Laptop Market: Market Growth, Opportunity, Competitive Analysis, Replacement Cycles, AI Integration, and Supply Chain Realignment (2026-2032)

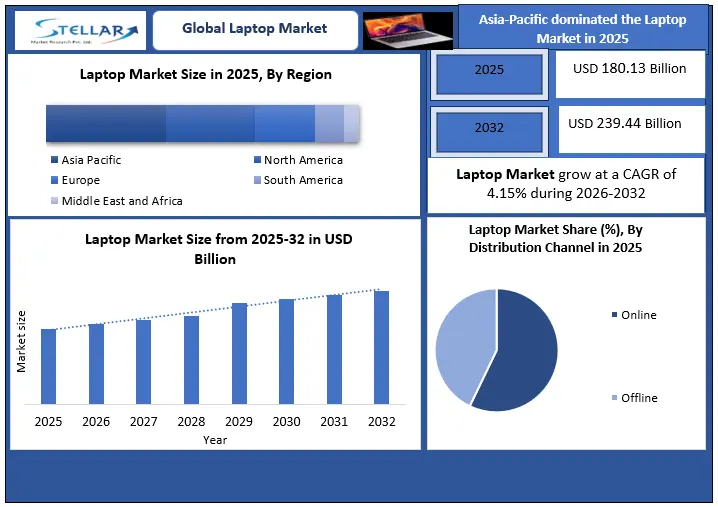

Laptop Market size was valued at USD 180.13 Bn. in 2025 and the total Laptop Market size is expected to grow at a CAGR of 4.15% from 2026 to 2032, reaching nearly USD 239.44 Bn. by 2032. The Global Laptop Industry is navigating a structurally mature demand environment, shaped by longer replacement cycles and a gradual transition toward AI-enabled personal computers, with Asia-Pacific remaining the primary production hub while demand growth shifts toward emerging markets.

Global Laptop Market Overview:

The Global Laptop Market represents the most commercially significant segment of the broader personal computer industry, accounting for over 73% of total global PC shipments. Laptop Market size was valued at USD 180.13 Bn. in 2025 and the total Laptop Market size is expected to grow at a CAGR of 4.15% from 2026 to 2032, reaching nearly USD 239.44 Bn. In 2025, global shipments of laptops reached approximately 187 million units, compared to total PC shipments of around XX million units, reinforcing laptops as the dominant computing form factor across consumer and commercial applications.

Laptop demand spans multiple use cases, including home computing, enterprise productivity, education, and gaming. While pandemic-era demand pulled forward volumes, the market has since normalized, with shipment volumes stabilizing in the 185–190-million-unit range. Despite volume moderation, value growth is supported by higher average selling prices driven by premium ultrabooks, gaming laptops, and early adoption of AI-capable devices.

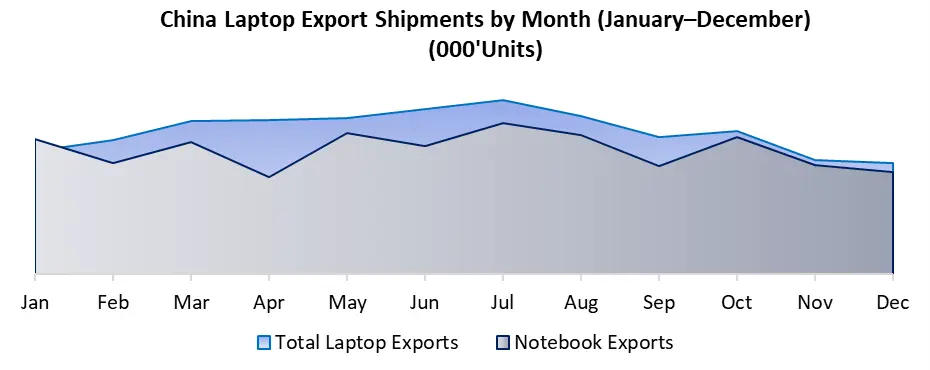

From a supply perspective, manufacturing remains highly concentrated in Asia. China continues to account for nearly 89% of global laptop production, though incremental diversification toward Vietnam, India, and Mexico is underway, primarily to mitigate geopolitical and tariff-related risks rather than to expand capacity.

Global Laptop Market Key Highlights

- Value over Volume: Despite modest shipment growth, the laptop market size (USD) continues to expand, supported by premium pricing, gaming laptops, and enterprise-grade devices.

- Supply Concentration: China remains the dominant exporter under key HS Code classifications, contributing nearly nine-tenths of global laptop exports, increasing systemic exposure to trade policy and logistics disruptions.

- AI Transition: AI-enabled laptops accounted for over 30% of global shipments in 2025, accelerating chipset upgrades and influencing enterprise procurement decisions.

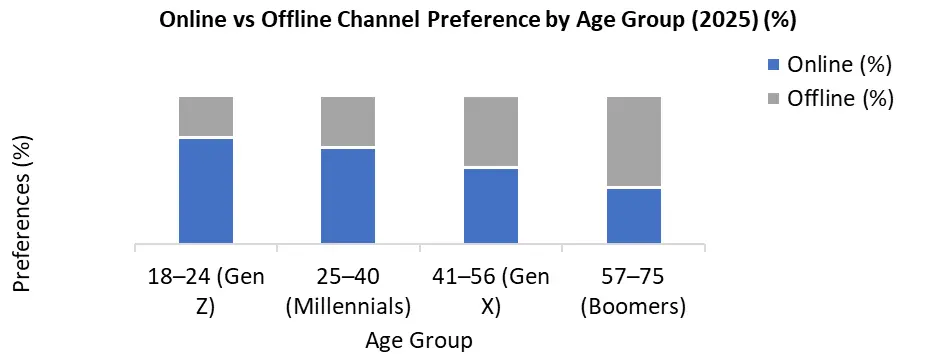

- Channel Shift: Online retail now represents over 55% of global laptop sales, reshaping pricing transparency and margin structures across OEMs and distributors.

- Competitive Intensity: The top five manufacturers control more than 52% of global shipments, reinforcing scale advantages in sourcing, pricing, and distribution.

- Shipment Stabilization: Global laptop shipments stabilized at around XX million units in 2025, following post-pandemic correction, with replacement-driven demand now defining market volumes.

To get more Insights: Request Free Sample Report

Laptop Market Dynamics

Adaptable Gadgets Driving Growth in the Laptop Market

The market has grown as a result of the adaptable gadgets that have been used in a variety of ways to suit different needs and preferences. These modes include laptop, tent, tablet, and stand mode. Thanks to their ability to switch between productivity and entertainment with ease, touchscreens, and detachable keyboards are popular options for people who multitask. The market has grown faster because laptop manufacturers still prioritize portability, emphasizing thin designs and long battery lives. This trend has led to technological advancements in the fields of large-capacity batteries, fast charging, and energy-efficient processors.

Users have taken advantage of extremely fast internet speeds and constant connectivity while on the go as 5G connectivity integration into laptops gains momentum. There is a strong demand for laptops as it has eliminated the need to use Wi-Fi hotspots or tether to a smartphone to provide quick access to cloud services, streaming, and collaboration tools. The purpose of laptops is to enable users to be more productive and stay connected virtually anywhere. The demand for notebooks has increased significantly, according to consumer electronics majors like HP, Apple, Lenovo, and Asus.

Challenges and Shifts in the Evolving Laptop Market

As consumer purchasing power has been undermined by inflation, there has been a recent decline in the number of PC and laptop owners as a result it has hindered market growth. The rise in mobile phones, which are without a doubt the most popular internet-using device across all generations, are overtaking PCs and laptops in the race for usage. The restricted availability of USB Type-C and Thunderbolt ports hinders the ability to directly connect external video devices, like projectors or monitors, as well as USB peripherals like storage devices, keyboards, and mice.

It has been difficult to guarantee compatibility with current peripherals that depend on different connection types because different laptops offer different configurations of Thunderbolt and USB Type-C ports. It is necessary to purchase laptop components from specific businesses, which has affected the total cost. Because these components are so important, the purchasing power of the makers of personal computers is limited compared to those of microprocessors (Intel and AMD) and graphics cards (NVidia and ATI). E. As oligopolies, the markets for CPUs and graphics cards have substantial negotiating power.

AI Integration and Innovation Driving the Future of the Laptop Market

Artificial intelligence (AI) integrated laptops are increasingly prevalent, enhancing user satisfaction and efficiency. Laptops equipped with AI features can enhance performance by analyzing usage patterns, enhance security with facial recognition, and extend battery life with smart power management. These clever characteristics offer ease and productivity, enhancing the user-friendliness and intuitiveness of laptops. The laptop sector has been constantly changing and adjusting to meet various preferences and needs.

Users have a variety of options available to help them find the ideal laptop, including gaming PCs, hybrid laptops, ultrabooks, and always-connected devices. The latest trends in manufacturing focus on creating devices that are smarter and more efficient, with a priority on sustainability, portability, and performance. Foreseeing progress in 5G connectivity, AI integration, and environmentally friendly design is prudent.

Laptop Market Segment Analysis

Laptop Market Size by End Use: Consumer vs Commercial

The consumer segment accounted for approximately 62% of global laptop shipments in 2025, driven by home computing, education, and gaming demand. However, average selling prices remain lower than in commercial channels, limiting value contribution. The commercial segment, including enterprise, government, and institutional buyers, represented 36% of shipments, but contributed over 45% of total laptop market revenue due to higher configuration standards, bulk procurement contracts, and bundled services. Enterprise refresh cycles are typically 36–48 months, providing shipment visibility despite broader market volatility.

Laptop Market size by Distribution Channel: Online vs Offline

Online sales channels accounted for approximately 55% of global laptop unit sales in 2025, translating to 105million units, supported by e-commerce platforms, brand-direct websites, and marketplace-led discounting strategies. Offline channels, including specialty electronics retailers, brand outlets, and system integrators, accounted for the remaining 44% of shipments. While declining in volume share, offline channels continue to dominate enterprise procurement and premium device sales above USD 1,200, where configuration support and after-sales services influence purchasing decisions.

Laptop Market Regional Analysis

Asia-Pacific accounted 44% of global laptop shipments in 2025, supported by strong demand from China, India, and Southeast Asia. The re7gion also serves as the primary manufacturing base, with China alone responsible for nearly 89% of global laptop exports under relevant HS Code classifications. North America represented around 25% of global shipments, but contributed over XX% of global laptop market revenue, reflecting higher average selling prices and strong penetration of premium and enterprise-grade devices.

Europe accounted for nearly 40 million units, with demand constrained by market saturation and elongated replacement cycles. However, Western Europe continues to support value growth through business laptops and regulatory-driven refreshes related to energy efficiency standards.

Laptop Market Competitive Landscape

The competitive landscape of the Global Laptop Industry is moderately consolidated. The top five manufacturers accounted for nearly 50% of global laptop shipments in 2025.

Lenovo led the market with a shipment share of roughly 43 million units, supported by strong commercial and public-sector demand. HP followed with a share of 21%, maintaining leadership in North America and education-focused deployments. Dell accounted for a shipment of nearly 29–30 million units, with over 70% of volumes concentrated in the commercial segment. Apple held a shipment share of 10%, but captured over 20% of global laptop market revenue, driven by premium pricing and ecosystem lock-in. ASUS contributed 8% of global shipments with gaming laptops accounting for over 40% of its laptop revenues. Collectively, these consumer electronics majors shape pricing trends, technology adoption, and channel strategies across the global laptop industry. Competitive advantage is defined by shipment scale, sourcing leverage, and the ability to integrate technological advancements such as AI acceleration without materially inflating end-user prices.

|

Global Laptop Market Scope |

||

|

Market Size in 2025 |

USD 180.13 Bn. |

|

|

Market Size in 2032 |

USD 239.44 Bn. |

|

|

CAGR (2026-2032) |

4.15% |

|

|

Historic Data |

2020-2025 |

|

|

Base Year |

2025 |

|

|

Forecast Period |

2026-2032 |

|

|

Segments Analysis |

By Operating System Windows macOS Linux ChromeOS |

By Price Range Upto 500 USD 501 to USD 1000 USD 1001 to USD 1500 USD 1501 to USD 2000 Above USD 2001 |

|

By Type Notebook Ultrabook 2-in-1 Laptop Gaming Laptop Chromebook |

By Distribution Channel Online E-commerce websites Company websites Offline Multi-brand stores Departmental stores Specialty stores Others |

|

|

By Screen Size Upto 10.9" 11" to 12.9“ 13" to 14.9" 15.0" to 16.9" More than 17“ |

By End Use Personal Business Gaming Others |

|

Laptop Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Russia, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Thailand, Vietnam, Philippines, and Rest of APAC)

Middle East and Africa (South Africa, GCC, Nigeria, Egypt, Turkey, and Rest of ME&A)

South America (Brazil, Argentina, Colombia, Chile, Peru, and the Rest of South America)

Laptop Market Key Players

Frequently Asked Questions

Laptop substitute has restrained market growth.

The Market size was valued at USD 180.12 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 4.15 % from 2026 to 2032, reaching nearly USD 239.43 Billion.

The segments covered in the market report are by type, Screen Size and End Use.

1. Global Laptop Market: Research Methodology

2. Global Laptop Market Introduction

2.1. Market Size (2025) & Forecast (2026-2032)

2.2. Market Size (USD) and Market Share (%) - By Segments, Regions and Country

2.3. Executive Summary

3. Global Laptop Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Product Portfolio

3.3.3. Distribution Channel Reach

3.3.4. After Sales and Service Support

3.3.5. Assembly Localization Initiatives

3.3.6. Technology and Innovations

3.3.7. New Product Launch Frequency

3.3.8. Marketing And Advertising Initiatives

3.3.9. Market Share (%)

3.3.10. Revenue (2025)

3.3.11. R&D Investment

3.3.12. Revenue Growth Rate (%)

3.3.13. Geographical Presence

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

3.6. Recent Developments

3.7. Market Positioning & Share Analysis

3.7.1. Company Revenue, Laptop Revenue, and Market Share (%)

3.7.2. SMR Competitive Positioning

3.8. Strategic Developments & Partnerships

4. Laptop Market: Dynamics

4.1. Laptop Market Trends

4.2. Laptop Market Dynamics

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

5. Laptop Pricing and Distribution Analysis (2025)

5.1. Laptop Price Trends by Brand Tier and Screen Size (2020–2025)

5.2. Price Band Share across Entry, Mid-range, and Premium Segments

5.3. Distribution Channel Mix and Geographic Reach

5.4. Online Sales Dynamics including Marketplaces and Brand D2C

5.5. Offline Retail Structure across Format and Store Type

6. Laptop Market Consumer Insights and Buying Behavior

6.1. Buyer Segmentation by Use Case and End User Type

6.2. Key Purchase Decision Drivers and Trade-offs

6.3. Channel Preference and Purchase Journey Flow

6.4. Brand Switching Behavior and Loyalty Patterns

6.5. Impact of Seasonality, Sales Events, and Promotions

7. Laptop Market Brand and Competitive Analysis

7.1. Market Share by Brand in Value and Volume Terms

7.2. Competitive Positioning by Price Band and Specifications

7.3. Go-to-market Strategies and Promotional Intensity

7.4. After-sales Coverage and Service Network Strength

7.5. Brand Perception and Customer Satisfaction Indicators

8. Laptop Market Technology and Product Innovation

8.1. Hardware Specification Evolution across Price Segments

8.2. Battery, Display, and Thermal Performance Trends

8.3. AI Features, Security Capabilities, and Software Integration

8.4. Form Factor Shifts and Emerging Product Categories

8.5. Sustainability, Repairability, and Product Longevity

9. Laptop Market Production and Local Assembly Landscape

9.1. Import Dependence versus Local Assembly Share

9.2. Role of PLI-driven Manufacturing and Contract Assemblers

9.3. Cost Structure and Infrastructure Readiness

9.4. Policy Incentives and Regulatory Environment

10. Laptop Market Structure by Specification and Usage

10.1. Operating System Penetration and Adoption Trends

10.2. Device Type Mix by Form Factor and Performance Class

10.3. Screen Size Preferences and Replacement Cycles

10.4. Price Sensitivity by Income Group and City Tier

10.5. End-use Adoption across Personal, Education, and Enterprise

11. Laptop Market: Role of Second-hand and Refurbished Devices

11.1. Share of Refurbished and Pre-owned Laptops in Total Volume

11.2. Demand Drivers and Core Buyer Segments

11.3. Pricing Gaps and Value Perception versus New Devices

11.4. Sales Channels and Refurbishment Ecosystem

11.5. Impact on New Device Sales and Upgrade Cycles

12. Laptop Market Enterprise and Commercial Laptop Market Analysis

12.1. Corporate Refresh Cycles and Procurement Models

12.2. Leasing, Managed IT, and Device-as-a-Service Adoption

12.3. SME versus Large Enterprise Buying Behavior

12.4. Role of System Integrators and B2B Channel Partners

12.5. Enterprise-specific Feature and Security Requirements

13. Regional and City-tier Demand Analysis

13.1. Urban versus Semi-urban Usage Patterns

13.2. Regional Pricing Variation and Channel Mix

13.3. Infrastructure Constraints and Connectivity Impact

13.4. Regional Growth Hotspots and Expansion Potential

14. Global Laptop Market: Size and Forecast by Segmentation (By Value USD Billion and Volume 000’Units) (2025-2032)

14.1. Global Laptop Market Size and Forecast, By Operating System

14.1.1. Windows

14.1.2. macOS

14.1.3. Linux

14.1.4. ChromeOS

14.2. Global Laptop Market Size and Forecast, By Type

14.2.1. Notebook

14.2.2. Ultrabook

14.2.3. 2-in-1 Laptop

14.2.4. Gaming Laptop

14.2.5. Chromebook

14.3. Global Laptop Market Size and Forecast, By Screen Size

14.3.1. Upto 10.9"

14.3.2. 11" to 12.9“

14.3.3. 13" to 14.9"

14.3.4. 15.0" to 16.9"

14.3.5. More than 17“

14.4. Global Laptop Market Size and Forecast, By Price Range

14.4.1. Upto 500

14.4.2. USD 501 to USD 1000

14.4.3. USD 1001 to USD 1500

14.4.4. USD 1501 to USD 2000

14.4.5. Above USD 2001

14.5. Global Laptop Market Size and Forecast, By Distribution Channel

14.5.1. Online

14.5.1.1. E-commerce websites

14.5.1.2. Company websites

14.5.2. Offline

14.5.2.1. Multi-brand stores

14.5.2.2. Departmental stores

14.5.2.3. Specialty stores

14.5.2.4. Others

14.6. Global Laptop Market Size and Forecast, By End Use

14.6.1. Personal

14.6.2. Business

14.6.3. Gaming

14.6.4. Others

14.7. Global Laptop Market Size and Forecast, By Region

14.7.1. North America

14.7.2. Europe

14.7.3. Asia Pacific

14.7.4. Middle East and Africa

14.7.5. South America

15. North America Laptop Market Size and Forecast By Segmentation (By Value USD Billion and Volume 000’Units) (2025-2032)

15.1. North America Market Size and Forecast, By Operating System

15.2. North America Market Size and Forecast, By Type

15.3. North America Market Size and Forecast, By Screen Size

15.4. North America Market Size and Forecast, By Price Range

15.5. North America Market Size and Forecast, By Distribution Channel

15.6. North America Market Size and Forecast, By End Use

15.7. North America Market Size and Forecast, By Country

15.7.1. United States

15.7.2. Canada

15.7.3. Mexico

16. Europe Laptop Market Size and Forecast By Segmentation (By Value USD Billion and Volume 000’Units) (2025-2032)

16.1. Europe Market Size and Forecast, By Operating System

16.2. Europe Market Size and Forecast, By Type

16.3. Europe Market Size and Forecast, By Screen Size

16.4. Europe Market Size and Forecast, By Price Range

16.5. Europe Market Size and Forecast, By Distribution Channel

16.6. Europe Market Size and Forecast, By End Use

16.7. Europe Market Size and Forecast, By Country

16.7.1. United Kingdom

16.7.2. France

16.7.3. Germany

16.7.4. Italy

16.7.5. Spain

16.7.6. Sweden

16.7.7. Russia

16.7.8. Rest of Europe

17. Asia Pacific Laptop Market Size and Forecast by Segmentation (By Value USD Billion and Volume 000’Units) (2025-2032)

17.1. Asia Pacific Market Size and Forecast, By Operating System

17.2. Asia Pacific Market Size and Forecast, By Type

17.3. Asia Pacific Market Size and Forecast, By Screen Size

17.4. Asia Pacific Market Size and Forecast, By Price Range

17.5. Asia Pacific Market Size and Forecast, By Distribution Channel

17.6. Asia Pacific Market Size and Forecast, By End Use

17.7. Asia Pacific Market Size and Forecast, By Country

17.7.1. China

17.7.2. Japan

17.7.3. South Korea

17.7.4. India

17.7.5. Australia

17.7.6. Malaysia

17.7.7. Thailand

17.7.8. Vietnam

17.7.9. Indonesia

17.7.10. Philippines

17.7.11. Rest of Asia Pacific

18. Middle East and Africa Laptop Market Size and Forecast By Segmentation (By Value USD Billion and Volume 000’Units) (2025-2032)

18.1. Middle East and Africa Market Size and Forecast, By Operating System

18.2. Middle East and Africa Market Size and Forecast, By Type

18.3. Middle East and Africa Market Size and Forecast, By Screen Size

18.4. Middle East and Africa Market Size and Forecast, By Price Range

18.5. Middle East and Africa Market Size and Forecast, By Distribution Channel

18.6. Middle East and Africa Market Size and Forecast, By End Use

18.7. Middle East and Africa Market Size and Forecast, By Country

18.7.1. South Africa

18.7.2. GCC

18.7.3. Nigeria

18.7.4. Egypt

18.7.5. Turkey

18.7.6. Rest of ME&A

19. South America Laptop Market Size and Forecast By Segmentation (By Value USD Billion and Volume 000’Units) (2025-2032)

19.1. South America Market Size and Forecast, By Operating System

19.2. South America Market Size and Forecast, By Type

19.3. South America Market Size and Forecast, By Finish

19.4. South America Market Size and Forecast, By Price Range

19.5. South America Market Size and Forecast, By Distribution Channel

19.6. South America Market Size and Forecast, By End Use

19.7. South America Market Size and Forecast, By Country

19.7.1. Brazil

19.7.2. Argentina

19.7.3. Colombia

19.7.4. Chile

19.7.5. Rest Of South America

20. Company Profile: Key Players

20.1. Lenovo

20.1.1. Company Overview

20.1.2. Business Portfolio

20.1.3. Financial Overview

20.1.4. SWOT Analysis

20.1.5. Strategic Analysis

20.1.6. Recent Developments

20.2. HP

20.3. Dell

20.4. Apple

20.5. ASUS

20.6. Acer

20.7. Microsoft

20.8. Samsung

20.9. Huawei

20.10. MSI

20.11. Razer

20.12. Toshiba

20.13. Fujitsu

20.14. Panasonic

20.15. LG

20.16. Sony

20.17. Alienware

20.18. Gigabyte

20.19. Schenker

20.20. HCL

20.21. Xiaomi

20.22. Honor

20.23. Chuwi

20.24. Teclast

20.25. Jumper

20.26. Framework

20.27. System76

20.28. Pine64

20.29. Purism

20.30. Quanta

21. Laptop Market Key Findings

22. Industry Recommendations