Additive Manufacturing Market Industry Overview, Size, Share, Growth Trends, Research Insights and Forecast 2026–2034

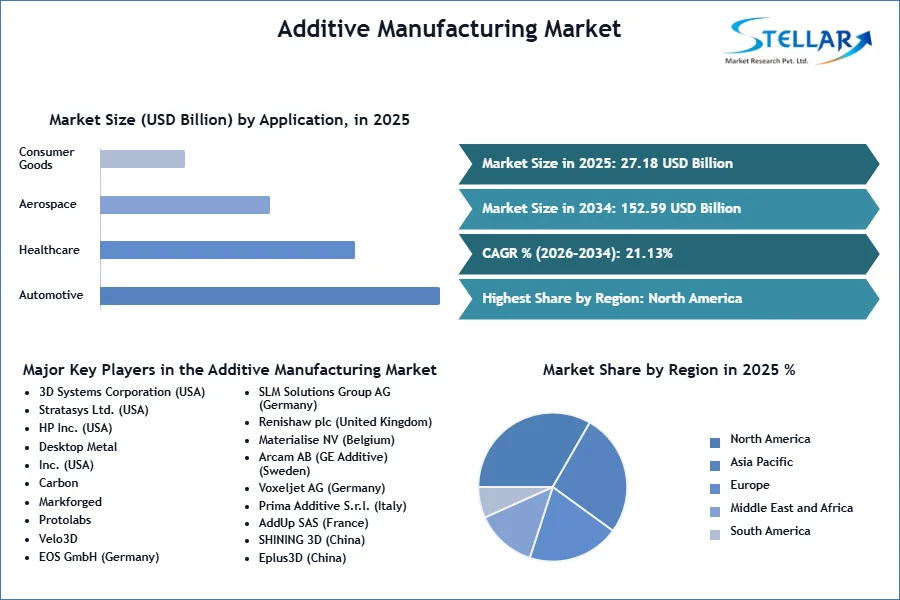

Additive Manufacturing Market was valued at USD 27.18 Billion in 2025. The Total Additive Manufacturing Market revenue is expected to grow by CAGR 21.13% from 2026 to 2034 and reach nearly USD 152.59 Billion in 2034.

Additive Manufacturing Market Overview:

Additive manufacturing is a process of making items by adding material layer by layer to digital 3D model. It uses Technology s such as FDM, SLM, or SLA and supports materials such as polymers, metals and composites. Additive manufacturing enables complex designs, reduces waste, and is widely used for aerospace, automotive and medical industries for rapid prototypes and custom parts.

Additive manufacturing market Aerospace, healthcare, automotive and consumer electronics sectors in the market are feeling significant growth, motivated to increase the growth in the market. The demand for complex, light and optimized components has intensified the change towards 3D printing technologies. Metal 3D printing, bioprinting, and progression in multi-content manufacturing is re-shaping production processes and reducing the market from time to time. integration of AI-operated software and digital twins increases proto typening and design adaptation, increasing operating efficiency. Governments and private players are investing in R&D and standardization to expand the additive manufacturing applications.

Trade and tariffs significantly influence the additive manufacturing market. Tariffs on raw materials like metal powders or specialized polymers increase Material Typicon costs, impacting pricing and competitiveness. Restrictions on imports/exports of additive manufacturing machinery or parts may hinder global supply chains and slow technology adoption, particularly in developing regions. Conversely, favorable trade agreements and tariff exemptions increase cross-border collaboration and investment. geopolitical tensions or sanctions may restrict access to advanced equipment and intellectual property, affecting innovation and global additive manufacturing market expansion. trade and tariff dynamics directly shape the growth, cost-efficiency, and global accessibility of additive manufacturing technologies.

To get more Insights: Request Free Sample Report

Additive Manufacturing Market Dynamics:

Technological Advancements to boost Additive Manufacturing Market Growth

Additive manufacturing (AM) technological progress in market development is a major driver. Constant innovations in material science, printing speed, multi-coating abilities, and precision have expanded Additive manufacturing applications in aerospace, healthcare, automotive and consumer electronics. Increased software integration with AI and simulation tools allows better design optimization and prototyping cycles to reduce.

Development such as metal 3D printing, bio-printing and large-form Additive manufacturing systems are enabling more complex and high-performance parts. These innovations are reducing Material Typeion costs, improving Material Type adaptation, and expedited from time to time, making the next generation an important environment of manufacturing.

Lightweight Components in Aerospace & Automotive to Create lucrative Opportunity for Additive Manufacturing Market Growth

Additive Manufacturing (AM) market plays an important role in the Material Typeion of mild, high -power components for aerospace and automotive sectors. Traditional manufacturing technology often limits design independence, leading to more engineer parts that add unnecessary weight. The additive manufacturing overcomes it by allowing the construction of complex geometric and forged structures that maintain structural integrity by reducing mass. In aerospace, lighter parts directly improve fuel efficiency, reduce emissions and contribute to extended flight boundaries. Similarly, in the motor vehicle industry, weight loss increases vehicle performance, fuel economy and regulatory emission standards.

Advanced materials such as titanium, aluminum mixture, and high-demonstration polymers further increase the strength-to-vision ratio. By integrating their supply chains to additive manufacturing, manufacturers rapid prototypes, test, and produce customized components, run innovation and cost savings. This change towards lightweight via additive manufacturing is important to meet the goals of stability and competitive performance benchmarks in high-rally, accurate-managed industries.

Material Gap in 3D Printing to Restrain the Additive Manufacturing Market growth

Limited material availability remains a key restraint in the additive manufacturing market. Although the range of printable materials is expanding, it still lags behind traditional manufacturing. Industries such as aerospace, automotive, and healthcare require materials with strict specifications, including high tensile strength, thermal resistance, chemical stability, and biocompatibility. many AM-compatible materials do not consistently meet these criteria, particularly under demanding operating conditions. This limits the use of AM for critical components. the development of new printable materials is expensive and time-consuming, which further delays widespread adoption of additive manufacturing in high-performance and regulated industry applications.

Additive Manufacturing Market Segmentation:

By Material Type, the additive manufacturing market is segmented into metal, plastic, alloys, and ceramics. The Metal segment dominated the market in 2025and is expected to hold the largest Additive Manufacturing Market share during the forecast period. Its increasing application in high demand industries such as aerospace, automotive and healthcare. Metals such as titanium, aluminium and stainless steel offer exceptional power, durability and heat resistance required for important components such as engine parts and medical transplants. Advance in metal 3D printing technologies, including selective laser melting and electron beam melting, have enhanced the excellence of Material Typicon and the value of the part, encouraging comprehensive adoption. Metals dominate because they meet the demand for industrial manufacturing mechanical and thermal requirements, which results in significant additive manufacturing market growt

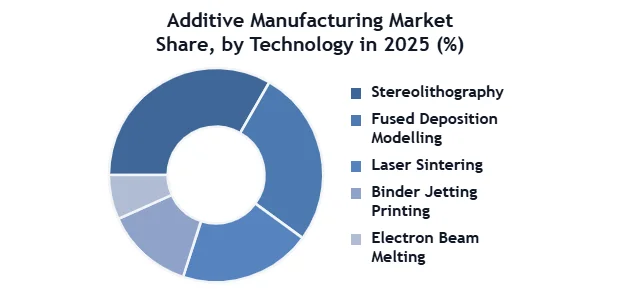

By Technology, the additive manufacturing market segmented into Stereolithography, Fused Deposition Modelling, Laser Sintering, Binder Jetting Printing, Electron Beam Melting and Others. Fused Deposition Modelling segment dominated the market in 2025and is expected to hold the largest Additive Manufacturing Market share during the forecast period. Cost-effectiveness, ease of use, and comprehensive material compatibility, especially with thermoplastic. It is widely adopted in industries from prototypes in consumer goods to motor vehicle and functional parts in industrial manufacturing. FDM printers are available in both desktop and industrial forms, making technology equally accessible to startups, educational institutions and large-scale manufacturers. the print resolution, continuous improvement in the power of speed and material have increased its versatility. While Technology s such as SLM and EBM are important for metal applications, FDM is most widely used due to its ability, scalability and comprehensive application base.

By Application, the additive manufacturing market segmented into Automotive, Healthcare, Aerospace, Consumer Goods, Architecture, and Others. The aerospace segment dominated the market in 2025and is expected to hold the largest market share during the forecast period. The industry's demand for lightweight, high strength, and complex components that reduce fuel consumption and progress performance. Additive manufacturing market enables the Material typicon of intricate parts with minimal material waste, making it ideal for aerospace applications such as engine components, air ducts, brackets, and structural elements. The sector also profits from the use of advanced metal 3D printing technologies like Selective Laser Melting and Electron Beam Melting, which meet strict aerospace quality and safety standards. the essential for rapid prototyping and portion consolidation supports additive manufacturing adoption. While automotive and healthcare are strong growth areas, aerospace leads in terms of price contribution and technological integration, especially for mission critical, custom, and low volume parts.

By Region, North America dominated the additive manufacturing Market in 2025 and is expected to hold largest share during the forecast period. This leadership is driven by a robust industrial base, particularly in aerospace, defence, and automotive areas, which profoundly invest in additive manufacturing for lightweight, high presentation components. The region also profits from a strong R&D ecosystem and important government support through initiatives like the U.S. Department of Défense’s additive manufacturing forward program, promoting advanced manufacturing adoption. the presence of key players such as Stratasys, 3D Systems, and Desktop Metal accelerates modernization and commercialization. With continued savings in technological advancement, North America remains the maximum mature and revenue generating region in the global additive manufacturing market.

Additive Manufacturing Market Competitive Landscape

The 3D System Corporation and Stratasys Ltd. Limited are two prominent players in the additive manufacturing market. The 3D system, is known for pioneering stereolithography (SLA) and focuses heavy on healthcare, aerospace and dental applications, offering metal and polymer 3D printers with software such as 3DXPTs. The USA and Israel leads in stratasys, FDMs and polygette technologies with dual headquarters and operates industries such as aerospace, education and motor vehicles. It has expanded through acquisitions such as original and co-stro additive manufacturing to increase Material Typicon capabilities. While the 3D system is stronger in medical and metal AM, Stratasys excel in multi-coal prototypes and industrial solutions. Both invest heavy in R&D and stability, but face growing competition from new entrances such as HP and desktop metals.

Additive Manufacturing Market Key Development

In 5 March 2025, the 3D System Corporation (USA) launched the NextDent LCD 1, a compact dental 3D printer for small dental labs and clinics. The launch marked a strategic expansion of its digital dental portfolio, which provides high precision, in-house printing solutions. Development reinforces the leadership of the 3D system in North America's Dental Additive Manufacturing sector by addressing the increasing demand for accessible and skilled dental 3D printing technology.

In 4 October 2024, Markforged (USA) launched the FX10, an advanced industrial composite 3D printer designed for producing high-strength, end use parts. Specifically engineered for demanding applications, the FX10 targets sectors like aerospace and defence in North America, offering improved speed, reliability, and material performance.

In June 2024, GE Additive (USA) opened a Customer Experience Centre in Cincinnati, Ohio to provide DfAM consulting and training. The centre supports U.S. manufacturers in adopting additive manufacturing technologies more effectively.

|

Additive Manufacturing Market Scope |

|

|

Market Size in 2025 |

USD 27.18 Bn. |

|

Market Size in 2034 |

USD 152.59 Bn. |

|

CAGR (2026-2034) |

21.13% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

by Material Type Metal Plastics Alloy Ceramics |

|

by Technology Stereolithography Fused Deposition Modelling Laser Sintering Binder Jetting Printing Electron Beam Melting Others |

|

|

by Application Automotive Healthcare Aerospace Consumer Goods Architecture Others |

|

|

Regional Scope |

North America- US, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key players in the Additive Manufacturing Market

North America

- 3D Systems Corporation (USA)

- Stratasys Ltd. (USA)

- HP Inc. (USA)

- Desktop Metal, Inc. (USA)

- Carbon, Inc. (USA)

- Markforged, Inc. (USA)

- Protolabs, Inc. (USA)

- Velo3D, Inc. (USA)

Europe

- EOS GmbH (Germany)

- SLM Solutions Group AG (Germany)

- Renishaw plc (United Kingdom)

- Materialise NV (Belgium)

- Arcam AB (GE Additive) (Sweden)

- Voxeljet AG (Germany)

- Prima Additive S.r.l. (Italy)

- AddUp SAS (France)

Asia-Pacific

- Farsoon Technologies (China)

- SHINING 3D (China)

- Eplus3D (China)

- XYZprinting, Inc. (Taiwan)

- Ricoh Company, Ltd. (Japan)

- DMG Mori Co., Ltd. (Japan)

- Matsuura Machinery Corporation (Japan)

- Aurora Labs Limited (Australia)

South America

- Cliever Technologic (Brazil)

- Alkimat Tecnologia (Brazil)

Middle East & Africa

- Immensa Technology Labs (United Arab Emirates)

- RAPDASA (via Aeroswift Project) (South Africa)

- Build Volume (South Africa)

- 3D Prototipagem (Brazil)

Frequently Asked Questions

Trade restrictions and tariffs raise costs and disrupt supply chains, while favourable agreements boost growth.

Companies use DRM, blockchain, and secure file transfer to protect IP.

Aerospace leads due to its need for lightweight, high-strength, complex parts.

3D Systems Corporation and Stratasys Ltd. are key leaders.

1. Additive Manufacturing Market Introduction

1.1. Study Assumption and Market Definition

1.2. Scope of the Study

1.3. Executive Summary

2. Additive Manufacturing Market: Competitive Landscape

2.1. Ecosystem Analysis

2.2. SMR Competition Matrix

2.3. Competitive Landscape

2.4. Key Players Benchmarking

2.4.1. Company Name

2.4.2. Business Segment

2.4.3. End-user Segment

2.4.4. Revenue (2025)

2.4.5. Company Locations

2.5. Market Structure

2.5.1. Market Leaders

2.5.2. Market Followers

2.5.3. Emerging Players

2.6. Mergers and Acquisitions Details

3. Additive Manufacturing Market: Dynamics

3.1. Additive Manufacturing Market Trends by Region

3.1.1. North America Additive Manufacturing Market Trends

3.1.2. Europe Additive Manufacturing Market Trends

3.1.3. Asia Pacific Additive Manufacturing Market Trends

3.1.4. Middle East and Africa Additive Manufacturing Market Trends

3.1.5. South America Additive Manufacturing Market Trends

3.2. Additive Manufacturing Market Dynamics

3.2.1. Global Additive Manufacturing Market Drivers

3.2.2. Global Additive Manufacturing Market Restraints

3.2.3. Global Additive Manufacturing Market Opportunities

3.2.4. Global Additive Manufacturing Market Challenges

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

3.5. Regulatory Landscape by Region

3.5.1. North America

3.5.2. Europe

3.5.3. Asia Pacific

3.5.4. Middle East and Africa

3.5.5. South America

3.6. Key Opinion Leader Analysis for Additive Manufacturing Industry

4. Additive Manufacturing Market: Global Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

4.1. Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

4.1.1. Metal

4.1.2. Plastics

4.1.3. Alloy

4.1.4. Ceramic

4.2. Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

4.2.1. Stereolithography

4.2.2. Fused Deposition Modelling

4.2.3. Laser Sintering

4.2.4. Binder Jetting Printing

4.2.5. Electron beam melting

4.2.6. others

4.3. Additive Manufacturing Market Size and Forecast, By Application (2026-2034)

4.3.1. Automotive

4.3.2. Healthcare

4.3.3. Aerospace

4.3.4. Consumer Goods

4.3.5. Architecture

4.3.6. Others

4.4. Additive Manufacturing Market Size and Forecast, by Region (2026-2034)

4.4.1. North America

4.4.2. Europe

4.4.3. Asia Pacific

4.4.4. Middle East and Africa

4.4.5. South America

5. North America Additive Manufacturing Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

5.1. North America Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

5.1.1. Metal

5.1.2. Plastics

5.1.3. Alloy

5.1.4. Ceramic

5.2. North America Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

5.2.1. Stereolithography

5.2.2. Fused Deposition Modelling

5.2.3. Laser Sintering

5.2.4. Binder Jetting Printing

5.2.5. Electron beam melting

5.2.6. others

5.3. North America Additive Manufacturing Market Size and Forecast, By Application (2026-2034)

5.3.1. Automotive

5.3.2. Healthcare

5.3.3. Aerospace

5.3.4. Consumer goods

5.3.5. Architecture

5.3.6. Others

5.4. North America Additive Manufacturing Market Size and Forecast, by Country (2026-2034)

5.4.1. United States

5.4.1.1. United States Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

5.4.1.1.1. Metal

5.4.1.1.2. Plastics

5.4.1.1.3. Alloy

5.4.1.1.4. Ceramic

5.4.1.2. United States Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

5.4.1.2.1. Stereolithography

5.4.1.2.2. Fused deposition modelling

5.4.1.2.3. Laser sintering

5.4.1.2.4. Binder jetting printing

5.4.1.2.5. Electron beam melting

5.4.1.2.6. others

5.4.1.3. United States Additive Manufacturing Market Size and Forecast, By Application (2026-2034)

5.4.1.3.1. Automotive

5.4.1.3.2. Healthcare

5.4.1.3.3. Aerospace

5.4.1.3.4. Consumer goods

5.4.1.3.5. Architecture

5.4.1.3.6. Others

5.4.2. Canada

5.4.2.1. Canada Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

5.4.2.1.1. Metal

5.4.2.1.2. Plastics

5.4.2.1.3. Alloy

5.4.2.1.4. Ceramic

5.4.2.2. Canada Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

5.4.2.2.1. Stereolithography

5.4.2.2.2. Fused deposition modelling

5.4.2.2.3. Laser sintering

5.4.2.2.4. Binder jetting printing

5.4.2.2.5. Electron beam melting

5.4.2.2.6. others

5.4.2.3. Canada Additive Manufacturing Market Size and Forecast, By Application (2026-2034)

5.4.2.3.1. Automotive

5.4.2.3.2. Healthcare

5.4.2.3.3. Aerospace

5.4.2.3.4. Consumer goods

5.4.2.3.5. Architecture

5.4.2.3.6. Others

5.4.2.4. Mexico Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

5.4.2.4.1. Metal

5.4.2.4.2. Plastics

5.4.2.4.3. Alloy

5.4.2.4.4. Ceramic

5.4.2.5. Mexico Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

5.4.2.5.1. Stereolithography

5.4.2.5.2. Fused deposition modelling

5.4.2.5.3. Laser sintering

5.4.2.5.4. Binder jetting printing

5.4.2.5.5. Electron beam melting

5.4.2.5.6. others

5.4.2.6. Mexico Additive Manufacturing Market Size and Forecast, By Application (2026-2034)

5.4.2.6.1. Automotive

5.4.2.6.2. Healthcare

5.4.2.6.3. Aerospace

5.4.2.6.4. Consumer goods

5.4.2.6.5. Architecture

5.4.2.6.6. Others

6. Europe Additive Manufacturing Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

6.1. Europe Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

6.2. Europe Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

6.3. Europe Additive Manufacturing Market Size and Forecast, Application (2026-2034)

6.4. Europe Additive Manufacturing Market Size and Forecast, by Country (2026-2034)

6.4.1. United Kingdom

6.4.1.1. United Kingdom Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

6.4.1.2. United Kingdom Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

6.4.1.3. United Kingdom Additive Manufacturing Market Size and Forecast, Application (2026-2034)

6.4.2. France

6.4.2.1. France Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

6.4.2.2. France Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

6.4.2.3. France Additive Manufacturing Market Size and Forecast, Application (2026-2034)

6.4.3. Germany

6.4.3.1. Germany Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

6.4.3.2. Germany Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

6.4.3.3. Germany Additive Manufacturing Market Size and Forecast, Application (2026-2034)

6.4.4. Italy

6.4.4.1. Italy Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

6.4.4.2. Italy Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

6.4.4.3. Italy Additive Manufacturing Market Size and Forecast, Application (2026-2034)

6.4.5. Spain

6.4.5.1. Spain Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

6.4.5.2. Spain Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

6.4.5.3. Spain Additive Manufacturing Market Size and Forecast, Application (2026-2034)

6.4.6. Sweden

6.4.6.1. Sweden Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

6.4.6.2. Sweden Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

6.4.6.3. Sweden Additive Manufacturing Market Size and Forecast, Application (2026-2034)

6.4.7. Austria

6.4.7.1. Austria Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

6.4.7.2. Austria Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

6.4.7.3. Austria Additive Manufacturing Market Size and Forecast, Application (2026-2034)

6.4.8. Rest of Europe

6.4.8.1. Rest of Europe Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

6.4.8.2. Rest of Europe Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

6.4.8.3. Rest of Europe Additive Manufacturing Market Size and Forecast, Application (2026-2034)

7. Asia Pacific Additive Manufacturing Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

7.1. Asia Pacific Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

7.2. Asia Pacific Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

7.3. Asia Pacific Additive Manufacturing Market Size and Forecast, Application (2026-2034)

7.4. Asia Pacific Additive Manufacturing Market Size and Forecast, by Country (2026-2034)

7.4.1. China

7.4.1.1. China Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

7.4.1.2. China Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

7.4.1.3. China Additive Manufacturing Market Size and Forecast, Application (2026-2034)

7.4.2. S Korea

7.4.2.1. S Korea Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

7.4.2.2. S Korea Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

7.4.2.3. S Korea Additive Manufacturing Market Size and Forecast, Application (2026-2034)

7.4.3. Japan

7.4.3.1. Japan Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

7.4.3.2. Japan Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

7.4.3.3. Japan Additive Manufacturing Market Size and Forecast, Application (2026-2034)

7.4.4. India

7.4.4.1. India Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

7.4.4.2. India Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

7.4.4.3. India Additive Manufacturing Market Size and Forecast, Application (2026-2034)

7.4.5. Australia

7.4.5.1. Australia Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

7.4.5.2. Australia Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

7.4.5.3. Australia Additive Manufacturing Market Size and Forecast, Application (2026-2034)

7.4.6. Indonesia

7.4.6.1. Indonesia Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

7.4.6.2. Indonesia Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

7.4.6.3. Indonesia Additive Manufacturing Market Size and Forecast, Application (2026-2034)

7.4.7. Philippines

7.4.7.1. Philippines Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

7.4.7.2. Philippines Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

7.4.7.3. Philippines Additive Manufacturing Market Size and Forecast, Application (2026-2034)

7.4.8. Malaysia

7.4.8.1. Malaysia Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

7.4.8.2. Malaysia Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

7.4.8.3. Malaysia Additive Manufacturing Market Size and Forecast, Application (2026-2034)

7.4.9. Vietnam

7.4.9.1. Vietnam Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

7.4.9.2. Vietnam Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

7.4.9.3. Vietnam Additive Manufacturing Market Size and Forecast, Application (2026-2034)

7.4.10. Thailand

7.4.10.1. Thailand Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

7.4.10.2. Thailand Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

7.4.10.3. Thailand Additive Manufacturing Market Size and Forecast, Application (2026-2034)

7.4.11. Rest of Asia Pacific

7.4.11.1. Rest of Asia Pacific Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

7.4.11.2. Rest of Asia Pacific Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

7.4.11.3. Rest of Asia Pacific Additive Manufacturing Market Size and Forecast, Application (2026-2034)

8. Middle East and Africa Additive Manufacturing Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

8.1. Middle East and Africa Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

8.2. Middle East and Africa Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

8.3. Middle East and Africa Additive Manufacturing Market Size and Forecast, Application (2026-2034)

8.4. Middle East and Africa Additive Manufacturing Market Size and Forecast, by Country (2026-2034)

8.4.1. South Africa

8.4.1.1. South Africa Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

8.4.1.2. South Africa Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

8.4.1.3. South Africa Additive Manufacturing Market Size and Forecast, Application (2026-2034)

8.4.2. GCC

8.4.2.1. GCC Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

8.4.2.2. GCC Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

8.4.2.3. GCC Additive Manufacturing Market Size and Forecast, Application (2026-2034)

8.4.3. Nigeria

8.4.3.1. Nigeria Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

8.4.3.2. Nigeria Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

8.4.3.3. Nigeria Additive Manufacturing Market Size and Forecast, Application (2026-2034)

8.4.4. Rest of ME&A

8.4.4.1. Rest of ME&A Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

8.4.4.2. Rest of ME&A Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

8.4.4.3. Rest of ME&A Additive Manufacturing Market Size and Forecast, Application (2026-2034)

9. South America Additive Manufacturing Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

9.1. South America Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

9.2. South America Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

9.3. South America Additive Manufacturing Market Size and Forecast, Application (2026-2034)

9.4. South America Additive Manufacturing Market Size and Forecast, by Country (2026-2034)

9.4.1. Brazil

9.4.1.1. Brazil Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

9.4.1.2. Brazil Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

9.4.1.3. Brazil Additive Manufacturing Market Size and Forecast, Application (2026-2034)

9.4.2. Argentina

9.4.2.1. Argentina Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

9.4.2.2. Argentina Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

9.4.2.3. Argentina Additive Manufacturing Market Size and Forecast, Application (2026-2034)

9.4.3. Rest of South America

9.4.3.1. Rest of South America Additive Manufacturing Market Size and Forecast, By Material Type (2026-2034)

9.4.3.2. Rest of South America Additive Manufacturing Market Size and Forecast, By Technology (2026-2034)

9.4.3.3. Rest of South America Additive Manufacturing Market Size and Forecast, Application (2026-2034)

10. Company Profile: Key Players

10.1. 3D Systems Corporation

10.1.1. Company Overview

10.1.2. Business Portfolio

10.1.3. Financial Overview

10.1.4. SWOT Analysis

10.1.5. Strategic Analysis

10.1.6. Recent Developments

10.2. 3D Systems Corporation

10.3. Stratasys Ltd.

10.4. HP Inc.

10.5. Desktop Metal, Inc.

10.6. Carbon, Inc.

10.7. Markforged, Inc.

10.8. Protolabs, Inc.

10.9. Velo3D, Inc.

10.10. EOS GmbH

10.11. SLM Solutions Group AG

10.12. Renishaw plc

10.13. Materialise NV

10.14. Arcam AB (GE Additive)

10.15. Voxeljet AG

10.16. Prima Additive S.r.l.

10.17. AddUp SAS

10.18. Farsoon Technologies

10.19. SHINING 3D

10.20. Eplus3D

10.21. XYZprinting, Inc.

10.22. Ricoh Company, Ltd.

10.23. DMG Mori Co., Ltd.

10.24. Matsuura Machinery Corporation

10.25. Aurora Labs Limited

10.26. Cliever Tecnologia

10.27. Alkimat Tecnologia

10.28. Immensa Technology Labs

10.29. RAPDASA (via Aeroswift Project)

10.30. BuildVolume

10.31. 3D Prototipagem

11. Key Findings

12. Analyst Recommendations

13. Additive Manufacturing Market: Research Methodology