Micromobility Market Key Growth Potential and Forecast Analysis (2025-2032) by Network Type, Hardware, Communication Type, End User, Services, and Region

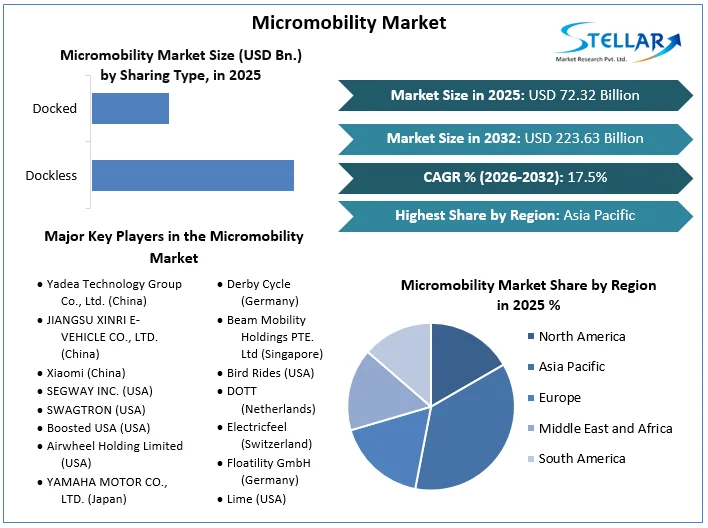

Micromobility Market size was valued at US$ 72.32 Billion in 2025 and the total Micromobility Market revenue is expected to grow at 17.5% through 2026 to 2032, reaching nearly US$ 223.63 Billion.

Micromobility Market Overview:

Micromobility is a growing transportation sector that includes commuting using a variety of lightweight vehicles such as electric scooters, electric skateboards, and electric bicycles. Factors such as increasing traffic congestion, rising oil and gas prices, ease of parking and saturation in the auto sector are expected to drive the market growth during the forecast period. In addition, factors such as the growth of e-bikes and e-scooter rental and sharing services around the world are expected to create new opportunities for micro-mobility in the coming years. Micromobility market is expected to register CAGR of 17.5% during the forecast period.

To get more Insights: Request Free Sample Report

Micromobility Market Dynamics:

Increase in venture capital and strategic investments:

Significant increase in carpooling preference among car-poolers is a key factor contributing to the growth of carpooling and carpooling. In addition, the proliferation of services offered by major players in the micromobility market, including Uber and Ola, and the ability to choose convenient pick-up and drop-off locations are encouraging consumers to choose services. Carpooling and carpooling. In addition, the significant increase in the number of carpooling services and many carpooling services such as bike sharing and car sharing even for short distances are driving the growth of micro mobile market. In addition, carpooling service providers offer benefits such as affordable door-to-door pickup and drop-off, passenger travel information, and greater convenience than service providers. Traditional carpooling. This will boost demand for carpooling services. In addition, several service providers offer various facilities, offers, and discounts, such as monthly pass on shared ride, to reduce the expenses of daily commuters.

Stakeholders have invested more than $5.7 billion in micro mobile start-ups since 2015, with more than 85% targeting China. The micromobility market has acquired a solid customer base and is about two to three times faster than car sharing or carpooling. For example, within a few years, several micro-mobility start-ups had cumulative valuations in excess of $1 billion. Two circumstances are the source of this accelerated expansion. First, most shared micromobility launches happen in enabling environments. Urban consumers have come to appreciate and use shared mobility solutions, such as car sharing, carpooling, and email.

Lower break-even points favouring the economies:

The economy of shared micro-mobility is largely favourable for companies in the industry. Companies are finding it much easier to scale up micro-mobility assets (e.g. e-bikes) than car-based sharing solutions. For example, the current acquisition cost for an electric scooter is around $400, compared to the thousands of dollars needed to buy a car. So while today's car-sharing solutions take several years to become economically viable, an outside case estimate from a leader in shared mobility suggests a car scooter can break even in less than four months.

The struggle of service providers of Micromobility:

The global strike is having a profound effect on service provider ratings, industry employed workers and the pace of industry consolidation. For example, the value of a company that operates a global network of e-bikes and e-scooters recently dropped by 79%. Another supplier halted operations in six US cities and all European markets, laying off 30% of its workforce. A third company has reduced staff hours by 60% while providing a streamlined fleet of scooters for healthcare workers in Germany. The shutdown has also prompted consolidation moves in the industry. For example, a micromobility company recently acquired the e-bicycle and e-scooter business of a major ride hailing company.

Cities are providing extra assist for cycling:

Worldwide, the lockdown has pushed new citywide policies. One foremost end result is an improved awareness on bicycle lanes. Consider the following:

- Milan has introduced that 35 kilometers of streets formerly utilized by automobiles may be transitioned to taking walks and biking lanes after the lockdown is lifted.

- Paris will convert 50 kilometers of lanes normally reserved for automobiles to bicycle lanes. It additionally plans to invest $325 million to replace its bicycle network.

- Brussels is popping forty kilometers of vehicle lanes into cycle paths.

- Seattle completely closed 30 kilometers of streets to maximum vehicles, supplying extra area for human beings to stroll and biking following the lockdown.

- Montreal introduced the advent of extra than 320 kilometers of latest pedestrian and bicycle paths throughout the city.

COVID Impact Analysis:

As the pandemic broke out in some places, it was only natural that people would start traveling again. According to Apple's analysis of iPhone data, passenger- kilometres travelled by private and shared micro-vehicle have decreased by about 60-70% in Europe and the United States. Interestingly, the same data source showed U shape recovery; extrapolating this trend suggests a recovery to pre-crisis tourism levels in 2021-22.

To determine if and when the micromobility will recover, we conducted a global consumer survey in May 2020. It included more than 7,000 respondents from seven global markets. Demand: China, France, Germany, Italy, Japan, United Kingdom and the United States. Our goal is to study consumer behaviour and expectations about mobility before, during, and after the crisis which is done in reports.

According to consumer survey by Micromobility Council, the use of micromobility could increase. It shows that the number of respondents willing to regularly use micromobility in the next normal will increase by 9% for the private micromobility and 12% for the general micromobility compared to pre-crisis levels. Given these trends, we believe private and shared micromobility solutions will fully recover passenger kilometres travelled, with no significant decline from pre-crisis levels. We also believe that overall mobility will fully return to pre-crisis levels.

Micromobility Market Segmentation:

Android Segment is dominating the market in terms of user base:

Based on the type of vehicle, the micromobility market is divided into electric kick scooters, electric skateboards and electric bicycles. The electric bicycle segment dominated the market in 2025, accounting for more than 85% of global sales. The segment is expected to register over 14.3% CAGR over the forecast period as it is the cheapest and most convenient alternative to public transport. Some countries are working to encourage the use of electric bicycles, using both regulatory and subsidy changes to reduce the burden on public transport. In addition, compared to other transportation systems such as buses and taxis, electric bicycles are easier to charge, cheaper and do not require a large investment to support the infrastructure. Hence, an increase in the demand for electric bicycles across the world is being observed.

The electric scooter segment is expected to post the second highest CAGR of 10.3% during the forecast period. The demand for these scooters has increased since 2017 due to the strong investment by the players in the shared electric scooter market when it was still in the transition phase. The scooter sharing market is currently undergoing a dynamic development with the entry of global companies such as Uber Technologies, Inc.; Bird, Inc.; Lyft; and Lime operate in the on-demand transportation industry.

Micromobility Market Regional Insights:

In 2025, the Asia Pacific region dominated the micromobility market, accounting for more than 45% of worldwide revenue. The majority of micromobility car manufacturers are based in Asia Pacific, Europe, and North America. These companies make money by selling their products around the world, either through their own distribution channels or through OEMs. Governments in countries like India, China, and Japan are establishing standards and rules for vehicle charging infrastructure, which is likely to boost regional market growth. Furthermore, over the projection period, Asia Pacific is expected to be the fastest-growing regional market.

The demographic characteristics of consumers vary by area. Drivers of electric kick scooters in North America and Europe tend to see them as a way of life, but those in Latin America, the Middle East and Africa, and Asia Pacific see them as a practical mode of transportation. Consumer happiness, which can be measured using a variety of metrics such as performance, maintenance costs, and durability, is a critical consideration for businesses looking to keep or gain new consumers. Vendors attempting to attract customers during the debut of any car, on the other hand, focus on two primary factors: design/style and specifications. Micromobility may theoretically include all passenger travels of fewer than 8 kilometres (5 miles), which represent for 50 to 60% of total passenger miles travelled in China, Europe, and the United States today. Micromobility solutions, for example, may cover around 20% of public transportation travel (in addition to addressing the first- and last-mile gap) as well as all journeys taken by private bike, moped, scooter, or foot today.

However, SMR anticipate that shared micromobility will only use 8 to 15% of this hypothetical market. Customer acceptance, weather conditions, age fit, and micromobility's lesser presence in rural areas are all factors that limit its applicability for relevant mobility use cases (for example, limited room when going shopping).

The objective of the report is to present a comprehensive analysis of the Micromobility Market to the stakeholders in the industry. The report provides trends that are most dominant in the Micromobility Market and how these trends will influence new business investments and market development throughout the forecast period. The report also aids in the comprehension of the Micromobility Market dynamics and competitive structure of the market by analyzing market leaders, market followers, and regional players.

The qualitative and quantitative data provided in the Micromobility Market report is to help understand which market segments, regions are expected to grow at higher rates, factors affecting the market, and key opportunity areas, which will drive the industry and market growth through the forecast period. The report also includes the competitive landscape of key players in the industry along with their recent developments in the Micromobility Market. The report studies factors such as company size, market share, market growth, revenue, production volume, and profits of the key players in the Micromobility Market.

The report provides Porter's Five Force Model, which helps in designing the business strategies in the market. The report helps in identifying how many rivals are existing, who they are, and how their product quality is in the Market. The report also analyses if the Micromobility Market is easy for a new player to gain a foothold in the market, do they enter or exit the market regularly if the market is dominated by a few players, etc.

The report also includes a PESTEL Analysis, which aids in the development of company strategies. Political variables help in figuring out how much a government can influence the Market. Economic variables aid in the analysis of economic performance drivers that have an impact on the Market. Understanding the impact of the surrounding environment and the influence of environmental concerns on the Micromobility Market is aided by legal factors.

Micromobility Market Scope:

|

Micromobility Market |

|

|

Market Size in 2025 |

USD 72.32 Bn. |

|

Market Size in 2032 |

USD 223.63 Bn. |

|

CAGR (2026-2032) |

17.5% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

by Vehicle Type

|

|

by Battery Type

|

|

|

By Sharing Type

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Micromobility Market Players:

- Yadea Technology Group Co., Ltd. (China)

- JIANGSU XINRI E-VEHICLE CO., LTD. (China)

- Xiaomi (China)

- SEGWAY INC. (USA)

- SWAGTRON (USA)

- Boosted USA (USA)

- Airwheel Holding Limited (USA)

- YAMAHA MOTOR CO., LTD. (Japan)

- Accell Group (Netherlands)

- Derby Cycle (Germany)

- Beam Mobility Holdings PTE. Ltd (Singapore)

- Bird Rides (USA)

- DOTT (Netherlands)

- Electricfeel (Switzerland)

- Floatility GmbH (Germany)

- Lime (USA)

- Neuron

- VOI

- Yulu Bikes Pvt. Ltd (China)

Frequently Asked Questions

APAC region have the highest growth rate in the Micromobility market.

Yadea Technology Group Co., Ltd. (China), JIANGSU XINRI E-VEHICLE CO., LTD. (China), Xiaomi (China), SEGWAY INC. (USA), SWAGTRON (USA), Boosted USA (USA), Airwheel Holding Limited (USA), YAMAHA MOTOR CO., LTD. (Japan), Accell Group (Netherlands), Derby Cycle (Germany), Beam Mobility Holdings PTE. Ltd (Singapore), Bird Rides (USA), DOTT (Netherlands), Electricfeel (Switzerland) and others are the key players in the Micromobility market.

Moped and Scooters segment is dominating the market owing to increasing purchasing rate of the scooters and low installation cost of sharing autonomy in the vehicles.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Up Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Micromobility Market Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Micromobility Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Market Share

3.2.8. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovations

4. Micromobility Market: Dynamics

4.1. Micromobility Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Micromobility Market Drivers

4.3. Micromobility Market Restraints

4.4. Micromobility Market Opportunities

4.5. Micromobility Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Legal Factors

4.7.5. Environmental Factors

4.8. Technological Analysis

4.8.1. Smart Parking Technology

4.8.2. In-app software Educates and Increases Safe Vehicle Use

4.8.3. Connective Technology Allows Multimodality

4.8.4. Battery Swapping

4.8.5. Technological Roadmap

4.9. Regulatory Landscape

4.9.1. Market Regulation by Region

4.9.1.1. North America

4.9.1.2. Europe

4.9.1.3. Asia Pacific

4.9.1.4. Middle East and Africa

4.9.1.5. South America

4.9.2. Impact of Regulations on Market Dynamics

4.9.3. Government Schemes and Initiatives

5. Micromobility Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

5.1. Micromobility Market Size and Forecast, by Vehicle Type (2025-2032)

5.1.1. Skateboards

5.1.2. Hover board

5.1.3. Low Speed EVs

5.1.4. Segway

5.1.5. Mopeds and Scooters

5.1.6. E-kick scooters

5.1.7. Bicycles

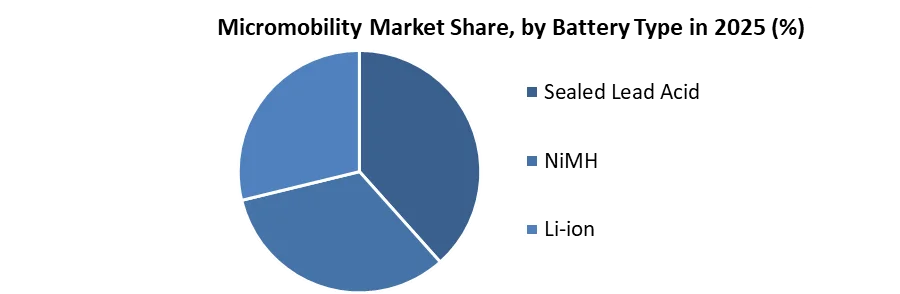

5.2. Micromobility Market Size and Forecast, by Battery Type (2025-2032)

5.2.1. Sealed Lead Acid

5.2.2. NiMH

5.2.3. Li-ion

5.3. Micromobility Market Size and Forecast, by Sharing Type (2025-2032)

5.3.1. Dockless

5.3.2. Docked

5.4. Micromobility Market Size and Forecast, by Region (2025-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Micromobility Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

6.1. North America Micromobility Market Size and Forecast, by Vehicle Type (2025-2032)

6.1.1. Skateboards

6.1.2. Hover board

6.1.3. Low Speed EVs

6.1.4. Segway

6.1.5. Mopeds and Scooters

6.1.6. E-kick scooters

6.1.7. Bicycles

6.2. North America Micromobility Market Size and Forecast, by Battery Type (2025-2032)

6.2.1. Sealed Lead Acid

6.2.2. NiMH

6.2.3. Li-ion

6.3. North America Micromobility Market Size and Forecast, by Sharing Type (2025-2032)

6.3.1. Dockless

6.3.2. Docked

6.4. North America Micromobility Market Size and Forecast, by Country (2025-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Micromobility Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

7.1. Europe Micromobility Market Size and Forecast, by Vehicle Type (2025-2032)

7.2. Europe Micromobility Market Size and Forecast, by Battery Type (2025-2032)

7.3. Europe Micromobility Market Size and Forecast, by Sharing Type (2025-2032)

7.4. Europe Micromobility Market Size and Forecast, by Country (2025-2032)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Micromobility Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

8.1. Asia Pacific Micromobility Market Size and Forecast, by Vehicle Type (2025-2032)

8.2. Asia Pacific Micromobility Market Size and Forecast, by Battery Type (2025-2032)

8.3. Asia Pacific Micromobility Market Size and Forecast, by Sharing Type (2025-2032)

8.4. Asia Pacific Micromobility Market Size and Forecast, by Country (2025-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Rest of Asia Pacific

9. Middle East and Africa Micromobility Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

9.1. Middle East and Africa Micromobility Market Size and Forecast, by Vehicle Type (2025-2032)

9.2. Middle East and Africa Micromobility Market Size and Forecast, by Battery Type (2025-2032)

9.3. Middle East and Africa Micromobility Market Size and Forecast, by Sharing Type (2025-2032)

9.4. Middle East and Africa Micromobility Market Size and Forecast, by Country (2025-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Nigeria

9.4.4. Rest of ME&A

10. South America Micromobility Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

10.1. South America Micromobility Market Size and Forecast, by Vehicle Type (2025-2032)

10.2. South America Micromobility Market Size and Forecast, by Battery Type (2025-2032)

10.3. South America Micromobility Market Size and Forecast, by Sharing Type (2025-2032)

10.4. South America Micromobility Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. Yadea Technology Group Co., Ltd. (China)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. JIANGSU XINRI E-VEHICLE CO., LTD. (China)

11.3. Xiaomi (China)

11.4. SEGWAY INC. (USA)

11.5. SWAGTRON (USA)

11.6. Boosted USA (USA)

11.7. Airwheel Holding Limited (USA)

11.8. YAMAHA MOTOR CO., LTD. (Japan)

11.9. Accell Group (Netherlands)

11.10. Derby Cycle (Germany)

11.11. Beam Mobility Holdings PTE. Ltd (Singapore)

11.12. Bird Rides (USA)

11.13. DOTT (Netherlands)

11.14. Electricfeel (Switzerland)

11.15. Floatility GmbH (Germany)

11.16. Lime (USA)

11.17. Neuron

11.18. VOI

11.19. Yulu Bikes Pvt. Ltd (China)

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook