Vegetable Puree Market - Industry Analysis and Forecast 2026-2034

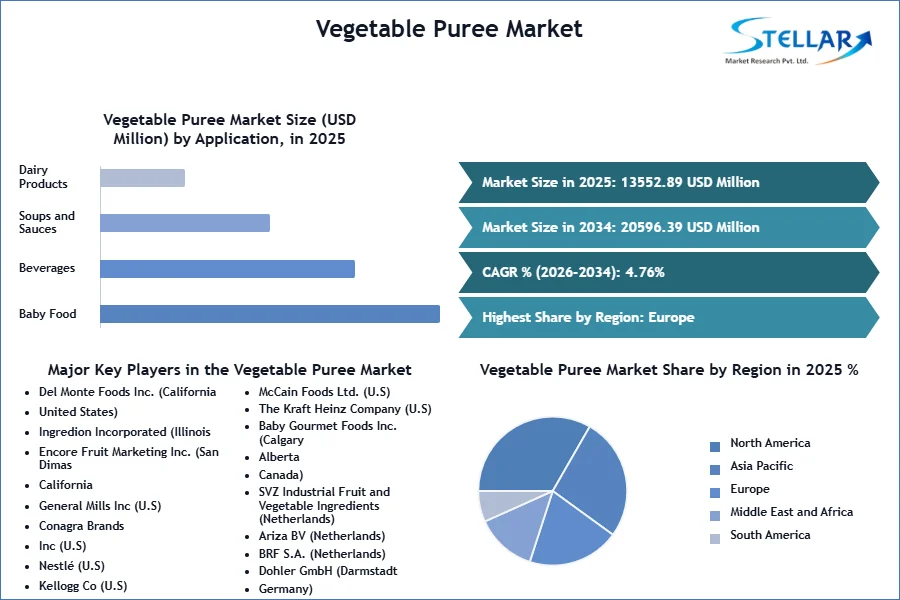

The Vegetable Puree Market size was valued at USD 13552.89 Million. in 2025 and the total Global Vegetable Puree revenue is expected to grow at a CAGR of 4.76% from 2026 to 2034, reaching nearly USD 20596.39 Million. by 2034.

Vegetable Puree Market Overview:

The global vegetable puree market has experienced robust growth in recent years, driven by increasing consumer demand for convenient and health-oriented products. Purees are pulp-based products that are more viscous than juices. Vegetable puree, also known as mash, is prepared by grinding and pressing cooked vegetables before blending or sifting until they have a liquid consistency or a creamy paste-like texture. Puree is an efficient way to retain or eat the full range of nutrients. It may be stored and frozen for an extended length of time without losing any nutritional value. Purees are cooked or uncooked ingredients that are crushed, combined and pressed into a supple, solid paste, usually fruits, vegetables, and legumes.

Vegetable purees, derived from fresh and quality vegetables, offer a rich source of vitamins and minerals, making them popular in various culinary applications such as baby foods, beverages, soups, sauces, and bakery products. These purees retain the taste, color, and nutrients of original vegetables, appealing to health-conscious consumers seeking nutritious options for themselves and their families. Moreover, the demand for convenience foods is boosting the vegetable puree market growth, as vegetable purees provide an easy-to-use solution with a long shelf-life, eliminating the need for tedious vegetable preparation. The rapid expansion of the food and beverage industry globally further drives vegetable puree industry growth, with more manufacturers incorporating vegetable purees into their products to meet consumer preferences for natural and healthier ingredients.

Based on Application, the baby food segment held the largest market share of 37.86% in terms of value in the global vegetable puree market in 2025 and is expected to maintain its dominance by 2034. This dominance is attributed to growing urbanization that has resulted in increased demand for baby food products. The Asia Pacific region is expected to register a high growth rate in the vegetable puree market, owing to the increasing population and rising disposable income of the demographic. India accounts for the largest share of the food and beverage sector by sales, followed by China and Indonesia. Rapid expansion in the tourism industry is expected to boost the construction of new hotels and restaurants, thus driving overall vegetable puree demand from the food service sector in the region.

The vegetable puree market presents potential opportunities for the manufacturers to grow through diversification of product offerings, catering to different consumer preferences and nutritional needs. Additionally, the growing popularity of organic foods and the availability of various vegetable puree options are expected to further increase the market revenue share during the forecast period. However, consumer preferences for fresh vegetables and packaging and transportation challenges for pureed foods are expected to hinder the global vegetable puree market growth during the forecast period.

To get more Insights: Request Free Sample Report

Vegetable Puree Market Regional Analysis:

Europe: Tomato Puree Demand Surges, Fueling Growth Of Vegetable Puree Market In Europe

According to the MMR analysis, the tomato is the most popular vegetable in Europe. Consumers tend to have committed to eating more fruits and vegetables in the spring rather than the New Year. 40% of customers purchase fruits and vegetables every other day, while 47% do so once a week. The United Kingdom (88%), the Netherlands (84%), and Belgium (82%) have the highest preference for purchasing fruits and vegetables from supermarkets. In Italy and Spain, local markets are more popular. Discounters rank bottom, with the exception of Germany, where 26% prefer to shop from these types of merchants.

Promotions affect the purchasing decisions of 70% of customers. Approximately 87% of customers consume veggies for supper, 69% for lunch, and only 5% for morning. Tomatoes, potatoes, carrots, mushrooms, and sweet peppers are the most popular vegetables among consumers. In Europe, tomatoes are at the top of this list. As a result, the demand for vegetable puree has significantly increased in European countries, thanks to its nutritional benefits, versatility, and convenience, thereby supporting the Europe vegetable puree market size.

Vegetable purees offer a practical solution for incorporating more vegetables into daily meals, aligning with the consumers’ increasing health consciousness and busy lifestyles. The growing customer preference for health-promoting and ready-to-cook products is driving the Europe vegetable puree market growth. According to the report Europe 2020 from the Ministry of Foreign Affairs, changing consumer eating habits and their steady shift away from conventional breakfast in favor of new options such as smoothies and soups has fueled demand for vegetable puree in European countries, major in the United Kingdom, the Netherlands, Belgium, Spain, Italy, Germany, etc.

The increased consumption of ready-to-eat/cook items with high nutritional content, as well as the incorporation of exotic vegetable puree in a variety of culinary products, all contribute to the European vegetable puree market revenue size and growth. In Europe, Tomato puree demand has witnessed a significant demand during the historic period (2019-2024) and according to the MMR analysis, the tomato puree segment growth is expected to grow at a rapid CAGR during the forecast period.

North America: Technological Innovations And Government Support Boost The North American Vegetable Puree Market

North America is expected to hold the second dominant position in the global vegetable puree market by 2034. This dominance is expected to be attributed to increasing awareness of health and wellness among North American consumers, and growing demand for cleaner food products that are minimally processed and retain all the nutritional values in it. In addition, rapidly increasing technological innovations and advancements in the food and beverage industry, particularly in the United States and Canada are further expected to boost the North American vegetable puree market size during the forecast period. For instance, vegetable puree manufacturers are increasingly adopting heat exchangers for puree production.

Heat Exchangers provides solutions and equipment capable of handling purées and concentrates, including those containing particulates and fiber, in the vegetable processing industry. Heat Exchangers’ technology has been developed to meet the demand of today’s tomato processors. As the demand for tomato purees is experiencing rapid growth, these advancements benefit the vegetable puree industry to meet the global tomato puree demand.

Canada's Investment In Vegetable Puree Production Spurs Market Growth In North America

In addition, supportive government initiatives further boost the vegetable puree industry revenue growth. For instance, On January 7, 2020, the Canadian and Manitoba governments announced an investment of over USD 582,000 in innovative equipment for Canadian Prairie Garden Puree Products Inc. This equipment enabled the company to transform Manitoba-grown produce, including fruits, vegetables, and pulse crops, into nutritious purees using a unique technology that preserves better color, flavor, texture, and nutritional benefits without preservatives. This method is also more cost-effective and environmentally friendly, using 30% less water and energy.

The investment supports Manitoba's goal of expanding its food processing industry to USD 5.5 Million by 2022. The company plans to increase its workforce from nine to nearly 60 employees and utilize culled vegetables that might otherwise be wasted. The purees, which can be stored at room temperature for up to two years, are sold to food manufacturers and food service customers.

This initiative is part of the Growing Value program, which helps agri-businesses adapt to market forces and environmental considerations, with federal and provincial governments investing USD 176 million under the Growing Forward 2 framework to enhance the agriculture industry’s competitiveness. This government investment significantly boosts the vegetable puree market in North America, particularly in Canada. By enabling Canadian Prairie Garden Puree Products Inc. to produce high-quality, preservative-free purees efficiently, the market is expected to see increased availability and variety of puree products. The technology’s environmental benefits and cost-effectiveness also drive demand among eco-conscious consumers and businesses, enhancing the vegetable puree market competitiveness. Additionally, the expansion of local processing capacity supports regional agriculture, reduces food waste, and fosters job creation, further strengthening the North American vegetable puree market.

Asia Pacific: Vegetables Supply Chain Disruptions Drive Surge In Vegetable Puree Demand In India

Asia Pacific region is expected to be a lucrative region for vegetable puree manufacturers, distributors, suppliers, etc. during the forecast period. The growing veganism, rising disposable income, improved standard of living, increasing awareness of the product, etc., are some of the major factors driving vegetable puree sales in the APAC countries. China and India are the leaders in the Asia Pacific vegetable puree market in terms of both revenue and volume share during the forecast period. In India, as fresh produce prices soar, particularly tomatoes, demand for tomato puree and frozen vegetables has surged, causing stock shortages and increased production by manufacturers in 2025. In Delhi, tomato prices have risen from Rs. 26.4 to Rs. 106.91 per kilogram in an August month. Consequently, tomato puree sales have increased by 300%, and frozen vegetable demand by 50%. Companies like Dabur and Mother Dairy are ramping up production to meet the heightened demand.

However, supply chain disruptions and lean production months have exacerbated the shortage. Retailers and online grocery firms like BigBasket, Swiggy Instamart, and Blinkit are struggling to keep up, with business-to-business wholesalers also running out of stock. Experts note the difficulty in predicting shortfalls in perishable food production, leading to potential temporary shortages in FMCG products. The significant price increase in fresh tomatoes and other vegetables in India is driving a substantial rise in demand for vegetable purees, thereby supporting the Indian vegetable puree market size.

This shift is influenced by the affordability and convenience of purees compared to fresh produce. Manufacturers are ramping up production to address the surge, potentially increasing the vegetable puree market in India. The increased reliance on processed vegetable products due to supply chain disruptions and seasonal production gaps could lead to long-term growth in the vegetable puree segment as consumers seek stable, cost-effective alternatives. Additionally, the heightened demand is further expected to encourage innovation and expansion in the puree processing industry, enhancing product availability and variety.

China's Growing Baby Foods Market Supports Growth Of Vegetable Puree Market In APAC

China’s Growing Baby Foods Market is expected to support the vegetable puree market in China in terms of sales revenue during the forecast period. According to the China National Bureau of Statistics, Chinese parents are spending 30% of their household income on their children. In 2020, the increase in expenditure made China’s Baby Food & Drink Market worth USD 30.1 Million and is expected to grow at a CAGR of 9.65% from 2021-2026. Thanks to rising malnutrition cases among babies, health concerns, and improved economic conditions, China’s organic baby food market has been rapidly growing in recent years. Chinese parents prioritize their children's wellness and are willing to spend on high-quality, expensive products. The increasing number of working women and busy lifestyles drive demand for convenient organic baby foods.

Key factors include fast-paced lifestyles, more working women choosing bottle feeding, safety concerns about locally grown ingredients, slow growth levels in children, a growing middle class with more disposable income, and social media influence are further increasing the product demand. Organic baby food, free from pesticides, antibiotics, hormones, artificial flavors, preservatives, and colors, is highly valued by Chinese parents. These factors collectively influence the China vegetable puree market during the forecast period. Additionally, the growth in e-commerce and the variety of available products support the global vegetable puree market size. The busy lifestyles of Chinese parents and the increasing number of working mothers further boost the demand for ready-made vegetable purees, making them a vital component of the organic baby food market's growth.

Vegetable Puree Market Scope:

|

Vegetable Puree Market |

|

|

Market Size in 2025 |

USD 13552.89 Million |

|

Market Size in 2034 |

USD 20596.39 Million |

|

CAGR (2026-2034) |

4.76 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments Covered |

By Product Type

|

|

By Application

|

|

|

By Distribution Channels

|

|

|

Regional Scope |

North America United States, Canada, And Mexico |

|

Europe United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, And The Rest Of Europe |

|

|

Asia Pacific China, India, Japan, South Korea, Australia, ASEAN, And The Rest Of APAC |

|

|

Middle East And Africa South Africa, GCC, And The Rest Of The Middle East, And Africa |

|

|

South America Brazil, Argentina, And The Rest Of South America |

|

Key Players in the Vegetable Puree Market

North America

- Del Monte Foods Inc. (California, United States)

- Ingredion Incorporated (Illinois, United States)

- Encore Fruit Marketing Inc. (San Dimas, California, United States)

- General Mills Inc (U.S)

- Conagra Brands, Inc (U.S)

- Nestlé (U.S)

- Kellogg Co (U.S)

- McCain Foods Ltd. (U.S)

- The Kraft Heinz Company (U.S)

- Baby Gourmet Foods Inc. (Calgary, Alberta, Canada)

Europe

- SVZ Industrial Fruit and Vegetable Ingredients (Netherlands)

- Ariza BV (Netherlands)

- BRF S.A. (Netherlands)

- Dohler GmbH (Darmstadt, Germany)

- Kiril Mischeff Ltd. (UK)

- Wm. Morrison Supermarkets (UK)

- 2 Sisters Food Group (UK)

- General Mills Inc (UK)

- Nestlé S.A. (Switzerland)

- Hormel Foods (Hungary)

- Waitrose (Columbia, UK)

- Lemon concentrate S.L.U (Spain)

Asia Pacific

- Nikken Foods Co. Ltd. (Tokyo, Japan)

- Kagome Co. Ltd. (Tokyo, Japan)

- Astral Foods (India)

- Conrox Agro and Food Pvt. (Maharashtra, India)

- Unilever (India)

Middle East & Africa

- Sun Impex (Dubai, UAE)

South America

- BRF S.A. (Brazil)

- JBS S.A. (Brazil)

Frequently Asked Questions

Factors such as increasing consumer demand for convenient and healthy food options, rising awareness about the nutritional benefits of vegetable purees, increasing veganism, and the growing trend of plant-based diets are driving the global vegetable puree market growth.

Consumer preferences are driving product development in the vegetable puree market towards clean-label products, allergen-free formulations, and sustainable packaging options to meet the demand for healthier, more transparent, and environmentally friendly choices.

Opportunities in the global vegetable puree market include expanding into emerging markets, diversifying product offerings to cater to specific dietary preferences and lifestyle trends, and investing in research and development to innovate new vegetable puree formulations and applications.

Technological advancements in food processing and packaging techniques are improving the shelf life, quality, and safety of vegetable puree products, thereby driving the vegetable puree market growth.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Vegetable Puree Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2034) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Vegetable Puree Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

4. Vegetable Puree Market: Dynamics

4.1. Vegetable Puree Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Vegetable Puree Market Drivers

4.3. Vegetable Puree Market Restraints

4.4. Vegetable Puree Market Opportunities

4.5. Vegetable Puree Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape by Region

4.10.1. North America

4.10.2. Europe

4.10.3. Asia Pacific

4.10.4. Middle East and Africa

4.10.5. South America

5. Vegetable Puree Market: Global Market Size and Forecast by Segmentation (by Value in USD Billion and Volume in Kilotons) (2026-2034)

5.1. Vegetable Puree Market Size and Forecast, by Product Type (2026-2034)

5.1.1. Single Vegetable Purees

6.1.1.1 Carrot Puree

6.1.1.2 Tomato Puree

6.1.1.3 Pumpkin Puree

6.1.1.4 Spinach Puree

6.1.1.5 Sweet Potato Puree

6.1.1.6 Others

5.1.2. Mixed Vegetable Purees

5.2. Vegetable Puree Market Size and Forecast, by Application (2026-2034)

5.2.1. Baby Food

5.2.2. Beverages

5.2.3. Soups and Sauces

5.2.4. Dairy Products

5.2.5. Others

5.3. Vegetable Puree Market Size and Forecast, by Distribution Channels (2026-2034)

5.3.1. Offline

5.3.1.1. Supermarket/Hypermarket

5.3.1.2. Grocery Stores

5.3.1.3. Others

5.3.2. Online

5.4. Vegetable Puree Market Size and Forecast, by Region (2026-2034)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Vegetable Puree Market Size and Forecast by Segmentation (by Value in USD Billion and Volume in Kilotons) (2026-2034)

6.1. North America Vegetable Puree Market Size and Forecast, by Product Type (2026-2034)

6.1.1. Single Vegetable Purees

6.1.1.7 Carrot Puree

6.1.1.8 Tomato Puree

6.1.1.9 Pumpkin Puree

6.1.1.10 Spinach Puree

6.1.1.11 Sweet Potato Puree

6.1.1.12 Others

6.1.2. Mixed Vegetable Purees

6.2. North America Vegetable Puree Market Size and Forecast, by Application (2026-2034)

6.2.1. Baby Food

6.2.2. Beverages

6.2.3. Soups and Sauces

6.2.4. Dairy Products

6.2.5. Others

6.3. North America Vegetable Puree Market Size and Forecast, by Distribution Channels (2026-2034)

6.3.1. Offline

6.3.1.1. Supermarket/Hypermarket

6.3.1.2. Grocery Stores

6.3.1.3. Others

6.3.2. Online

6.4. North America Vegetable Puree Market Size and Forecast, by Country (2026-2034)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Vegetable Puree Market Size and Forecast by Segmentation (by Value in USD Billion and Volume in Kilotons) (2026-2034)

7.1. Europe Vegetable Puree Market Size and Forecast, by Product Type (2026-2034)

7.2. Europe Vegetable Puree Market Size and Forecast, by Application (2026-2034)

7.3. Europe Vegetable Puree Market Size and Forecast, by Distribution Channels (2026-2034)

7.4. Europe Vegetable Puree Market Size and Forecast, by Country (2026-2034)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Vegetable Puree Market Size and Forecast by Segmentation (by Value in USD Billion and Volume in Kilotons) (2026-2034)

8.1. Asia Pacific Vegetable Puree Market Size and Forecast, by Product Type (2026-2034)

8.2. Asia Pacific Vegetable Puree Market Size and Forecast, by Application (2026-2034)

8.3. Asia Pacific Vegetable Puree Market Size and Forecast, by Distribution Channels (2026-2034)

8.4. Asia Pacific Vegetable Puree Market Size and Forecast, by Country (2026-2034)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Rest of Asia Pacific

9. Middle East and Africa Vegetable Puree Market Size and Forecast by Segmentation (by Value in USD Billion and Volume in Kilotons) (2026-2034)

9.1. Middle East and Africa Vegetable Puree Market Size and Forecast, by Product Type (2026-2034)

9.2. Middle East and Africa Vegetable Puree Market Size and Forecast, by Application (2026-2034)

9.3. Middle East and Africa Vegetable Puree Market Size and Forecast, by Distribution Channels (2026-2034)

9.4. Middle East and Africa Vegetable Puree Market Size and Forecast, by Country (2026-2034)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Nigeria

9.4.4. Rest of ME&A

10. South America Vegetable Puree Market Size and Forecast by Segmentation (by Value in USD Billion and Volume in Kilotons) (2026-2034)

10.1. South America Vegetable Puree Market Size and Forecast, by Product Type (2026-2034)

10.2. South America Vegetable Puree Market Size and Forecast, by Application (2026-2034)

10.3. South America Vegetable Puree Market Size and Forecast, by Distribution Channels (2026-2034)

10.4. South America Vegetable Puree Market Size and Forecast, by Country (2026-2034)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. Del Monte Foods Inc. (California, United States)

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc.)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Ingredion Incorporated (Illinois, United States)

11.3. Encore Fruit Marketing Inc. (San Dimas, California, United States)

11.4. General Mills Inc (U.S)

11.5. Conagra Brands, Inc (U.S)

11.6. Nestlé (U.S)

11.7. Kellogg Co (U.S)

11.8. McCain Foods Ltd. (U.S)

11.9. The Kraft Heinz Company (U.S)

11.10. Baby Gourmet Foods Inc. (Calgary, Alberta, Canada)

11.11. SVZ Industrial Fruit and Vegetable Ingredients (Netherlands)

11.12. Ariza BV (Netherlands)

11.13. BRF S.A. (Netherlands)

11.14. Dohler GmbH (Darmstadt, Germany)

11.15. Kiril Mischeff Ltd. (UK)

11.16. Wm. Morrison Supermarkets (UK)

11.17. 2 Sisters Food Group (UK)

11.18. General Mills Inc (UK)

11.19. Nestlé S.A. (Switzerland)

11.20. Hormel Foods (Hungary)

11.21. Waitrose (Columbia, UK)

11.22. Lemon concentrate S.L.U (Spain)

11.23. Nikken Foods Co. Ltd. (Tokyo, Japan)

11.24. Kagome Co. Ltd. (Tokyo, Japan)

11.25. Astral Foods (India)

11.26. Conrox Agro and Food Pvt. (Maharashtra, India)

11.27. Unilever (India)

11.28. Sun Impex (Dubai, UAE)

11.29. BRF S.A. (Brazil)

11.30. JBS S.A. (Brazil)

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook