Proteases Market Global Industry Analysis and Forecast (2026-2032)

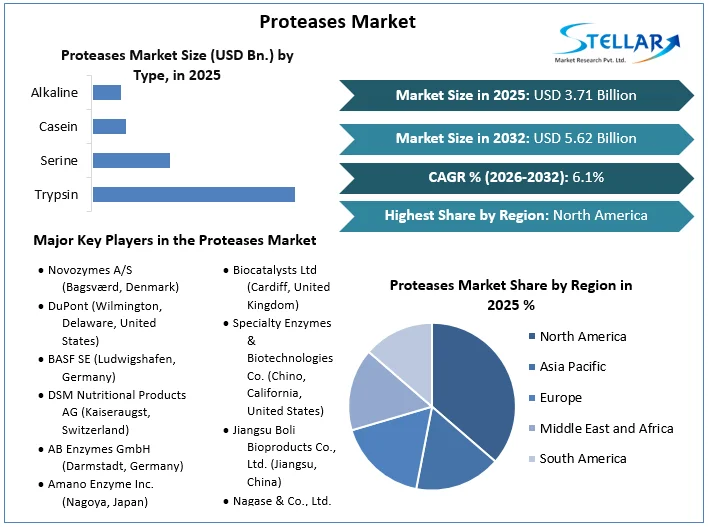

Global Proteases Market size was valued at USD 3.71 Bn. in 2025 and is expected to reach USD 5.62 Bn. by 2032, at a CAGR of 6.1%.

Proteases Market Overview

Proteases, also known as proteolytic enzymes or proteinases, are enzymes that catalyze the hydrolysis of peptide bonds in proteins, leading to the breakdown of proteins into smaller polypeptides or amino acids. The proteases market is driven by their extensive applications across several industries including food and beverages, pharmaceuticals, detergents, and biotechnology. In the food industry, proteases are used for processes including meat tenderization, cheese manufacturing, and the production of protein hydrolysates. For the development of drugs for digestive disorders and as anti-inflammatory agents proteases are largely used. The detergent industry leverages proteases for their capability to break down protein stains, thereby enhancing cleaning efficiency. The biotechnological applications of proteases include their use in recombinant DNA technology and protein sequencing. The market is also driven by the increasing demand for proteases in waste management and leather processing.

North America and Europe dominate the market due to the presence of well-established industrial sectors and advanced research facilities, while the Asia-Pacific region is witnessing rapid growth driven by increasing industrialization and demand for processed foods. Key players in the proteases market include Novozymes, DSM, DuPont, and BASF, which emphasize innovations and strategic collaborations to expand their product portfolios and enhance their market presence. The rising trend towards sustainable and eco-friendly products is driving the development of microbial and plant-based proteases, which are perceived as more environmentally friendly alternatives.

To get more Insights: Request Free Sample Report

Proteases Market Trend

Shift towards the development and use of microbial and plant-based proteases

The proteases market is increasingly favoring microbial and plant-based proteases over traditional animal-based ones due to their extensive industrial applications and inherent advantages. Microbial proteases, produced by bacteria, molds, and yeasts, are cost-effective and versatile, used in cheese manufacturing, leather processing, and detergents due to their capability to function across varied pH and temperature ranges. Plant-based proteases such as papain and bromelain are gaining popularity for their superior performance in hydrolyzing by-products including cheese whey and bird feathers, producing bioactive peptides with health benefits. These enzymes are also essential in meat tenderization and provide significant advantages due to their low-cost isolation, stability under diverse conditions, and broad substrate affinity, making them ideal for biotechnological applications.

The shift towards these proteases is driven by the demand for sustainable, environmentally friendly processes, as they play roles in wastewater treatment and recovery of high-protein by-products drive the Proteases Market growth. Continued research is enhancing production efficiency and identifying new proteases, with the future of the market focused on leveraging microbial and plant sources for sustainable, cost-effective and versatile industrial solutions, aligning with global sustainability goals.

Proteases Market Dynamics

Increasing demand for proteases in the food and beverage industry to boost Market Growth

Proteases catalyze the breakdown of proteins into smaller peptides and amino acids and are essential in enhancing the texture, flavor, and nutritional quality of various food products. In meat processing, proteases degrade muscle fiber proteins and collagen post-slaughter, significantly improving meat tenderness. This enzymatic action transforms tough muscle tissue into tender, edible meat and enhances various nutritional indicators, benefiting the deep processing of meat products.

- For instance, the application of trypsin in meat processing promote the hydrolysis of proteins, increasing the presence of flavor-enhancing small amino acid peptides, thereby improving the overall flavor profile of meat foods.

In baked goods, proteases reduce gluten strength, which improves dough plasticity, increases volume, improves toughness, and shortens the forming time. This enzymatic modification is vital for producing high-quality bread, cakes, and biscuits. In beverages such as beer and tea, proteases help prevent protein precipitation during storage, thereby maintaining clarity and taste. Protease treatment in tea increases the amino nitrogen content by 13% to 39%, enhancing the umami and flavor of the tea. Also, in beer production, neutral proteases reduce the content of macromolecular proteins, improving stability during storage and eliminating unwanted tastes in fruit wines and other fermented drinks, which boosts Proteases Market growth.

Proteases are instrumental in developing new beverage products, such as the creation of nutritionally rich, easily digestible, and uniquely flavored beverages such as orange juice peanut peptide drinks. Fermentation technology, a cornerstone of beer, wine, cheese, yogurt, and bread production, also relies heavily on proteases for breaking down proteins, carbohydrates, and lipids into smaller molecules, facilitating microorganism activity for fermentation. The versatility of proteases extends across various applications within the food industry, including tenderizing meat, improving the texture of baked goods, hydrolyzing milk proteins for cheese production, and enhancing the nutritional content of soy products which is responsible for the Proteases Market growth. The increasing consumer demand for high-protein diets, processed foods, and innovative, health-focused food and beverage products continues to drive the protease market, making these enzymes essential in modern food and beverage manufacturing.

The high cost and complexity of enzyme purification and stabilization processes to hamper Market Growth

Purifying proteases to achieve the necessary level of purity and activity involves multiple steps such as precipitation, chromatography, and filtration, each requiring precise reagents and advanced equipment. These processes are labor-intensive and demand substantial financial investment, which is unaffordable, particularly for small and medium-sized enterprises, which is responsible for hampering the Proteases Market growth. Once purified, proteases need to be stabilized to maintain their activity under industrial conditions, which include extreme pH levels, high temperatures, and the presence of organic solvents. Stabilization techniques, such as immobilization on solid supports or chemical modification, add another layer of complexity and cost.

The need for precise conditions to prevent denaturation or degradation of the enzymes poses additional technical challenges. These stabilization strategies include the use of costly materials and sophisticated technologies, escalating production expenses. This financial burden is compounded by the requirement for continuous research and development to enhance enzyme efficiency and tailor them to specific industrial applications, which hamper Proteases Market growth. The combined effect of these factors expensive purification methods, intricate stabilization needs and the ongoing need for innovation limit the widespread adoption of proteases.

Companies find it challenging to justify the initial investment and operational costs against the benefits, particularly when cheaper alternatives or synthetic chemical processes are available. The complexity of these processes necessitates specialized knowledge and expertise, which not be readily available to all market players, thereby restricting market entry and competition. These barriers slow down the market's growth and hinder the scalability of protease applications across various sectors.

Proteases Market Segment Analysis

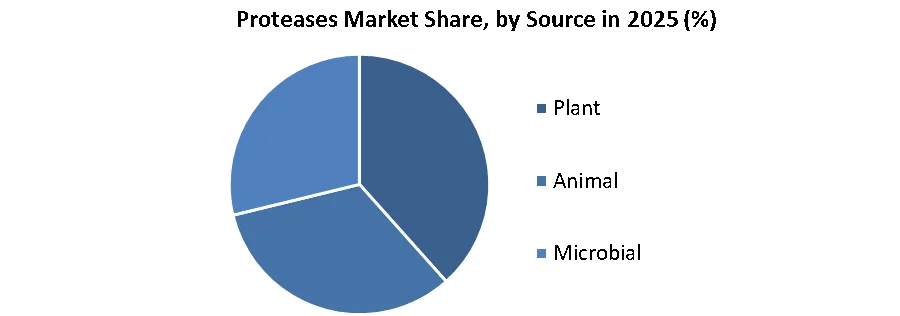

Based on the Source, the market is segmented into Plant, Animal and Microbial. Microbial proteases are expected to dominate the Proteases Market over the forecast period. Microbial proteases, produced by bacteria, molds, yeasts, and fungi, provide significant versatility, scalability, and cost-effectiveness in comparison to their counterparts. The microbial fermentation process enables efficient and controlled enzyme production on a large scale, meeting the increasing demand across several industries. Microbial proteases exhibit robust activity and stability under a wide range of pH, temperature, and environmental conditions, making them preferable for diverse industrial applications.

The microbial proteases are genetically engineered and optimized for specific functions, enhancing their efficacy and performance in targeted applications including food processing, pharmaceuticals, detergents, and waste treatment, which drive Proteases Market growth. The sustainable nature of microbial fermentation processes aligns with increasing environmental concerns and regulatory pressures, driving the adoption of microbial proteases as eco-friendly alternatives to animal-derived enzymes.

Based on Type, the market is categorized into Trypsin, Serine, Casein, Alkaline Protease and Others. Serine proteases dominated the Proteases Market in 2025. Serine proteases, characterized by the presence of a serine residue at their active site, play a crucial role in numerous biological processes and industrial applications. They are widely utilized due to their versatility, specificity, and efficiency in catalyzing peptide bond hydrolysis. In industries such as food processing, pharmaceuticals, and detergent manufacturing, serine proteases are extensively employed for their ability to efficiently break down proteins into peptides and amino acids.

Trypsin, a subtype of serine protease, holds particular prominence in the market due to its widespread use in protein analysis, cell culture, and biopharmaceutical production. The serine proteases exhibit optimal activity under a broad range of pH and temperature conditions, making them suitable for various industrial processes requiring proteolytic activity. The advancements in enzyme engineering and biotechnology have enabled the development of recombinant serine proteases with enhanced stability, specificity, and catalytic efficiency, driving the proteases market growth.

Proteases Market Regional Insights

North America dominated the Proteases Market in 2025 and is expected to continue its dominance during the forecast period. The region boasts a well-established industrial infrastructure and robust research and development capabilities, development innovation and technological advancement in enzyme production and application. Major economies such as the United States and Canada are home to leading biotechnology and pharmaceutical companies, academic institutions, and research centers that drive the development of novel proteases and their applications across several industries.

This conducive ecosystem supports collaborations between academia and industry, enabling the translation of research findings into commercial products, which boosts Proteases Market growth. North America benefits from a strong regulatory framework that ensures product safety and efficacy, offering confidence to manufacturers and consumers alike. Regulatory agencies such as the Food and Drug Administration (FDA) in the United States uphold stringent standards for enzyme-based products, thereby enhancing market credibility and fostering trust among end-users.

The region's diverse industrial landscape, encompassing sectors such as food and beverage, pharmaceuticals, healthcare, and biotechnology, creates a vast and lucrative Proteases Market for proteases. Proteases find widespread application in food processing, where they are used for flavor enhancement, tenderization, and protein modification. In the pharmaceutical and healthcare sectors, proteases are used in drug development, formulation, and manufacturing processes. They are utilized in the production of therapeutic proteins, biologics, and diagnostic reagents, contributing to the region's leadership in the biopharmaceutical industry. North America's strong emphasis on sustainability and environmental stewardship drives the adoption of enzyme-based solutions in waste treatment, biofuel production and other eco-friendly applications. As a result, demand for proteases continues to soar across diverse end-use industries, driving North America Proteases Market growth.

|

Proteases Market Scope |

|

|

Market Size in 2025 |

USD 3.71 Bn. |

|

Market Size in 2032 |

USD 5.62 Bn. |

|

CAGR (2026-2032) |

6.1 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Source Plant Animal Microbial |

|

By Type Trypsin Serine Casein Alkaline Others |

|

|

By End User Food And Beverage Pharmaceuticals Healthcare Others |

|

|

Regional Scope |

North America (United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa ( South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Proteases Market Key Players

- Novozymes A/S (Bagsværd, Denmark)

- DuPont (Wilmington, Delaware, United States)

- BASF SE (Ludwigshafen, Germany)

- DSM Nutritional Products AG (Kaiseraugst, Switzerland)

- AB Enzymes GmbH (Darmstadt, Germany)

- Amano Enzyme Inc. (Nagoya, Japan)

- Chr. Hansen Holding A/S (Horsholm, Denmark)

- Dyadic International Inc. (Jupiter, Florida, United States)

- Enzyme Development Corporation (New York, United States)

- Advanced Enzyme Technologies Limited (Thane, India)

- Biocatalysts Ltd (Cardiff, United Kingdom)

- Specialty Enzymes & Biotechnologies Co. (Chino, California, United States)

- Jiangsu Boli Bioproducts Co., Ltd. (Jiangsu, China)

- Nagase & Co., Ltd. (Tokyo, Japan)

- Solvay SA (Brussels, Belgium)

- MAPS Enzymes Ltd (Hyderabad, India)

- Advanced Enzyme Technologies Ltd (Thane, India)

- Creative Enzymes (Shirley, New York, United States)

- Roche Diagnostics Corporation (Basel, Switzerland)

- Enzyme Solutions Inc. (Athens, Georgia, United States)

- Amicogen Inc. (Jinju, South Korea)

- Enzyme Innovation (St. Louis, Missouri, United States)

- BBI Solutions (Cardiff, United Kingdom)

Frequently Asked Questions

North America is expected to dominate the Proteases Market during the forecast period.

The Proteases Market size is expected to reach USD 5.62 billion by 2032.

The major top players in the Global Proteases Market are Novozymes A/S (Bagsværd, Denmark), DuPont (Wilmington, Delaware, United States), BASF SE (Ludwigshafen, Germany), DSM Nutritional Products AG (Kaiseraugst, Switzerland), AB Enzymes GmbH (Darmstadt, Germany), Amano Enzyme Inc. (Nagoya, Japan), Chr. Hansen Holding A/S (Horsholm, Denmark) and others.

The increasing demand for proteases in various industries such as food and beverage, pharmaceuticals, and detergents; and rising applications in biotechnology for protein modification and synthesis are expected to drive market growth during the forecast period.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Proteases Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Proteases Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. New Product Launches

4. Proteases Market: Dynamics

4.1. Proteases Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Proteases Market Drivers

4.3. Proteases Market Restraints

4.4. Proteases Market Opportunities

4.5. Proteases Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape

4.10.1. Market Regulation by Region

4.10.1.1. North America

4.10.1.2. Europe

4.10.1.3. Asia Pacific

4.10.1.4. Middle East and Africa

4.10.1.5. South America

4.10.2. Government Schemes and Initiatives

5. Proteases Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

5.1. Proteases Market Size and Forecast, by Source (2025-2032)

5.1.1. Plant

5.1.2. Animal

5.1.3. Microbial

5.2. Proteases Market Size and Forecast, by Type (2025-2032)

5.2.1. Trypsin

5.2.2. Serine

5.2.3. Casein

5.2.4. Alkaline

5.2.5. Others

5.3. Proteases Market Size and Forecast, by End User (2025-2032)

5.3.1. Food and Beverage

5.3.2. Pharmaceuticals

5.3.3. Healthcare

5.3.4. Others

5.4. Proteases Market Size and Forecast, by Region (2025-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Proteases Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

6.1. North America Proteases Market Size and Forecast, by Source (2025-2032)

6.1.1. Plant

6.1.2. Animal

6.1.3. Microbial

6.2. North America Proteases Market Size and Forecast, by Type (2025-2032)

6.2.1. Trypsin

6.2.2. Serine

6.2.3. Casein

6.2.4. Alkaline

6.2.5. Others

6.3. North America Proteases Market Size and Forecast, by End User (2025-2032)

6.3.1. Food and Beverage

6.3.2. Pharmaceuticals

6.3.3. Healthcare

6.3.4. Others

6.4. North America Proteases Market Size and Forecast, by Country (2025-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Proteases Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

7.1. Europe Proteases Market Size and Forecast, by Source (2025-2032)

7.2. Europe Proteases Market Size and Forecast, by Type (2025-2032)

7.3. Europe Proteases Market Size and Forecast, by End User (2025-2032)

7.4. Europe Proteases Market Size and Forecast, by Country (2025-2032)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Proteases Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

8.1. Asia Pacific Proteases Market Size and Forecast, by Source (2025-2032)

8.2. Asia Pacific Proteases Market Size and Forecast, by Type (2025-2032)

8.3. Asia Pacific Proteases Market Size and Forecast, by End User (2025-2032)

8.4. Asia Pacific Proteases Market Size and Forecast, by Country (2025-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Rest of Asia Pacific

9. Middle East and Africa Proteases Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

9.1. Middle East and Africa Proteases Market Size and Forecast, by Source (2025-2032)

9.2. Middle East and Africa Proteases Market Size and Forecast, by Type (2025-2032)

9.3. Middle East and Africa Proteases Market Size and Forecast, by End User (2025-2032)

9.4. Middle East and Africa Proteases Market Size and Forecast, by Country (2025-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Nigeria

9.4.4. Rest of ME&A

10. South America Proteases Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

10.1. South America Proteases Market Size and Forecast, by Source (2025-2032)

10.2. South America Proteases Market Size and Forecast, by Type (2025-2032)

10.3. South America Proteases Market Size and Forecast, by End User (2025-2032)

10.4. South America Proteases Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. Novozymes A/S (Bagsværd, Denmark)

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc.)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. DuPont (Wilmington, Delaware, United States)

11.3. BASF SE (Ludwigshafen, Germany)

11.4. DSM Nutritional Products AG (Kaiseraugst, Switzerland)

11.5. AB Enzymes GmbH (Darmstadt, Germany)

11.6. Amano Enzyme Inc. (Nagoya, Japan)

11.7. Chr. Hansen Holding A/S (Horsholm, Denmark)

11.8. Dyadic International Inc. (Jupiter, Florida, United States)

11.9. Enzyme Development Corporation (New York, United States)

11.10. Advanced Enzyme Technologies Limited (Thane, India)

11.11. Biocatalysts Ltd (Cardiff, United Kingdom)

11.12. Specialty Enzymes & Biotechnologies Co. (Chino, California, United States)

11.13. Jiangsu Boli Bioproducts Co., Ltd. (Jiangsu, China)

11.14. Nagase & Co., Ltd. (Tokyo, Japan)

11.15. Solvay SA (Brussels, Belgium)

11.16. MAPS Enzymes Ltd (Hyderabad, India)

11.17. Advanced Enzyme Technologies Ltd (Thane, India)

11.18. Creative Enzymes (Shirley, New York, United States)

11.19. Roche Diagnostics Corporation (Basel, Switzerland)

11.20. Enzyme Solutions Inc. (Athens, Georgia, United States)

11.21. Amicogen Inc. (Jinju, South Korea)

11.22. Enzyme Innovation (St. Louis, Missouri, United States)

11.23. BBI Solutions (Cardiff, United Kingdom)

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook