Size and Forecast, By Component (2026-2034)

6.3.1. Master cylinders

6.3.2. Brake pads

6.3.3. Brake shoes

6.3.4. Brake calipers

6.3.5. Brake disc rotors

6.4. North Brake System Market Size and Forecast, By Actuation (2026-2034)

6.4.1. Hydraulics

6.4.2. Pneumatic

6.5. North Brake System Market Size and Forecast, By Vehicle Type (2026-2034)

6.5.1. Passenger Cars

6.5.2. Commercial Vehicle

6.5.3. Trucks

6.5.4. Buses

6.6. North America Brake System Market Size and Forecast, by Country (2026-2034)

6.6.1. United States

6.6.2. Canada

6.6.3. Mexico

7. Europe Brake System Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2034)

7.1. Europe Brake System Market Size and Forecast, By type (2026-2034)

7.2. Europe Brake System Market Size and Forecast, By Technology(2026-2034)

7.3. Europe Brake System Market Size and Forecast, By Component (2026-2034)

7.4. Europe Brake System Market Size and Forecast, By Actuation (2026-2034)

7.5. Europe Brake System Market Size and Forecast, By Vehicle Type (2026-2034)

7.6. Europe Brake System Market Size and Forecast, By Industry Type(2026-2034)

7.7. Europe Brake System Market Size and Forecast, by Country (2026-2034)

7.7.1. United Kingdom

7.7.2. France

7.7.3. Germany

7.7.4. Italy

7.7.5. Spain

7.7.6. Sweden

7.7.7. Russia

7.7.8. Rest of Europe

8. Asia Pacific Brake System Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2034)

8.1. Asia Pacific Brake System Market Size and Forecast, By type (2026-2034)

8.2. Asia Pacific Brake System Market Size and Forecast, By Technology(2026-2034)

8.3. Asia Pacific Brake System Market Size and Forecast, By Component (2026-2034)

8.4. Asia Pacific Brake System Market Size and Forecast, By Actuation (2026-2034)

8.5. Asia Pacific Brake System Market Size and Forecast, By Vehicle Type (2026-2034)

8.6. Asia Pacific Brake System Market Size and Forecast, By Industry Type (2026-2034)

8.7. Asia Pacific Brake System Market Size and Forecast, by Country (2026-2034)

8.7.1. China

8.7.2. S Korea

8.7.3. Japan

8.7.4. India

8.7.5. Australia

8.7.6. ASEAN

8.7.7. Rest of Asia Pacific

9. Middle East and Africa Brake System Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2034)

9.1. Middle East and Africa Brake System Market Size and Forecast, By type (2026-2034)

9.2. Middle East and Africa Brake System Market Size and Forecast, By Technology(2026-2034)

9.3. Middle East and Africa Brake System Market Size and Forecast, By Component (2026-2034)

9.4. Middle East and Africa Brake System Market Size and Forecast, By Actuation (2026-2034)

9.5. Middle East and Africa Brake System Market Size and Forecast, By Vehicle Type (2026-2034)

9.6. Middle East and Africa Brake System Market Size and Forecast, By Industry Type (2026-2034)

9.7. Middle East and Africa Brake System Market Size and Forecast, by Country (2026-2034)

9.7.1. South Africa

9.7.2. GCC

9.7.3. Nigeria

9.7.4. Rest of ME&A

10. South America Brake System Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2034)

10.1. South America Brake System Market Size and Forecast, By type (2026-2034)

10.2. South America Brake System Market Size and Forecast, By Technology(2026-2034)

10.3. South America Brake System Market Size and Forecast, By Component (2026-2034)

10.4. South America Brake System Market Size and Forecast, By Actuation (2026-2034)

10.5. South America Brake System Market Size and Forecast, By Vehicle Type (2026-2034)

10.6. South America Brake System Market Size and Forecast, By Industry Type (2026-2034)

10.7. South America Brake System Market Size and Forecast, by Country (2026-2034)

10.7.1. Brazil

10.7.2. Argentina

10.7.3. Rest Of South America

11. Company Profile: Key Players

11.1. Akebono Brake Industry

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Brembo

11.3. Continental AG

11.4. Robert Bosch GmbH

11.5. Knorr-Bremse AG

11.6. Mando Corporation

11.7. Aisin Seiki

11.8. Advics

11.9. Hitachi Astemo, Ltd.

11.10. Nissin Kogyo

11.11. ZF Friedrichshafen

11.12. Haldex

11.13. Tenneco(Federal-mogul)

12. Key Findings

13. Industry Recommendations