Semiconductor Memory Market - Global Industry Analysis and Forecast 2026-2034

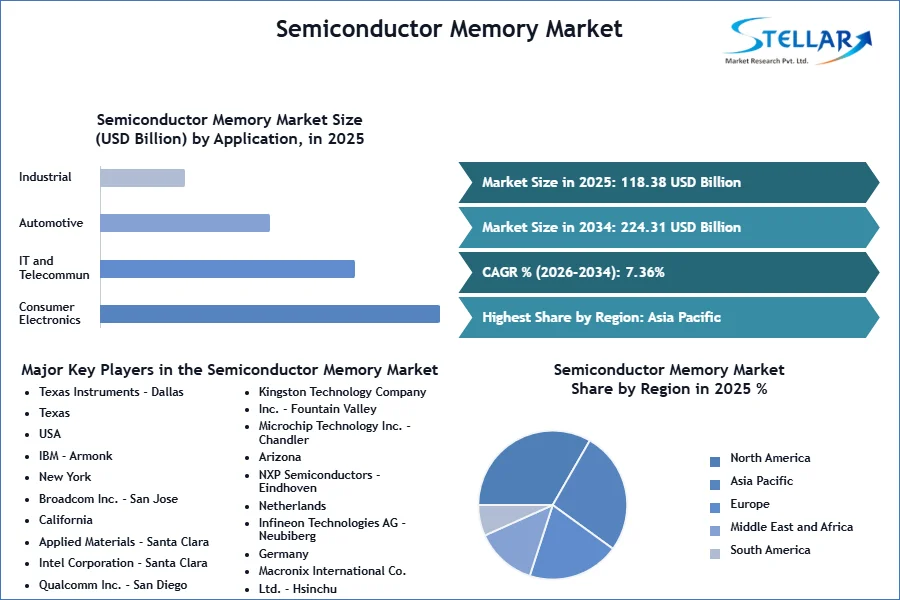

Semiconductor Memory Market size was valued at USD 118.38 Bn. in 2025 and the total Semiconductor Memory Market size is expected to grow at a CAGR of 7.36 % from 2026 to 2034, reaching nearly USD 224.31 Bn. by 2034.

Semiconductor Memory Market Overview:

A type of electronic memory known as semiconductor memory stores digital data by making use of semiconductor materials, most commonly silicon. Semiconductor memory is a sort of computerized electronic memory that utilizes semiconductor material, ordinarily silicon, to store and recover advanced information. Semiconductor memory is extensively used in the production of electronic components, utilizing computer processing techniques. It plays a crucial role in the creation of computer-based printed circuit boards (PCBs), greatly contributing to the growth of the Semiconductor Memory Market.

In addition, the increasing need for high-performance computing and the burgeoning use of 5G services are driving the semiconductor memory Industry. For instance, to provide carriers with up to $9 billion in Universal Service Fund funding to provide advanced 5G mobile wireless services in rural America (including up to $680 million for deployment on tribal territories), the Commission created the 5G Fund for Rural America in October 2020. Additionally, the Fund allows at least $1 billion expressly for deployments supporting the requirements of precision agriculture.

The semiconductor memory market is highly competitive, and key players in the industry include Samsung, SK Hynix, Micron, Nanya Technology Corporation, Winbond Electronics Corporation, Intel, Kioxia, WDC, and others provides in the Semiconductor Memory Market report. These companies have distinguished themselves through their technological advancements, semiconductor memory industry growth, and substantial sales revenues, making them leaders in the industry.

Semiconductor chip import shipments in the World stood at 95K, imported by 1,657 World Importers from 3,657 Suppliers.

The world imports most of its Semiconductor chips from South Korea, China, and Japan

The top 3 importers of Semiconductor chips are Vietnam with 65,308 shipments followed by Russia with 9,426 and India at the 3rd spot with 5,745 shipments.

To get more Insights: Request Free Sample Report

Semiconductor Memory Market Dynamics:

Driving Forces Behind the Growing Semiconductor Memory Market

Increasing application of semiconductor components in different industries, such as consumer electronics, automotive, and IT & Telecom expected to fuel the semiconductor memory market growth. Rapid development in the form of automation and digitalization in the electronics industry coupled with the implementation of memory-based elements in advanced products such as wearable devices, smartphones, and electronic gadgets propels the Semiconductor Memory industry growth across the globe.

The growing integration of electronic components and improving automotive systems in automobiles is expected to create growth opportunities for leading players in the semiconductor memory industry. Modernization of infotainment vehicle design systems, autonomous driving systems, and safety systems drives semiconductor memory market growth during the forecast period. DRAM and flash memory used in lighting control & ADAS systems offer vehicle systems high speed and connectivity.

The need for increased capacity, improved speeds, and reduced power usage remains a driving force for innovation in Semiconductor memory technologies. Additionally, a rise of data-heavy technologies such as AI, ML, and big data analysis drives the demand for Semiconductor memory solutions. Therefore, it is expected that the semiconductor memory market continues to be strong, influenced by ongoing changes in the industry.

Applications and Challenges of Emerging Memory Technologies in Advanced Computing

The tangible applications of emerging memories are mainly serving as embedded non-volatile memories for the global buffer in microprocessors/accelerators or code storage as in microcontrollers. It is understood that emerging memories are facing difficulties directly competing against the high-density DRAM/NAND products in the standalone memory space. As of 2023, emerging memories are available from foundry platforms at mature legacy nodes.

For instance, TSMC is offering resistive random-access memory (RRAM) at 40-nm/28-nm/22-nm nodes.8 TSMC is also offering spin-transfer torque magnetic random-access memory (STT-MRAM) at 22-nm/16-nm nodes.9 STMicroelectronics is offering phase change memory (PCM) at 28-nm node,10 and GlobalFoundries is offering FeFET at 28-nm/22-nm nodes.11 Sony and Micron are developing FeRAM based on HfO2 material, and the prototype chip density increased from 64 kb12 to 32 Gb13 recently. The general characteristics of these emerging memories include sub-100-ns write/read speed, >106 endurance cycles, and more years of retention, while the MRAM has a unique advantage of low write voltage (<1 V), and FeFET has a unique advantage of low write energy (<10 fJ/bit).

Emerging memories are attractive for certain niche Semiconductor Memory markets, for example, automotive and aerospace electronics where stringent requirements exist on high/low-temperature performance or immunity to radiation effects. The challenges for increasing the application space include lowering the write voltage and making the technologies compatible with more advanced logic processes such as 7 nm or beyond, improving endurance and retention, and supporting reliable multilevel operation. The research community is also actively exploring using the emerging memories in the new computing paradigm such as in-memory computing or in-memory search to accelerate the data-intensive workloads such as AI/ML and combinatorial optimization.

Semiconductor Memory Market Segment Analysis:

By Type, DRAM held the largest share in 2024 for the Semiconductor Memory Industry. Dynamic random-access memory (DRAM) is used as the main memory, and it is often regarded as off-chip standalone memory with input/output (I/O) links communicating with microprocessors/accelerators. The demand for high-performance and low-power DRAM solutions in mobile devices is expected to boost the Semiconductor Memory market growth. DRAM scaling as of 2023 has reached a 12-nm node and the bit density reaches more than 300 Mbit/mm2 for DDR54 and exceeds 1 Gbit/mm2 for HBM3 that employs the 3D die stacking.

With the help of the government, regional market participants have been raising their production levels to keep up with the rising demand for DRAM globally. For example, ChangXin Memory Technology (CXMT) declared in March 2022 that it intended to produce DDR5 for the Chinese market. Recently, CXMT's goals have increased as a result of a sizable investment from Ruili Integration, its parent business. The corporation wants to increase manufacturing capacity and facilities while also investing more in R&D. By the end of this year, CXMT plans to set up its mass production facilities following the successful testing of DDR5 manufacturing. To support the growth of the regional Semiconductor Memory market, the business intends to introduce more sophisticated 17nm (LP) DDR5 and other advanced process memory chips in China.

May 2023- Micron announced their plans to invest USD 3.7 billion in new DRAM chips in Japan.

September 2023- Samsung Electronics, a global leader in advanced memory technology, developed the industry's first 32-gigabit (Gb) DDR5 DRAM1 using 12 nanometers (nm)-class process technology.

Table: Highlights Key Applications Areas Along with Key Characteristics for The Various Memory Types

|

Types |

Computer |

Comms |

Consumer |

Auto |

Industrial |

Government |

Key Technology

|

|

DRAM |

51 % |

37 % |

8 % |

1 % |

2% |

0% |

|

|

SRAM |

7 % |

23 % |

4% |

15% |

48% |

3 % |

|

|

Flash |

49 % |

31% |

16 % |

2% |

2% |

0% |

|

|

Others |

8% |

12% |

36% |

10% |

33% |

1% |

Includes EPROM, Nor Flash, and emerging technologies for commercial applications. |

Semiconductor Memory Market Regional Insight:

Asia Pacific dominate region in 2024 for the Semiconductor Memory Market. Economic growth leads to a rise in consumer purchases of gadgets such as smartphones, tablets, and laptops. The Asia Pacific area is undergoing swift increase in the Internet of Things (IoT) sector. Devices associated with IoT, including smart home items, wearable tech, and industrial IoT projects, require a considerable volume of memory for data storage and analysis. The rise in interconnected devices leads to a greater need for advanced semiconductor memory solutions to meet these demands.

In South Korea, the companies have been increasing the production of DRAM. In June 2022, SK Hynix supply the Industry's First HBM3 DRAM to Nvidia Corporation. The company has begun the mass production of HBM3, the world's best-performing DRAM. With accelerating advancements in cutting-edge technologies like artificial intelligence and big data, major global technology companies are seeking ways to process increasing volumes of data rapidly. In response to the launch of new CPUs by Intel Corporation and AMD that support DDR5 DRAM solutions for PCs and servers, South Korean suppliers are developing solutions to complement the arrival of the new CPUs. All these factors drive the regional Semiconductor Memory market growth.

Rising Data Demands Propel Growth in Semiconductor Memory Market

The increasing demand for data centers also boosts the demand for Semiconductor Memory Market. By 2025, it’s estimated that the world will have generated more than 180 zettabytes (180 trillion gigabytes) of data, driven by dramatic increases in both consumer and business data. People share more than 8,000 photos per second on Snapchat, view about 4 billion videos per day on Facebook, and watch one billion hours of YouTube every day.

Now add to that the data generated every minute on Zoom, Twitter, Instagram, and so on. Small amounts of data add up too. As buildings and cities get smarter, sensors are everywhere on every streetlight, traffic light, parking meter, elevator, and air conditioner. The IoT data is also increasingly generated by pieces of industrial equipment, shipping crates, agricultural assets, and so on. Data is everywhere and it’s growing rapidly.

In October 2023, local authorities announced that China's southwestern Province of Guizhou has 39 significant data centers in operation or under construction.

Semiconductor Memory Market Competitive Landscape:

The semiconductor memory market is intensely competitive, with major companies always striving to innovate and distinguish their offerings to keep and increase their presence in the market. The environment is influenced by technological progress, strategic alliances, and focused market targeting, enabling firms to meet a variety of customer needs and remain competitive in the swiftly changing sector.

Texas Instruments Incorporated (TI) stands out as a key figure in the world of semiconductors, recognized for its diverse collection of analog and embedded processing technologies. Although TI is not commonly associated with leading the charge in unpredictable and stable memory areas such as DRAM or NAND flash memory, it remains instrumental in the semiconductor memory landscape by offering a range of distinct memory solutions and uses.

In February 2023, Texas Instruments Incorporated announced that it would invest USD 11 billion into the construction of its next 300-mm semiconductor wafer fabrication plant in Utah, U.S. The company aimed to expand its manufacturing capacity to meet the growing demand for semiconductors in electronics.

SK Hynix focuses on producing high-density and high-speed DRAM chips. The company leverages its technological capabilities to compete effectively in the market.

In August 2023, SK HYNIX INC. announced that it had started supplying a 24GB LPDDR5X DRAM mobile DRAM package, the industry’s first such solution with a 24 GB capacity. The new product provides enhanced performance while consuming low power. The company aimed to meet its customers’ needs with this product.

In Conclusion, leading players in the semiconductor Memory Market focus on innovative memory systems, including 3D NAND, DRAM, and up-and-coming solutions such as MRAM and ReRAM. These advancements provide improved performance, reduced energy use, and increased storage space, all of which are essential for today's applications. Key Players are seeking opportunities in the automotive, Internet of Things, artificial intelligence, and distributed computing sectors. For instance, Texas Instruments has been broadening its range of semiconductor products to meet the increasing demands of the automotive industry.

Semiconductor Memory Market Scope:

|

Semiconductor Memory Market |

|

|

Market Size in 2025 |

USD 118.38 Bn. |

|

Market Size in 2034 |

USD 224.31 Bn. |

|

CAGR (2026-2034) |

7.36 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments

|

By Memory Type

|

|

By Application

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Semiconductor Memory Market Key Players:

- Micron Technology - Boise, Idaho, USA

- Texas Instruments - Dallas, Texas, USA

- IBM - Armonk, New York, USA

- Broadcom Inc. - San Jose, California, USA

- Applied Materials - Santa Clara, California, USA

- Intel Corporation - Santa Clara, California, USA

- Qualcomm Inc. - San Diego, California, USA

- Kingston Technology Company, Inc. - Fountain Valley, California, USA

- Microchip Technology Inc. - Chandler, Arizona, USA

- NXP Semiconductors - Eindhoven, Netherlands

- Infineon Technologies AG - Neubiberg, Germany

- Macronix International Co., Ltd. - Hsinchu, Taiwan

- Powerchip Technology Corporation - Hsinchu, Taiwan

- Samsung Electronics - Suwon, South Korea

- Taiwan Semiconductor - Hsinchu, Taiwan

- SK Hynix - Icheon, South Korea

- Toshiba - Tokyo, Japan

- Renesas Electronics Corporation - Tokyo, Japan

- Fujitsu Limited - Tokyo, Japan

- Shanghai Huali Microelectronics Corporation (HLMC) - Shanghai, China

Frequently Asked Questions

Increasing application of semiconductor components in different industries, such as consumer electronics, automotive, and IT & Telecom expected to fuel the semiconductor memory market growth.

The Market size was valued at USD 118.38 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 7.36 % from 2026 to 2034, reaching nearly USD 224.31 Billion.

The segments covered in the market report are By Memory Types and Applications.

Asia Pacific Dominate region in the Semiconductor Memory market.

1. Semiconductor Memory Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Assumptions

2. Semiconductor Memory Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2034) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Semiconductor Memory Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2023)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

4. Semiconductor Memory Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Semiconductor Memory Market Size and Forecast by Segments (by Value USD Million)

5.1. Semiconductor Memory Market Size and Forecast, By Memory Type (2025-2032)

5.1.1. DRAM

5.1.2. SRAM

5.1.3. ROM

5.1.4. EEPROM

5.1.5. Others

5.2. Semiconductor Memory Market Size and Forecast, By Application (2025-2032)

5.2.1. Consumer Electronics

5.2.2. IT and Telecommunication

5.2.3. Automotive

5.2.4. Industrial

5.2.5. Aerospace and Defense

5.2.6. Medical

5.2.7. Others

5.3. Semiconductor Memory Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Semiconductor Memory Market Size and Forecast (by Value USD Million)

6.1. North America Semiconductor Memory Market Size and Forecast, By Memory Type (2025-2032)

6.1.1. DRAM

6.1.2. SRAM

6.1.3. ROM

6.1.4. EEPROM

6.1.5. Others

6.2. North America Semiconductor Memory Market Size and Forecast, By Application (2025-2032)

6.2.1. Consumer Electronics

6.2.2. IT and Telecommunication

6.2.3. Automotive

6.2.4. Industrial

6.2.5. Aerospace and Defense

6.2.6. Medical

6.2.7. Others

6.3. North America Semiconductor Memory Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Semiconductor Memory Market Size and Forecast (by Value USD Million)

7.1. Europe Semiconductor Memory Market Size and Forecast, By Memory Type (2025-2032)

7.2. Europe Semiconductor Memory Market Size and Forecast, By Application (2025-2032)

7.3. Europe Semiconductor Memory Market Size and Forecast, by Country (2025-2032)

7.3.1. UK

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Semiconductor Memory Market Size and Forecast (by Value USD Million)

8.1. Asia Pacific Semiconductor Memory Market Size and Forecast, By Memory Type (2025-2032)

8.2. Asia Pacific Semiconductor Memory Market Size and Forecast, By Application (2025-2032)

8.3. Asia Pacific Semiconductor Memory Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Bangladesh

8.3.11. Pakistan

8.3.12. Rest of Asia Pacific

9. Middle East and Africa Semiconductor Memory Market Size and Forecast (by Value USD Million)

9.1. Middle East and Africa Semiconductor Memory Market Size and Forecast, By Memory Type (2025-2032)

9.2. Middle East and Africa Semiconductor Memory Market Size and Forecast, By Application (2025-2032)

9.3. Middle East and Africa Semiconductor Memory Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Egypt

9.3.4. Nigeria

9.3.5. Rest of ME&A

10. South America Semiconductor Memory Market Size and Forecast (by Value USD Million)

10.1. South America Semiconductor Memory Market Size and Forecast, By Memory Type (2025-2032)

10.2. South America Semiconductor Memory Market Size and Forecast, By Application (2025-2032)

10.3. South America Semiconductor Memory Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest of South America

11. Company Profile: Key players

11.1. Micron Technology - Boise, Idaho, USA

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Texas Instruments - Dallas, Texas, USA

11.3. IBM - Armonk, New York, USA

11.4. Broadcom Inc. - San Jose, California, USA

11.5. Applied Materials - Santa Clara, California, USA

11.6. Intel Corporation - Santa Clara, California, USA

11.7. Qualcomm Inc. - San Diego, California, USA

11.8. Kingston Technology Company, Inc. - Fountain Valley, California, USA

11.9. Microchip Technology Inc. - Chandler, Arizona, USA

11.10. NXP Semiconductors - Eindhoven, Netherlands

11.11. Infineon Technologies AG - Neubiberg, Germany

11.12. Macronix International Co., Ltd. - Hsinchu, Taiwan

11.13. Powerchip Technology Corporation - Hsinchu, Taiwan

11.14. Samsung Electronics - Suwon, South Korea

11.15. Taiwan Semiconductor - Hsinchu, Taiwan

11.16. SK Hynix - Icheon, South Korea

11.17. Toshiba - Tokyo, Japan

11.18. Renesas Electronics Corporation - Tokyo, Japan

11.19. Fujitsu Limited - Tokyo, Japan

11.20. Shanghai Huali Microelectronics Corporation (HLMC) - Shanghai, China

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook