Sales Force Automation Market - Global Industry Analysis and Forecast 2026-2034

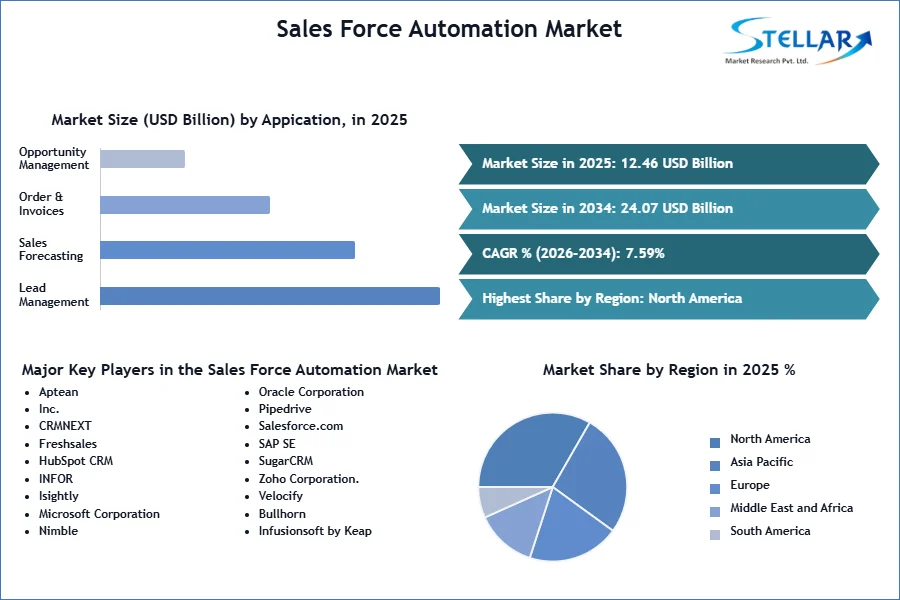

The Sales Force Automation Market size was valued at USD 12.46 Bn. in 2025 and the total Global Sales Force Automation revenue is expected to grow at a CAGR of 7.59% from 2026 to 2034, reaching nearly USD 24.07 Bn. by 2034.

Sales Force Automation Market Overview

Sales Force Automation (SFA) refers to the use of software and technology to streamline and automate sales-related tasks, such as customer contact management, opportunity tracking, order processing, and forecasting. The report provides a comprehensive analysis of current market trends, challenges, and opportunities, focusing on critical segments and regional dynamics. It highlights key insights into Sales Force Automation market trends, identifies potential challenges, and explores growth opportunities across different segments and regions. Salesforce has undergone a significant transformation by restructuring for both short and long-term goals, aiming to increase productivity, profitability, and operational efficiency.

They are intensifying efforts in innovation, enhancing core products, and embedding AI and data into their CRM platform. Also, Salesforce is prioritizing strengthening customer relationships and raising deeper connections with both stockholders and customers the same. These strategic initiatives underscore Salesforce's commitment to maintaining leadership in the CRM industry and harnessing technological advancements to better serve its clientele. The demand for Sales Force Automation (SFA) is set to experience significant growth as businesses prioritize digital transformation and integrate AI into customer relationship management.

Across industries, companies are expected to adopt AI-driven solutions to streamline sales processes and enhance customer engagement, driving Sales Force Automation Industry growth. Projected growth in the Sales Force Automation market underscores a sustained upward trend, driven by the rising adoption of advanced analytics, automation, and improvements in sales efficiency. The trend signifies a strategic move towards leveraging technology to optimize sales operations and deliver tailored customer experiences, cementing SFA's role as a crucial component of modern business strategies.

Salesforce Automation Market Revenue Insights Cover in the SMR Report:

- Over 154,000 businesses utilize Salesforce's services.

- Salesforce commands a 23.8% share of the CRM market, surpassing the combined market share of its top four competitors.

- The company employs 75,687 individuals worldwide.

To get more Insights: Request Free Sample Report

Sales Force Automation Market Dynamics

Need for Operational Efficiency and Productivity

Sales Force Automation (SFA) systems significantly reduce the time sales representatives spend on repetitive tasks like data entry, scheduling meetings, and sending follow-up emails. The automation allows sales teams to focus more on strategic activities such as engaging with customers and closing deals. Automating these tasks not only enhances productivity but also reduces human errors, ensuring data accuracy and consistency. Sales representatives typically spend around 64% of their time on non-revenue-generating tasks but with the implementation of Sales Force Automation (SFA) tools, that reduced to approximately 34%.

The shift allows significantly more time for actual selling activities. Companies adopting SFA systems report up to a 20% reduction in administrative costs, leading to substantial cost savings. Additionally, businesses utilizing SFA tools see an average increase of 10-15% in sales productivity. The increase is due to more efficient task management and a greater focus on core sales activities, enhancing overall performance and revenue generation.

- Companies using SFA systems experienced a 14.5% increase in sales productivity and a 12.5% reduction in sales cycle time.

- Between 2018 and 2023, the implementation of streamlined sales processes through SFA led to an average sales cycle reduction of 15-20%.

- According to an SMR study, 67% of companies reported improved decision-making capabilities after implementing SFA performance-tracking features.

Integration of AI and Machine Learning

AI and ML integration in SFA systems enhances predictive analytics and sales forecasting by analyzing historical sales data with precision, enabling businesses to forecast sales, optimize inventory, and anticipate customer needs effectively. These systems also personalize customer interactions by analyzing preferences and behavior and tailoring marketing messages and sales pitches to enhance engagement and retention. Real-time data processing by AI-driven SFA systems provides actionable insights that aid strategic decision-making, helping sales managers identify promising leads, prioritize Sales Force Automation opportunities, and allocate resources efficiently. The technological advancement significantly increases overall sales performance by improving efficiency, accuracy, and customer satisfaction in the competitive market landscape.

Businesses utilizing AI-powered SFA tools have witnessed significant gains in efficiency. According to SMR Analysis companies integrating AI into sales operations reported a 15% increase in productivity and a 30% decrease in sales cycle times between 2019 and 2024. The improvement underscores AI's role in streamlining processes and enhancing operational speed within sales teams. Also, personalized customer interactions driven by AI have led to increased customer satisfaction rates. Harvard Business Review highlighted that businesses adopting AI-driven customer insights observed a 15% enhancement in customer satisfaction metrics during the same period, highlighting AI's impact on adopting stronger customer relationships and loyalty.

Operational Challenges and Solutions in Switching SFA Vendors

Dependence on a single vendor for Sales Force Automation (SFA) solutions poses significant risks. If the vendor faces financial instability, shifts its business strategy, or discontinues support for the product, the client company may experience disruption. Vendor lock-in can make it challenging to switch to another provider without incurring high costs and operational disruptions. The dependencies also limit the flexibility to adapt to new Sales Force Automation technologies or market demands, as businesses are bound to the vendor’s roadmap and capabilities. From 2019 to 2024, concerns about vendor lock-in prompted 74% of companies to express apprehension when considering new IT solutions, including SFA systems.

In 2024 60% of businesses faced difficulties switching SFA vendors due to high costs and operational disruptions. As a result, the adoption of multi-vendor strategies increased by 25%. Service reliability was also a major issue, with a 2020 Salesforce study revealing that 45% of businesses experienced significant downtime annually, impacting sales performance. SMR Analysis, showed that reliable SFA systems led to a 20% increase in sales productivity and a 15% improvement in customer satisfaction, driving a 30% increase in high-uptime SFA solution adoption.

Sales Force Automation Market Segment Analysis

By Deployment, Cloud-based Sales Force Automation (SFA) solutions have seen remarkable growth over the past few years. In 2024, cloud-based SFA systems accounted for 70% of the Sales Force Automation market share, a significant increase from about 50% in 2024. Cloud-based SFA systems offer unparalleled scalability, enabling businesses to adjust resources easily based on current demands, which is ideal for dynamic environments. They help reduce upfront investments in hardware and IT infrastructure by leveraging a cost-efficient subscription-based model, beneficial for SMEs with limited capital.

The accessibility of these systems allows sales teams to access data from anywhere, facilitating remote work and boosting productivity. Rapid deployment and regular updates from cloud providers ensure minimal downtime and constant access to the latest features, security enhancements, and compliance updates, making cloud-based solutions highly efficient and adaptable.

Sales Force Automation Market Regional Insights

The Sales Force Automation market in North America has seen significant growth in 2024 because of the region's advanced technological infrastructure and high adoption rates of digital solutions among businesses. North America leads in technological innovation, particularly in AI, ML, and cloud computing. The integration of these technologies into Sales Force Automation (SFA) tools enhances capabilities like predictive analytics and automation, driving Sales Force Automation market growth. North American businesses prioritize customer relationship management and digital transformation, driving a strong demand for SFA solutions to streamline sales processes and enhance customer experiences. The stable economic environment in North America supports investments in advanced software solutions.

Companies are increasingly willing to invest in SFA tools to maintain a competitive edge. Major Sales Force Automation suppliers like Salesforce have introduced AI-powered features such as Einstein Analytics, offering advanced analytics and automation capabilities that improve sales efficiency and provide deeper insights. There is a significant shift towards cloud-based SFA solutions due to their scalability, flexibility, and lower upfront costs, with companies like Microsoft and Oracle expanding their offerings to meet the Sales Force Automation Market demand. Also, small and medium-sized enterprises (SMEs) are increasingly adopting SFA tools to enhance their sales processes, contributing to the overall growth of the Sales Force Automation Industry in North America.

Sales Force Automation Market Competitive Landscape

The Sales Force Automation market is highly competitive, featuring numerous key players offering a variety of products and services. Salesforce introduced Einstein Analytics, an AI-powered platform integrated with its Sales Force Automation tools, enhancing businesses' ability to gain actionable insights from sales data, automate routine tasks, and improve decision-making.

This solidifies Salesforce’s leadership in the Sales Force Automation market by leveraging advanced AI and machine learning. Similarly, Microsoft launched Dynamics 365 Sales Insights, which utilizes AI for predictive analytics, lead scoring, and relationship analytics. The product helps sales teams forecast trends and identify high-potential leads, thereby improving sales outcomes. Seamlessly integrating with other Microsoft products, it offers a comprehensive solution for businesses within the Microsoft ecosystem.

Both Salesforce and Microsoft hold strong positions in the Sales Force Automation market. Salesforce, with its comprehensive suite and early AI adoption, remains a leader, while Microsoft offers a compelling alternative with its extensive product ecosystem, particularly appealing to enterprises already using its software. Salesforce's Einstein Analytics provides highly customizable, advanced AI-driven insights, ideal for deep analytics integration. Conversely, Microsoft’s Dynamics 365 Sales Insights focuses on predictive analytics and seamless integration with existing Microsoft products. Salesforce appreciates broader adoption across various industries due to its extensive capabilities, but Microsoft is rapidly gaining traction, especially among enterprises utilizing other Microsoft services.

- March 2024: Salesforce announced the general availability of Pro Suite, a scalable, flexible, complete offering to assist small businesses with AI CRM. Pro Suite enables advanced customization and features, such as sales forecasting and quoting, workflow and process automation, and live chat for customer service.

- August 2023: Botree Software launched a dynamic upgrade to its Sales Force Automation (SFA) app. The solution has been designed to develop sales operations and overall revenue productivity for brands across consumer durables, FMCG, and OTC pharma.

The Sales Force Automation (SFA) market is poised for substantial growth driven by digital transformation and the integration of AI technologies. Salesforce and Microsoft lead the market with innovative solutions like Einstein Analytics and Dynamics 365 Sales Insights, respectively, which enhance sales efficiency and customer engagement through advanced analytics and automation. The North American region, a hub of technological innovation, plays a pivotal role in the Sales Force Automation market growth due to its robust infrastructure and high adoption rates of digital solutions.

Cloud-based SFA systems are increasingly favored for their scalability and cost-efficiency, catering to diverse business needs across industries. As businesses prioritize operational efficiency and customer-centric strategies, SFA continues to evolve as a critical component of modern sales strategies, promising continued growth and innovation in the years ahead.

|

Sales Force Automation Market Scope |

|

|

Market Size in 2025 |

USD 12.46 Bn. |

|

Market Size in 2034 |

USD 24.07 Bn. |

|

CAGR (2026-2034) |

7.59% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Deployment Cloud On-premise |

|

By Enterprise Size Outlook Large Enterprises SMEs |

|

|

|

By End-use BFSI Retail Healthcare Telecom Manufacturing Automotive Media & Entertainment Others |

|

|

By Application Lead Management Sales Forecasting Order & Invoices Management Opportunity Management Others |

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Sales Force Automation Market

- Aptean, Inc.

- CRMNEXT

- Freshsales

- HubSpot CRM

- INFOR, INC.

- Isightly

- Microsoft Corporation

- Nimble

- Oracle Corporation

- Pipedrive

- Salesforce.com, Inc.,

- SAP SE

- SugarCRM

- Zoho Corporation.

- Velocify

- Bullhorn

- Infusionsoft by Keap

- SAP SE

- Bpm'online.

- Other.

Frequently Asked Questions

SFA is important because it helps sales teams automate repetitive tasks, reduce administrative burdens, improve data accuracy, and focus more on strategic activities like customer engagement and closing deals. It also enhances productivity and sales effectiveness.

Businesses should consider factors such as their specific sales processes, integration with existing systems, scalability, user-friendliness, vendor reliability, security features, and customer support when choosing an SFA system.

The Market size was valued at USD 12.46 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 7.59% from 2026 to 2034, reaching nearly 24.07 billion.

The segments covered in the market report are by Deployment, Enterprise Size Outlook Product Type, End-use and Application.

1. Sales Force Automation Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Assumptions

2. Sales Force Automation Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2034) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Sales Force Automation Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Developments and Innovations

4. Sales Force Automation Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape

4.9.1. Market Regulation by Region

4.9.1.1. North America

4.9.1.2. Europe

4.9.1.3. Asia Pacific

4.9.1.4. Middle East and Africa

4.9.1.5. South America

4.9.2. Impact of Regulations on Market Dynamics

5. Sales Force Automation Market Size and Forecast by Segments (by Value USD Million)

5.1. Asset Tracking Market Size and Forecast, By Deployment (2026-2034)

5.1.1. Cloud

5.1.2. On-premise

5.2. Asset Tracking Market Size and Forecast, By Enterprise Size Outlook (2026-2034)

5.2.1. Large Enterprises

5.2.2. SMEs

5.3. Asset Tracking Market Size and Forecast, By End-Use (2026-2034)

5.3.1. BFSI

5.3.2. Retail

5.3.3. Healthcare

5.3.4. Telecom

5.3.5. Manufacturing

5.3.6. Automotive

5.3.7. Media & Entertainment

5.3.8. Others

5.4. Asset Tracking Market Size and Forecast, By Application (2026-2034)

5.4.1. Lead Management

5.4.2. Sales Forecasting

5.4.3. Order & Invoices Management

5.4.4. Opportunity Management

5.4.5. Others

5.5. Asset Tracking Market Size and Forecast, by Region (2026-2034)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Sales Force Automation Market Size and Forecast (by Value USD Million)

6.1. North America Asset Tracking Market Size and Forecast, By Deployment (2026-2034)

6.1.1. Cloud

6.1.2. On-premise

6.2. North America Asset Tracking Market Size and Forecast, By Enterprise Size Outlook (2026-2034)

6.2.1. Large Enterprises

6.2.2. SMEs

6.3. North America Asset Tracking Market Size and Forecast, By End-Use (2026-2034)

6.3.1. BFSI

6.3.2. Retail

6.3.3. Healthcare

6.3.4. Telecom

6.3.5. Manufacturing

6.3.6. Automotive

6.3.7. Media & Entertainment

6.3.8. Others

6.4. North America Asset Tracking Market Size and Forecast, By Application (2026-2034)

6.4.1. Lead Management

6.4.2. Sales Forecasting

6.4.3. Order & Invoices Management

6.4.4. Opportunity Management

6.4.5. Others

6.5. North America Sales Force Automation Market Size and Forecast, by Country (2026-2034)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Sales Force Automation Market Size and Forecast (by Value USD Million)

7.1. Europe Asset Tracking Market Size and Forecast, By Deployment (2026-2034)

7.2. Europe Asset Tracking Market Size and Forecast, By Enterprise Size Outlook (2026-2034)

7.3. Europe Asset Tracking Market Size and Forecast, By End-Use (2026-2034)

7.4. Europe Asset Tracking Market Size and Forecast, By Application (2026-2034)

7.5. Europe Sales Force Automation Market Size and Forecast, by Country (2026-2034)

7.5.1. UK

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Austria

7.5.8. Rest of Europe

8. Asia Pacific Sales Force Automation Market Size and Forecast (by Value USD Million)

8.1. Asia Pacific Asset Tracking Market Size and Forecast, By Deployment (2026-2034)

8.2. Asia Pacific Asset Tracking Market Size and Forecast, By Enterprise Size Outlook (2026-2034)

8.3. Asia Pacific Asset Tracking Market Size and Forecast, By End-Use (2026-2034)

8.4. Asia Pacific Asset Tracking Market Size and Forecast, By Application (2026-2034)

8.5. Asia Pacific Sales Force Automation Market Size and Forecast, by Country (2026-2034)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. Indonesia

8.5.7. Malaysia

8.5.8. Vietnam

8.5.9. Taiwan

8.5.10. Bangladesh

8.5.11. Pakistan

8.5.12. Rest of Asia Pacific

9. Middle East and Africa Sales Force Automation Market Size and Forecast (by Value USD Million)

9.1. Middle East and Africa Asset Tracking Market Size and Forecast, By Deployment (2026-2034)

9.2. Middle East and Africa Asset Tracking Market Size and Forecast, By Enterprise Size Outlook (2026-2034)

9.3. Middle East and Africa Asset Tracking Market Size and Forecast, By End-Use (2026-2034)

9.4. Middle East and Africa Asset Tracking Market Size and Forecast, By Application (2026-2034)

9.5. Middle East and Africa Sales Force Automation Market Size and Forecast, by Country (2026-2034)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Egypt

9.5.4. Nigeria

9.5.5. Rest of ME&A

10. South America Sales Force Automation Market Size and Forecast (by Value USD Million)

10.1. South America Asset Tracking Market Size and Forecast, By Deployment (2026-2034)

10.2. South America Asset Tracking Market Size and Forecast, By Enterprise Size Outlook (2026-2034)

10.3. South America Asset Tracking Market Size and Forecast, By End-Use (2026-2034)

10.4. South America Asset Tracking Market Size and Forecast, By Application (2026-2034)

10.5. South America Sales Force Automation Market Size and Forecast, by Country (2026-2034)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest of South America

11. Company Profile: Key players

11.1. Aptean, Inc.

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.2.1. Service Name

11.1.2.2. Service Details

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. CRMNEXT

11.3. Freshsales

11.4. HubSpot CRM

11.5. INFOR, INC.

11.6. Isightly

11.7. Microsoft Corporation

11.8. Nimble

11.9. Oracle Corporation

11.10. Pipedrive

11.11. Salesforce.com, Inc.,

11.12. SAP SE

11.13. SugarCRM

11.14. Zoho Corporation.

11.15. Velocify

11.16. Bullhorn

11.17. Infusionsoft by Keap

11.18. SAP SE

11.19. Bpm'online.

11.20. Other.

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook