Methanol Catalyst Market Global Industry Analysis and Forecast (2026-2032)

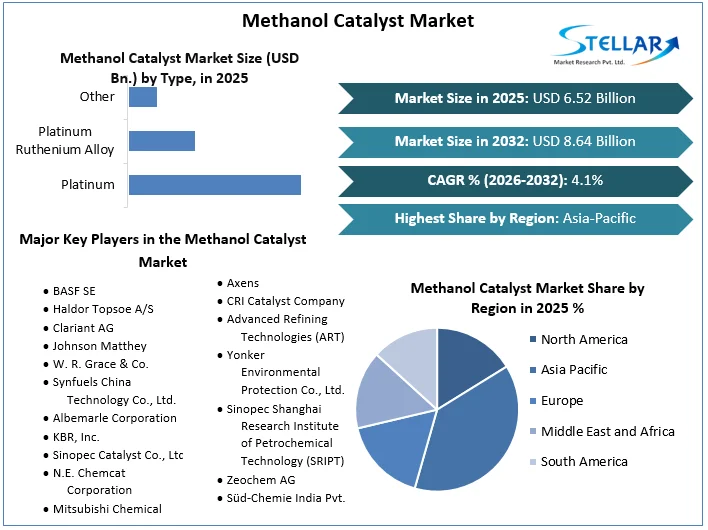

Methanol Catalyst Market Size was valued at USD 6.52 Bn in 2025 and is expected to reach USD 8.64 Bn by 2032 at a CAGR of 4.1 % over the forecast period.

Methanol Catalyst Market Overview

The manufacturing and use of catalysts to speed up the conversion of raw materials, often natural gas or coal, into methanol is a part of the methanol catalyst market. Methanol is an essential chemical component utilized in many different sectors, including those producing chemicals, polymers, and fuels. The chemical reactions necessary for the creation of methanol are sped up significantly by catalysts. The demand for methanol-based products, developments in catalyst technology, and environmental laws all have an impact on the market's growth. Different methanol synthesis techniques use various types of catalysts, each with pros and cons, such as copper-based and zinc oxide-based catalysts. Developments in environmentally friendly and sustainable manufacturing, as well as breakthroughs in catalyst design to increase efficiency and selectivity.

To get more Insights: Request Free Sample Report

Methanol Catalyst Market Dynamics

The market for catalysts is directly impacted by the increased demand for methanol as a feedstock across numerous industries, including chemicals, plastics, automotive, and energy. The demand for effective methanol production rises as these sectors develop. Methanol is regarded as an environmentally friendly and multipurpose fuel that may be utilized in both fuel cells and as a clean-burning fuel for automobiles. The market for catalysts is boosted as a result of the drive toward sustainable technologies and better energy sources.

The demand for better catalyst technologies is driven by ongoing research and development projects to improve the efficiency, selectivity, and lifetime of catalysts. Improvements in catalyst composition and design lead to better methanol synthesis procedures. The growth of the petrochemical industry and the rising need for methanol-derived chemicals like formaldehyde and acetic acid fuel methanol production, which in turn propels the catalyst market.

Methanol Catalyst Market Restraints

Changes in the cost of raw materials needed to make methanol, such as coal and natural gas, can affect production costs and, as a result, the profitability of companies that make methanol catalysts. The expenses associated with setting up methanol production facilities and investing in cutting-edge catalyst technologies can be prohibitive for some businesses, preventing them from joining the market or improving their current procedures. It is challenging to create catalysts with excellent selectivity, activity, and stability under various operating circumstances. The speed of invention and the uptake of new catalysts might be slowed down by technological obstacles. Modifications to laws governing trade, renewable energy standards, and emissions can have an impact on the methanol market's dynamics and investment choices.

Global economic variables Economic downturns can have an impact on industrial activity, which might result in a decrease in demand for methanol and its derivative products. The availability of raw materials and catalytic components can be impacted by supply chain disruptions caused by geopolitical reasons, natural catastrophes, or other unforeseen events, which can have an influence on production schedules. The mature market could present problems for the methanol sector, particularly in areas with existing production facilities. Compared to developing markets with more room for expansion, growth may be slower.

Methanol Catalyst Market Opportunities

On a global level, the methanol catalyst market offers a number of attractive opportunities. A climate that is advantageous for the production of methanol is created by the increased focus on sustainability and the switch to greener energy sources. Methanol has the potential to be used in a variety of fuel-related applications, from fuel cells to clean-burning motor fuels. This creates opportunities for catalyst producers to create cutting-edge technologies that boost methanol production efficiency, use less energy, and emit fewer greenhouse gases. Furthermore, the development of Methanol-to-Olefins (MTO) technology offers a tremendous opportunity by enabling the conversion of methanol into worthwhile olefin products. Finally, research and development expenditures to solve issues like catalyst stability, selectivity, and scalability might open up fresh opportunities for growth and differentiation in the cutthroat methanol catalyst market.

Methanol Catalyst Market Challenge

On a global level, the methanol catalyst market is faced with a number of formidable obstacles. The continual need to create catalysts that strike a compromise between high activity, selectivity, and stability is one of the main challenges. Catalyst design continues to face a difficult task in achieving and maintaining these qualities under a variety of operational situations. The price volatility of raw materials, particularly natural gas and coal, which directly affects manufacturing costs and total profitability, is another market restraint. Environmental issues are also a significant challenge. Although methanol is regarded as a greener fuel, it still requires a significant amount of energy and emits carbon dioxide.

The industry must strike a delicate balance between meeting demand and mitigating the environmental impact of methanol production as efforts to achieve global sustainability targets accelerate. Competing another level of difficulty is added by technologies like direct carbon capture and procedures based on renewable energy. These options can challenge the established catalyst-driven methanol manufacturing techniques, forcing the sector to change and advance.

Methanol Catalyst Market Trends

The global market for methanol catalysts is being shaped by many industry trends:

1. Growing Demand for Methyl Ethanol The demand for effective and cutting-edge catalysts to improve methanol production is driven by the rising demand for methanol as a critical feedstock in numerous industries, including chemicals, fuels, and polymers.

2. Switch to renewable methanol: The development of sustainable and renewable energy sources has sparked interest in the production of methanol from renewable feedstock’s like biomass or collected carbon dioxide, which calls for specialized catalysts.

3. Initiatives for Emission Reduction: As a cleaner-burning alternative fuel and to cut down on emissions in transportation, methanol is being investigated. In order to transform methanol into fuels like gasoline or dimethyl ether (DME), catalysts are essential.

4. Catalyst Technology Advancements: Current research is focused on methanol yields and process effectiveness, on creating catalysts with enhanced selectivity, stability, and activity.

5. Processes for converting methanol to olefins (MTO) and hydrocarbons (MTH) Growing in popularity are the MTO and MTH processes, which turn methanol into useful olefins and hydrocarbons, respectively. Catalysts are essential for streamlining these conversion procedures.

6. Increasing Investments in the Petrochemical Sector The demand for methanol-based products is rising due to growth in the petrochemical industry, which is being driven by demand for plastics and chemicals. This is having an effect on the catalyst market.

7. Asian and Pacific Rim Dominance Due to its rapid industrialization and rising demand for chemicals and fuels, the Asia-Pacific region, particularly China, is a significant consumer of methanol and a significant market for methanol catalysts.

Regional Insights for Methanol Catalyst Market

Asia-Pacific: Due to its strong industrialization, notably in nations like China and India, this region dominates the worldwide methanol catalyst market. The expansion of the catalyst market is fuelled by the need for methanol, which is generated by numerous industries and applications. Methanol is widely produced and consumed in China, where the government actively promotes methanol as a cleaner fuel alternative. Due to a number of important factors, the worldwide methanol catalyst market is significantly expanding and having an impact in the Asia Pacific region. Methanol is in high demand as a feedstock for chemicals, fuels, and plastics due to the region's rapid industrialization, especially in nations like China and India.

This need, in turn, stimulates the desire for effective and sophisticated catalysts that optimize the processes used to produce methanol. Further driving the demand for specialist catalysts is the region's growing emphasis on clean energy and sustainable manufacturing, which is encouraging investments in methanol-to-fuels processes and emission reduction technology. The Asia Pacific region has a thriving petrochemical, automotive, and electronics industries, which highlights the crucial function of methanol catalysts in these fields.

North America: The US has a substantial market share for methanol catalysts. Natural gas, a crucial feedstock for the manufacturing of methanol, is now more readily available as a result of the shale gas boom in the United States. The demand for methanol is influenced by the development of catalysts as well as the growing desire in cleaner chemicals and fuels.

Methanol Catalyst Market Segment Analysis

By Type: The market for methanol catalysts can be divided into a number of types, each of which caters to particular methanol production processes and efficiency requirements. Catalyst composition is one of the main segments, with copper-based catalysts being a common variety. In traditional methanol synthesis techniques like the low-pressure procedure, copper catalysts are frequently backed with zinc oxide or alumina. For the synthesis of methanol, these catalysts have great activity and selectivity. Catalysts based on zinc oxide are covered in another section. These are frequently used in high-pressure methanol synthesis. These catalysts are well recognized for their stability and efficiency under particular process conditions and are known to promote reactions at high pressures.

Additionally, due to their potential to increase selectivity and efficiency in the production of methanol, zeolite-based catalysts and mixed-metal oxide catalysts are gaining popularity. These cutting-edge catalysts types, such as CO conversion and product distribution, are created to improve particular parts of the reaction. Overall, the market for methanol catalysts is segmented by type, reflecting the variety of catalyst compositions and their functions in various methanol production processes. This segmentation enables catalyst producers to provide specialized solutions that fit particular process needs, catalytic efficiency objectives, and operational circumstances.

By Application: The various sectors that depend on methanol and its derivatives can be reflected in the global methanol catalyst market's application-based segmentation. The production of numerous chemicals including formaldehyde, acetic acid, and methyl methacrylate requires methanol as a critical feedstock, which makes the chemical sector one of its major application segments. These processes' catalysts are built to guarantee high conversion rates and superior product quality. The energy industry, which includes the manufacturing of methanol as a clean-burning fuel and its usage in fuel cells, is another key application segment. Catalysts are essential for maximizing the conversion of methanol into fuel, increasing combustion efficiency, and reducing pollutants.

Additionally, the production of resins, polymers, and plastics in the plastics and polymer industry depends on goods made from methanol. In these applications, catalysts concentrate on assisting in the synthesis of intermediates based on methanol that go towards the creation of these materials. Methanol is also being investigated as an alternate fuel source by the car sector due to its cleaner burning characteristics. In this situation, catalysts help turn methanol into fuel blends that adhere to pollution regulations. The numerous industrial sectors that depend on methanol and its derivatives are reflected in the segmentation of the methanol catalyst market by application. Manufacturers of catalysts customize their products to meet the unique needs of each application, enhancing workflows for productivity, sustainability, and product quality.

Methanol Catalyst Market: Competitive Landscape

The competitive environment in the global methanol catalyst market is defined by a blend of well-established companies, cutting-edge start-ups, and research-focused organizations. Clariant AG, Johnson Matthey, W. R. Grace & Co., Haldor Topsoe A/S, BASF SE, and Johnson Matthey are a few well-known catalyst producers. Due to their proficiency in catalyst production, robust research and development capabilities, and established alliances with methanol producers, these businesses have a substantial presence. Smaller, more specific businesses with a focus on catalyst solutions are emerging in addition to these industrial behemoths. These businesses frequently focus on developing unique catalyst compositions that are tailored for particular methanol production techniques or uses.

The advancement of catalyst technology is facilitated by players. Technological developments, sustainability initiatives, and the capacity to adjust to shifting industry demands are some of the variables that define the competitive dynamics of the methanol catalyst market. Manufacturers of catalysts that provide products in line with sustainability objectives are positioned for growth as the market places more emphasis on greener processes. Partnerships and collaborations are frequent tactics in this industry because they enable businesses to pool their resources and skills to tackle difficult problems and spur innovation. The competitive environment in the methanol catalyst market is likely to keep altering as the sector adapts to new trends and works to satisfy the needs of a shifting global energy and chemical landscape.

Methanol Catalyst Market Scope:

|

Methanol Catalyst Market |

|

|

Market Size in 2025 |

USD 6.52 Bn. |

|

Market Size in 2032 |

USD 8.64 Bn. |

|

CAGR (2026-2032) |

4.1% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

by Type

|

|

by Application

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Methanol Catalyst Market Key players

- BASF SE

- Haldor Topsoe A/S

- Clariant AG

- Johnson Matthey

- W. R. Grace & Co.

- Synfuels China Technology Co., Ltd.

- Albemarle Corporation

- KBR, Inc.

- Sinopec Catalyst Co., Ltd.

- N.E. Chemcat Corporation

- Mitsubishi Chemical Corporation

- Lummus Technology

- Sud-Chemie India Pvt. Ltd.

- Axens

- CRI Catalyst Company

- Advanced Refining Technologies (ART)

- Yonker Environmental Protection Co., Ltd.

- Sinopec Shanghai Research Institute of Petrochemical Technology (SRIPT)

- Zeochem AG

- Süd-Chemie India Pvt. Ltd.

- Evonik Industries AG

- CNPC Jilin Chemical Group Corporation

- Sichuan Tianyi Science & Technology Co., Ltd.

- JM Catalysts

- Tokuyama Corporation

- ICI Devoe

- JGC Catalysts and Chemicals Ltd.

- Norsk Hydro

- NatureWorks LLC

- ArticZymes Technologies

Frequently Asked Questions

Asia Pacific region is expected to dominate the Methanol Catalyst Market over the forecast period.

The market size of the Methanol Catalyst Market is expected to reach USD 8.64 Bn by 2032.

The major key players in the Methanol Catalyst Market are BASF SE, Haldor Topsoe A/S, Clariant AG, Johnson Matthey, W. R. Grace & Co.

Clean energy transition is expected to drive the Methanol Catalyst Market growth over the forecast period (2026-2032).

1. Methanol Catalyst Market: Research Methodology

2. Methanol Catalyst Market: Executive Summary

3. Methanol Catalyst Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Consolidation of the Market

4. Methanol Catalyst Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers by Region

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.7. PESTLE Analysis

4.8. Value Chain Analysis

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Methanol Catalyst Market Size and Forecast by Segments (by Value USD and Volume Units)

5.1. Methanol Catalyst Market Size and Forecast, by Type (2025-2032)

5.1.1. Platinum

5.1.2. Platinum Ruthenium Alloy

5.1.3. Other

5.2. Methanol Catalyst Market Size and Forecast, by Application (2025-2032)

5.2.1. Methanol Fuel Cell Catalyst

5.2.2. Hydrogen Fuel Cell Catalyst

5.2.3. Reformate Fuel Cell Catalyst

5.2.4. Other

5.3. Methanol Catalyst Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Methanol Catalyst Market Size and Forecast (by Value USD and Volume Units)

6.1. North America Methanol Catalyst Market Size and Forecast, by Type (2025-2032)

6.1.1. Platinum

6.1.2. Platinum Ruthenium Alloy

6.1.3. Other

6.2. North America Methanol Catalyst Market Size and Forecast, by Application (2025-2032)

6.2.1. Methanol Fuel Cell Catalyst

6.2.2. Hydrogen Fuel Cell Catalyst

6.2.3. Reformate Fuel Cell Catalyst

6.2.4. Other

6.3. North America Methanol Catalyst Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Methanol Catalyst Market Size and Forecast (by Value USD and Volume Units)

7.1. Europe Methanol Catalyst Market Size and Forecast, by Type (2025-2032)

7.1.1. Platinum

7.1.2. Platinum Ruthenium Alloy

7.1.3. Other

7.2. Europe Methanol Catalyst Market Size and Forecast, by Application (2025-2032)

7.2.1. Methanol Fuel Cell Catalyst

7.2.2. Hydrogen Fuel Cell Catalyst

7.2.3. Reformate Fuel Cell Catalyst

7.2.4. Other

7.3. Europe Methanol Catalyst Market Size and Forecast, by Country (2025-2032)

7.3.1. UK

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Methanol Catalyst Market Size and Forecast (by Value USD and Volume Units)

8.1. Asia Pacific Methanol Catalyst Market Size and Forecast, by Type (2025-2032)

8.1.1. Platinum

8.1.2. Platinum Ruthenium Alloy

8.1.3. Other

8.2. Asia Pacific Methanol Catalyst Market Size and Forecast, by Application (2025-2032)

8.2.1. Methanol Fuel Cell Catalyst

8.2.2. Hydrogen Fuel Cell Catalyst

8.2.3. Reformate Fuel Cell Catalyst

8.2.4. Other

8.3. Asia Pacific Methanol Catalyst Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Bangladesh

8.3.11. Pakistan

8.3.12. Rest of Asia Pacific

9. Middle East and Africa Methanol Catalyst Market Size and Forecast (by Value USD and Volume Units)

9.1. Middle East and Africa Methanol Catalyst Market Size and Forecast, by Type (2025-2032)

9.1.1. Platinum

9.1.2. Platinum Ruthenium Alloy

9.1.3. Other

9.2. Middle East and Africa Methanol Catalyst Market Size and Forecast, by Application (2025-2032)

9.2.1. Methanol Fuel Cell Catalyst

9.2.2. Hydrogen Fuel Cell Catalyst

9.2.3. Reformate Fuel Cell Catalyst

9.2.4. Other

9.3. Middle East and Africa Methanol Catalyst Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Egypt

9.3.4. Nigeria

9.3.5. Rest of ME&A

10. South America Methanol Catalyst Market Size and Forecast (by Value USD and Volume Units)

10.1. South America Methanol Catalyst Market Size and Forecast, by Type (2025-2032)

10.1.1. Platinum

10.1.2. Platinum Ruthenium Alloy

10.1.3. Other

10.2. South America Methanol Catalyst Market Size and Forecast, by Application (2025-2032)

10.2.1. Methanol Fuel Cell Catalyst

10.2.2. Hydrogen Fuel Cell Catalyst

10.2.3. Reformate Fuel Cell Catalyst

10.2.4. Other

10.3. South America Methanol Catalyst Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest of South America

11. Company Profile: Key players

11.1. BASF SE

11.1.1. Company Overview

11.1.2. Financial Overview

11.1.3. Business Portfolio

11.1.4. SWOT Analysis

11.1.5. Business Strategy

11.1.6. Recent Developments

11.2. Haldor Topsoe A/S

11.3. Clariant AG

11.4. Johnson Matthey

11.5. W. R. Grace & Co.

11.6. Synfuels China Technology Co., Ltd.

11.7. Albemarle Corporation

11.8. KBR, Inc.

11.9. Sinopec Catalyst Co., Ltd.

11.10. N.E. Chemcat Corporation

11.11. Mitsubishi Chemical Corporation

11.12. Lummus Technology

11.13. Sud-Chemie India Pvt. Ltd.

11.14. Axens

11.15. CRI Catalyst Company

11.16. Advanced Refining Technologies (ART)

11.17. Yonker Environmental Protection Co., Ltd.

11.18. Sinopec Shanghai Research Institute of Petrochemical Technology (SRIPT)

11.19. Zeochem AG

11.20. Süd-Chemie India Pvt. Ltd.

11.21. Evonik Industries AG

11.22. CNPC Jilin Chemical Group Corporation

11.23. Sichuan Tianyi Science & Technology Co., Ltd.

11.24. JM Catalysts

11.25. Tokuyama Corporation

11.26. ICI Devoe

11.27. JGC Catalysts and Chemicals Ltd.

11.28. Norsk Hydro

11.29. NatureWorks LLC

11.30. ArticZymes Technologies

12. Key Findings

13. Industry Recommendation