Semiconductor Foundry Market - Global Industry Overview and Forecast 2026-2034 Trends, Dynamics, Segmentation

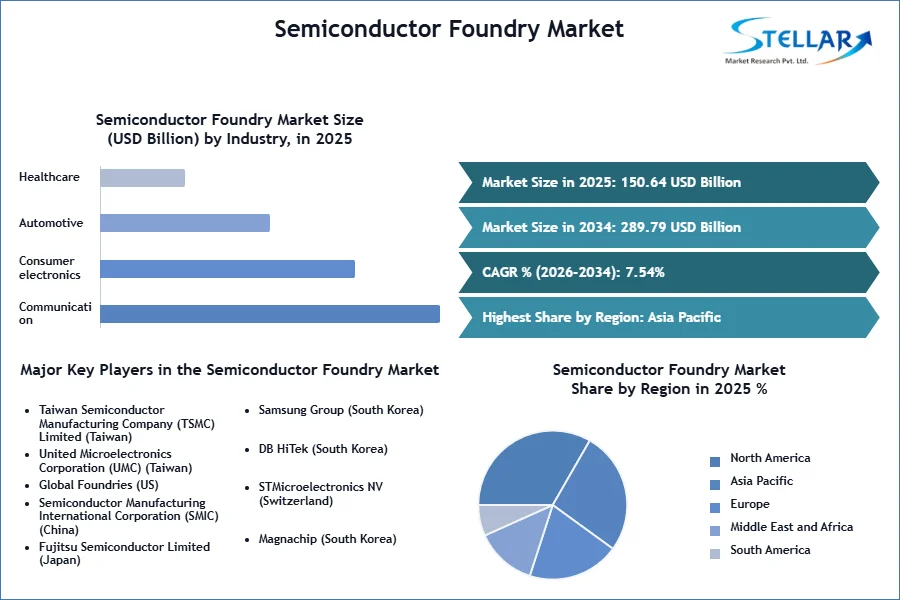

Semiconductor Foundry Market is expected to grow at a CAGR of 7.54% during the forecast period. Semiconductor Foundry Market is expected to reach USD 289.79 Bn. in 2034 from USD 150.64 Bn in 2025.

Semiconductor Foundry Market Overview:

The Semiconductor Foundry Market is studied by segments like Technology Node (10/7/5 nm, 16/14 nm, 20 nm, 45/40 nm, 65 nm, 130 nm, and others), Industry (communication, consumer electronics, automotive, healthcare, aerospace, and others) and Region (North America, Europe, Asia-Pacific, and Rest of the World). The report consists of the Trend, Forecast, Competitive Analysis, and Growth Opportunities of the market.

For the forecast period of 2026 to 2034, the report provides a complete analysis that reflects today's Semiconductor Foundry Market realities and future market prospects. To provide a comprehensive perspective of the market, the research segments and analyses it in great detail. The key data and observations offered in the study can help market participants and investors identify low-hanging fruit in the market and build growth strategies.

To get more Insights: Request Free Sample Report

The Semiconductor Foundry Market is studied by segments like Technology Node (10/7/5 nm, 16/14 nm, 20 nm, 45/40 nm, 65 nm, 130 nm, and others), Industry (communication, consumer electronics, automotive, healthcare, aerospace, and others) and Region (North America, Europe, Asia-Pacific, and Rest of the World). The report consists of the Trend, Forecast, Competitive Analysis, and Growth Opportunities of the market.

For the forecast period of 2026 to 2034, the report provides a complete analysis that reflects today's Semiconductor Foundry Market realities and future market prospects. To provide a comprehensive perspective of the market, the research segments and analyses it in great detail. The key data and observations offered in the study can help market participants and investors identify low-hanging fruit in the market and build growth strategies.

Semiconductor Foundry Market Dynamics:

Growth of Machine learning and Artificial Intelligence

The introduction of newer technologies tends to drive demand in the semiconductor market. Demand for mobile processors, for example, has fueled the development in the semiconductor foundry market, while cloud computing adoption has boosted demand for server CPUs and storage. In the recent decade, the semiconductor industry has experienced extraordinary expansion. The next growth cycle will most likely be driven by artificial intelligence. Artificial Intelligence-driven use cases are projected to spread across every industrial category over time. However, how rapidly businesses embrace AI will be determined by factors such as the amount of money invested in the technology and its development.

5G and IoT to positively impact the growth

Internet-connected devices that collect and analyze data using sensors and software will be a significant area of development for semiconductors in the coming decade. Smart factories, for example, may help you monitor shop floor activities and ensure that every equipment is running at maximum efficiency, freeing up floor space and lowering expenses. Furthermore, the emergence of smart homes allows consumers to utilize a smartphone app to control their home's lighting and appliances. IoT devices may also enable customers to remotely monitor security elements in their homes, such as if the windows are open, or if smoke is leaking.

Mobile telecommunications networks have seen significant improvements in reliability, speed, and latency since the transition to 4G and the upgrade to 5G. To acquire the data, they need from 5G, all Internet-connected devices require high-speed connections. Mobile phone manufacturers have been working on 5G phones in preparation for the future market. The need for semiconductors is predicted to rise as a result of these new, complicated phones, resulting in growth in the semiconductor foundry market.

Government Initiatives

Furthermore, governments in countries like South Korea, Taiwan, the United States, and other key foundry hubs are increasingly incentivizing and investing to increase their respective countries' industrial presence. For example, the South Korean government said in May 2021 that it expects to invest USD 451 billion in tax breaks to help chipmakers compete in the face of a serious global scarcity of crucial components. Such trends are likely to boost the individual countries' worldwide market positions.

Automotive Industry is a great driving force

Semiconductors are used in Infotainment Systems, ECUs, and Sensors, which are the primary parts among other automotive electronics components. Rising demand for a safe personal transport has helped the car sector recover. Furthermore, the demand for semiconductors has been fueled by the rise of electric and driverless automobiles.

By the end of the decade, 2030, the European Commission hopes to have around 30 million electric vehicles at least on European roads. As governments push for the adoption of electric vehicles, demand for semiconductors for features like blind-spot detection, backup cameras, and crucial connection functions has risen significantly. The advancement of ADAS or Advanced Driver Assistance Systems helps to the development of driverless vehicles, resulting in the market's expansion. The Indian Ministry of Road and Highway Transport revealed that it is working on a mandate that will require all cars to include ADAS by 2022.

Due to a scarcity of semiconductor-based electronics components, numerous automotive manufacturers are having difficulty keeping up with manufacturing schedules. Furthermore, in recent years, the shortage has been amplified by the limited capacity growth of 8-inch semiconductor manufacture. This has resulted in price rises in the short run. This scenario, combined with a considerable drop in global demand for passenger and commercial vehicles, had a negative influence on the automotive segment's revenues.

For example, due to a semiconductor shortage, Ford stated in April 2022 that its Flat Rock assembly factory outside Detroit would be shut down. GM also stated that a key pickup truck manufacturing factory outside Fort Wayne, Indiana, would be idle for two weeks in April.

Semiconductor Foundry Market Segment Analysis:

Based on the industry application, the Semiconductor Foundry market is classified into communication, consumer electronics, automotive, healthcare, aerospace, and others. In 2025, the semiconductor Foundry Market is likely to be dominated by the consumer electronics segment. Customer electronics is one of the world's fastest-growing businesses, because to rising demand for newer technologies and rapid technological advancements to meet consumer needs. Companies have been focused on building high-performing, easy-to-use products in response to rising consumer demand.

Based on technology node, the semiconductor foundry market has been divided into 10/7/5 nm, 16/14 nm, 20 nm, 45/40 nm, 65 nm, 130 nm, and others. The 130 nm technology node, especially, dominated the market in 2025, and it is expected to continue to do so throughout the review period. This is because the nodes with a 130 nm technology have a longer life and a lower cost structure.

Semiconductor Foundry Market Regional Insights:

Based on region, the Asia Pacific region has the largest share of semiconductor foundries in the world, with significant businesses such as TSMC and Samsung Electronics, based there. Taiwan, Japan, South Korea, and China are the most important countries, each with a large market share.

China has set a high bar for itself in the semiconductor industry. The country is strengthening its domestic IC business and expects to produce more chips with the help of USD 150 billion in funding. Greater China is a geopolitical hotspot that includes Hong Kong, China, and Taiwan. The trade war between the United States and China is increasing tensions in an area where all of the top process technology is concentrated, prompting many Chinese firms to invest in such semiconductor foundries.

Newly registered chip-related enterprises in China have more than quadrupled in the first 5 months of 2025 compared to the same period last year, indicating that the government is putting out every effort to achieve semiconductor self-sufficiency, despite the country's heavy reliance on imports and technologies of the US to meet domestic demand. According to the Qichacha, China saw 15,700 new enterprises from January to May 2024, doing everything from designing to producing chips.

To understand the Semiconductor Foundry Market and study the market trends. Focusing on the regional Semiconductor Foundry market, knowing the drivers and challenges of the same. Understanding the market segment geographically to gauge the growth potential.

The report includes analytical models like the Porter’s Five Forces, which helps in understanding the operating environment of the competition in the Semiconductor Foundry Market and thereby study the stakeholders to derive an efficient strategy; and PESTLE Analysis to gain a macro perspective of the Semiconductor Foundry Market in terms of political aspects like Government stability, policies, trade regulation and economic aspects like market trends, taxes and inflation. It also provides the effect of environmental factors and influence of social and legal aspects on the Semiconductor Foundry Market.

Semiconductor Foundry Market Scope:

|

Semiconductor Foundry Market |

|

|

Market Size in 2025 |

USD 150.64 Bn. |

|

Market Size in 2034 |

USD 289.79 Bn. |

|

CAGR (2026-2034) |

7.5% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segment Scope |

By Technology Node

|

|

by Industry

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Semiconductor Foundry Market Key Players:

- Taiwan Semiconductor Manufacturing Company (TSMC) Limited (Taiwan)

- United Microelectronics Corporation (UMC) (Taiwan)

- Global Foundries (US)

- Semiconductor Manufacturing International Corporation (SMIC) (China)

- Fujitsu Semiconductor Limited (Japan)

- Samsung Group (South Korea)

- DB HiTek (South Korea)

- STMicroelectronics NV (Switzerland)

- Magnachip (South Korea)

- TowerJazz (Tower Semiconductor Limited) (Israel)

- HH Grace (China)

- Vanguard International Semiconductor Corporation (Taiwan)

- United Microelectronics Corporation (Taiwan)

- X-FAB Silicon Foundries (Germany), Magnachip (South Korea)

- Powerchip Semiconductor Manufacturing Corp. (Taiwan)

Frequently Asked Questions

The APAC region is expected to hold the highest share in the Semiconductor Foundry Market.

The market size of the Semiconductor Foundry Market is expected to reach 289.79 Bn by 2034.

The forecast period for the Semiconductor Foundry Market is 2026-2034.

The market size of the Semiconductor Foundry Market in 2025 was 150.64 Bn.

1. Semiconductor Foundry Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market breakdown and Data Triangulation

1.4. Research Assumptions

2. Semiconductor Foundry Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2034) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Semiconductor Foundry Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovations

4. Semiconductor Foundry Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

Regulatory Landscape

4.8.1. Market Regulation by Region

4.8.1.1. North America

4.8.1.2. Europe

4.8.1.3. Asia Pacific

4.8.1.4. Middle East and Africa

4.8.1.5. South America

4.8.2. Impact of Regulations on Market Dynamics

4.8.3. Government Schemes and Initiatives

5. Semiconductor Foundry Market Size and Forecast by Segments (by Value USD Billion)

5.1. Semiconductor Foundry Market Size and Forecast, By Technology Node (2026-2034)

5.1.1. 10/7/5 nm

5.1.2. 16/14 nm

5.1.3. 20 nm

5.1.4. 45/40 nm

5.1.5. 65 nm

5.1.6. 130 nm

5.1.7. Others

5.2. Semiconductor Foundry Market Size and Forecast, By Industry (2026-2034)

5.2.1. Communication

5.2.2. Consumer electronics

5.2.3. Automotive

5.2.4. Healthcare

5.2.5. Aerospace

5.2.6. Others

5.3. Semiconductor Foundry Market Size and Forecast, by Region (2026-2034)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Semiconductor Foundry Market Size and Forecast (by Value USD Billion)

6.1. North America Semiconductor Foundry Market Size and Forecast, By Technology Node (2026-2034)

6.1.1. 10/7/5 nm

6.1.2. 16/14 nm

6.1.3. 20 nm

6.1.4. 45/40 nm

6.1.5. 65 nm

6.1.6. 130 nm

6.1.7. Others

6.2. North America Semiconductor Foundry Market Size and Forecast, By Industry (2026-2034)

6.2.1. Communication

6.2.2. Consumer electronics

6.2.3. Automotive

6.2.4. Healthcare

6.2.5. Aerospace

6.2.6. Others

6.3. North America Semiconductor Foundry Market Size and Forecast, by Country (2026-2034)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Semiconductor Foundry Market Size and Forecast (by Value USD Billion)

7.1. Europe Semiconductor Foundry Market Size and Forecast, By Technology Node (2026-2034)

7.2. Europe Semiconductor Foundry Market Size and Forecast, By Industry (2026-2034)

7.3. Europe Semiconductor Foundry Market Size and Forecast, by Country (2026-2034)

7.3.1. UK

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Semiconductor Foundry Market Size and Forecast (by Value USD Billion)

8.1. Asia Pacific Semiconductor Foundry Market Size and Forecast, By Technology Node (2026-2034)

8.2. Asia Pacific Semiconductor Foundry Market Size and Forecast, By Industry (2026-2034)

8.3. Asia Pacific Semiconductor Foundry Market Size and Forecast, by Country (2026-2034)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Bangladesh

8.3.11. Pakistan

8.3.12. Rest of Asia Pacific

9. Middle East and Africa Semiconductor Foundry Market Size and Forecast (by Value USD Billion)

9.1. Middle East and Africa Semiconductor Foundry Market Size and Forecast, By Technology Node (2026-2034)

9.2. Middle East and Africa Semiconductor Foundry Market Size and Forecast, By Industry (2026-2034)

9.3. Middle East and Africa Semiconductor Foundry Market Size and Forecast, by Country (2026-2034)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Egypt

9.3.4. Nigeria

9.3.5. Rest of ME&A

10. South America Semiconductor Foundry Market Size and Forecast (by Value USD Billion)

10.1. South America Semiconductor Foundry Market Size and Forecast, By Technology Node (2026-2034)

10.2. South America Semiconductor Foundry Market Size and Forecast, By Industry (2026-2034)

10.3. South America Semiconductor Foundry Market Size and Forecast, by Country (2026-2034)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest of South America

11. Company Profile: Key players

11.1. Taiwan Semiconductor Manufacturing Company (TSMC) Limited (Taiwan)

11.1.1. Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. United Microelectronics Corporation (UMC) (Taiwan)

11.3. Global Foundries (US)

11.4. Semiconductor Manufacturing International Corporation (SMIC) (China)

11.5. Fujitsu Semiconductor Limited (Japan)

11.6. Samsung Group (South Korea)

11.7. DB HiTek (South Korea)

11.8. STMicroelectronics NV (Switzerland)

11.9. Magnachip (South Korea)

11.10. TowerJazz (Tower Semiconductor Limited) (Israel)

11.11. HH Grace (China)

11.12. Vanguard International Semiconductor Corporation (Taiwan)

11.13. United Microelectronics Corporation (Taiwan)

11.14. X-FAB Silicon Foundries (Germany), Magnachip (South Korea)

11.15. Powerchip Semiconductor Manufacturing Corp. (Taiwan)

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook