Lager Market Industry Analysis and Forecast (2026-2032)

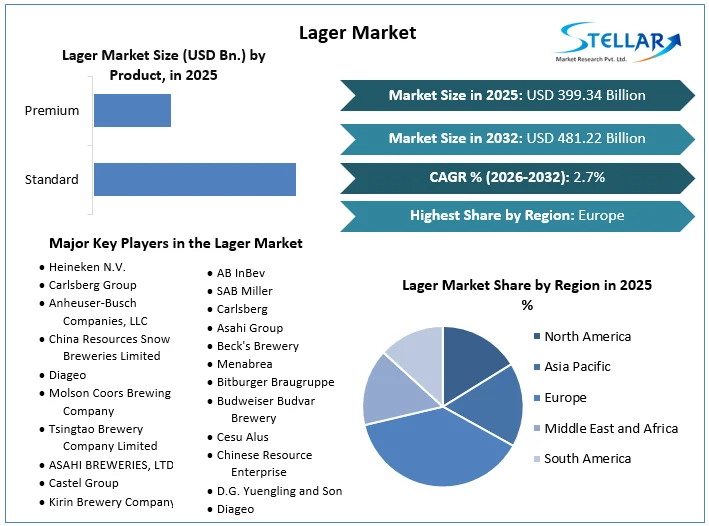

The Lager Market size was valued at USD 399.34 Bn. in 2025 and the total Global Lager revenue is expected to grow at a CAGR of 2.70% from 2026 to 2032, reaching nearly USD 481.22 Bn. by 2032.

Lager Market Overview

Lager is a type of beer that is fermented and conditioned at low temperatures. It originated in central Europe and is known for its clean, crisp taste. The SMR report provides a comprehensive analysis of key trends, market drivers, challenges, and opportunities shaping the global lager industry. Breweries are responding to health-conscious consumer demands with new offerings like non-alcoholic and low-alcohol lagers, growing market penetration and accessibility. Simultaneously, the rise in consumer interest in premium and craft lagers is enhancing market value and profitability. The shift underscores a preference for higher-quality, artisanal brews that provide evolving tastes and preferences in the competitive beer landscape.

As breweries innovate and diversify their product lines, they capitalize on these trends to capture broader market segments and sustain growth in the dynamic lager market. Assisting breweries in innovating new flavors, sustainable packaging, and health-focused products is crucial to meeting changing consumer preferences. By aligning with trends toward healthier lifestyles and environmental consciousness, breweries enhance market relevance and appeal. Additionally, expanding distribution networks and entering emerging markets represent strategic opportunities to capitalize on increasing consumer bases.

The approach not only facilitates broader product accessibility but also positions breweries to leverage growing Lager market demand in regions where beer consumption is increasing. By combining innovation with strategic expansion efforts, breweries effectively navigate competitive pressures and sustain long-term growth in the global beer industry.

- India exported 5,040 shipments of Lager beer, making it the third-largest exporter globally. The primary destinations for Indian Lager beer exports are the United States, the United Arab Emirates, and Oman. It underscores India's significant role in the global Lager beer market. The top exporters are the Netherlands with 16,943 shipments and Belgium with 6,214 shipments, indicating intense competition in the international beer trade. India’s export volume highlights its contribution to global beer industry dynamics, reflecting both market demand and competitive positioning among major exporting nations.

To get more Insights: Request Free Sample Report

Lager Market Dynamics

Rising Demand for Low-Alcohol, Non-Alcoholic, and Low-Calorie Lagers

The health and wellness trend is significantly influencing the lager market, with a growing consumer base seeking healthier beverage options. The change is informed by an increased consciousness of the effects of alcohol on personal health and preference for fitness in life. There is a growing demand for low-alcohol, non-alcoholic, and low-calorie lagers that define this trend. Breweries have come up with new brands such as Heineken 0.0 to produce low-alcohol, non-alcoholic, and low-calorie beers that are being well-received by consumers. Highlighting nature's contents while including vitamins attracts those who desire a good-health lifestyle.

These products are now found in supermarkets, and local shops or can be bought online all over the world as it has become a global phenomenon. The strategies of promotion are geared towards health branding to underscore the benefits that accrue from using these products thereby giving priority to younger generations such as the millennial generation and Generation Z who value wellness in association with change to new things. The broad distribution networks coupled with targeted marketing efforts have resulted in increasing sales of healthy beer alternatives around the globe.

- According to SMR Analysis, it indicates that 47% of global consumers were trying to reduce their alcohol intake, with 66% of those respondents indicating an interest in non-alcoholic alternatives.

Increasing Health Consciousness Leading to a Decline in Traditional Lager Consumption

The continuously growing health consciousness of consumers is indeed changing completely the lager market. Consumers are wiser about the health implications of their drinks and are in search of healthier alternatives to the drinks. The development has a current effect on the old types of lagers, which are allegedly less healthy since they have higher alcohol as well as calorie contents. Breweries are innovating by offering healthier options like low-alcohol, non-alcoholic, and low-calorie lagers.

Heineken 0.0, a non-alcoholic beer, exemplifies this trend, with Heineken's 2021 annual report showing a 29% global volume growth in 2020. These products are increasingly available in supermarkets, convenience stores, and online platforms, reflecting strong consumer demand. For instance, the availability of non-alcoholic beer in the United States rose by 38% from 2018 to 2023, according to SMR Analysis. Its increased availability indicates the growing acceptance and Lager market penetration of healthier lager alternatives.

Lager Market Segment Analysis

By Product, Standard lager holds a substantial portion of the Lager market, appealing widely because of its affordability and familiar taste profile. The standard lager segment exerts a profound influence on the beer market, primarily targeting budget-conscious consumers seeking a straightforward and refreshing beer experience at an accessible price point. These lagers enjoy widespread availability in supermarkets, convenience stores, and bars, which contributes to their dominance in terms of volume sales. Their affordability and consistent demand provide breweries with a stable revenue stream, bolstering overall market stability even amidst fluctuating consumer preferences.

Despite the competitive landscape, characterized by numerous brands vying for Lager market share, standard lagers maintain their stronghold due to breweries' focus on cost-efficiency and scalability. The segment remains highly competitive yet essential, as breweries strive to meet the mass Lager market demand for economical and reliable beer choices. Consumer preference for standard lagers remains robust across a broad demographic, ensuring their enduring popularity despite the growing interest in premium and craft beers.

Lager Market Regional Insights

Europe has a rich brewing tradition and remains a crucial region for the lager market. The market in Europe is influenced by diverse consumer preferences, strong competition, and regulatory environments. The non-alcoholic beer experienced notable growth, with sales increasing by 9% in 2025, led prominently by Germany. The trend underscores a rising consumer preference for healthier beverage options. Also, European breweries are enhancing sustainability efforts. For instance, Carlsberg introduced the "Snap Pack" packaging, reducing plastic usage by up to 76%. These initiatives reflect a broader industry shift towards environmental responsibility and resonate with consumers increasingly prioritizing sustainability in their purchasing decisions.

Germany is the most dominant country in the European lager market. It has a long-standing brewing heritage and is home to some of the world's largest and most renowned breweries. According to SMR Analysis, Germany accounted for approximately 25% of Europe's total beer production in 2021, underscoring its significant influence in the region. European governments are actively promoting responsible drinking through health campaigns.

In the UK, initiatives like the "Drinkaware" campaign educate consumers on alcohol consumption's impacts. Also, several European countries incentivize small and independent breweries with tax incentives and subsidies. Germany's Beer Duty Law, for instance, offers tax relief to small brewers, fostering the growth of craft beer production. These governmental supports aim to balance consumer education on responsible alcohol use while nurturing the diversity and sustainability of the Lager industry across Europe.

Lager Market Competitive Landscape

Breweries like Heineken with Heineken 0.0 and AB InBev with Budweiser Zero have tapped into the rising demand for healthier beverage options by introducing non-alcoholic and low-alcohol variants. These products cater to health-conscious consumers, expanding choices and attracting a demographic focused on wellness. Meanwhile, craft breweries are innovating with new flavors and styles, challenging traditional lager perceptions and appealing to enthusiasts seeking premium and artisanal experiences. New product launches in the lager market bring diversity, catering to diverse consumer tastes and preferences.

They create competitive pressure among breweries to innovate continuously, driving improvements in product quality and marketing strategies. These innovations not only expand consumer choice but also stimulate Lager market growth by attracting new demographics and increasing consumption occasions. Particularly, the introduction of non-alcoholic and premium variants has been instrumental in broadening Lager market demand, responding effectively to evolving consumer preferences for healthier options and higher-quality drinking experiences.

- In September 2022, United Breweries Holdings Limited launched Heineken Silver, a new addition to its beer lineup, marking the brand's latest entry into the burgeoning premium segment.

- In July 2021, Heineken N.V., a multinational brewing company from the Netherlands, announced its successful acquisition of controlling interest in United Breweries Limited (UBL) during UBL's Annual General Meeting in India.

- In February 2022, Molson Coors Beverage Company introduced Madri Exceptional Lager in UK superstores as part of its strategy to build a consumer following in the region.

|

Lager Market Scope |

|

|

Market Size in 2025 |

USD 399.34 Bn. |

|

Market Size in 2032 |

USD 481.22 Bn. |

|

CAGR (2026-2032) |

2.70% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Product Standard Premium |

|

By Distribution Channel On-trade Off-trade |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Lager Market

- Heineken N.V.

- Carlsberg Group

- Anheuser-Busch Companies, LLC

- China Resources Snow Breweries Limited

- Diageo

- Molson Coors Brewing Company

- Tsingtao Brewery Company Limited

- ASAHI BREWERIES, LTD.

- Castel Group

- Kirin Brewery Company.

- AB InBev

- SAB Miller

- Carlsberg

- Asahi Group

- Beck's Brewery

- Menabrea

- Bitburger Braugruppe

- Budweiser Budvar Brewery

- Cesu Alus

- Chinese Resource Enterprise

- D.G. Yuengling and Son

- Diageo

- Forst

- Grupo Modelo

Frequently Asked Questions

Breweries differentiate through product innovation, branding strategies emphasizing quality and heritage, collaborations with local suppliers, and direct-to-consumer sales channels.

The lager market contributes significantly to global economies through employment in brewing and distribution sectors, export revenues, and tourism related to beer festivals and brewery tours.

The Market size was valued at USD 399.34 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 2.70% from 2026 to 2032, reaching nearly 481.22 billion.

The segments covered in the market report are by Product and Distribution Channel.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Lager Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Lager Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

4. Lager Market: Dynamics

4.1. Lager Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Lager Market Drivers

4.3. Lager Market Restraints

4.4. Lager Market Opportunities

4.5. Lager Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Trade Analysis

4.11. Regulatory Landscape

4.11.1. Market Regulation by Region

4.11.1.1. North America

4.11.1.2. Europe

4.11.1.3. Asia Pacific

4.11.1.4. Middle East and Africa

4.11.1.5. South America

4.11.2. Impact of Regulations on Market Dynamics

4.11.3. Government Schemes and Initiatives

5. Lager Market: Global Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Litres) (2025-2032)

5.1. Lager Market Size and Forecast, by Product (2025-2032)

5.1.1. Standard

5.1.2. Premium

5.2. Lager Market Size and Forecast, by Distribution Channel (2025-2032)

5.2.1. On-trade

5.2.2. Off-trade

5.3. Lager Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Lager Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Litres) (2025-2032)

6.1. North America Lager Market Size and Forecast, by Product (2025-2032)

6.1.1. Standard

6.1.2. Premium

6.2. North America Lager Market Size and Forecast, by Distribution Channel (2025-2032)

6.2.1. On-trade

6.2.2. Off-trade

6.3. North America Lager Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Lager Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Litres) (2025-2032)

7.1. Europe Lager Market Size and Forecast, by Product (2025-2032)

7.2. Europe Lager Market Size and Forecast, by Distribution Channel (2025-2032)

7.3. Europe Lager Market Size and Forecast, by Country (2025-2032)

7.3.1. United Kingdom

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Russia

7.3.8. Rest of Europe

8. Asia Pacific Lager Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Litres) (2025-2032)

8.1. Asia Pacific Lager Market Size and Forecast, by Product (2025-2032)

8.2. Asia Pacific Lager Market Size and Forecast, by Distribution Channel (2025-2032)

8.3. Asia Pacific Lager Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. India

8.3.3. Japan

8.3.4. South Korea

8.3.5. Australia

8.3.6. ASEAN

8.3.7. Rest of Asia Pacific

9. Middle East and Africa Lager Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Litres) (2025-2032)

9.1. Middle East and Africa Lager Market Size and Forecast, by Product (2025-2032)

9.2. Middle East and Africa Lager Market Size and Forecast, by Distribution Channel (2025-2032)

9.3. Middle East and Africa Lager Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Egypt

9.3.4. Rest of the Middle East and Africa

10. South America Lager Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Litres) (2025-2032)

10.1. South America Lager Market Size and Forecast, by Product (2025-2032)

10.2. South America Lager Market Size and Forecast, by Distribution Channel (2025-2032)

10.3. South America Lager Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest Of South America

11. Company Profile: Key Players

11.1. Heineken N.V.

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc.)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Carlsberg Group

11.3. Anheuser-Busch Companies, LLC

11.4. China Resources Snow Breweries Limited

11.5. Diageo

11.6. Molson Coors Brewing Company

11.7. Tsingtao Brewery Company Limited

11.8. ASAHI BREWERIES, LTD.

11.9. Castel Group

11.10. Kirin Brewery Company.

11.11. AB InBev

11.12. SAB Miller

11.13. Carlsberg

11.14. Asahi Group

11.15. Beck's Brewery

11.16. Menabrea

11.17. Bitburger Braugruppe

11.18. Budweiser Budvar Brewery

11.19. Cesu Alus

11.20. Chinese Resource Enterprise

11.21. D.G. Yuengling and Son

11.22. Diageo

11.23. Forst

11.24. Grupo Modelo

11.25. XXX Inc.

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook