Semiconductor Manufacturing Chemical Market Industry Analysis and Forecast (2026-2032)

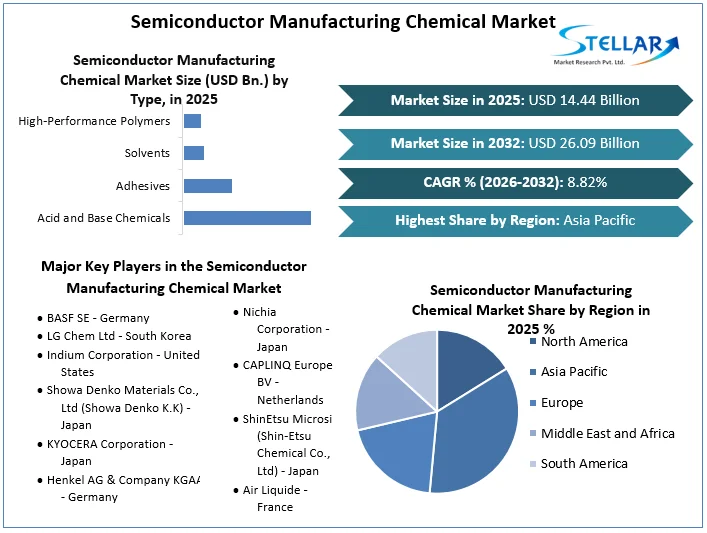

The Semiconductor Manufacturing Chemical Market size was valued at USD 14.44 Bn. in 2025 and the total Global Semiconductor Manufacturing Chemical revenue is expected to grow at a CAGR of 8.82% from 2026 to 2032, reaching nearly USD 26.09 Bn. by 2032.

Semiconductor Manufacturing Chemical Market Overview:

Semiconductor manufacturing chemicals are specialized substances essential for fabricating integrated circuits and microchips. These chemicals encompass a range of materials, including photoresists, etchants, CMP slurries, cleaning agents, dopants, precursors, dielectric materials, and various gases. Photoresists are light-sensitive materials used in photolithography to create detailed circuit patterns on wafers.

Etchants, available in wet and dry forms, remove material to define intricate geometries. CMP slurries, containing abrasives and chemicals, planarize wafer surfaces, ensuring smoothness for subsequent steps. Cleaning agents remove contaminants, maintaining wafer purity. Dopants modify the electrical properties of semiconductors by introducing impurities, while precursors in CVD and ALD processes form thin films. Dielectric materials insulate and separate conducting regions, and gases like nitrogen, oxygen, and silane play crucial roles in doping, etching, and deposition processes.

These chemicals are vital for the ongoing advancements in semiconductor technology, driving the industry's push towards higher performance, smaller nodes, and greater material purity. The demand for sophisticated semiconductor devices in various applications, from consumer electronics to automotive and industrial sectors, underscores the significance of semiconductor manufacturing chemicals in the semiconductor manufacturing chemical market globally.

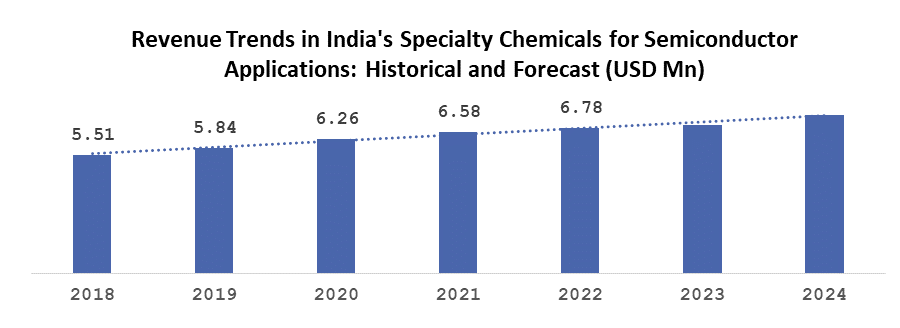

India's Emerging Semiconductor Manufacturing Chemicals Market (USD Mn)

The Semiconductor Manufacturing Chemical Market in India is witnessing significant growth, driven by the country's robust position as the 6th largest seller of specialty chemicals globally, contributing approximately 3% to the global chemical industry. This growth is underpinned by the availability of essential chemicals such as Sulphuric Acid, Hydrochloric Acid (HCL), Nitric Acid, Hydrogen Peroxide (H2O2), Ethanol, and Carbon, along with critical industrial gases like oxygen, nitrogen, argon, and carbon dioxide.

Key states such as Gujarat, Rajasthan, Haryana, and Andhra Pradesh house some of the largest chemical plants, bolstering the production capacity required to meet the demands of semiconductor manufacturers worldwide. The market is expected to grow at a highest CAGR over 2026-2032, driven by increasing demand for advanced electronic devices, favorable government policies, and technological advancements in semiconductor manufacturing processes. This positions India as a vital player in the global semiconductor supply chain, providing the necessary chemicals to support the industry's growth

To get more Insights: Request Free Sample Report

Semiconductor Manufacturing Chemical Market Dynamics:

The semiconductor manufacturing chemical market exhibits a dynamic landscape shaped by several key drivers, each playing a significant role in steering the industry's trajectory and fostering growth. Technological advancements and innovations stand as primary drivers, driving the semiconductor manufacturing chemical industry forward in tandem with the relentless pace of semiconductor technology evolution. With a continuous quest for enhanced device performance, speed, and energy efficiency, the industry continuously demands cutting-edge chemical formulations adapted to the semiconductor manufacturing chemical market.

Notably, emerging technologies such as 5G, artificial intelligence, and the Internet of Things necessitate specialized chemical solutions to meet the stringent requirements of modern semiconductor manufacturing processes. This continuous pursuit of technical excellence ensures that the semiconductor manufacturing chemical market remains at the forefront, adept at catering to the rising complexity and demands of the global electronics sector.

Furthermore, the growing demand for electronic devices serves as a pivotal driver, bolstering the semiconductor manufacturing chemical market's growth trajectory. The global usage of smartphones, tablets, laptops, and smart appliances, coupled with rapid technological advancements, underscores the imperative for high-performance semiconductors and the essential role of chemicals tailored to the semiconductor manufacturing chemical market. Semiconductor chemicals play a crucial role across the manufacturing, packaging, and testing stages, facilitating the attainment of stringent performance and efficiency standards mandated by contemporary electronic devices. As consumer preferences gravitate towards increasingly sophisticated and feature-rich gadgets, the semiconductor manufacturing chemical sector experiences a sustained uptick in demand, underscoring the indispensability of specialized chemicals in preserving the quality and functionality of electronic components.

Moreover, the growth of global connectivity and communication, particularly fueled by the widespread deployment of 5G networks, emerges as another driving force propelling the semiconductor manufacturing chemical market forward. The imperative for high-speed data transmission, coupled with the burgeoning device interconnectivity facilitated by the Internet of Things (IoT), necessitates advancements in semiconductor technology and corresponding chemicals within the semiconductor manufacturing chemical market. These advancements entail the utilization of specific chemicals in critical fabrication processes such as deposition, etching, and cleaning. As the world becomes increasingly digitally interconnected, the semiconductor manufacturing chemical market witnesses a surge in demand, driven by the pivotal role these chemicals play in ensuring the efficiency and durability of semiconductor devices that power contemporary communication networks.

Environmental regulations use a significant influence on the semiconductor manufacturing chemical market, compelling companies to embrace environmentally responsible practices tailored to the Semiconductor Manufacturing Chemical Market. With sustainability gaining momentum, stringent environmental standards prompt the sector to embrace greener methodologies and materials. This entails a growing preference for semiconductor compounds with reduced environmental impact, as manufacturers strive to minimize waste, energy consumption, and the utilization of hazardous materials in semiconductor production. Compliance with environmental mandates not only aligns with global sustainability objectives but also positions enterprises favorably in the market, catering to the burgeoning demand for ecologically sustainable solutions in the semiconductor manufacturing chemical sector.

Semiconductor Manufacturing Chemical Market Segments Analysis:

By Distribution Channel, Solvents holds a dominant position, commanding a semiconductor manufacturing chemical market share of more than 25% in 2025. Their dominance stems from their critical function across several indispensable processes involved in semiconductor fabrication. These chemicals are instrumental in maintaining the cleanliness and purity of semiconductor components by effectively removing impurities and particles that could compromise the integrity of the final product. Particularly in processes demanding high levels of purity, such as semiconductor manufacturing, solvents, especially high-purity variants, are indispensable. Even minute impurities can introduce flaws, underscoring the significance of solvents in ensuring the desired quality standards.

Moreover, solvents play a crucial role in photolithography procedures, a cornerstone of semiconductor fabrication, where they facilitate the dissolution and removal of photoresists that define intricate circuit designs on semiconductor wafers. The precision required in semiconductor manufacturing heavily relies on the capacity of solvents to selectively remove specific materials, enabling the precise patterning essential for advanced semiconductor devices.

Furthermore, solvents are integral to chemical mechanical polishing (CMP) procedures, which are essential for planarizing the semiconductor surface. By ensuring uniformity across various layers and promoting proper adhesion, CMP procedures help minimize defects and enhance overall chip performance. This underscores the multifaceted role of solvents in semiconductor manufacturing, where their efficacy extends beyond mere cleanliness to include critical functions essential for achieving the desired performance and quality standards in semiconductor devices.

By Application, in 2025, the Etching Chemicals sub-segment emerged as the dominant force within the semiconductor manufacturing chemical market. Etching enables precise removal of materials from semiconductor wafers, facilitating the creation of intricate patterns and features essential for the fabrication of integrated circuits and other semiconductor devices. The continuous pursuit of miniaturization and the evolution of innovative semiconductor designs, such as FinFET transistors and 3D NAND memory, have intensified the demand for precise etching methods.

Furthermore, heightened environmental awareness and the imperative for sustainable manufacturing processes are propelling the development of greener and more eco-friendly etching chemicals. This convergence of precision, innovation, and environmental responsibility underscores the pivotal position of the etching segment within the semiconductor chemicals market, signalling its crucial role in semiconductor production and reflecting the evolving landscape of the industry.

Semiconductor Manufacturing Chemical Market Regional Analysis:

In 2024, Asia Pacific asserted its dominance as the leading region in the global semiconductor manufacturing chemical market. Renowned for driving semiconductor innovation, research, and development, Asia Pacific shines as a beacon for cutting-edge advancements in semiconductor manufacturing and technology. Key players like Taiwan, South Korea, and China have ascended as premier hubs for semiconductor production and technical breakthroughs. Backed by robust government support and substantial research investments, the region boasts a resilient semiconductor supply chain, ensuring timely and efficient delivery of semiconductor products to global markets. Serving as a dynamic industry hub, the Asia Pacific not only shapes market size but also steers the trajectory of semiconductor technology and its worldwide applications.

China commands the forefront of global electronics production, boasting the largest manufacturing base for electronic goods globally. With products like smartphones, TVs, and various personal devices witnessing significant growth, China's electronic industry stands as a powerhouse in the global market. Recording a 13% growth in 2022, surpassing the 10% rise in 2021, the Chinese electronics market continues to expand, with a projected 7% growth rate for 2023. In fact, China's electronic industry surged by 14% in 2022 and is estimated to grow by 8% in 2023.Despite its manufacturing prowess, China remains a net importer of semiconductor chips, manufacturing less than 20% of the semiconductors it utilizes. Nevertheless, the lucrative demand both domestically and internationally in 2022 propelled 101 Chinese-listed semiconductor companies to announce net profits, signaling a positive trend for the Semiconductor Manufacturing Chemical Market.

India's domestic electronics manufacturing sector is on a steady growth trajectory, fueled by favorable government policies such as 100% foreign direct investment (FDI) and streamlined production processes. Initiatives like the Modified Incentive Special Package Scheme (M-SIPS) and the Electronics Development Fund (EDF) further bolster the sector, with a substantial budget earmarked for domestic electronics manufacturing in India.

Semiconductor Manufacturing Chemical Market Recent Development:

A recent development in the Semiconductor Manufacturing Chemical Market is the growing emphasis on sustainability and environmental responsibility within the industry. As demand for semiconductors continues to rise, manufacturers are increasingly focusing on reducing the environmental impact of their operations. This includes efforts to minimize water and energy consumption, reduce chemical waste, and implement cleaner production processes. Additionally, there is a growing trend towards the development of eco-friendly semiconductor manufacturing chemicals. Companies are investing in research and development to create chemicals that are less toxic, more biodegradable, and have a smaller carbon footprint. These efforts align with global initiatives to combat climate change and promote sustainable development.

Furthermore, partnerships and collaborations between semiconductor manufacturers and chemical suppliers are becoming more common. By working together, companies can leverage each other's expertise to develop innovative solutions that meet both performance and sustainability requirements. Overall, the recent focus on sustainability and environmental responsibility in the Semiconductor Manufacturing Chemical Market represents a positive shift towards a more sustainable and resilient industry.

- In January 2023, JSR Corporation made a significant strategic announcement regarding its subsidiary, JSR Electronic Materials Korea. The corporation disclosed its intention to acquire additional shares of JSR Electronic Materials Korea Co., Ltd. (JEMK), aiming to attain complete ownership of JEMK as a wholly owned subsidiary within the JSR Corporation's portfolio. Notably, JEMK currently serves as the sales agent and distributor for JSR’s Electronic Materials business operations in Korea.

- In November 2022, BASF achieved a notable milestone with the inauguration of a state-of-the-art Research and Development (R&D) facility in Ansan, South Korea, known as the Engineering Plastics Innovation Center (EPIC). This cutting-edge facility serves as the central hub for BASF’s R&D initiatives, integrating expertise acquired through the recent acquisition of Solvay’s polyamide business, along with other innovative capabilities. Additionally, the facility hosts a dedicated Consumer Electronics Competency Center (CECC), underscoring BASF's commitment to advancing innovation in the consumer electronics sector.

Global Semiconductor Manufacturing Chemical Market Scope:

|

Semiconductor Manufacturing Chemical Market |

|

|

Market Size in 2025 |

USD 14.44 Bn. |

|

Market Size in 2032 |

USD 26.09 Bn. |

|

CAGR (2026-2032) |

8.82% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Type Acid and Base Chemicals Adhesives Solvents High-Performance Polymers |

|

|

By Application Cleaning Chemicals Etching Chemicals Photoresist Chemical Deposition Chemicals Others |

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Leading Semiconductor Manufacturing Chemical manufacturers include

- BASF SE - Germany

- LG Chem Ltd - South Korea

- Indium Corporation - United States

- Showa Denko Materials Co., Ltd (Showa Denko K.K) - Japan

- KYOCERA Corporation - Japan

- Henkel AG & Company KGAA - Germany

- Sumitomo Chemical Co., Ltd - Japan

- Dow Chemical Co. (Dow Inc.) - United States

- International Quantum Epitaxy PLC - United Kingdom

- Nichia Corporation - Japan

- CAPLINQ Europe BV - Netherlands

- ShinEtsu Microsi (Shin-Etsu Chemical Co., Ltd) - Japan

- Air Liquide - France

- Linde Group - Ireland (formerly Germany)

- Merck KGaA - Germany

- Hitachi Chemical Co., Ltd - Japan

- JSR Corporation - Japan

- DuPont Electronics & Industrial - United States

- Entegris - United States

- SUMCO Corporation - Japan

- GlobalWafers Co., Ltd - Taiwan

- Siltronic AG - Germany

- SK Siltron - South Korea

Frequently Asked Questions

Semiconductor manufacturing chemicals find widespread applications in various stages of semiconductor device fabrication. Some common applications include Cleaning, Etching, Photoresist and others.

The increasing demand for semiconductors across various industries, including consumer electronics, automotive, healthcare, and telecommunications, is a primary driver of market growth.

The CAGR of Semiconductor Manufacturing Chemical Market over 2026-2032 is 8.82%.

The Asia-Pacific region is experiencing the fastest growth in the Semiconductor Manufacturing Chemical market, driven by its prominent semiconductor manufacturing hubs and increasing demand for electronic devices, followed by North America and Europe.

1. Semiconductor Manufacturing Chemical Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Assumptions

2. Semiconductor Manufacturing Chemical Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Semiconductor Manufacturing Chemical Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

3.5. Semiconductor Manufacturing Chemical Industry Ecosystem

3.5.1. Ecosystem Analysis

3.5.2. Role of the Companies in the Ecosystem

4. Semiconductor Manufacturing Chemical Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape

4.10.1. Market Regulation by Region

4.10.1.1. North America

4.10.1.2. Europe

4.10.1.3. Asia Pacific

4.10.1.4. Middle East and Africa

4.10.1.5. South America

4.10.2. Impact of Regulations on Market Dynamics

4.10.3. Government Schemes and Initiatives

5. Semiconductor Manufacturing Chemical Market Size and Forecast by Segments (by Value USD Million and Volume in Tonnes)

5.1. Semiconductor Manufacturing Chemical Market Size and Forecast, By Type (2025-2032)

5.1.1. Acid and Base Chemicals

5.1.2. Adhesives

5.1.3. Solvents

5.1.4. High-Performance Polymers

5.2. Semiconductor Manufacturing Chemical Market Size and Forecast, By Application (2025-2032)

5.2.1. Cleaning Chemicals

5.2.2. Etching Chemicals

5.2.3. Photoresist Chemical

5.2.4. Deposition Chemicals

5.2.5. Others

5.3. Semiconductor Manufacturing Chemical Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Semiconductor Manufacturing Chemical Market Size and Forecast (by Value USD Million and Volume in Tonnes)

6.1. North America Semiconductor Manufacturing Chemical Market Size and Forecast, By Type (2025-2032)

6.1.1. Acid and Base Chemicals

6.1.2. Adhesives

6.1.3. Solvents

6.1.4. High-Performance Polymers

6.2. North America Semiconductor Manufacturing Chemical Market Size and Forecast, By Application (2025-2032)

6.2.1. Cleaning Chemicals

6.2.2. Etching Chemicals

6.2.3. Photoresist Chemical

6.2.4. Deposition Chemicals

6.2.5. Others

6.3. North America Semiconductor Manufacturing Chemical Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Semiconductor Manufacturing Chemical Market Size and Forecast (by Value USD Million and Volume in Tonnes)

7.1. Europe Semiconductor Manufacturing Chemical Market Size and Forecast, By Type (2025-2032)

7.2. Europe Semiconductor Manufacturing Chemical Market Size and Forecast, By Application (2025-2032)

7.3. Europe Semiconductor Manufacturing Chemical Market Size and Forecast, by Country (2025-2032)

7.3.1. UK

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Semiconductor Manufacturing Chemical Market Size and Forecast (by Value USD Million and Volume in Tonnes)

8.1. Asia Pacific Semiconductor Manufacturing Chemical Market Size and Forecast, By Type (2025-2032)

8.2. Asia Pacific Semiconductor Manufacturing Chemical Market Size and Forecast, By Application (2025-2032)

8.3. Asia Pacific Semiconductor Manufacturing Chemical Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Bangladesh

8.3.11. Pakistan

8.3.12. Rest of Asia Pacific

9. Middle East and Africa Semiconductor Manufacturing Chemical Market Size and Forecast (by Value USD Million and Volume in Tonnes)

9.1. Middle East and Africa Semiconductor Manufacturing Chemical Market Size and Forecast, By Type (2025-2032)

9.2. Middle East and Africa Semiconductor Manufacturing Chemical Market Size and Forecast, By Application (2025-2032)

9.3. Middle East and Africa Semiconductor Manufacturing Chemical Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Egypt

9.3.4. Nigeria

9.3.5. Rest of ME&A

10. South America Semiconductor Manufacturing Chemical Market Size and Forecast (by Value USD Million and Volume in Tonnes)

10.1. South America Semiconductor Manufacturing Chemical Market Size and Forecast, By Type (2025-2032)

10.2. South America Semiconductor Manufacturing Chemical Market Size and Forecast, By Application (2025-2032)

10.3. South America Semiconductor Manufacturing Chemical Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest of South America

11. Company Profile: Key players

11.1. BASF SE - Germany

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. LG Chem Ltd - South Korea

11.3. Indium Corporation - United States

11.4. Showa Denko Materials Co., Ltd (Showa Denko K.K) - Japan

11.5. KYOCERA Corporation - Japan

11.6. Henkel AG & Company KGAA - Germany

11.7. Sumitomo Chemical Co., Ltd - Japan

11.8. Dow Chemical Co. (Dow Inc.) - United States

11.9. International Quantum Epitaxy PLC - United Kingdom

11.10. Nichia Corporation - Japan

11.11. CAPLINQ Europe BV - Netherlands

11.12. ShinEtsu Microsi (Shin-Etsu Chemical Co., Ltd) - Japan

11.13. Air Liquide - France

11.14. Linde Group - Ireland (formerly Germany)

11.15. Merck KGaA - Germany

11.16. Hitachi Chemical Co., Ltd - Japan

11.17. JSR Corporation - Japan

11.18. DuPont Electronics & Industrial - United States

11.19. Entegris - United States

11.20. SUMCO Corporation - Japan

11.21. GlobalWafers Co., Ltd - Taiwan

11.22. Siltronic AG - Germany

11.23. SK Siltron - South Korea

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook