Vitamin K Market Global Industry Analysis and Forecast (2026-2032)

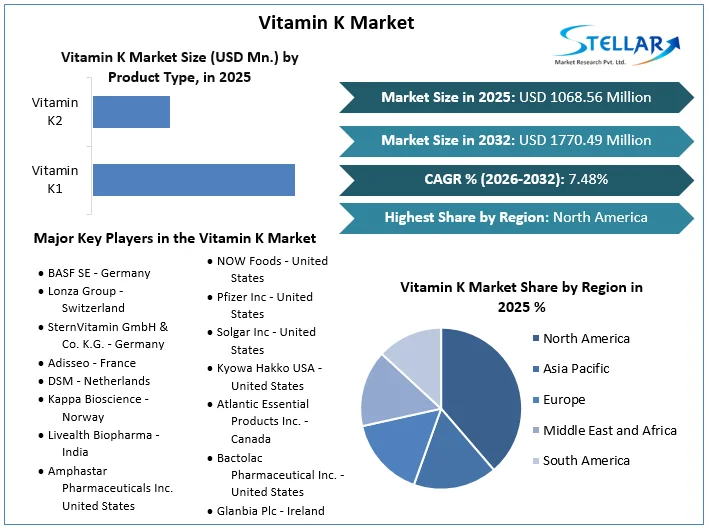

The Vitamin K Market size was valued at USD 1068.56 Mn. in 2025 and the total Vitamin K Market size is expected to grow at a CAGR of 7.48% from 2026 to 2032, reaching nearly USD 1770.49 Mn. by 2032.

Vitamin K Market Overview

The Vitamin K market is a global industry that produces, distributes, and consumes vitamin K products, which are essential for blood clotting, bone health, and cardiovascular health. Vitamin K is found in two forms phytonadione found in green leafy vegetables and plant-based foods, and menaquinone found in animal-based foods and gut bacteria. It is commonly used for treating vitamin K deficiency, reversing warfarin's blood-thinning effects, and supporting bone health. The market includes dietary supplements, fortified foods, pharmaceutical formulations, and medical applications. The growing awareness of Vitamin K's importance in maintaining bone health is expected to drive market growth.

The increasing prevalence of chronic diseases like osteoporosis, blood coagulation, arthritis, diabetes, cardiovascular disease, and skin-related diseases is expected to drive market growth size. Consumption of Vitamin K in sufficient amounts helps prevent several diseases. The geriatric population and the trend of preventive healthcare are projected to create significant growth opportunities for the Vitamin K market.

To get more Insights: Request Free Sample Report

Vitamin K Market Dynamics:

The vitamin K market is expected to grow because of the increasing prevalence of chronic disorders, such as hemorrhagic disease in newborns, neonatal bleeding, osteoporosis, arthritis, diabetes, and cardiovascular disease. Infants and newborns are more susceptible to vitamin K deficiencies, leading to increased demand for vitamin K tablets, supplements, or injections. Consumer awareness about the importance of vitamins and minerals, such as Vitamin K, is increasing, leading to heightened demand for products containing Vitamin K. Awareness campaigns and media coverage highlighting the role of Vitamin K in preventing bone fractures and cardiovascular issues contribute to market growth.

The global Vitamin K market is growing because of increased awareness of its health benefits, especially in bone and cardiovascular health. Consumer demand for dietary supplements and functional foods enriched with Vitamin K is expected to continue. Innovations in product formulations and growing applications in cosmetics and pharmaceuticals contribute to market growth.

Government frameworks mandate the fortification of food products with essential nutrients, including Vitamin K. Compliance with these morals improves consumer confidence in fortified foods and creates a constant demand for Vitamin K among food producers. This trend towards proactive health management is raising market growth and a shift towards proactive health management among consumers.

North America is experiencing prominent developments in regulations and consumer preferences towards Vitamin K-enriched products, with a growing trend towards natural and organic sources. Research on Vitamin K's role in immune support and aging-related conditions is also driving interest in the market.

The vitamin K market faces several challenges, such as low consumer awareness about its importance for overall health, varying regulatory environments across industries, the high cost of extracting and packing vitamin K formulations, and its health benefits Ongoing scientific research on the topic and resulting competition other micronutrient supplements and foods complicate market positioning and consumer education efforts. Concerted efforts in research, education, regulation, and market growth strategies are essential to unlock the full potential of the vitamin K market. The regulatory framework varies from region to region, and ongoing scientific research into the role of vitamin K2 in heart health and bone metabolism affects consumer confidence and market acceptance.

The Vitamin K market presents several promising opportunities for growth and development. First, demand increases among consumers as awareness of the health benefits of vitamin K, especially vitamin K2, increases. Research is producing this trend that shows its role in bone health, cardiovascular health, and other potential areas such as cognitive function. Advances in technology and manufacturing processes increase the efficiency and scalability of the production processes for vitamin K and fortified foods thereby reducing costs and expanding the market, especially in areas where food shortages are common.

Regulatory support for dietary supplements and enforcement programs in different countries promote market growth opportunities. Governments and health organizations recognize the importance of vitamin K and other micronutrients in public health, resulting in variable policies and guidelines Also, partnerships and collaborations among key players in the pharmaceutical, nutraceutical, and food industries support innovation and product development, leading to the development of new formulations and delivery methods to cater to diverse customers which they want to address. All these factors contribute to the promising outlook of the Vitamin K market globally.

Vitamin K Market Segment Analysis:

Based on Application, the osteoporosis segment dominated the vitamin K market, as it plays a crucial role in bone metabolism and mineralization, reducing fracture risk. This condition is primarily affecting older adults, particularly postmenopausal women and elderly individuals, who are at higher risk of bone-related complications. As the global population ages, the prevalence of osteoporosis is expected to rise, driving demand for interventions supporting bone health, including vitamin K supplements.

The dermal application segment also held a significant share of the vitamin K market, with numerous skin applications including resolving bruising, suppressing pigmentation, limiting acneiform side effects, and aiding in wound healing. Vitamin K is non-irritating and safe for all skin types, and it improves wound healing by increasing contraction and assisting in collagen and blood vessel formation. Its redox properties allow the skin to detoxify reactive oxygen species formed from exposure to UV rays and pollution.

Vitamin K Market Regional Insight:

North American vitamin K market, which dominated the market in 2025, driven by factors such as prominent manufacturers, a growing geriatric population, awareness of nutritional benefits, investment in research, demand for injectables, and the prevalence of chronic disorders like neonatal bleeding, arthritis, cancer, diabetes, vascular calcification, and osteoporosis. The region's established market of dietary supplements and fortified foods is also fueled by high healthcare expenditure and individuals willing to invest in preventive measures. The rising frequency of vitamin K-related disorders, such as newborn hemorrhage, osteoporosis, and vascular calcification, is positively impacting the industry's growth. Sedentary lifestyles, poor dietary habits, and lack of exercise are activating risk factors associated with these diseases, further boosting regional growth.

- The U.S. market is experiencing significant growth because of increasing demand for nutritional products, advanced healthcare infrastructure, wellness focus, vitamin K-related disorders, and innovative product development.

Vitamin K Market Competitive Landscape:

- 24 Jun 2024, dsm-firmenich, the leading innovator in health, nutrition, and beauty has recently launched a shrimp module for Sustell™, allowing shrimp farmers to map, reduce the full environmental footprint of their operations and meet environmental sustainability targets.

- In 2024, Lonza is closing manufacturing facilities in Guangzhou, China, and Hayward, California. The closures are begin in Q1 2024 and be completed by early 2025. The company reported an impairment loss of $2.12 million combined with $58 million in restructuring costs.

|

Vitamin K Market Scope |

|

|

Market Size in 2025 |

USD 1068.56 Mn. |

|

Market Size in 2032 |

USD 1770.49 Mn. |

|

CAGR (2026-2032) |

7.48 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Product Type Vitamin K1 Vitamin K2 |

|

By Route of Administration Oral Topical Parenteral |

|

|

By Application Osteoporosis Vitamin K Dependent Clotting Factor Deficiency (VKCFD) Prothrombin deficiency Vitamin K Deficiency Bleeding (VKDB) Dermal Application Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Vitamin K Market

- BASF SE - Germany

- Lonza Group - Switzerland

- SternVitamin GmbH & Co. K.G. - Germany

- Adisseo - France

- DSM - Netherlands

- Kappa Bioscience - Norway

- Livealth Biopharma - India

- Amphastar Pharmaceuticals Inc. - United States

- NOW Foods - United States

- Pfizer Inc - United States

- Solgar Inc - United States

- Kyowa Hakko USA - United States

- Atlantic Essential Products Inc. - Canada

- Bactolac Pharmaceutical Inc. - United States

- Glanbia Plc - Ireland

- ADM (Archer Daniels Midland) - United States

- Farbest Brands - United States

- BTSA Biotechnologias Aplicadas S.L. - Spain

- Rabar Pty Ltd - Australia

- Viridis BioPharma - United States

Frequently Asked Questions

North America is expected to lead the Vitamin K Market during the forecast period.

An analysis of profit trends and projections for companies in the Vitamin K Market is included, offering insights into factors driving profitability, cost management strategies, and financial performance metrics.

The Vitamin K Market size was valued at USD 1068.56 Million in 2025 and the total Vitamin K Market size is expected to grow at a CAGR of 7.48% from 2026 to 2032, reaching nearly USD 1770.49 Million by 2032.

The segments covered in the market report are by Product Type, by Route of Administration, and by Application.

1. Vitamin K Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market breakdown and Data Triangulation

1.4. Assumptions

2. Vitamin K Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Vitamin K Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Portfolio

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

4. Vitamin K Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape

4.9.1. Market Regulation by Region

4.9.1.1. North America

4.9.1.2. Europe

4.9.1.3. Asia Pacific

4.9.1.4. Middle East and Africa

4.9.1.5. South America

4.9.2. Impact of Regulations on Market Dynamics

4.9.3. Government Schemes and Initiatives

5. Vitamin K Market Size and Forecast by Segments (by Value USD Million)

5.1. Vitamin K Market Size and Forecast, By Product Type (2025-2032)

5.1.1. Vitamin K1

5.1.2. Vitamin K2

5.2. Vitamin K Market Size and Forecast, By Route of Administration (2025-2032)

5.2.1. Oral

5.2.2. Topical

5.2.3. Parenteral

5.3. Vitamin K Market Size and Forecast, By Application (2025-2032)

5.3.1. Osteoporosis

5.3.2. Vitamin K Dependent Clotting Factor Deficiency (VKCFD)

5.3.3. Prothrombin deficiency

5.3.4. Vitamin K Deficiency Bleeding (VKDB)

5.3.5. Dermal Application

5.3.6. Others

5.4. Vitamin K Market Size and Forecast, by Region (2025-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Vitamin K Market Size and Forecast (by Value USD Million)

6.1. North America Vitamin K Market Size and Forecast, By Product Type (2025-2032)

6.1.1. Vitamin K1

6.1.2. Vitamin K2

6.2. North America Vitamin K Market Size and Forecast, By Route of Administration (2025-2032)

6.2.1. Oral

6.2.2. Topical

6.2.3. Parenteral

6.3. North America Vitamin K Market Size and Forecast, By Application (2025-2032)

6.3.1. Osteoporosis

6.3.2. Vitamin K Dependent Clotting Factor Deficiency (VKCFD)

6.3.3. Prothrombin deficiency

6.3.4. Vitamin K Deficiency Bleeding (VKDB)

6.3.5. Dermal Application

6.3.6. Others

6.4. North America Vitamin K Market Size and Forecast, by Country (2025-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Vitamin K Market Size and Forecast (by Value USD Million)

7.1. Europe Vitamin K Market Size and Forecast, By Product Type (2025-2032)

7.2. Europe Vitamin K Market Size and Forecast, By Route of Administration (2025-2032)

7.3. Europe Vitamin K Market Size and Forecast, By Application (2025-2032)

7.4. Europe Vitamin K Market Size and Forecast, by Country (2025-2032)

7.4.1. UK

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Vitamin K Market Size and Forecast (by Value USD Million)

8.1. Asia Pacific Vitamin K Market Size and Forecast, By Product Type (2025-2032)

8.2. Asia Pacific Vitamin K Market Size and Forecast, By Route of Administration (2025-2032)

8.3. Asia Pacific Vitamin K Market Size and Forecast, By Application (2025-2032)

8.4. Asia Pacific Vitamin K Market Size and Forecast, by Country (2025-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Bangladesh

8.4.11. Pakistan

8.4.12. Rest of Asia Pacific

9. Middle East and Africa Vitamin K Market Size and Forecast (by Value USD Million)

9.1. Middle East and Africa Vitamin K Market Size and Forecast, By Product Type (2025-2032)

9.2. Middle East and Africa Vitamin K Market Size and Forecast, By Route of Administration (2025-2032)

9.3. Middle East and Africa Vitamin K Market Size and Forecast, By Application (2025-2032)

9.4. Middle East and Africa Vitamin K Market Size and Forecast, by Country (2025-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Egypt

9.4.4. Nigeria

9.4.5. Rest of ME&A

10. South America Vitamin K Market Size and Forecast (by Value USD Million)

10.1. South America Vitamin K Market Size and Forecast, By Product Type (2025-2032)

10.2. South America Vitamin K Market Size and Forecast, By Route of Administration (2025-2032)

10.3. South America Vitamin K Market Size and Forecast, By Application (2025-2032)

10.4. South America Vitamin K Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest of South America

11. Company Profile: Key players

11.1. BASF SE - Germany

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Lonza Group - Switzerland

11.3. SternVitamin GmbH & Co. K.G. - Germany

11.4. Adisseo - France

11.5. DSM - Netherlands

11.6. Kappa Bioscience - Norway

11.7. Livealth Biopharma - India

11.8. Amphastar Pharmaceuticals Inc. - United States

11.9. NOW Foods - United States

11.10. Pfizer Inc - United States

11.11. Solgar Inc - United States

11.12. Kyowa Hakko USA - United States

11.13. Atlantic Essential Products Inc. - Canada

11.14. Bactolac Pharmaceutical Inc. - United States

11.15. Glanbia Plc - Ireland

11.16. ADM (Archer Daniels Midland) - United States

11.17. Farbest Brands - United States

11.18. BTSA Biotechnologias Aplicadas S.L. - Spain

11.19. Rabar Pty Ltd - Australia

11.20. Viridis BioPharma - United States

11.21. XX.inc

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook