SUV Market Industry Analysis and Forecast (2026-2032)

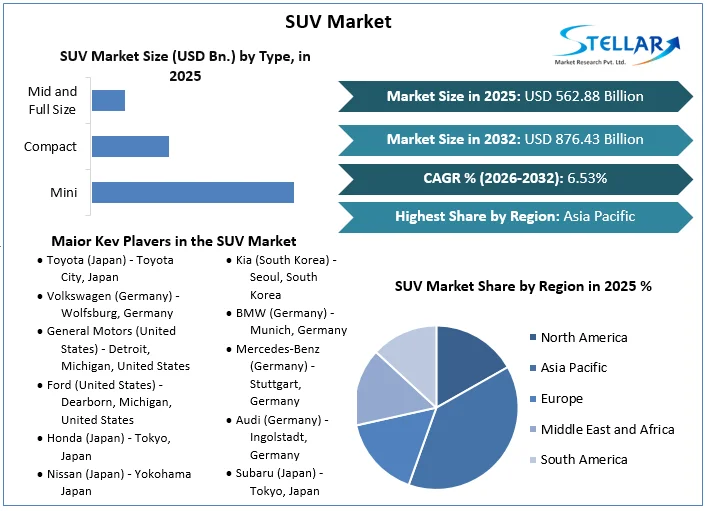

SUV Market size was valued at USD 562.88 Billion in 2025 and the total SUV revenue is expected to grow at a CAGR of 6.53% from 2026 to 2032, reaching nearly USD 876.43 Billion by 2032.

SUV Market Overview

A sport utility vehicle is a car classification that combines elements of road-going passenger cars with features from off-road vehicles, such as raised ground clearance and four-wheel drive.

The SUV report offers a detailed analysis supported by dependable statistics on trade and profit by players for the period 2020- 2025. The report also includes company description, major business, SUV product preface, recent developments, and SUV deals by region, type, operation, and deals channel. The global SUV Market is divided in the report to better grasp the market, which includes profiles of the competitive landscape and their market values. The report also covers technology trends and SUV development. The report assists Automotive companies, as well as new entrants and industry chain companies in the market, by supplying revenue data for the whole market and different sub-segments based on company, product type, application, and regions.

SUVs have become a popular choice of vehicle, across the globe. SUVs are preferred more owing to their commanding stance and strong road presence when compared to other types of vehicles such as sedans or hatchbacks. The SUV market is experiencing a surge in demand owing to customer preferences for versatile and spacious vehicles, trends towards compact and electric SUVs, local special circumstances in different regions, and underlying macroeconomic factors. As these factors continue to evolve, the SUV market is likely to see further growth and development during the forecast years.

- SUVs propel India to 3rd largest car market in the world in FY24

- Car, and SUV sales up 27%, and volumes hit the highest ever in the domestic market

To get more Insights: Request Free Sample Report

SUV Market Dynamics

The Rise and Evolution of SUVs in Automotive Market

Sport Utility Vehicles (SUVs) have become increasingly popular thanks to their versatility and adaptability in meeting various consumer needs. The popularity of these vehicles is still strong as SUVs offer many benefits, making them an ideal choice for many car buyers. It provides ample space, all-weather capability, towing capability, safety features, and a higher driving position has propelled the market growth. These vehicles are designed to blend the features of both traditional cars and trucks, offering a compelling combination of spacious interiors, off-road capabilities, and often, advanced technology.

Modern SUVs have become increasingly fuel-efficient, thanks to advancements in technology and engineering resulting in higher demand. Surged SUV models that feature efficient engines, aerodynamic designs, and lightweight materials that contribute to better fuel economy have accelerated the market growth. Additionally, hybrid and electric SUV options are becoming more prevalent, offering environmentally conscious consumers the opportunity to reduce their carbon footprint without compromising on performance or utility. Economic stability and low-interest rates also encourage consumers to make big-ticket purchases, further driving the demand for SUVs.

- According to STELLAR Analysis, SUV market unit sales are expected to reach 12,580.0k vehicles in 2028.

Navigating Challenges in SUV Market

SUVs contribute more to climate change and environmental damage than smaller cars since they are often less fuel-efficient and need more resources to construct. Their danger of rollovers is further increased by their greater centre of gravity. SUVs are heavier and bigger than normal passenger cars, as it use more fuel to run resulting in hindering the market growth. The increasing prices of SUVs have led to restraint the market growth. The increased height and weight of SUVs have led to challenges in safety risks to smaller vehicles and pedestrians in a collision. It has led to strict safety standards for SUVs.

Emerging Trends in the SUV Market

The popularity of compact SUVs is one of the major trends in the SUV industry. These more compact SUVs are gaining popularity because it provide all the features of an SUV but in a more manageable and economical package. Urbanites who appreciate an SUV's adaptability and practicality but need a car that's simple to park and through crowded city streets are drawn to compact SUVs. An additional development in the SUV market is the rising popularity of electric SUVs. Consumers are looking for more environmentally friendly alternatives to conventional gasoline-powered vehicles as environmental concerns gain traction. The advantages of an SUV are combined with lower carbon emissions in electric vehicles. The popularity of electric SUVs has increased due to the practicality and affordability of these vehicles brought about by advancements in battery technology.

SUV Market Segment Analysis

Based on Type, the Compact SUV segment held the largest market share with increasing CAGR through the forecast period. Compared to traditional vehicles, Compact SUVs usually have a unibody structure, unlike traditional SUV which has a body-on-frame design. The design of the Compact SUV ensures better handling on the road, reminiscent of a car's agility that has boosted the market demand. The unibody construction resists twisting during turns, delivering superior on-road performance. With available all-wheel drive, compact SUVs excel in adverse weather conditions, providing excellent road grip. The Unibody design provides crumple zones that enhance safety during frontal impacts. The unique combination makes compact SUVs among the safest choices on the road, offering both protection and peace of mind.

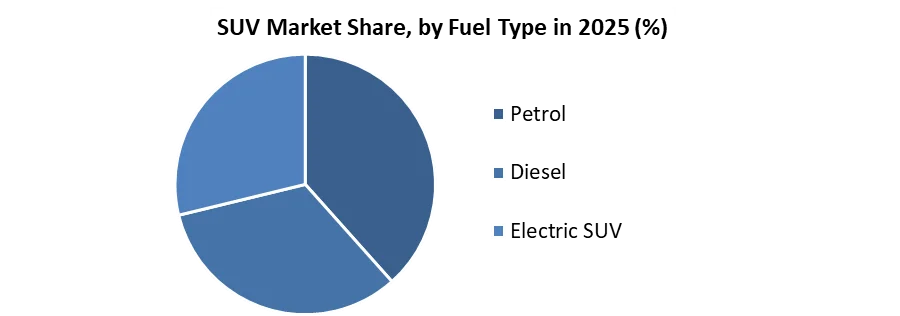

Based on Fuel type, the Diesel segment held the highest share in 2025 and is expected to dominate the market through the forecast period. SUV buyer’s preference for diesel owing to power and mileage contributed to diesel cars constituting 39.2% of total vehicle sales in 2025. Diesel engines have a higher compression ratio than gasoline engines, which reduces the wear and tear on the engine, as well as the use of lubricating oil. Diesel engines are also capable of burning a wider range of fuel types, including biodiesel and renewable diesel. These alternative fuels produce fewer emissions than regular diesel, making them even more eco-friendly. Diesel engines generally consume fewer litres of fuel per 100 kilometres travelled compared to gasoline engines. For instance, a diesel vehicle might consume around 6-8 litres per 100 kilometres, depending on the factors mentioned earlier.

SUV Market Regional Analysis

Asia Pacific dominated the market in 2025 and is expected to maintain the dominance till 2032 with an increasing CAGR. There is heavy investment in battery manufacturing as the demand for lithium-ion batteries is on the rise due to the growth in EVs. Additionally, companies are looking forward to hydrogen fuel cell electric vehicles. In the Asia Pacific region, there is an increase in consumer preference for sports utility vehicles.

The largest trend being driven by the increase in small and medium-sized SUVs and crossovers is the development of intelligent all-wheel drive and electrical AWD. Consumers in the APAC region select passenger automobiles equipped with AWS-type powertrain systems since it has safely operated on the road in winter or under any dangerous climatic circumstances. The market for sport utility cars is increasing more in Vietnam, Japan, China, and India. According to STELLAR Analysis, Indian companies held the most number of discussions on the SUV, followed by China, Australia, Hong Kong, Taiwan, and Japan.

SUV Market Competitive Landscape

- In 2023, Figure, a California-based company developing autonomous humanoid robots, announced that it has signed a commercial agreement with BMW Manufacturing Co., LLC to deploy general-purpose robots in automotive manufacturing environments. Under the agreement, BMW Manufacturing and Figure to pursue a milestone-based approach. In the first phase, the Figure is expected to identify initial use cases to apply the Figure robots in automotive production. Once the first phase has been completed, the Figure robots begin staged deployment at BMW's manufacturing facility in Spartanburg, South Carolina.

- In April 2024, South Korea's Hyundai Motor Group is expected to launch its first India-manufactured electric vehicles by 2025 as the parent of the Hyundai and Kia brands looks to boost its presence in the nascent space dominated by Tata Motors. Production of Hyundai's locally manufactured EVs is estimated to begin by the end of 2024 and launched by 2025, along with Kia's India-made EV, the Hyundai Motor Group said in a statement on Thursday, adding that it would unveil five models by 2030.

|

SUV Market Scope |

|

|

Market Size in 2025 |

USD 562.88 Bn. |

|

Market Size in 2032 |

USD 876.43 Bn. |

|

CAGR (2026-2032) |

6.53 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Type

|

|

By Fuel Type

|

|

|

By Price Range

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

SUV Market Key Player

- Toyota (Japan) - Toyota City, Japan

- Volkswagen (Germany) - Wolfsburg, Germany

- General Motors (United States) - Detroit, Michigan, United States

- Ford (United States) - Dearborn, Michigan, United States

- Honda (Japan) - Tokyo, Japan

- Nissan (Japan) - Yokohama, Japan

- Hyundai (South Korea) - Seoul, South Korea

- Kia (South Korea) - Seoul, South Korea

- BMW (Germany) - Munich, Germany

- Mercedes-Benz (Germany) - Stuttgart, Germany

- Audi (Germany) - Ingolstadt, Germany

- Subaru (Japan) - Tokyo, Japan

- Jeep (United States) - Toledo, Ohio, United States

- Lexus (Japan) - Nagoya, Japan

- Chevrolet (United States) - Detroit, Michigan, United States

- Land Rover (United Kingdom) - Whitley, United Kingdom

- Mitsubishi (Japan) - Tokyo, Japan

- Volvo (Sweden) - Gothenburg, Sweden

- Porsche (Germany) - Stuttgart, Germany

- GMC (United States) - Detroit, Michigan, United States

- Buick (United States) - Detroit, Michigan, United States

- Tesla (United States) - Palo Alto, California, United States

- Infiniti (Japan) - Yokohama, Japan

- Jaguar (United Kingdom) - Whitley, United Kingdom

- Dodge (United States) - Auburn Hills, Michigan, United States

Frequently Asked Questions

The popularity of compact SUVs is the trend for SUV growth.

The Market size was valued at USD 562.88 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 6.53 % from 2026 to 2032, reaching nearly USD 876.43 Billion.

The segments covered in the market report are by Type, Fuel Type, and Price Range.

1. SUV Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Assumptions

2. SUV Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. SUV Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

3.5. SUV Industry Ecosystem

3.5.1. Ecosystem Analysis

3.5.2. Role of the Companies in the Ecosystem

4. SUV Market: Dynamics

4.5. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.6. Market Drivers

4.7. Market Restraints

4.8. Market Opportunities

4.9. Market Challenges

4.10. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.11. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.12. Technological Roadmap

4.13. Value Chain Analysis and Supply Chain Analysis

4.14. Trade Analysis

4.15. Regulatory Landscape

4.15.1. Market Regulation by Region

4.15.1.1. North America

4.15.1.2. Europe

4.15.1.3. Asia Pacific

4.15.1.4. Middle East and Africa

4.15.1.5. South America

4.15.2. Impact of Regulations on Market Dynamics

4.15.3. Government Schemes and Initiatives

5. SUV Market Size and Forecast by Segments (by Value USD Million and Volume in Thousand Units)

5.5. SUV Market Size and Forecast, By Type (2025-2032)

5.5.1. Mini

5.5.2. Compact

5.5.3. Mid and Full Size

5.6. SUV Market Size and Forecast, By Fuel Type (2025-2032)

5.6.1. Petrol

5.6.2. Diesel

5.6.3. Electric SUV

5.7. SUV Market Size and Forecast, By Price Range (2025-2032)

5.7.1. Medium

5.7.2. Premium

5.8. SUV Market Size and Forecast, by Region (2025-2032)

5.8.1. North America

5.8.2. Europe

5.8.3. Asia Pacific

5.8.4. Middle East and Africa

5.8.5. South America

6. North America SUV Market Size and Forecast (by Value USD Million and Volume in Thousand Units)

6.5. North America SUV Market Size and Forecast, By Type (2025-2032)

6.5.1. Mini

6.5.2. Compact

6.5.3. Mid and Full Size

6.6. North America SUV Market Size and Forecast, By Fuel Type (2025-2032)

6.6.1. Petrol

6.6.2. Diesel

6.6.3. Electric SUV

6.7. North America SUV Market Size and Forecast, By Price Range (2025-2032)

6.7.1. Medium

6.7.2. Premium

6.8. North America SUV Market Size and Forecast, by Country (2025-2032)

6.8.1. United States

6.8.2. Canada

6.8.3. Mexico

7. Europe SUV Market Size and Forecast (by Value USD Million and Volume in Thousand Units)

7.5. Europe SUV Market Size and Forecast, By Type (2025-2032)

7.6. Europe SUV Market Size and Forecast, By Fuel Type (2025-2032)

7.7. Europe SUV Market Size and Forecast, By Price Range (2025-2032)

7.8. Europe SUV Market Size and Forecast, by Country (2025-2032)

7.8.1. UK

7.8.2. France

7.8.3. Germany

7.8.4. Italy

7.8.5. Spain

7.8.6. Sweden

7.8.7. Austria

7.8.8. Rest of Europe

8. Asia Pacific SUV Market Size and Forecast (by Value USD Million and Volume in Thousand Units)

8.5. Asia Pacific SUV Market Size and Forecast, By Type (2025-2032)

8.6. Asia Pacific SUV Market Size and Forecast, By Fuel Type (2025-2032)

8.7. Asia Pacific SUV Market Size and Forecast, By Price Range (2025-2032)

8.8. Asia Pacific SUV Market Size and Forecast, by Country (2025-2032)

8.8.1. China

8.8.2. S Korea

8.8.3. Japan

8.8.4. India

8.8.5. Australia

8.8.6. Indonesia

8.8.7. Malaysia

8.8.8. Vietnam

8.8.9. Taiwan

8.8.10. Bangladesh

8.8.11. Pakistan

8.8.12. Rest of Asia Pacific

9. Middle East and Africa SUV Market Size and Forecast (by Value USD Million and Volume in Thousand Units)

9.5. Middle East and Africa SUV Market Size and Forecast, By Type (2025-2032)

9.6. Middle East and Africa SUV Market Size and Forecast, By Fuel Type (2025-2032)

9.7. Middle East and Africa SUV Market Size and Forecast, By Price Range (2025-2032)

9.8. Middle East and Africa SUV Market Size and Forecast, by Country (2025-2032)

9.8.1. South Africa

9.8.2. GCC

9.8.3. Egypt

9.8.4. Nigeria

9.8.5. Rest of ME&A

10. South America SUV Market Size and Forecast (by Value USD Million and Volume in Thousand Units)

10.5. South America SUV Market Size and Forecast, By Type (2025-2032)

10.6. South America SUV Market Size and Forecast, By Fuel Type (2025-2032)

10.7. South America SUV Market Size and Forecast, By Price Range (2025-2032)

10.8. South America SUV Market Size and Forecast, by Country (2025-2032)

10.8.1. Brazil

10.8.2. Argentina

10.8.3. Rest of South America

11. Company Profile: Key players

11.5. Toyota (Japan) - Toyota City, Japan

11.5.1. Company Overview

11.5.2. Product Segment

11.5.2.1. Product Name

11.5.2.2. Product Details (Price, Features, etc.)

11.5.3. Financial Overview

11.5.3.1. Total Revenue

11.5.3.2. Segment Revenue

11.5.3.3. Regional Revenue

11.5.4. SWOT Analysis

11.5.5. Strategic Analysis

11.5.6. Recent Developments

11.6. Volkswagen (Germany) - Wolfsburg, Germany

11.7. General Motors (United States) - Detroit, Michigan, United States

11.8. Ford (United States) - Dearborn, Michigan, United States

11.9. Honda (Japan) - Tokyo, Japan

11.10. Nissan (Japan) - Yokohama, Japan

11.11. Hyundai (South Korea) - Seoul, South Korea

11.12. Kia (South Korea) - Seoul, South Korea

11.13. BMW (Germany) - Munich, Germany

11.14. Mercedes-Benz (Germany) - Stuttgart, Germany

11.15. Audi (Germany) - Ingolstadt, Germany

11.16. Subaru (Japan) - Tokyo, Japan

11.17. Jeep (United States) - Toledo, Ohio, United States

11.18. Lexus (Japan) - Nagoya, Japan

11.19. Chevrolet (United States) - Detroit, Michigan, United States

11.20. Land Rover (United Kingdom) - Whitley, United Kingdom

11.21. Mitsubishi (Japan) - Tokyo, Japan

11.22. Volvo (Sweden) - Gothenburg, Sweden

11.23. Porsche (Germany) - Stuttgart, Germany

11.24. GMC (United States) - Detroit, Michigan, United States

11.25. Buick (United States) - Detroit, Michigan, United States

11.26. Tesla (United States) - Palo Alto, California, United States

11.27. Infiniti (Japan) - Yokohama, Japan

11.28. Jaguar (United Kingdom) - Whitley, United Kingdom

11.29. Dodge (United States) - Auburn Hills, Michigan, United States

11.30. XXX

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook